Beef Wrap September 16

The cash cattle market was essentially steady this week, averaging

$142.79, up $0.31 from last week. Prices in the North were steady

to slightly lower and prices in the South were steady to slightly

higher. The price gap between the North and South has narrowed

to the point where it isn’t much of an issue anymore. The bad news

for packers was that while they were out there paying steady

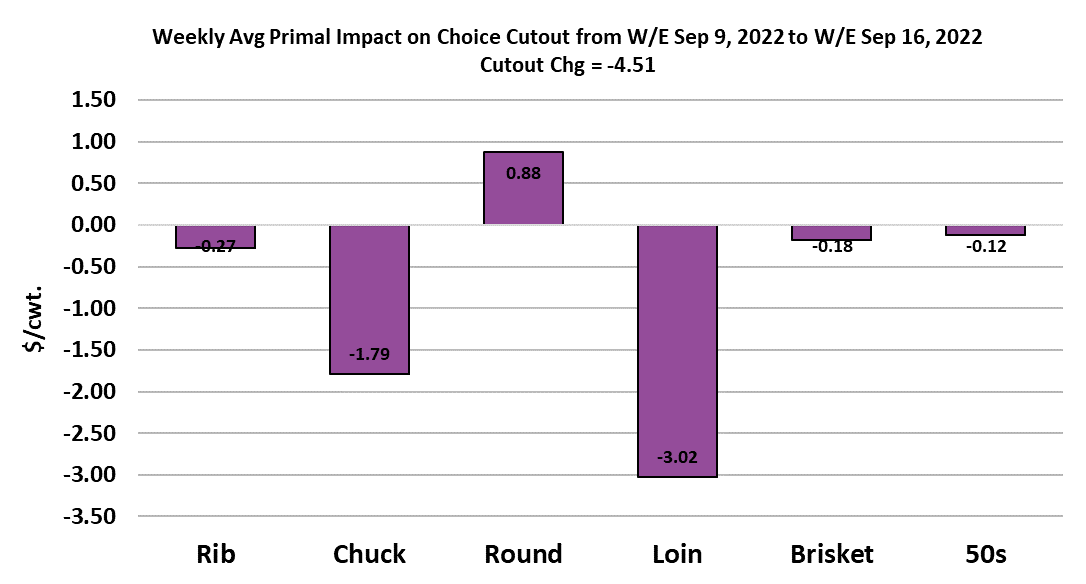

money for cattle, the value of their beef was moving lower. The

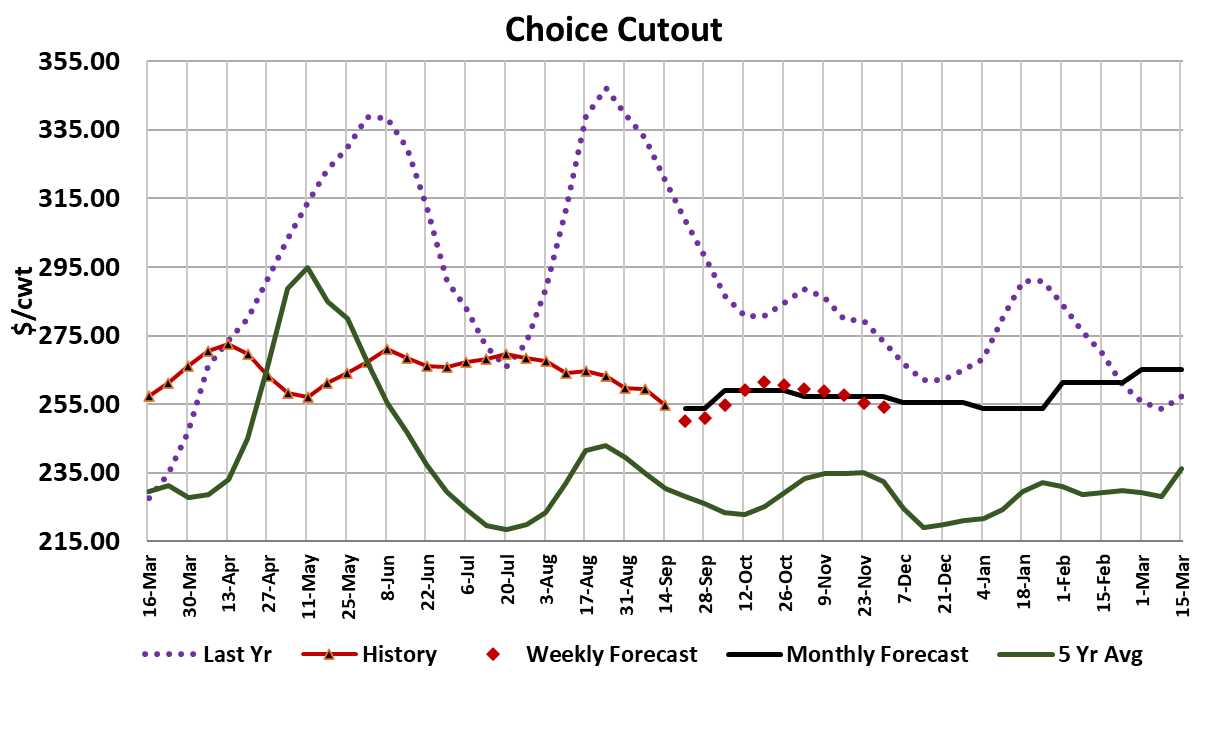

Choice cutout dropped $4.51/cwt to average $254.76 on the week

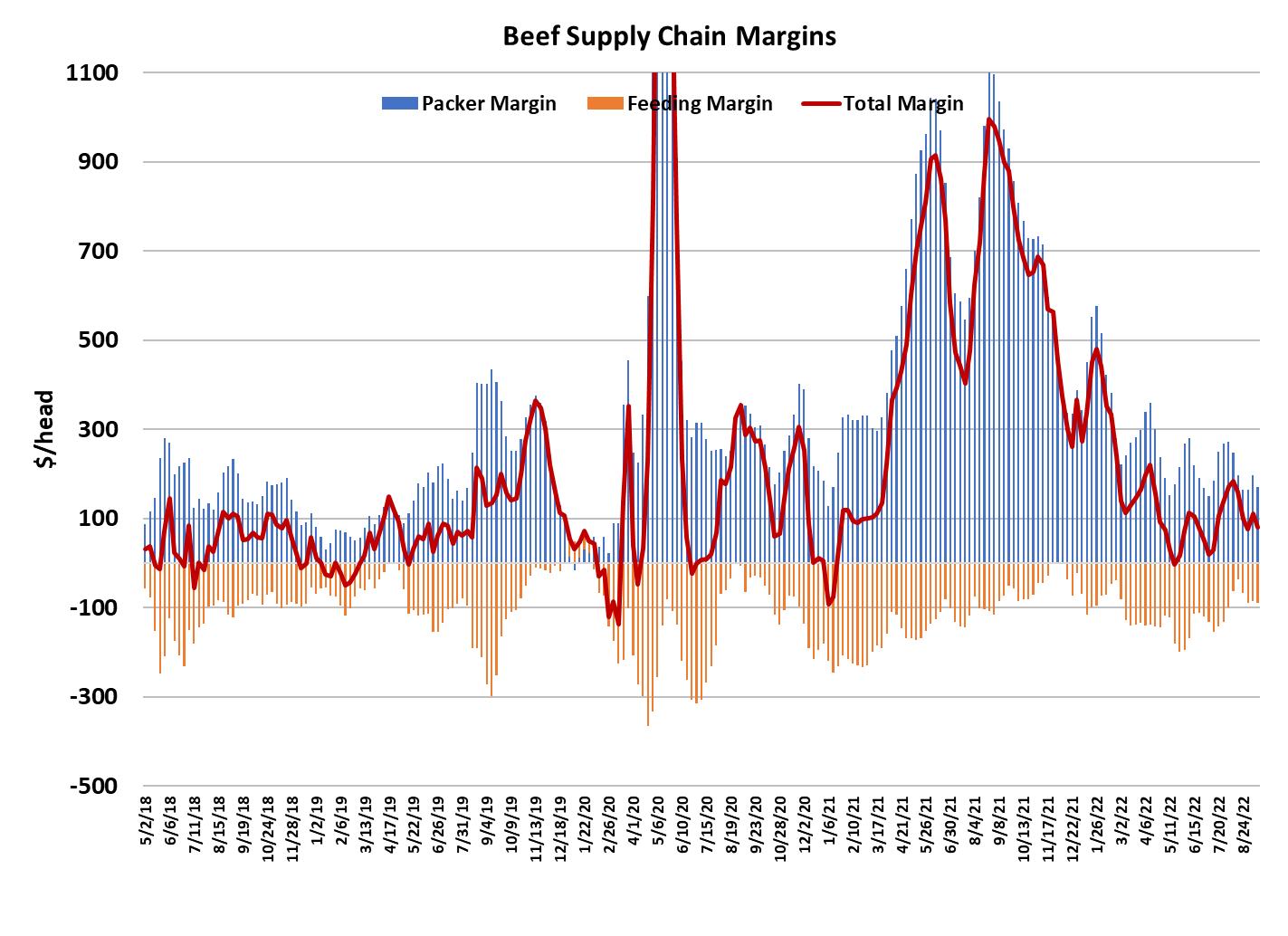

and the Select dropped $5.69 to $231.71. Packer margins

dropped about $25/head to $170 and if I’m correct about the beef

slipping further next week, then we could see packer margins drop

into the low $100s. It was a little bit disturbing to see the beef

market struggle so much coming off a short kill the week before

and that probably says something about the near-term prospects

for beef demand.

This week’s fed kill was close to 520k, down from the 533k that

packers were killing just before the holiday weeks. Maybe they

sensed that they need to dial it back a bit to relieve some of the

supply pressure on the beef market. Soon they will be forced to

dial it back even more because market-ready numbers of steers

and heifers in October are expected to be in the 500-510k range.

Users should be actively covering their needs right now while price

levels are sagging in anticipation of a rebound in beef prices during

October. The cattle market could also see some additional

strength in October too. Cattle carcass weights continue to tell a

story of very current feedyards and the grading also points in that

direction. A couple more weeks of strong kills and by October the

cattle feeders should have enough leverage to advance the cattle

market. Packers will be hoping that the gains in the beef are strong

enough to pay for those more expensive cattle without crushing

their margin.

Last week, I was concerned that the small uptick in the combined

margin was a head fake and sure enough, the combined margin

turned back lower this week. If the last two demand cycles are any

guide, the combined margin needs to get back near zero before a

new upcycle will begin. So, I’m calling the cutouts softer over the

next two weeks to accomplish that objective and then I expect them

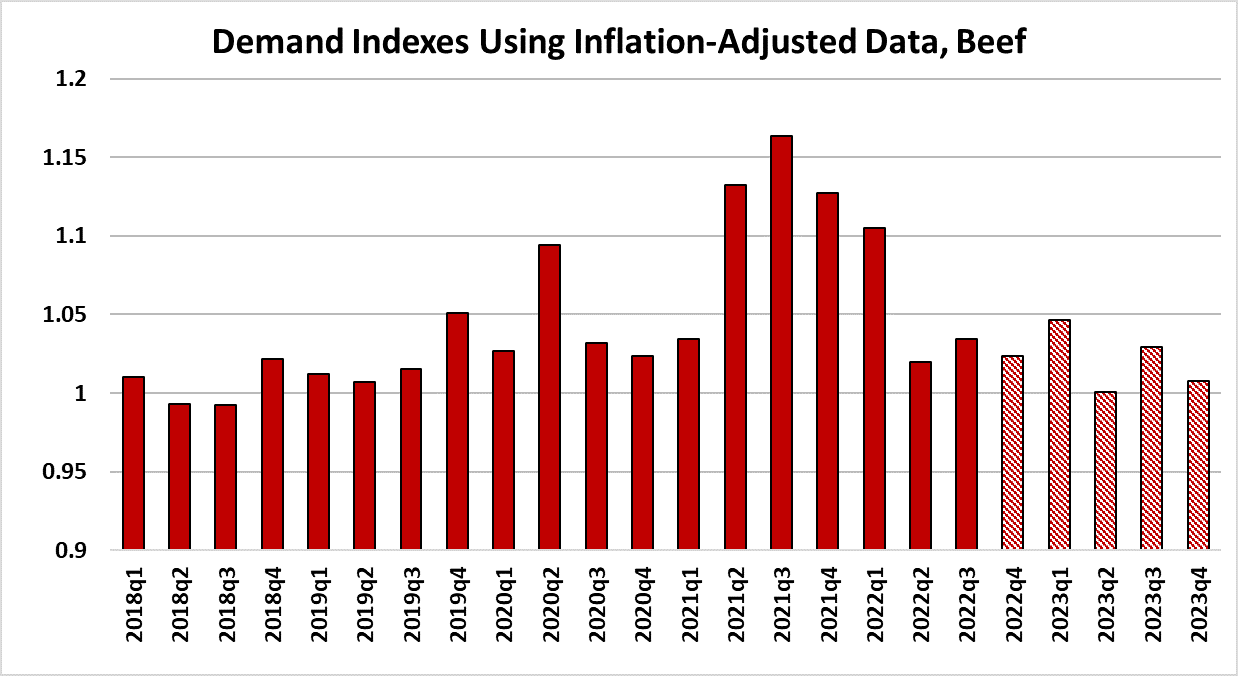

start marching higher. Speaking of demand, it is important to note

that this week I completely reformulated the demand index

calculation to take into account the impact of inflation. I was

concerned that the presence of such high inflation in the economy

was clouding my ability to accurately gauge beef demand, so I now

calculate the demand indexes using deflated prices (deflated by the

Consumer Price Index).

Back when inflation was consistently running 1-2% per year, it

wasn’t a big deal to calculate the indexes with unadjusted prices

and I think analysts tended to avoid using deflated prices where

possible because it just introduces another source of error when

attempting to forecast, because that would require a forecast of the

CPI in order to arrive at a future price level. However, in a 8-9%

inflation environment, ignoring inflation can lead to undershooting

on price forecasts by a significant margin. In the case of the beef

market, this change helped me to more clearly see that most, if not

all, of the demand boost from the pandemic has already come out

of beef prices. The attached chart shows the updated demand

indexes by quarter and it is clear that after experiencing a bubble

in 2021, they are now back down near pre-pandemic levels (and

have been for the last 2 quarters). This has led me to stop looking

for further big downward corrections in demand based on the

easing of the pandemic.

That has already happened. However, demand could still suffer

due to adverse macroeconomic conditions, so I’m not saying that

demand can’t get worse from here. Equity markets sold off hard

again this week and more indicators are starting to emerge that

suggest a global slowdown is not far around the corner. So, we

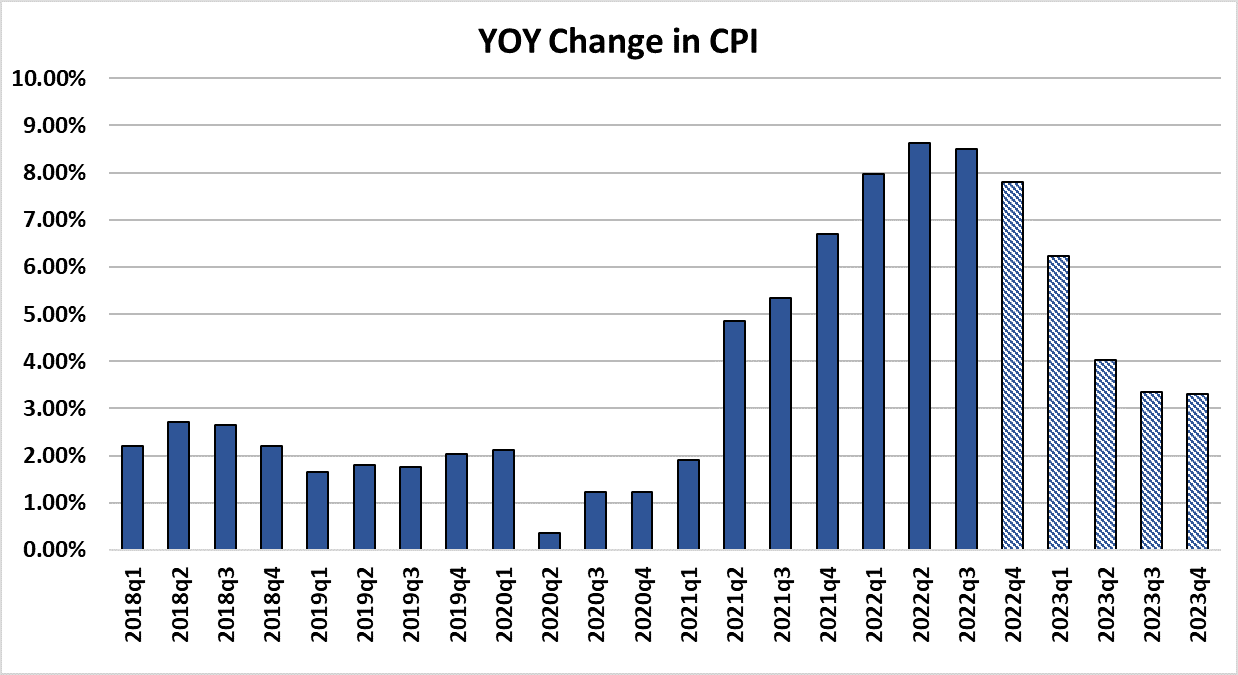

are not out of the demand “woods” yet. I’ve also attached a chart

of quarterly CPI so that you can get a sense of what my CPI

forecast looks like. This is impounded in the beef demand

indexes now, so if I’m really wrong on the CPI, it has the potential

to make the demand forecast really wrong also. One negative

factor that cropped up this week was the weekly export data. It

looked pretty weak relative to what we had been seeing over the

summer.

Recall that USDA took a 4-week break in reporting the data while

they straightened out their system problems. Now that we aren’t in

the dark anymore, it looks like international demand for US beef

has been softening during the intervening period. However, I get

nervous about data integrity whenever USDA’s systems are acting

up, so I don’t want to place too much emphasis on this right now.

Let’s see how the next few weeks’ worth of export data come in.

Next week, look for the cutouts to drift a little lower and packers

possibly to take a little off of the cash cattle market. The fed kill

should be close to even with this week and maybe a little larger.

Buyers should be busy working on their holiday needs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}