Beef Wrap September 29

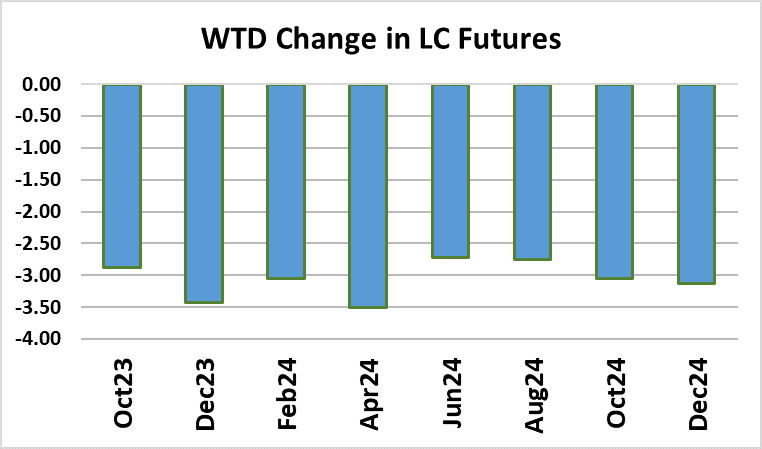

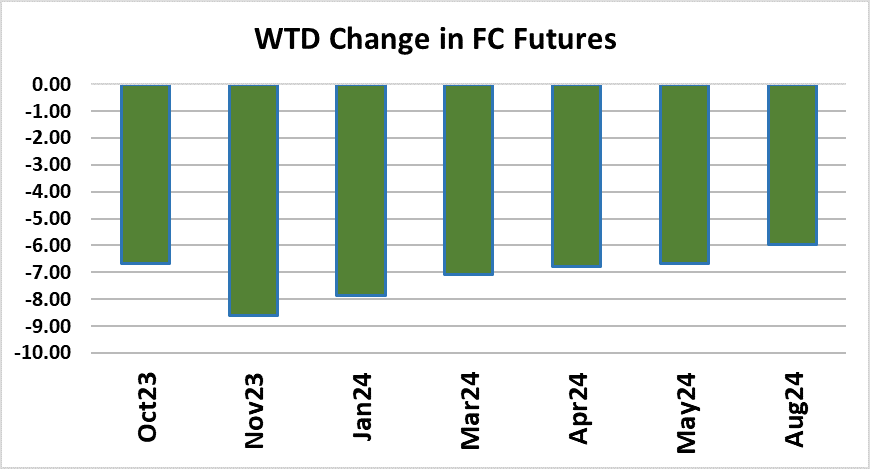

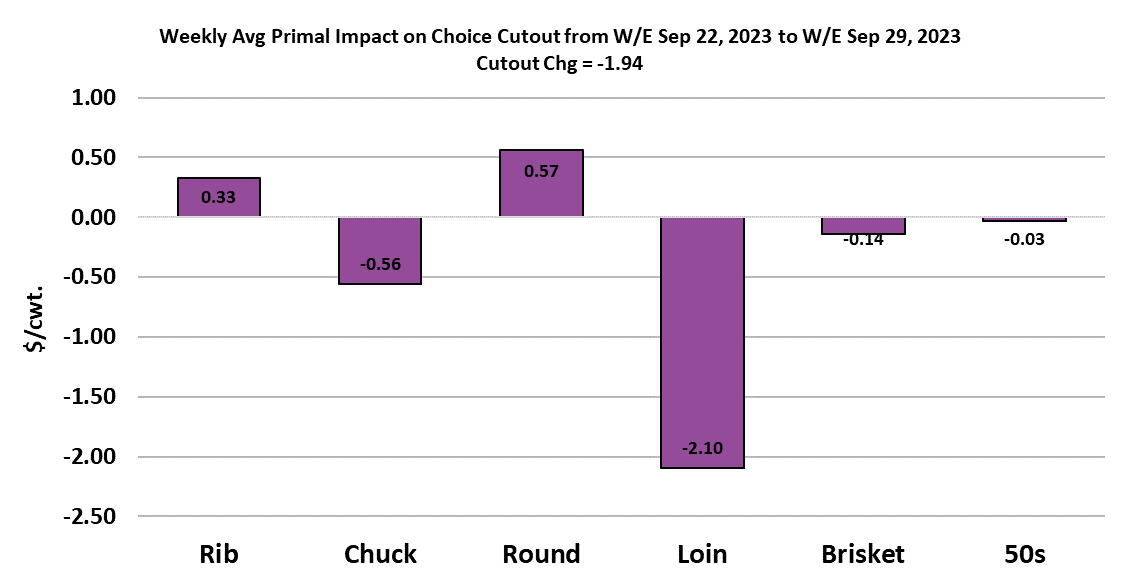

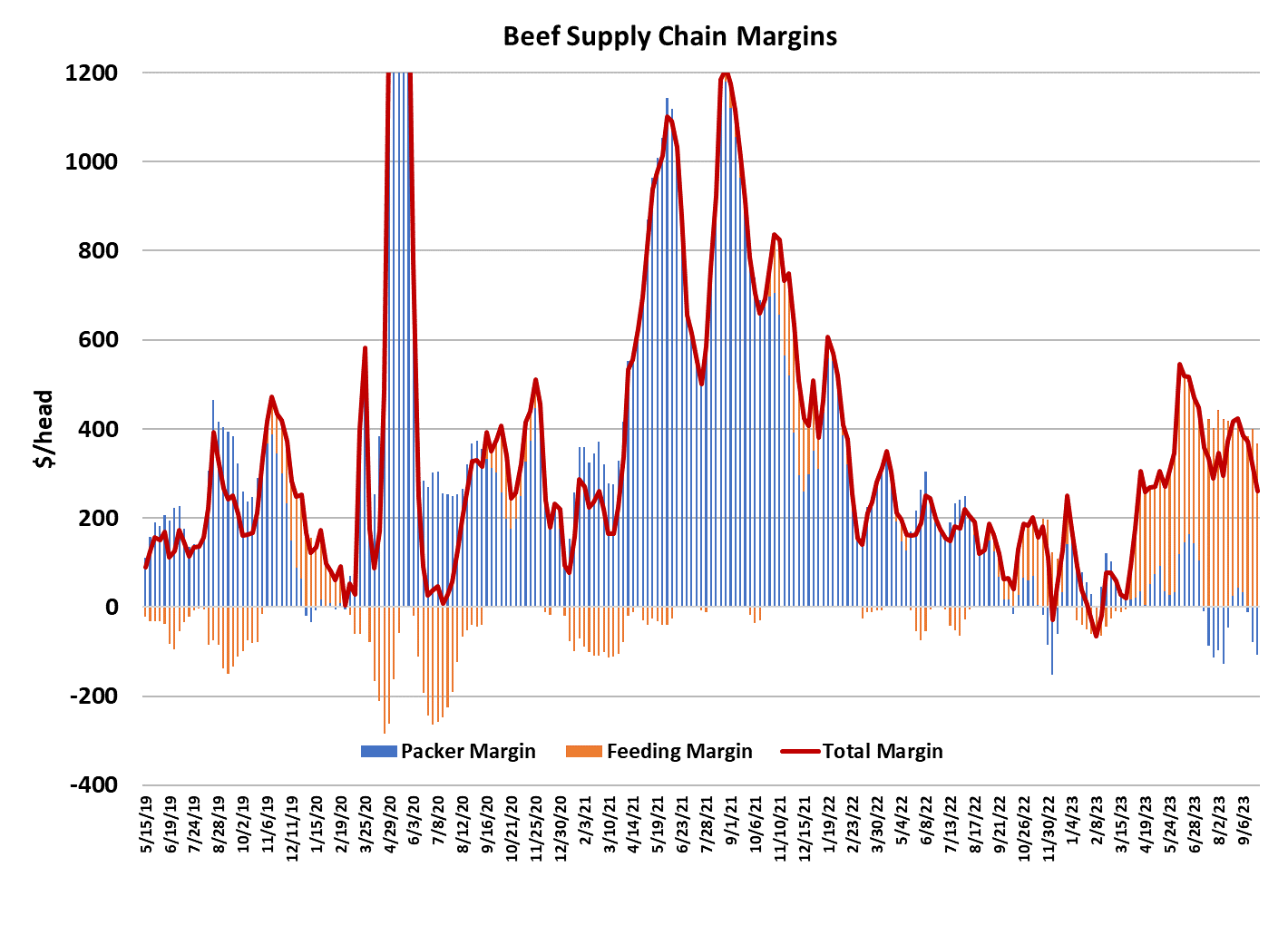

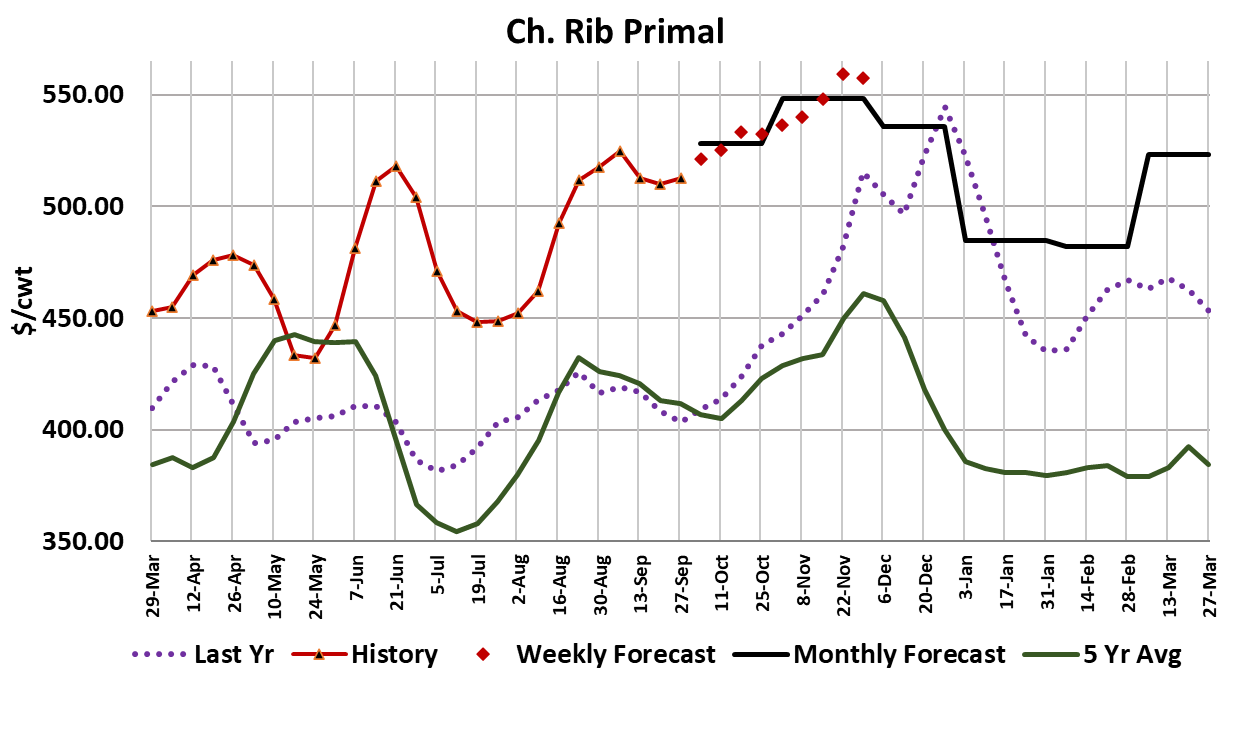

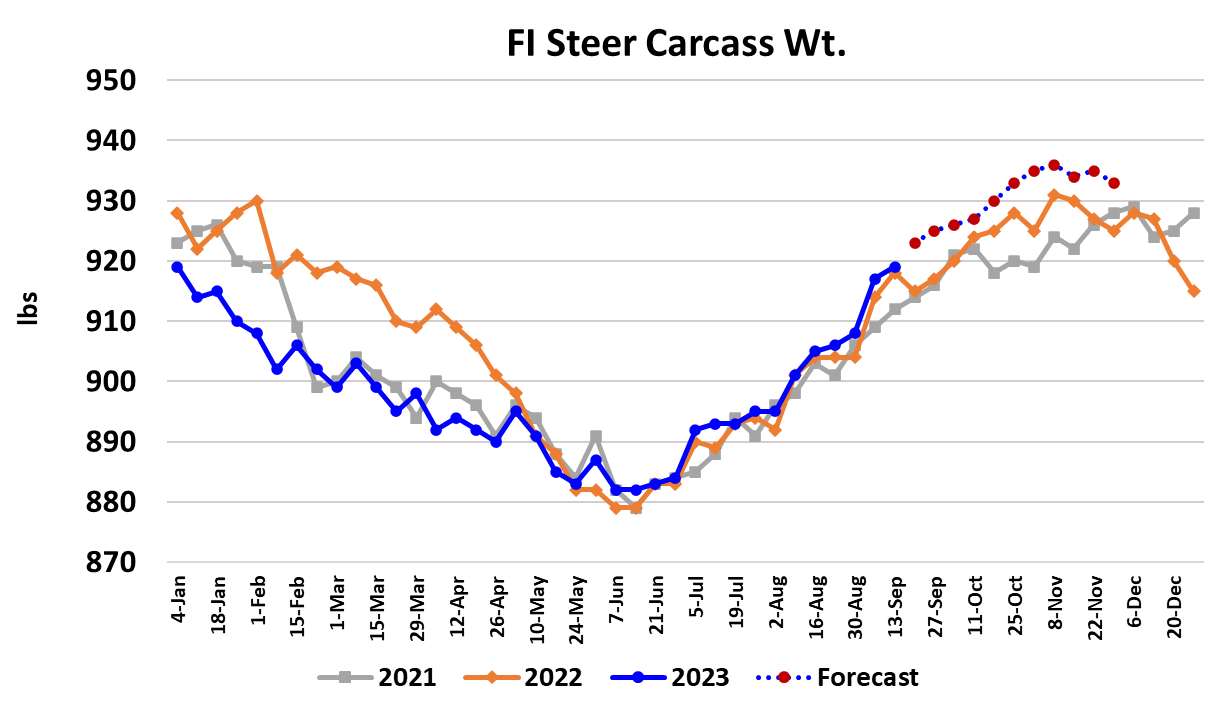

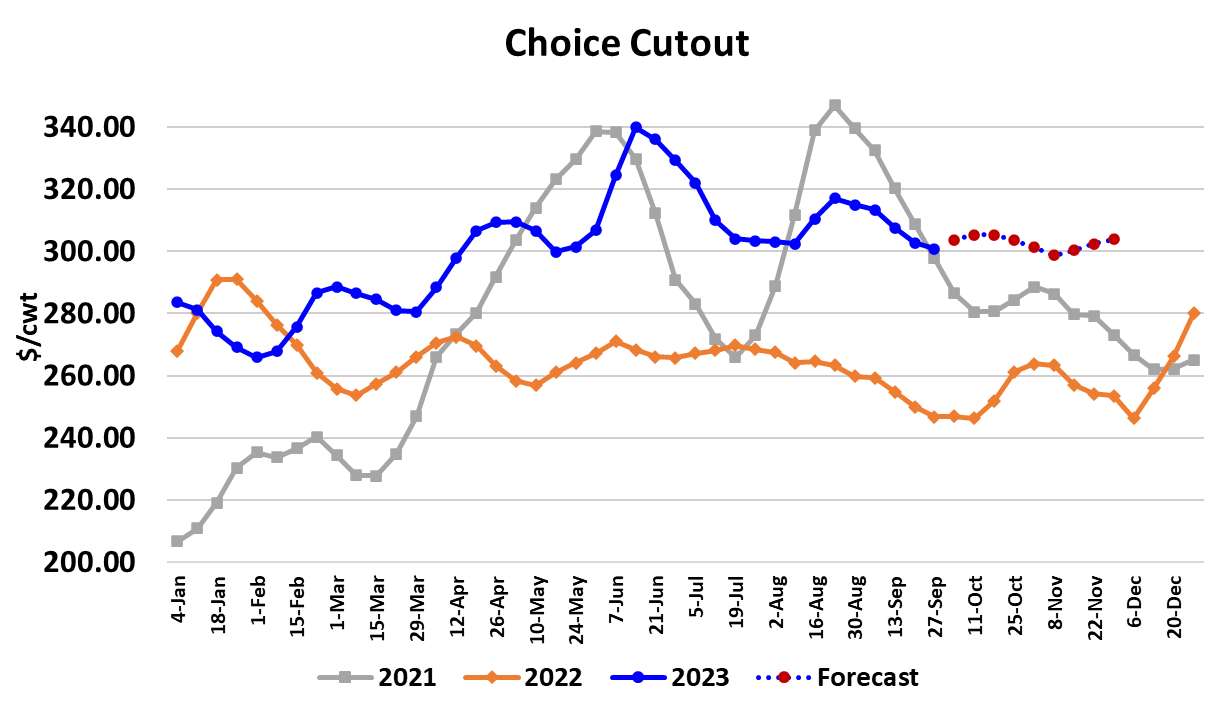

The spread between cattle prices in the North and South narrowed further this week as live cash trade in the North was about $1-2 lower than the week before while trade in the South was fully steady at $183/cwt. It looks like the average of all live sales was close to $183.80, which is down just a little less than $1 from last week. Outside markets really influenced the cattle market this week. The stock market sold off hard on Tuesday as traders became increasingly concerned over the gridlock in Washington that will likely produce a government shutdown this weekend. LC futures tanked right along with the stock market and packers were quick to offer steady money in the South and eventually they found some takers. The fact that packers were quick to offer steady money on a Tuesday tells me that they were concerned that they might have to pay more had they waited. It looks like packers bought fewer cattle than they did the week prior, but we won’t know for sure until USDA releases the totals for the week on Monday. Packers will have access to their October formula cattle starting next week, so that might reduce their need for spot market purchases. Packers also slashed the kill late in the week and so probably conserved a bit of inventory that way. The total fed kill only amounted to 475k, down 10k from the week before. Early in the week it appeared that packers were running hard because the daily fed kills were posting at or above 100k. However, they really dialed down the Friday fed kill (estimated at only 71k) and only scheduled about 6k for Saturday. It appears that packers are once again are going into margin management mode and with good reason because this week’s margin averaged -$107/head. The timing of this reduced kill might get the attention of beef buyers who normally start building holiday inventory in October. The cutouts slipped lower again this week, with the Choice dropping $1.94/cwt. on a weekly average basis and the Select losing $2.35/cwt. On Friday afternoon, the Choice cutout was dangerously close to slipping below the $300 mark. Market participants are anxiously awaiting some seasonal improvement in demand, but so far that hasn’t materialized. The combined margin is still tracking lower and that suggests that beef demand is still in a downcycle. Of course, it is always possible that this week’s small kill will catch some buyers out of position and thus “create some demand” as they battle with other buyers to get coverage. The rib primal did increase about $3/cwt. this week after two weeks where it trended lower. The attached chart indicates that it was the loin primal that had the biggest negative impact on the Choice cutout and one reason is that the tenderloins were down about 2% on the week. Clearly, the holiday demand hasn’t shown up there yet. It feels like the market is at a crossroads now. Either the normal seasonal demand improvement will show up and take the cutouts higher as is typical at this time of year or it won’t show up and that could leave the Choice cutout wallowing in the $290s this fall. I’d favor the former over the latter, but anything is possible. Traders seem to be more concerned about the demand side of the market more now than they have been in a long time. There are headwinds on the horizon. Student loan repayments are scheduled to restart in October and that will drain a lot of disposable income out of the economy. A prolonged government shutdown could also push the country closer to a recession and that wouldn’t be good for beef demand. Retail prices remain very high, and retailers have little appetite for lowering them it seems, so beef could lose some demand to the other proteins in the retail sector. On the other side of the coin is the tendency for improved beef demand heading toward the holidays and the fact that domestic beef demand has been very resilient over the past couple of years. Nearly every time I have wanted to forecast softening demand it has surprised me by holding up much better than expected. It feels like a significant gamble to think things will be different this time around. Carcass weights continue to press higher in normal seasonal fashion. USDA reported steer weights up 2 pounds to 919 this week and that comes after a whopping 9 pound gain the week before. I am looking for weights to top somewhere near 936 pounds in the middle of November. The DTDS weights remain low, primarily because the trend effect has been mostly absent in the last year or two and that is probably due to high-than-normal corn prices during that period. Feedyards appear to still be relatively current, but that is starting to slip and if packers maintain the kill at low levels for a few more weeks it could start to cause a mild backup in the cattle supply. For now however, it looks like the cash cattle market isn’t going to give much ground and so packers will just have to find a way to extract more money from beef buyers if they want to improve profitability. Next week, watch the cutouts for signs that this week’s small production is causing some buyers to scramble. If the market can’t manage at least a small increase in the cutouts next week, it is probably time to get concerned about deteriorating demand and price expectations will need to be adjusted lower.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}