Beef Wrap September 30

The margin squeeze on beef packers is getting more intense. This

week’s margin only registered $68/head and next week could be

even smaller. That is the result of a mostly steady cash cattle

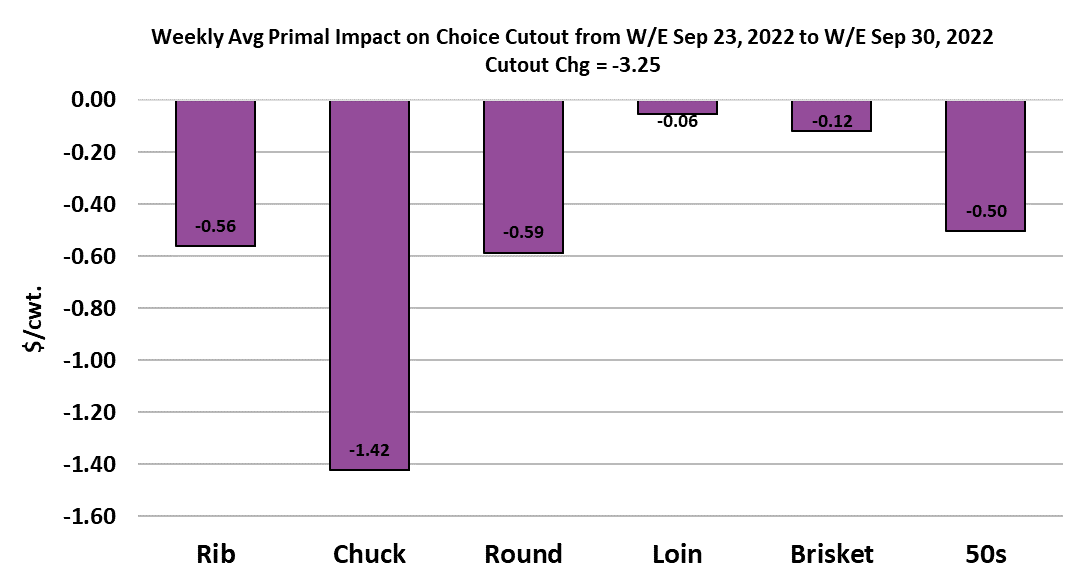

market and falling beef cutouts. The Choice cutout lost $3.25/cwt.

and the Select was down $3.40/cwt. The fact that cash cattle were

able to trade nearly steady at $144.55/cwt. is a testament to

feedyard currentness because in addition to falling cutouts, the

futures market continued its move lower as well and the US equity

markets were also in a freefall. So there was a lot of negativity in

the air that could have dragged cash cattle lower, but didn’t.

Packers will probably slow the kill down in the next few weeks, not

just because their margins are under pressure, but also because

the number of market-ready cattle should be tighter in October than

it was in September. Perhaps that will help stem the slide in the

beef market. Or not. I don’t get the sense that this is really a

supply-driven pullback in prices.

Instead, I think it has more to do with the demand side of the market

and what is going on the macroeconomy. The macro picture seems

to get darker every day and the stock market is reflecting that

sentiment. Consumers are starting to be more cautious as they

spend and that is probably having an impact on how fast beef is

moving. Retail beef prices remain very high and that is a pretty

strong impediment to beef movement in this environment. What

really needs to happen is for retailers to begin lowering prices in

bigger chunks than the small declines we have seen lately. Of

course, retailers are fearful of lowering prices in this inflationary

environment where all of their costs, especially labor, have gone

way up. So that creates a bit of a stalemate that can probably only

be broken by further softness in wholesale prices that will give

retailers enough margin cover to start lowering the prices that

consumers see.

As the calendar turns to October, we normally expect to see interest

in the middle meats start to build as beef buyers prepare for the

upcoming end-of-year holidays. So far that hasn’t happened and

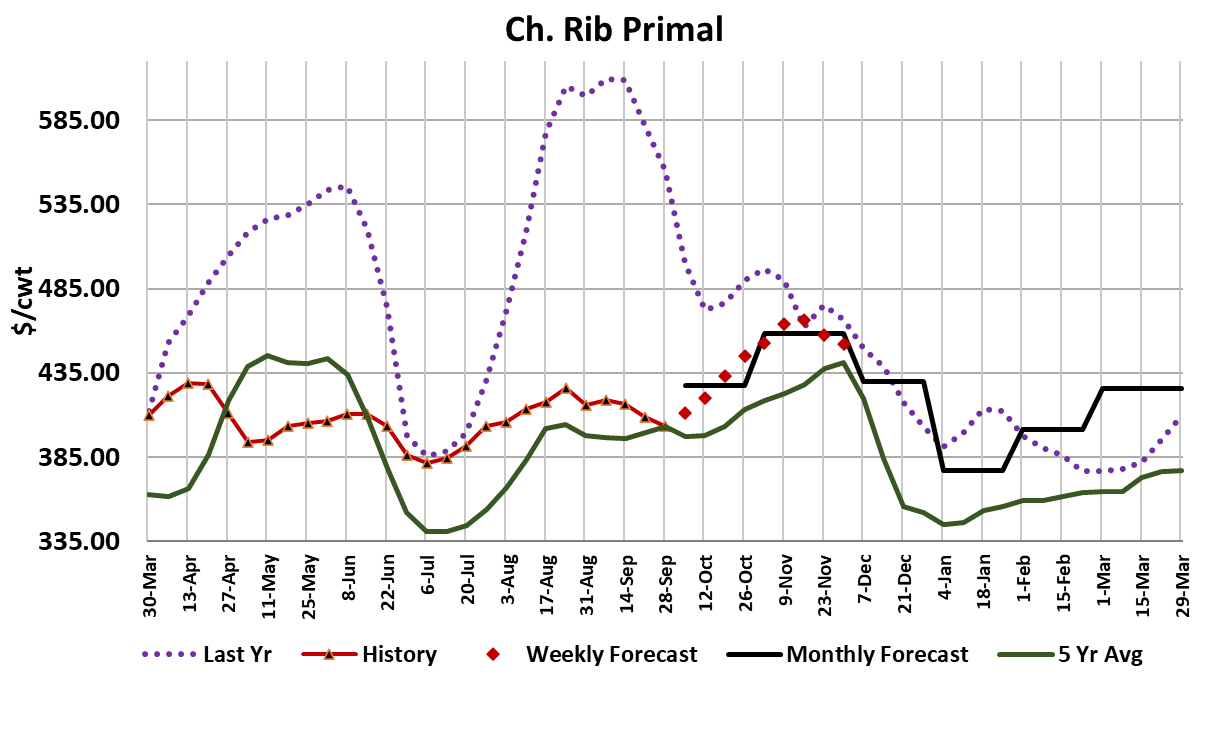

I’m sure that packers are anxiously anticipating that shift. The rib

and loin primals were both lower on the week. Recall that last year

the middle meats didn’t exhibit a holiday rally at all. Prices tracked

lower from September into January. Of course they started from

much higher levels that we are at today, so that likely contributed to

the odd seasonal pattern last year. For this past week, the rib

primal was priced over $150/cwt. lower than where it was last year

at this time. That is a 27% difference. However, this week’s rib

primal value was the second highest on record (after last year) and

about 10% over the 2018-2020 average.

We should be able to chalk that up to inflation, but it does make me wonder if perhaps this relatively high starting point will limit the potential for an Oct/Nov middle meat rally again this year. End meats have also been disappointing lately.

The chuck primal averaged under $200 for the first time in about a

year and a half. Chucks were the biggest drag on the cutout this

week and rounds were in second place. Even the fat trim has

nosedived recently and is now priced in the mid-$80s. It certainly

feels like we are still in a demand downdraft and both the daily

scatters and the combined margin confirm this. It has been a while

since we’ve seen the combined margin move below the zero line,

but I suspect that is about to happen over the next week or two.

Hopefully, that will mark the end of this demand cycle and a new

upcycle can begin. On the supply side of the market, this week’s

fed kill came in at 516k, down 6k from the week before. It was

mostly a smaller Friday kill that made the difference.

I think we can expect next week’s kill to be a little smaller yet as

smaller available cattle supplies will limit how far packers can push

the kill without having to raise cash cattle bids. In this margin

environment, the last thing that packers want is to have to pay up

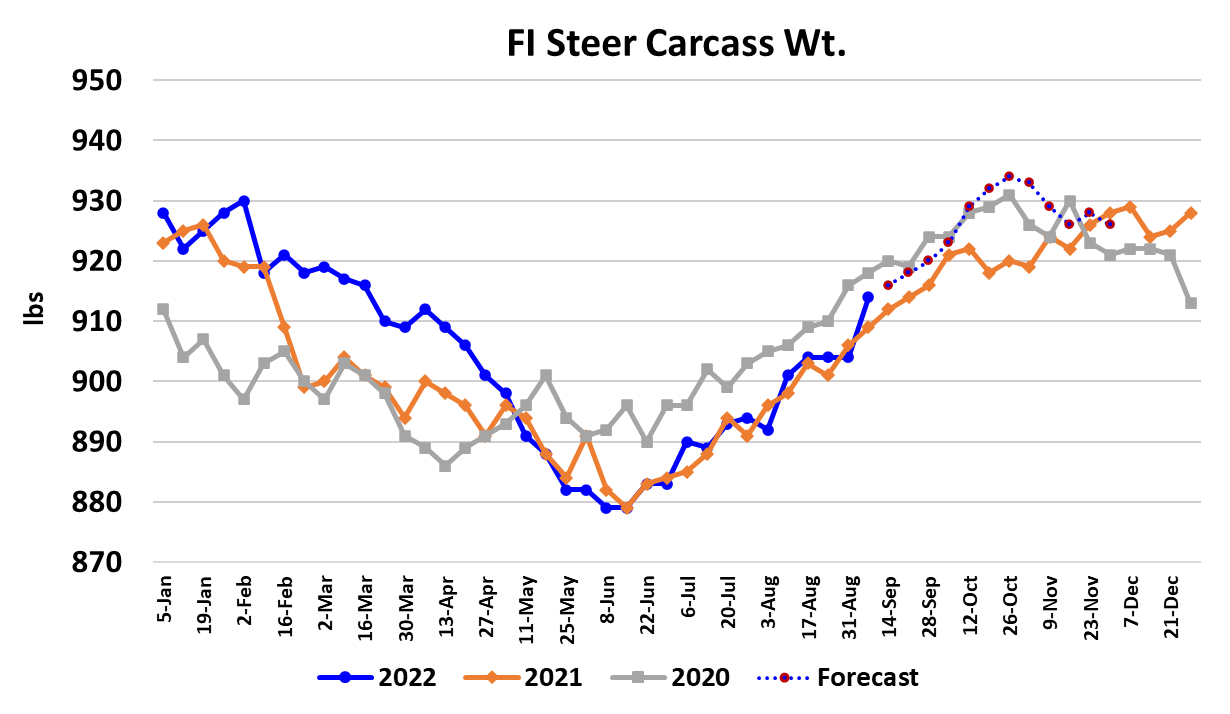

for cattle. Steer carcass weights were reported 4 pounds higher

this week and that comes on top of a 10 pound increase the week

before. As a result, the DTDS weights are starting to climb, but are

still very low historically and that is telling us that feedyards are still

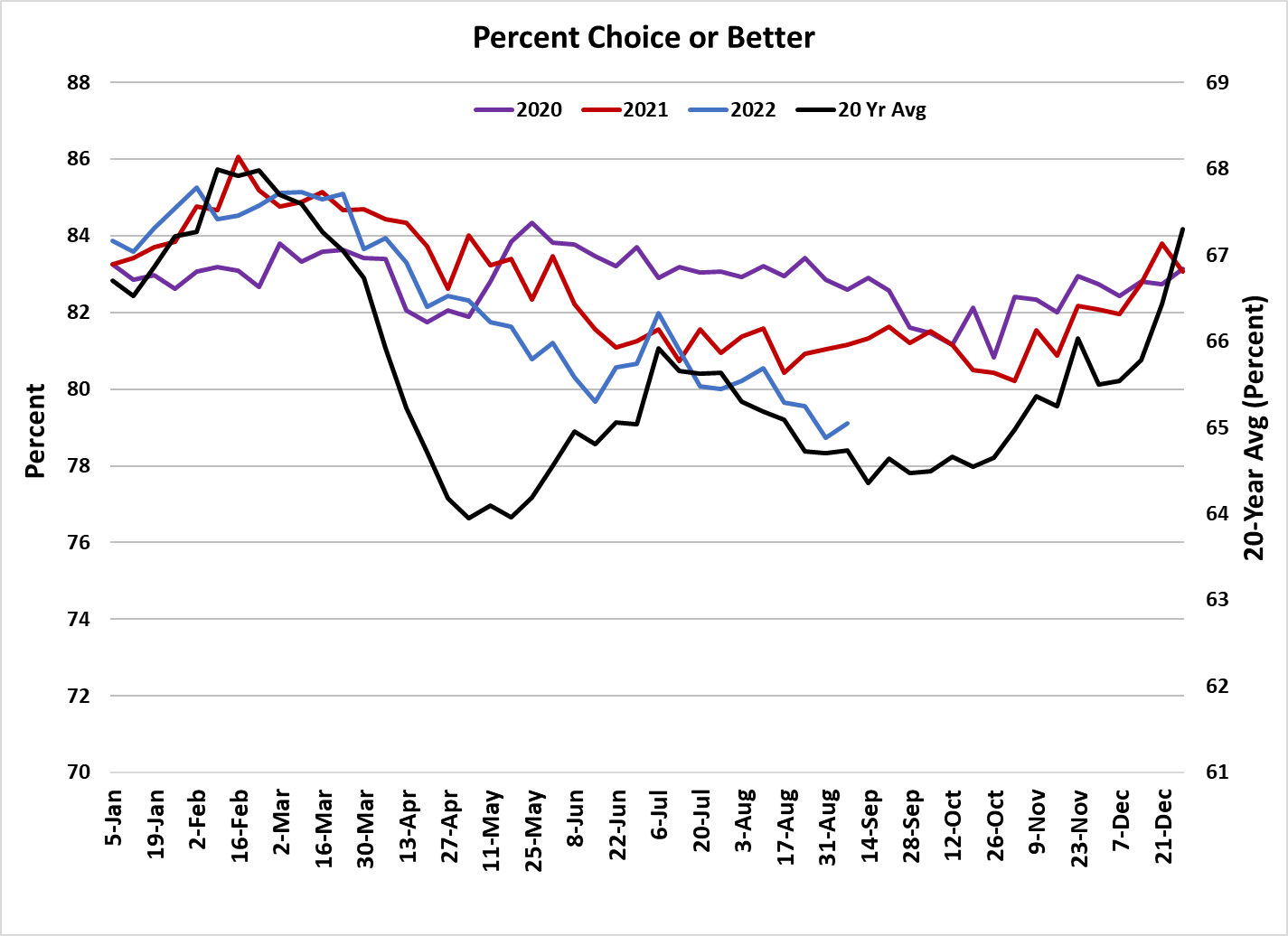

pretty current. The cattle aren’t grading very well either and that is

another sign that feedyards are current. The poor grading comes

at an inopportune time for beef buyers, who might find it a little

more difficult to find the high quality middles that they desire ahead

of the holidays. The Choice-Select spread averaged $26/cwt. this

year and there is concern that it could go higher as we move closer

to the holidays.

If it doesn’t it probably means that holiday demand for middles is

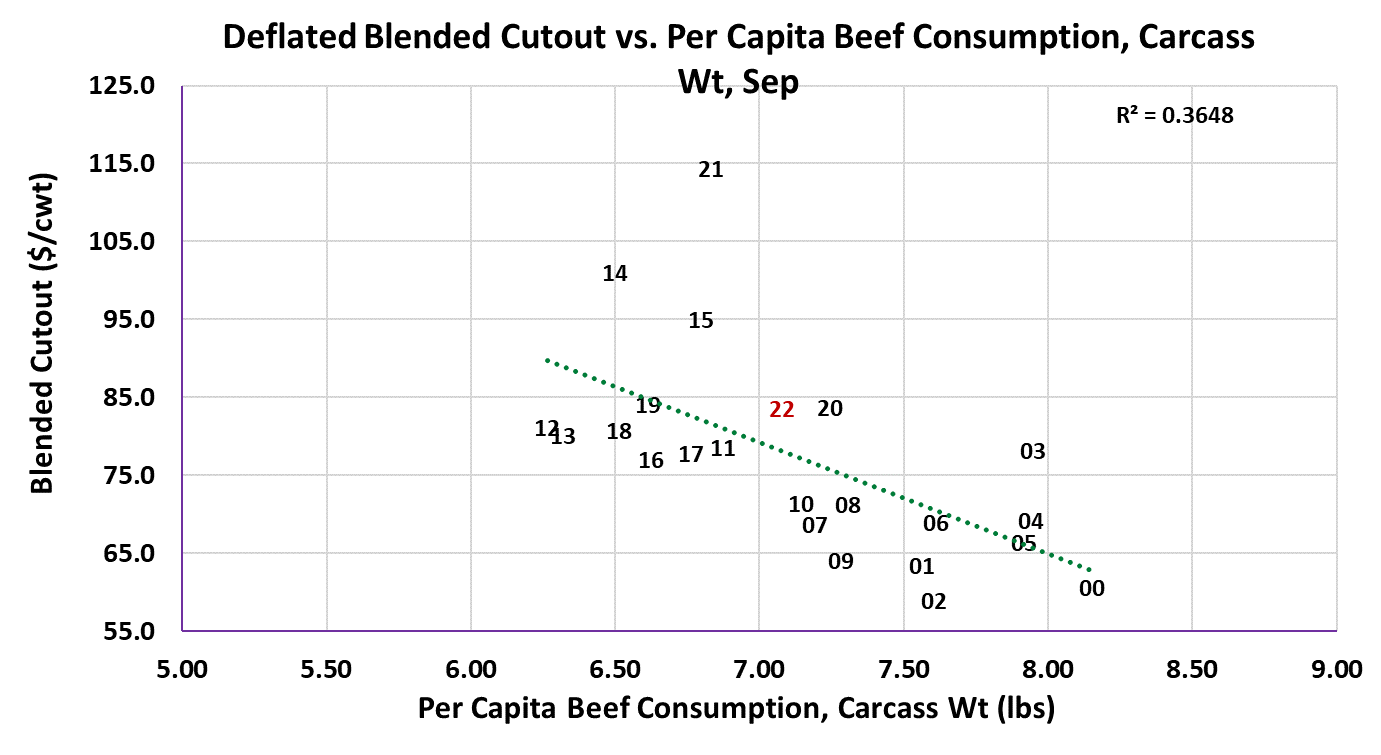

weaker than normal. The attached scatter diagram for October

shows just how much beef demand has declined from last year.

Per-capita consumption was only a tiny bit larger this September

compared to last, but the Sep 2022 data point is much, much closer

to the regression line than the data point from Sep 2021. The

great demand re-set has taken place and brought prices back

closer to pre-pandemic norms, but it may not be done yet and that

will likely keep market participants attention in the near term. Next

week, watch for the middle meats to get some kind of price lift. It is

time for that. Also watch cash cattle prices because there is a

reasonable chance that cattle feeders are able to move them

modestly higher.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}