Beef Wrap September 9

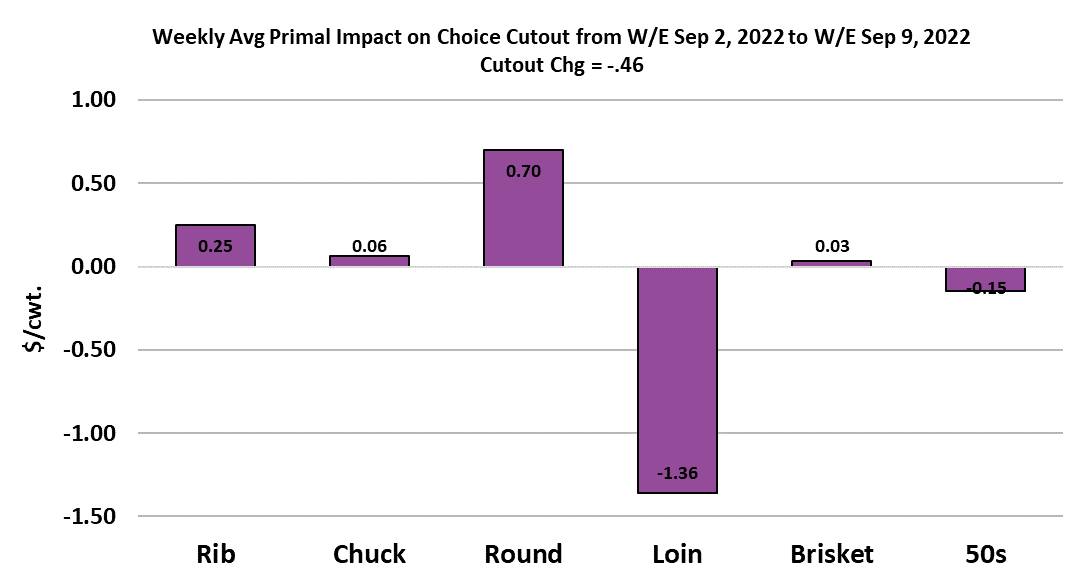

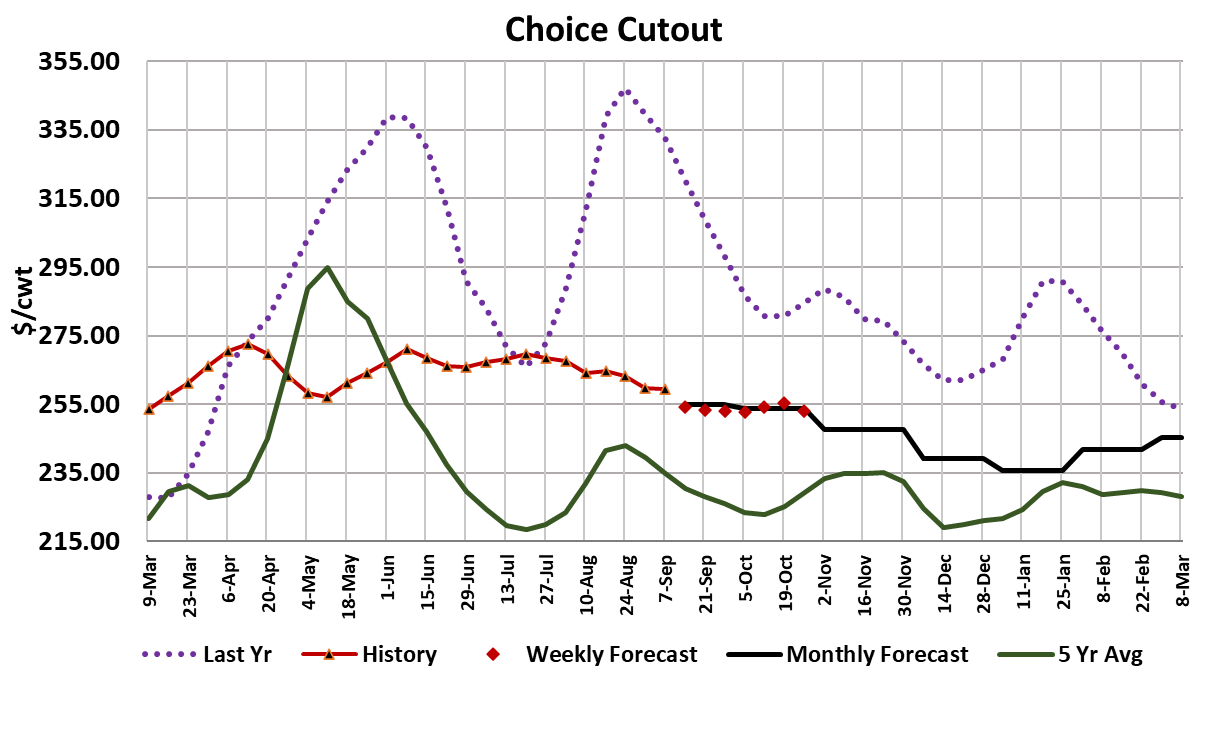

Once again, it was “steady as she goes” in the cattle and beef

complex. The Choice cutout lost only $0.46/cwt. this week and

the Select was down $2.17/cwt. The cash cattle market

averaged about $0.50/cwt. below last week’s average. The

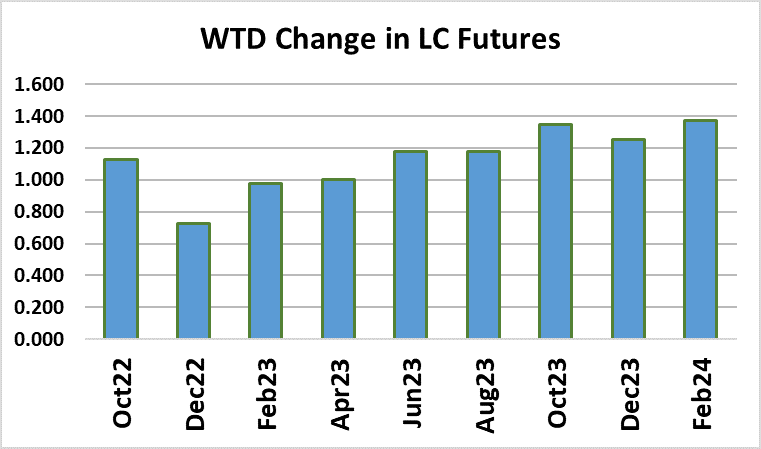

futures market moved about $1 higher on the week, with all of

that coming on Friday once market participants recognized that

packers were paying just a little more for those late clean-up

cattle purchases. Most of the softness in the Choice cutout was

driven by the loin primal, while the round gave the most support.

It was a little surprising that the recent small kills didn’t help the

cutout this week and that could be an ominous sign for next week

when much bigger production needs to clear the system. This

week’s fed slaughter is estimated at only 478k, down about 20k

from the week before and well below the 520-530k range that

was prevalent before the holiday.

I expect that packers will throttle back up to 530k next week. The

Saturday kill was quite large at 92k, of which about 80k was

steers and heifers. We should have a couple more weeks of

really big steer and heifer slaughter before kills start to taper

down near the beginning of October. Based on past placement

patterns, I’d look for weekly fed kills during October to average

around 500k per week, which is a pretty big drop from today’s

level and thus beef availability is likely to tighten up moving into

Q4. That may or may not mean higher cutouts, since there is a

chance that beef demand will be softer that what we saw in late

summer. Packer margins improved about $20/head this week to

average $189, as last week’s cheaper cattle purchases helped

the bottom line.

My forecast has the cutouts easing a little more next week as

larger production weighs on the market. The combined margin

made a little turn higher this week, but I am reluctant to call this a

bottom. If it is a bottom, it is happening at a higher level than has

characterized other recent bottoms. It could just be a head-fake

and next week’s combined margin could continue lower. Now

that summer is behind us and the kids are all back in school, the

post-COVID party atmosphere is done and it will be interesting to

see if beef demand erodes as a result. Some of the macro

variables got a little better this week as gas prices continued to

fall and the stock market posted a positive week. In the Southern

US, gas prices below $3/gallon are becoming commonplace

again. That will please all of the pickup truck and SUV drivers.

Will they spend their gas savings on a nice juicy steak to

celebrate?

I doubt it, but a little extra change in consumer’s pockets

certainly won’t hurt demand. We should look for middle meat

demand to improve in October and November, and much of that

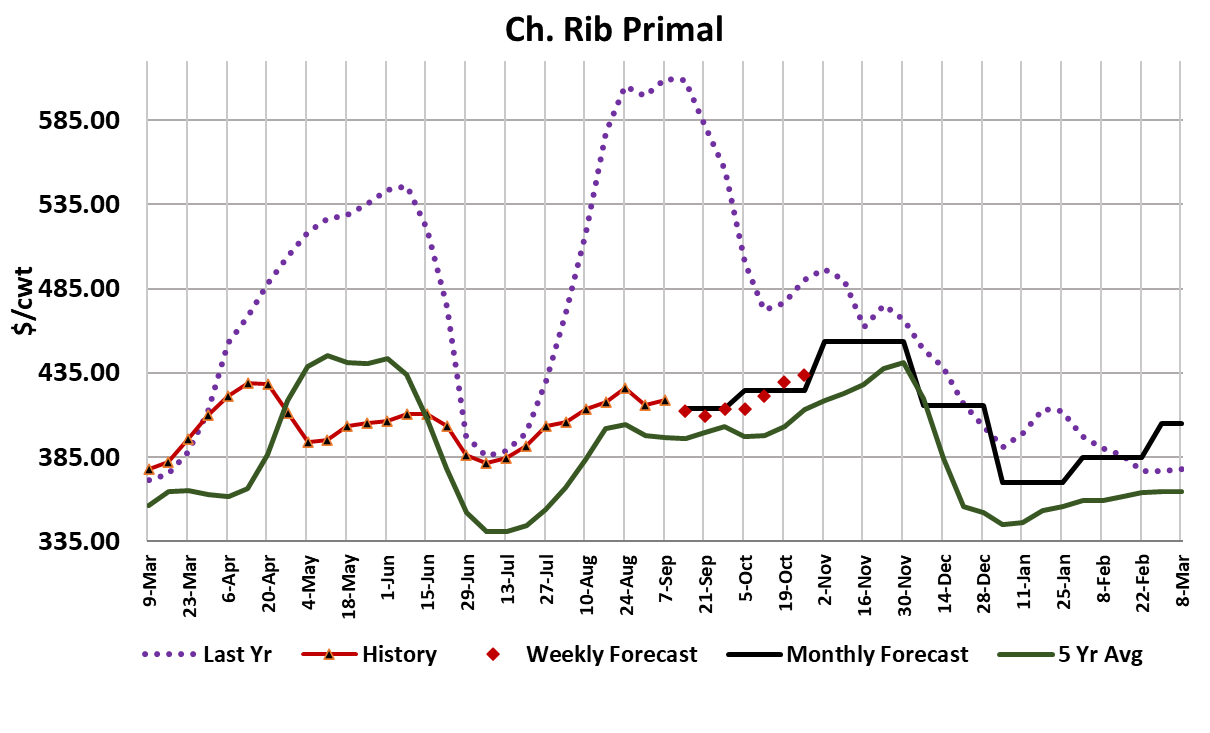

will be centered on the ribeyes and tenderloins. It’s not a given,

however. Recall that last year rib prices moved lower right

through the fall and didn’t really exhibit much of a holidayinduced demand bump. We often see better end meat demand

heading into October and that should be the case this year, but I

expect that the price gains will be moderate at best. Trimmings

markets likely work a little lower as demand through QSR

channels should be softer as fall begins. Actually, the safest,

and easiest, forecast would be just to call everything flat for the

next month or two. That is pretty much they way most items

traded throughout the summer.

The current forecast has the Choice cutout down in the low

$250s by the end of October. At that point in time I’d expect

cash cattle to be in the low $140s—not far different from today’s

pricing. Futures traders are more optimistic than that, with the

Oct contract settling near $146 this week. ERS released the

trade data for July this week and it showed total beef exports up

3.2% YOY and down 2.5% from June. Export volumes are

running above recent years at a time when US price levels are

also stronger than in years’ past, so that provides pretty strong

evidence that international demand for US beef is healthy. I

think we will see some modest softening of exports in Q4 from

current levels, but they could still be at, or slightly above, last

year. USDA still hasn’t repaired their weekly export reporting

system, so we remain in the dark about current export activity.

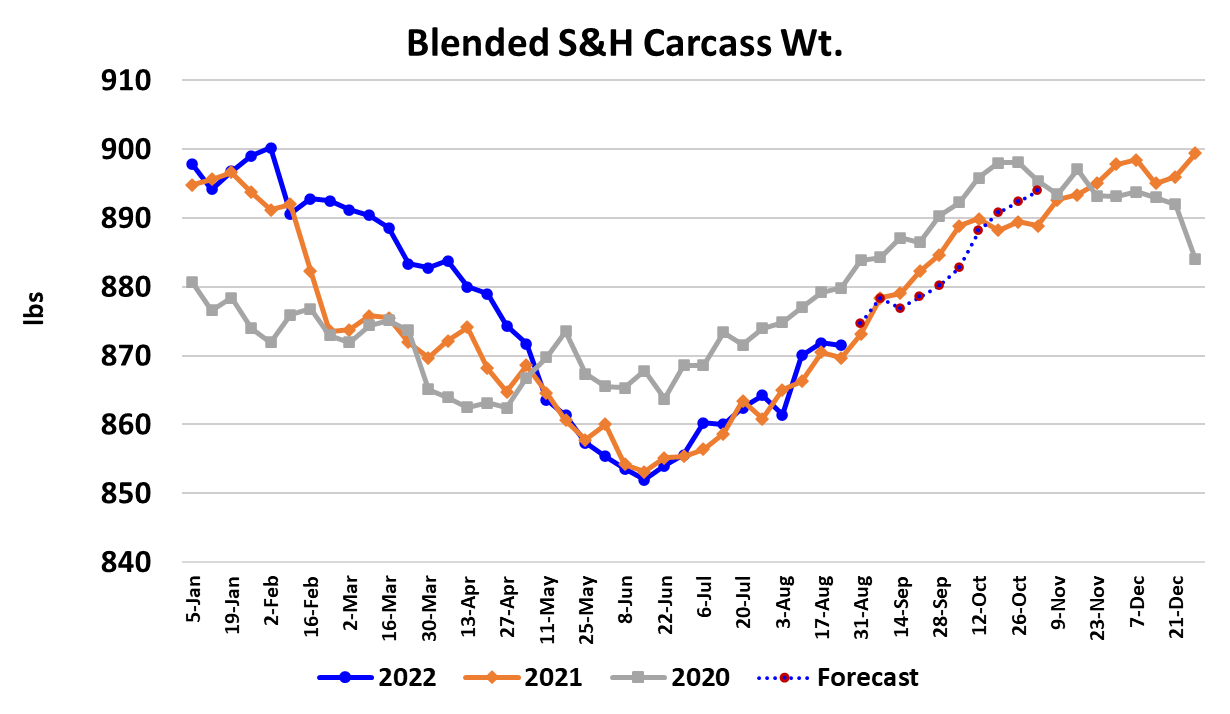

Steer carcass weights were unchanged this week at 904, and

have been slow to rise coming out of summer. The DTDS

weights remain at stubbornly low levels and that keeps me

thinking that feedyards are not backlogging any cattle at present.

Kills have just been too strong for that to happen. We should

see stronger weight increases in the next couple of FI data

releases because they will cover the recent holiday-reduced

kills. It is hard to imagine cash cattle prices slipping too much

given how bullish the weight picture looks. Next week watch the

cutouts to see how they perform under the weight of bigger

production. If they hold steady or advance, then that would be a

positive demand sign. More likely, the cutouts slide lower and

put pressure on packers to get cattle bought cheaper next week.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}