Beef Wrap September 23

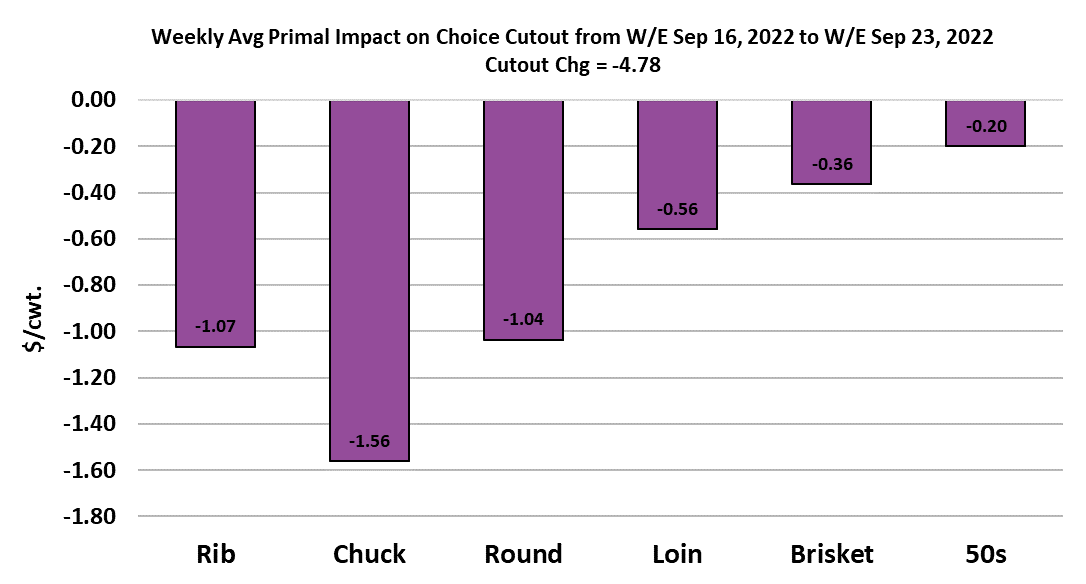

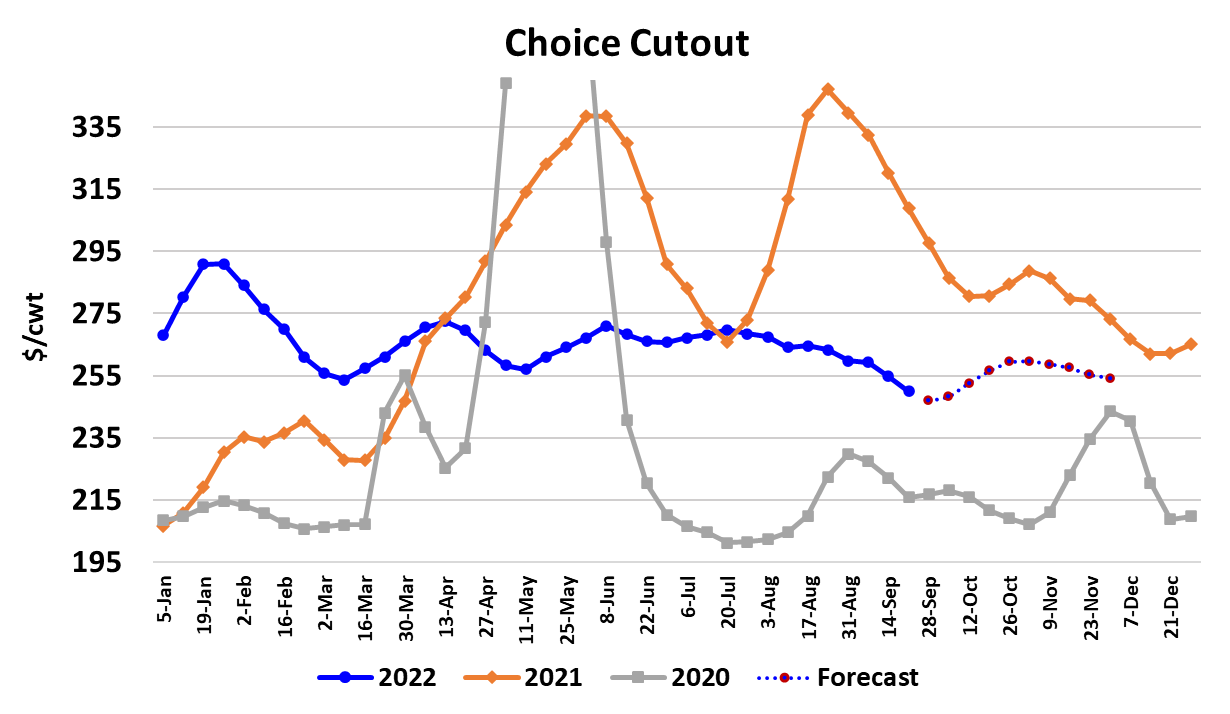

It was another bad week for packers, with the cutouts tracking lower

and the cash cattle market moving higher. On a weekly average

basis, the Choice cutout lost $4.78/cwt. and the Select cutout was

down $7.07/cwt. Cash cattle averaged about $1.30/cwt. over last

week and packers bought a lot more animals than they did the week

before. Perhaps they are trying to get some inventory around them

so that they won’t have to pay up again next week. Obviously, their

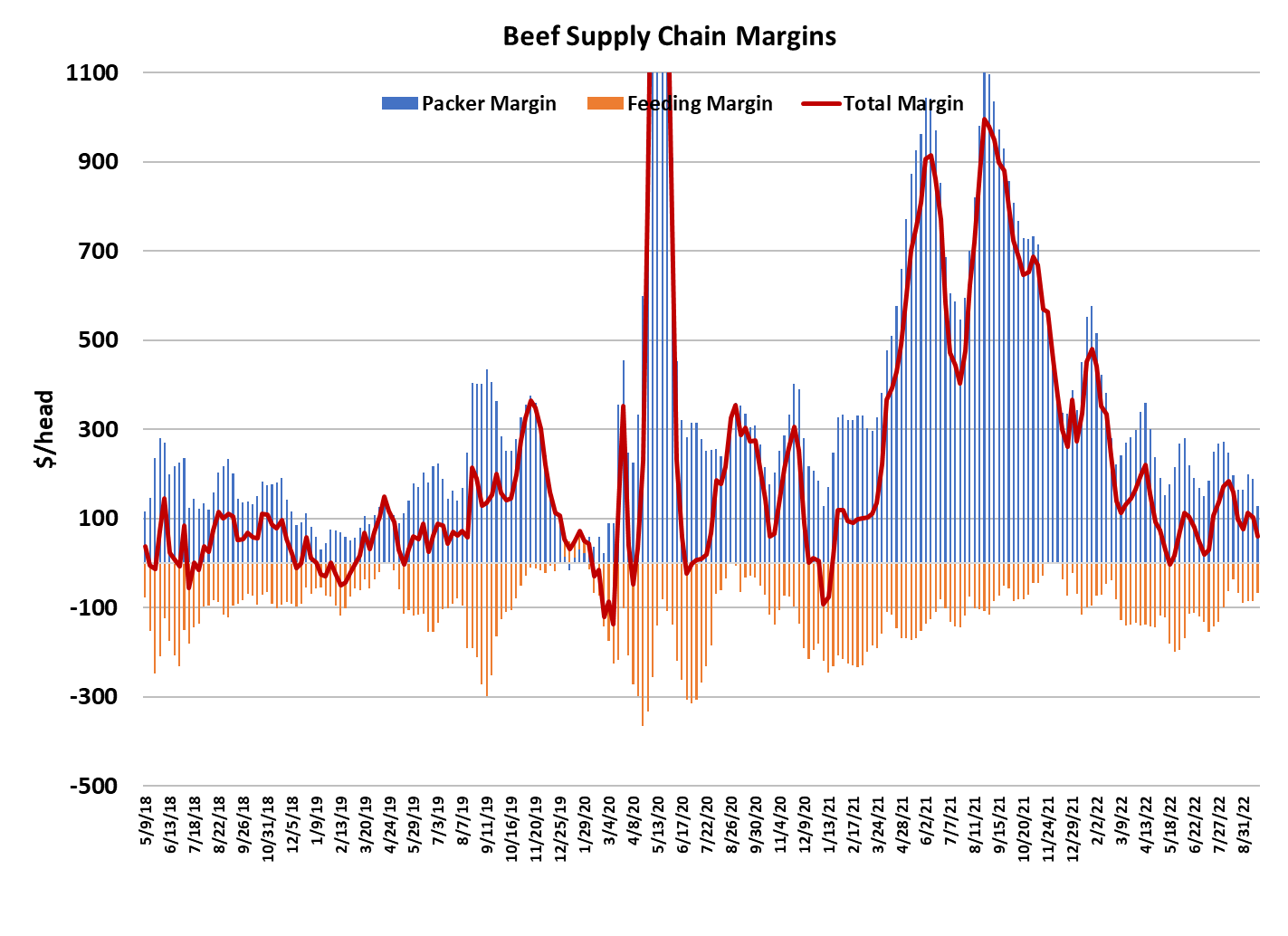

margin took a hit this week, dropping almost $60/head from the

week before to average $129/head. Unless the cutouts can stage a

substantial rally next week, margins are likely to fall below $100/

head when this week’s more expensive cattle show up at the

slaughterhouse.

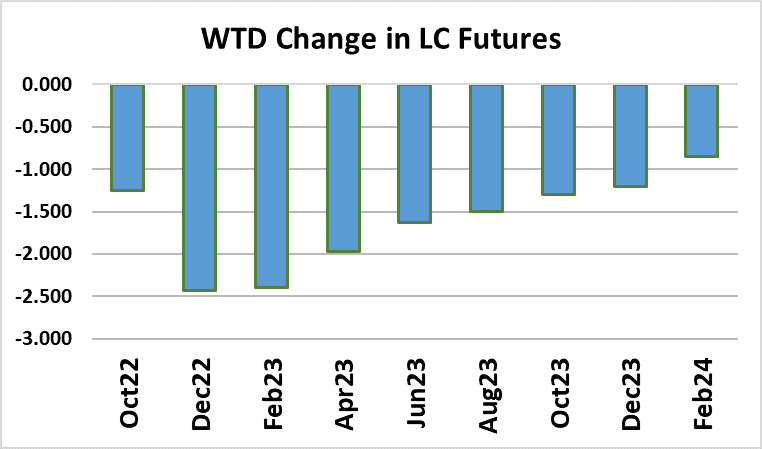

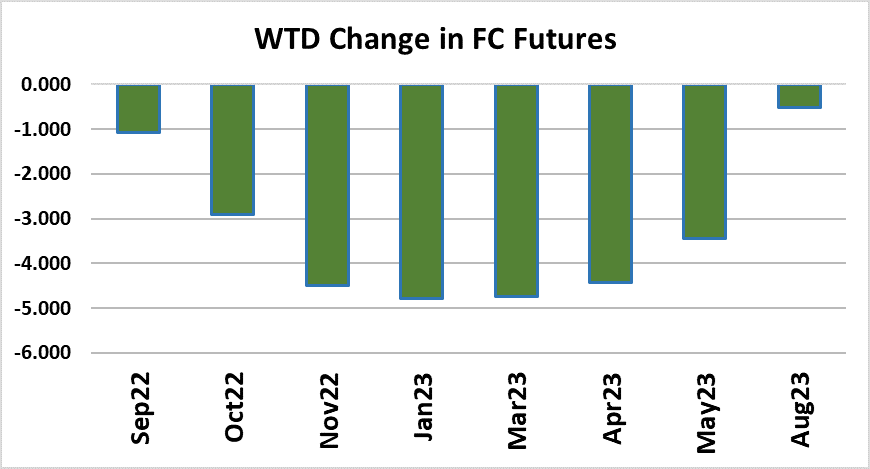

The futures market paid no attention to the fact that packers were

paying more for cash cattle and the most active Dec contract lost

almost $2.50/cwt. on the week. Cattle traders seemed to be more

focused on the possibility that the US will slip into a recession as a

result of the ongoing interest rate increases by the Federal Reserve,

who upped rates another 75 basis points this week. The stock

market had an awful week also and that can have a psychological

impact on consumers even before an official recession begins.

Traders see the beef cutouts falling day after day and the stock

market blaring warnings of and impending recession and that sends

them into selling mode. I think they are correct to sell the more

deferred issues, which have been supported at very high levels for

months now by the bull story of tightening cattle supplies in the

future. However, as this week showed, prices are not only

determined by supply. Demand has a lot to say about price levels

also and the bad news on the demand side is finally starting to get

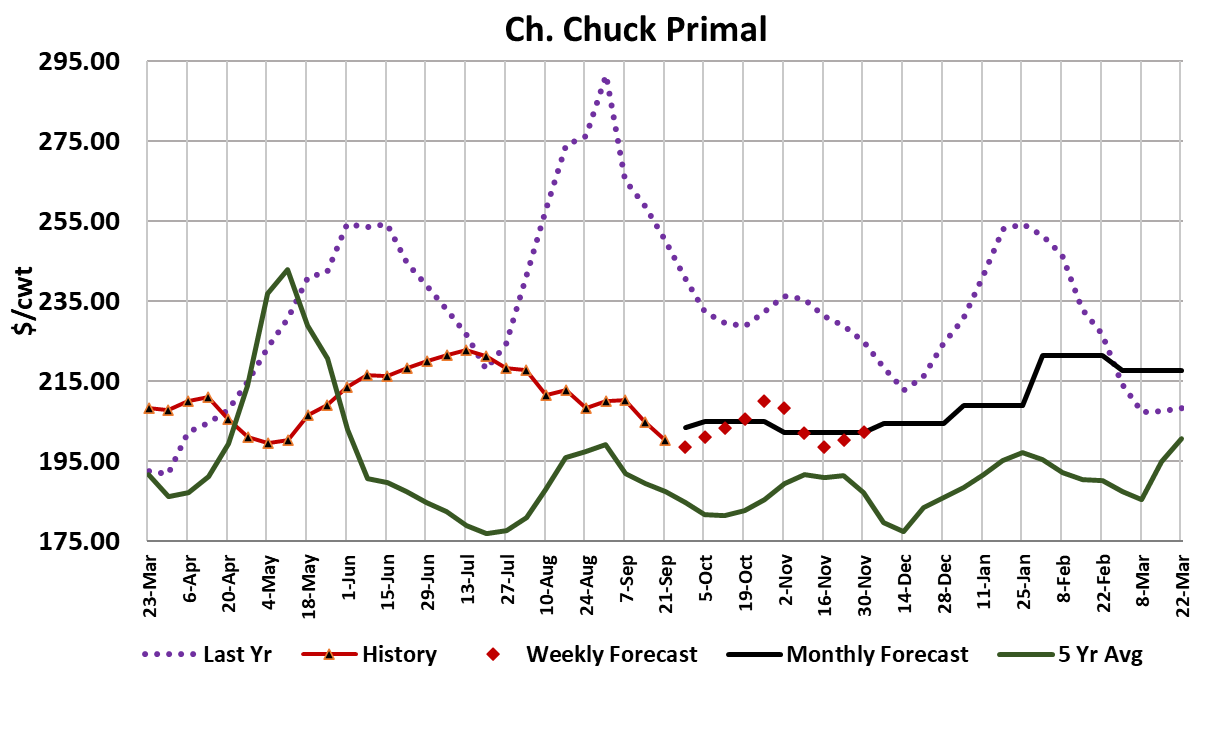

more focus in the cattle market. This week, all of the primals were

lower, but the end meats led the way.

Even ground beef saw prices slip this week. End meats and grinds

are the items that should see the least demand slippage in hard

times, but instead we are seeing the opposite. Maybe that is an

indicator that the hard times haven’t really arrived yet. However, as

we move into Q4 and the weather cools, end meat demand should

improve, if only for a couple of months. The combined margin

continued lower this week after a brief head-fake a couple of weeks

ago and it looks as though this demand downcycle may have

another couple of weeks to go before we get the combined margin

back down to the zero line where it has bottomed in the last two

cycles. International demand continues to look ok based on the

weekly data out of FAS, but the USD is very strong right now and

may get even stronger, so that could eventually dampen demand

from overseas. On the positive side, we should only be couple of weeks away from the start of the holiday middle meat strength that

normally materializes in October and runs to the middle of

December, so that source of demand could be what comes to the

rescue and turns the cutouts and combined margin higher in early

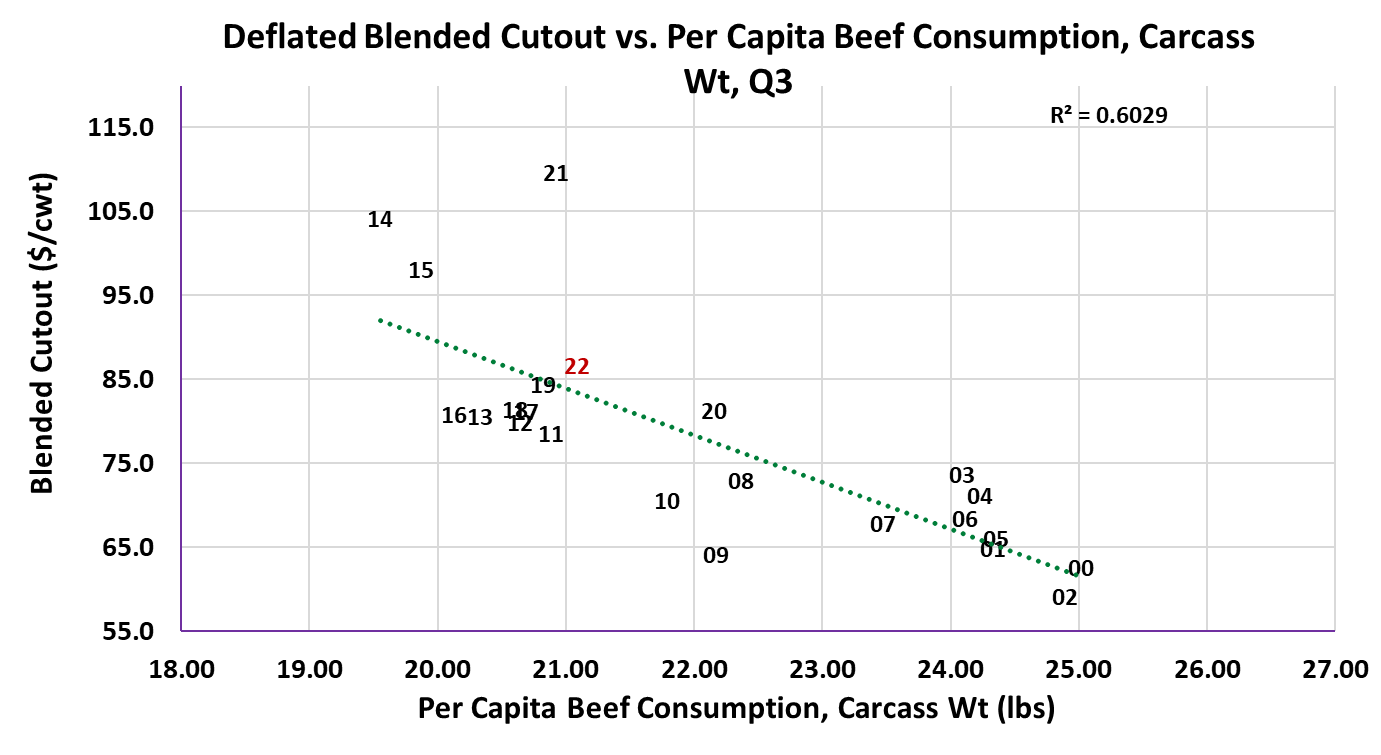

October. One thing worth considering is just how much demand

has already come down from 2021 levels. The attached scatter

diagram for Q3, which is nearly complete now, shows per-capita

consumption about the same in 2021 and 2022, but the price level

in 2022 is way, way below 2021.

It is almost back on the regression line. I think that Q4 will look

similar (2022 close to the regression line) and that is how I get the

Choice cutout averaging $255/cwt. in Q4. That isn’t very much

above today’s level. This week’s fed kill came in a little below

expectations at 516k. However, as we move into October, fed

supplies should tighten up based on past placement patterns and

we could see fed kills in October drop into the 500-510k range, or

perhaps a little lower. So, if the holiday middle meat demand

doesn’t turn the cutouts higher by early October, there is a good

chance that smaller cattle supplies and thus smaller fed kills will

provide some price support. Today’s Cattle on Feed report

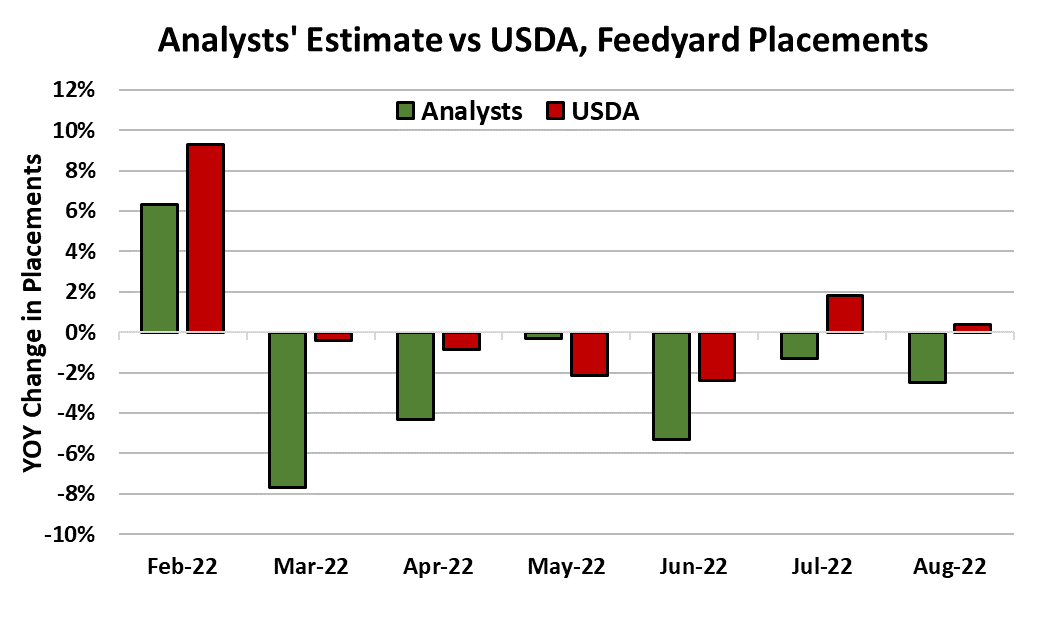

showed August feedyard placements up 0.5%, which was stronger

than the 2.5% decline that analysts were expecting. This is the

sixth time that has happened in the last seven months (chart

attached). Total on-feed inventories were reported to be about halfa-percent larger than last year also. So we are not going to run out

of cattle any time soon. This week, USDA gave us carcass weight

data for the week that included Labor Day and it showed steer

weights up a whopping 10 pounds from the week before. Some

increase in weights was expected due to the holiday, but a 10-

pound gain seems unusually strong.

That bumped the DTDS weights upward and while they are still

very low, they appear to be in recovery mode now. The percentage

of cattle grading Choice or better increased in this week’s data also.

Those two pieces of information have been the strongest evidence

for the supply-side bull case, but they could be losing some of their

luster now. I’m not ready to say that the cash cattle market is going

to fall apart because cattle feeders still seem to have a good bit of

leverage (as evidenced by this week’s cash price increase), but

maybe their grip on the cattle market is loosening just a bit. Next

week, it will be interesting to see how the futures reacts to the COF

report after all the selling that took place late this week. Also,

watch those outside markets also because today’s action made it

clear that traders are taking the potential for macro damage to beef

demand more seriously.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}