Beef Wrap October 7

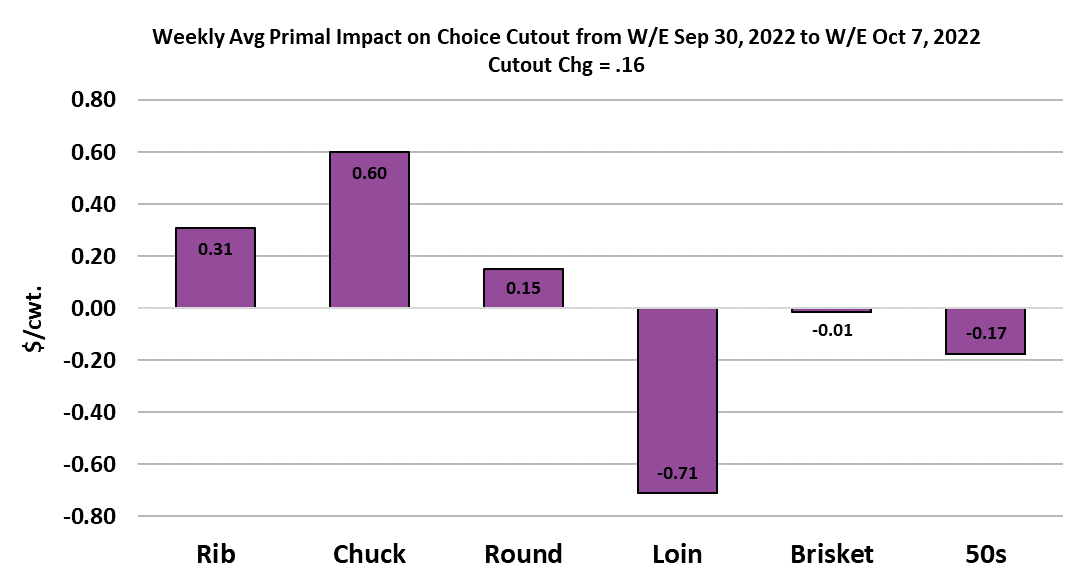

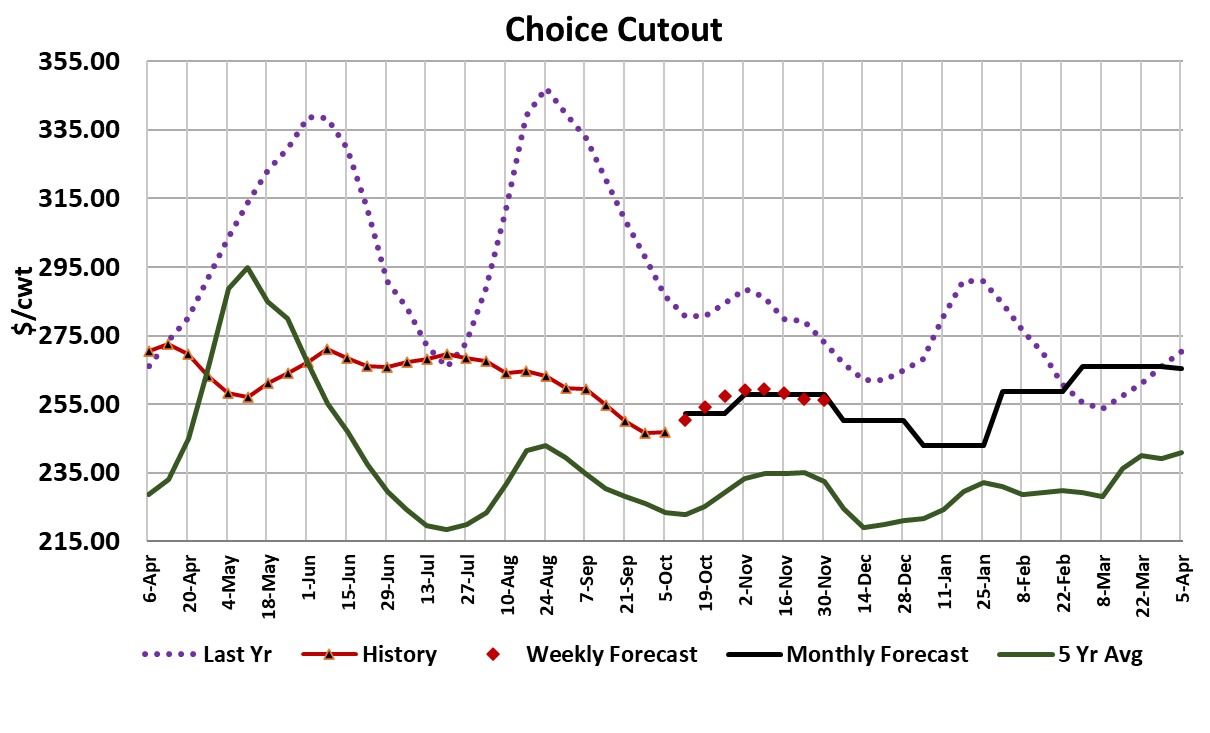

It was a pretty quiet week in the beef market with the Choice

cutout only gaining $0.16/cwt. on a weekly average basis and the

Select cutout losing $1.62/cwt. As a result, the blended cutout

was just a few cents lower on the week. The cash cattle market

was stronger, averaging close to $146, which was about $1.20/

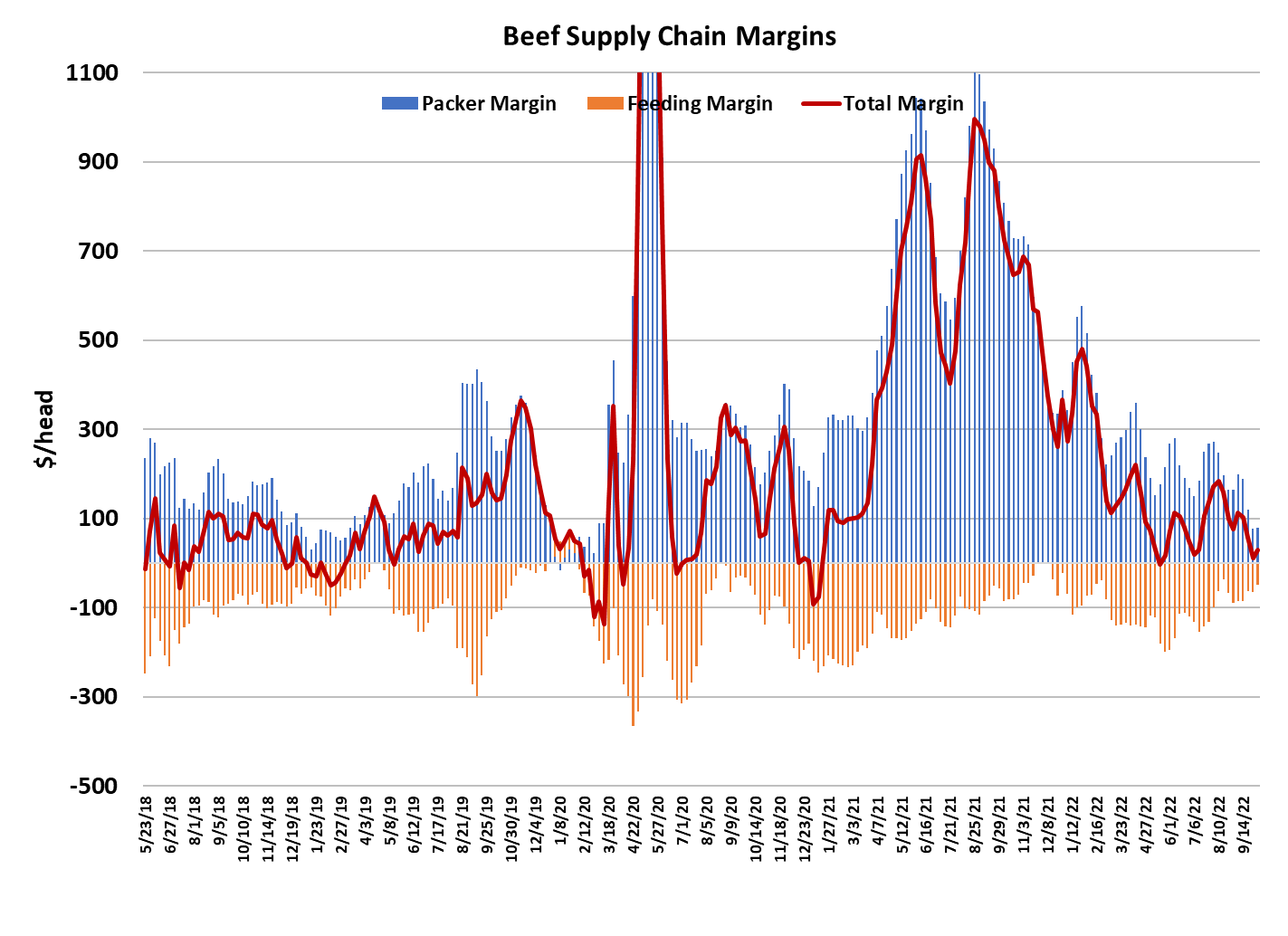

cwt over last week. Packer margins came in at about $78/head—

not much change from last week. So far we haven’t seen the

surging middle meat demand that normally starts early in Q4.

The rib primal posted a small week-on-week gain, but the loin

primal posted a small loss for the week. Perhaps the most

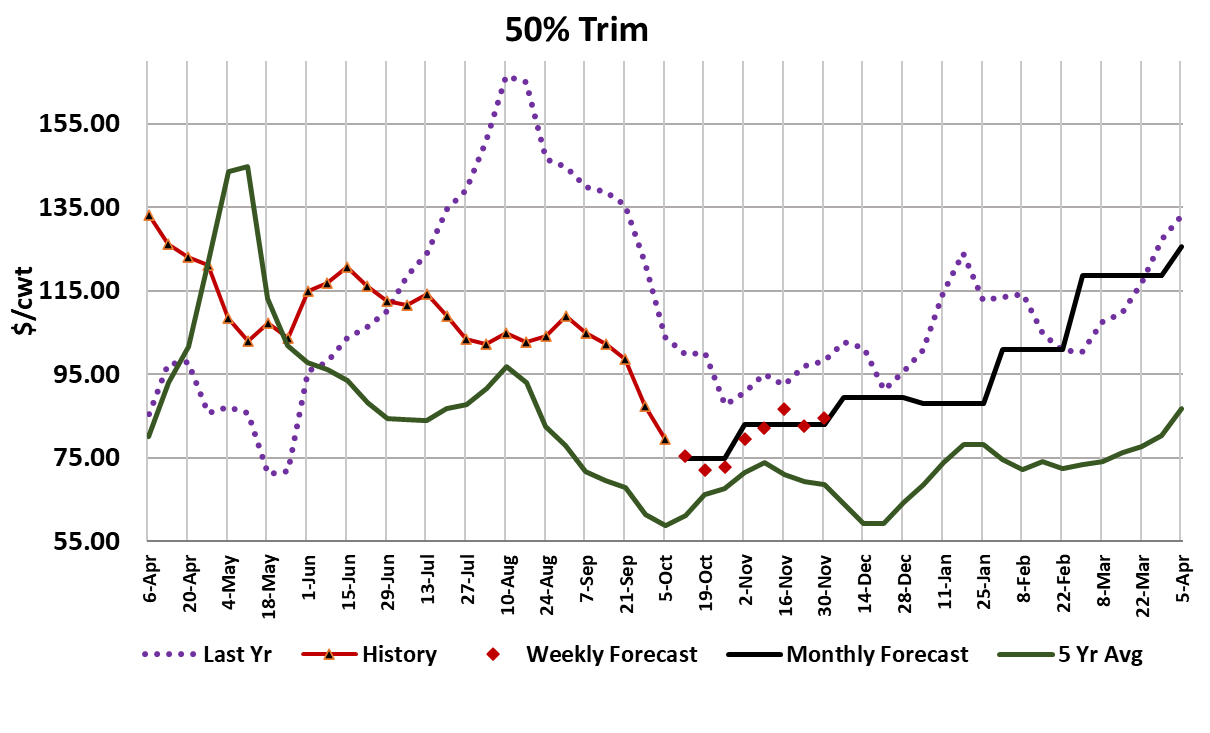

notable change in the beef complex this week was the 50s

moving below $80/cwt, down about $8 from the week before.

Given that fed kills are now smaller than they were back around

early September when the 50s were averaging in the low $100s,

I’d say that this drop in the 50s is more related to demand than

supply.

I take it as an ominous sign when one of the cheapest items in

the beef complex is having demand problems. Chicken prices

have been coming down rapidly as production is increasing and

that is likely steal some demand from the grinding complex in the

weeks and months ahead. The macro environment didn’t get any

better this week as equity markets posted strong gains early and

then gave all of it back at the end of the week. That is the type of

price action that makes people feel crummy about the prospects

for the future and is likely to dim their confidence in the economy.

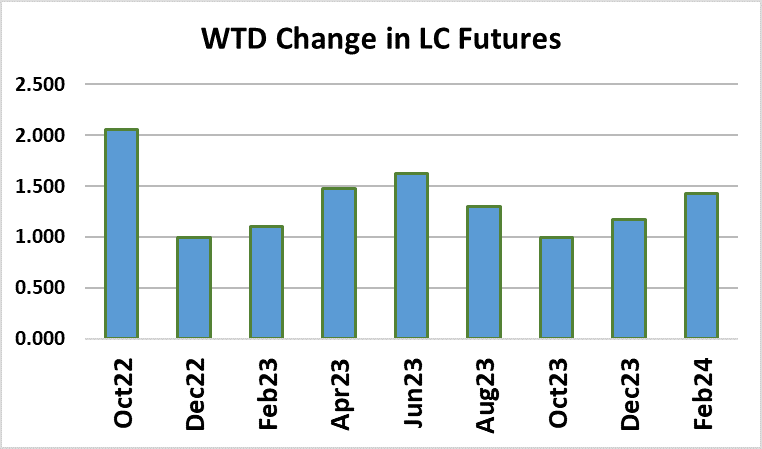

LC futures managed to rebound some this week, but that was just

a bounce up from seriously over-sold conditions in the prior

week. Futures traders must be encouraged that cash was able

to advance a little further this week, but packers really haven’t put

up much of a fight yet.

At some point in the next few weeks, I’d expect packers to dig in

and refuse to pay up for cattle and that will probably be met by

producers refusing to sell any cattle. We haven’t had a week of

no cattle trade for quite some time. Right now, I’d say that

producers have the upper hand because the front-end supply of

cattle still seems very current. The ultimate solution is for

packers to pull back on the kill, which is something they haven’t

shown much interest in. The other out would be for boxed beef

prices to rally sharply and restore packer margins without the

need to pressure the cash cattle market. The market is due for a

rally, so maybe that is how it will play out. The combined margin

ticked a little higher after nearly touching the zero line last week.

It could be that demand is just about to enter another upcycle. If

we do get some seasonal improvement in demand, I expect that

it will be much more muted than what we’ve seen in previous

years due to the challenging macro environment. On the supply

side, the fed kill came in at 516k, down just 3k from the week

before. The flow model has been pointing to tighter fed cattle

availability during October, but it seems that packers want to

continue killing as though it were August. Packer margins have

been so large for so long, that it is difficult to gauge at what

margin level they will start cutting the kill. Will they wait until

margins are negative or will a $20/head margin do the trick?

They may be able to avoid that tough decision altogether if they

can get a decent rally in the boxes, but with each passing week

the prospect of a sharp Q4 price rally seems less likely.

Steer carcass weights dropped three pounds this week, taking

back some of the stunning 14-pound gain that happened in the

previous two weeks. The DTDS weights remain rather low, so it

seems as if feedyards are still pretty current. Packers will not get

cattle prices down unless they reduce currentness of the cattle

supply. My forecast has steer weights gaining another 18

pounds over the next 5-6 weeks towards a top in mid-November.

USDA provided the trade data for August this week and it

showed beef exports only 0.3% below last year, but that was the

first monthly decline in exports so far in 2022. To be fair though,

August was the top month for exports last year. Through August,

beef exports are up 5.5% YOY and the forecast has them

finishing the year up 6.1%.

So, I’m not projecting any serious softness in the export market

for Q4, but I do think that we will see some YOY declines when

Q1 rolls around. August beef imports were down 18% YOY, but

again, August was the top in beef imports last year. It looks like

the US will remain a small next exporter of beef in 2022, so I

don’t really think that a darkening trade picture will be what

hampers pricing in the next few months. It is more likely to be

problems with domestic demand, but those might not manifest

until after the fall middle meat rally has run its course. Next

week, watch the middles, particularly ribs, for signs pre-holiday

demand is beginning to creep in. Also, watch the daily kills for

signs that the packers are starting to see the need to dial down

slaughter rates.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}