Beef Wrap September 2

The cash cattle market slipped lower again this week, averaging

$142.82, down almost $2 from the week before. That decline was

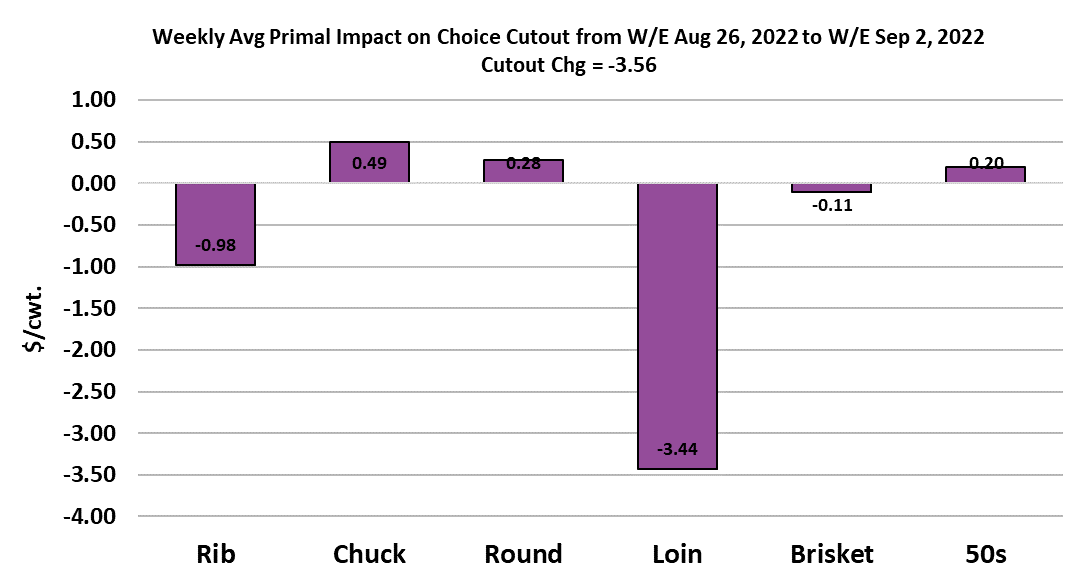

accompanied by further softness in the cutouts, with the Choice

dropping $3.56 to average $259.73 for the week, while the Select

was up $0.85 to average $239.07. However, the cutouts were

strengthening late in the week and stand a good chance of gaining

more early next week as packers will have less product to offer due

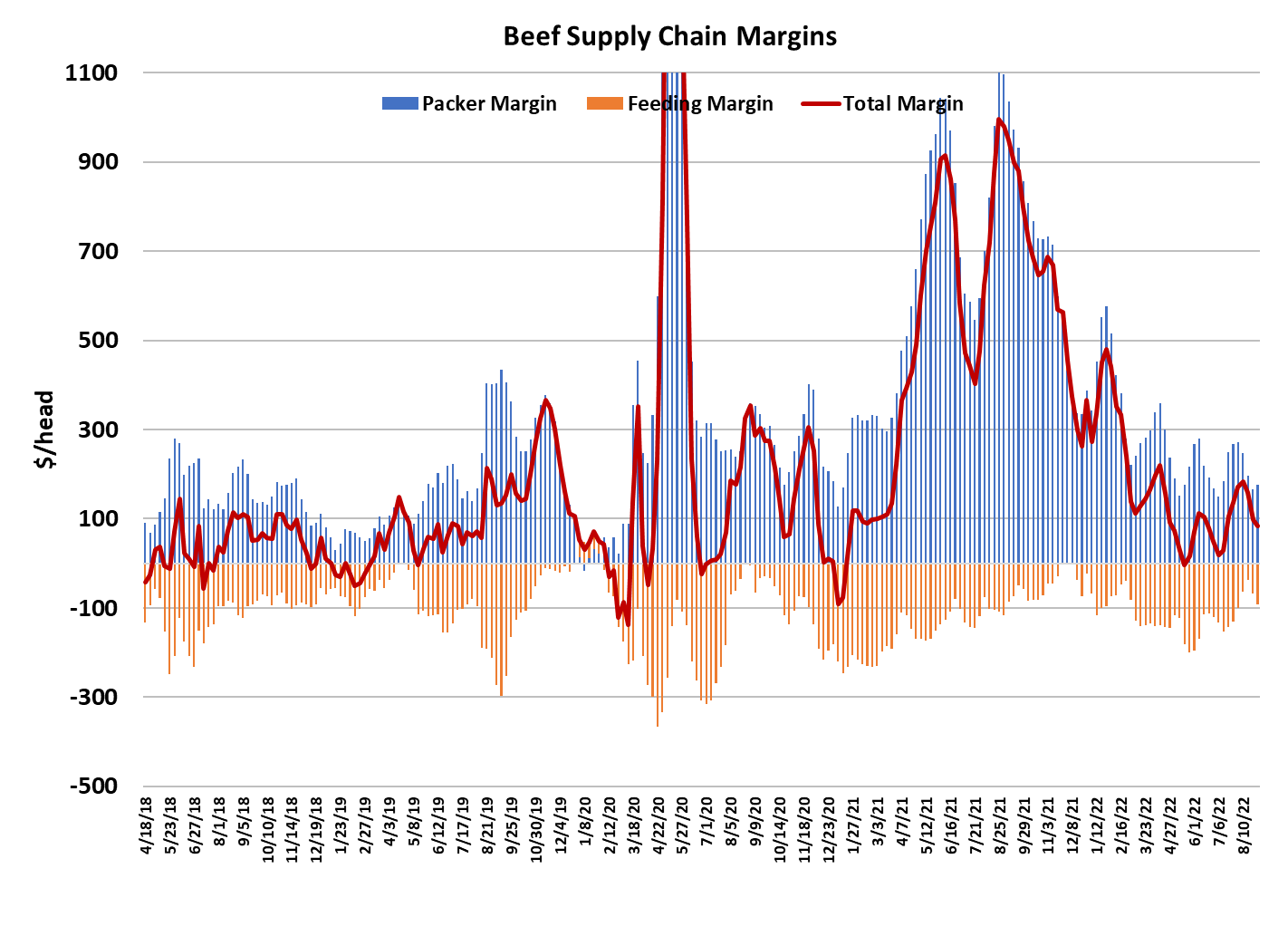

to the long holiday weekend. Packer margins posted a small gain

this week, up $10 to $175/head, but cattle feeding margins

declined more than packer margins gained, thus the combined

margin continued lower this week. It doesn’t look to me like the

combined margin is near a bottom yet and September can

sometimes be a weak month for beef demand, so it seems likely

that the current downcycle in the combined margin will continue for

a few more weeks.

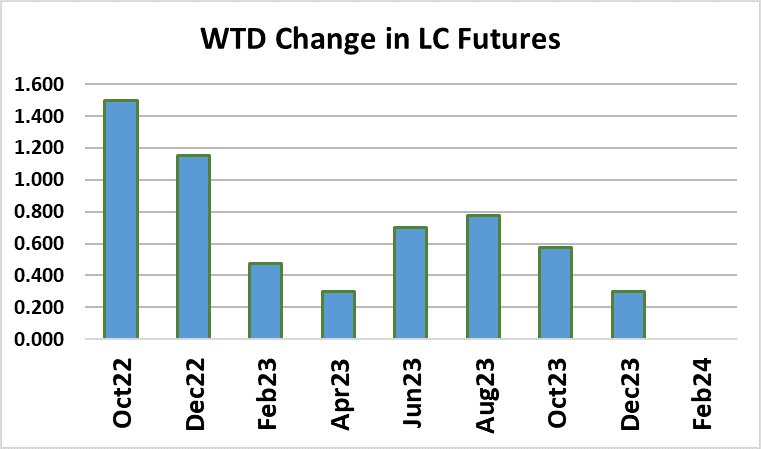

It was a quiet week as far as beef market news goes and most

everything seemed to play out as anticipated. The futures lost

ground early in the week but made that back plus some with a lateweek rally. Now that the Aug futures have expired, Oct will take

over as lead month and traders will not be constrained by the threat

of delivery in the near-term, so they can express their view on price

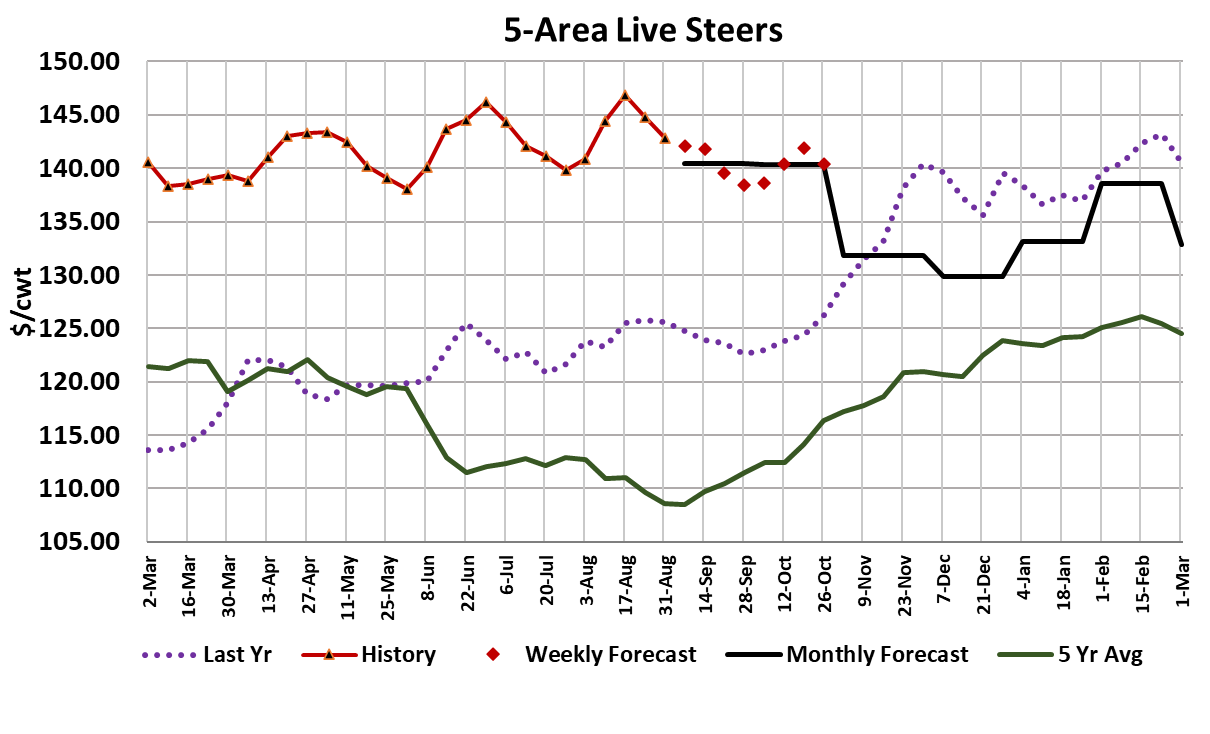

without worry. We have seen cash cattle prices oscillate in a

narrow band between the high $130s and the mid $140s for most

of the year. The attached chart shows this pattern clearly and if it

is to continue, then there is likely more downside risk in cash cattle

prices in the near term. At today’s close of $144.50, the Oct

futures are only about $1.50/cwt over the current cash market, so

producers won’t have much incentive to delay marketings and that

could be what keeps cash cattle prices on their downward

trajectory.

In addition, the short kills around Labor Day should reduce some of

the leverage that cattle feeders have had over packers in recent

weeks. This week’s fed slaughter registered 499k, and I’m dialing

in a 465k total for next week. After that, kills could easily bounce

back up to 530k per week, but I think that packers will want to be a

little more cautious and perhaps not press that hard immediately

following the holiday. Steer weights were reported three pounds

higher at 904 this week, so the seasonal pattern remains in place.

This week’s weight data didn’t do much to move the DTDS weights

and that is still a concern. Right now, the DTDS weights are the

single most bullish factor in the cattle fundamental picture.

Those weights suggest that feedyards remain very current at

present, but if that were the case, why were packers able to take

$4 off of cash cattle prices in the last two weeks? I suspect that

the low level of the DTDS probably reflects some ration changes

that cattle feeders have made in response to high corn prices and

thus cattle aren’t gaining as fast as they might would otherwise.

Of course, that also affects grading, and it is pretty clear that the

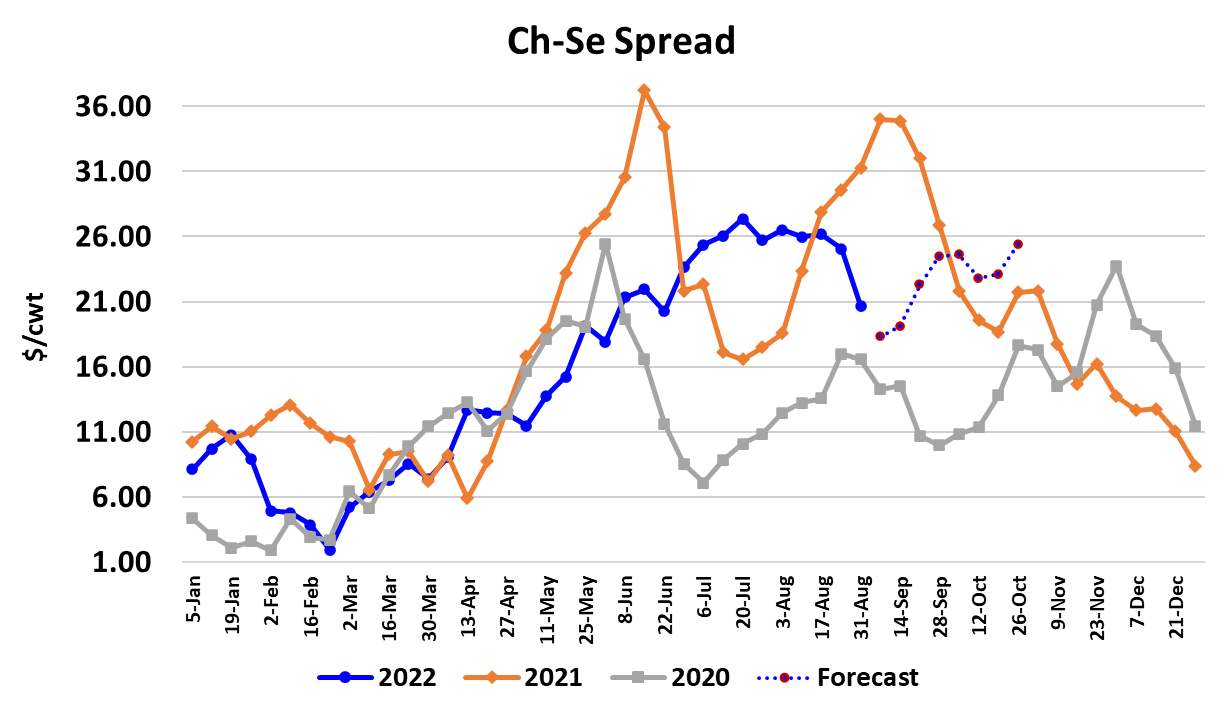

grade is pretty depressed right now. The Choice-Select spread

averaged $20.66/cwt this week, down a little over $4 from the

week before, but that was likely because middle meat demand

was a bit lower. That trend toward a narrower spread could

continue through the first half of September, but once the middle

meat buying for the end-of-year holidays starts to ramp up, I

would look for the spread to widen back out considerably.

In fact, buyers that need Choice or Prime product in Q4 would be

wise to use any price weakness that might arise in September to

cover needs for the end of the year. I wouldn’t be surprised to

see the spread between Choice and Select to exceed $35/cwt at

times this fall. There wasn’t much improvement in the macro

picture this week and the equity markets posted further losses. If

that continues, consumer spending is likely to slow and that

would be a negative for Q4 beef demand. Oil and gasoline prices

are the one bright spot, and consumers in some parts of the US

might soon see gas prices below $3/gallon. However, one of the

things pressuring oil prices right now is an expansion of COVID-related lockdowns in China and that has the potential to temper China’s demand for US been in the near term.

If it does, we probably won’t know about it right away because

USDA’s weekly export reporting system is offline for at least a

couple more weeks. Our next read on beef exports will come on

Thursday, when ERS releases the official trade data for July. I’m

looking for another strong showing in that data, perhaps up

5-10% from last year. Next week, we could see an early bounce

in wholesale prices as retailers fill-in after the long weekend, but

that might only last a couple of days. Look for cattle prices to

continue lower and the futures to take back some of the optimism

it displayed on Friday.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}