Beef Wrap September 22

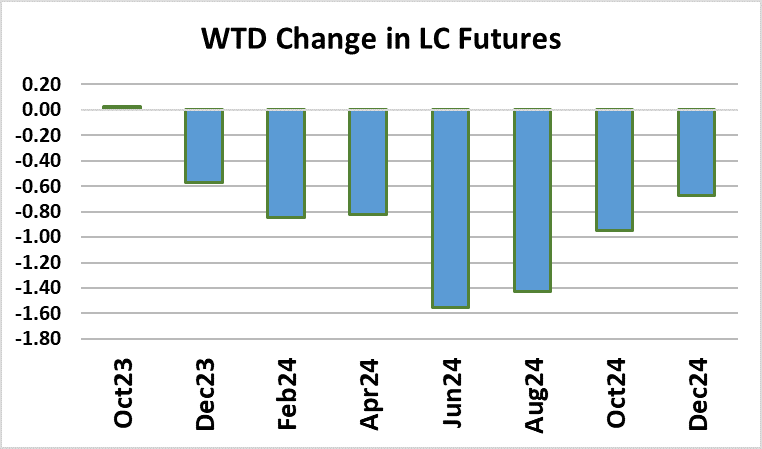

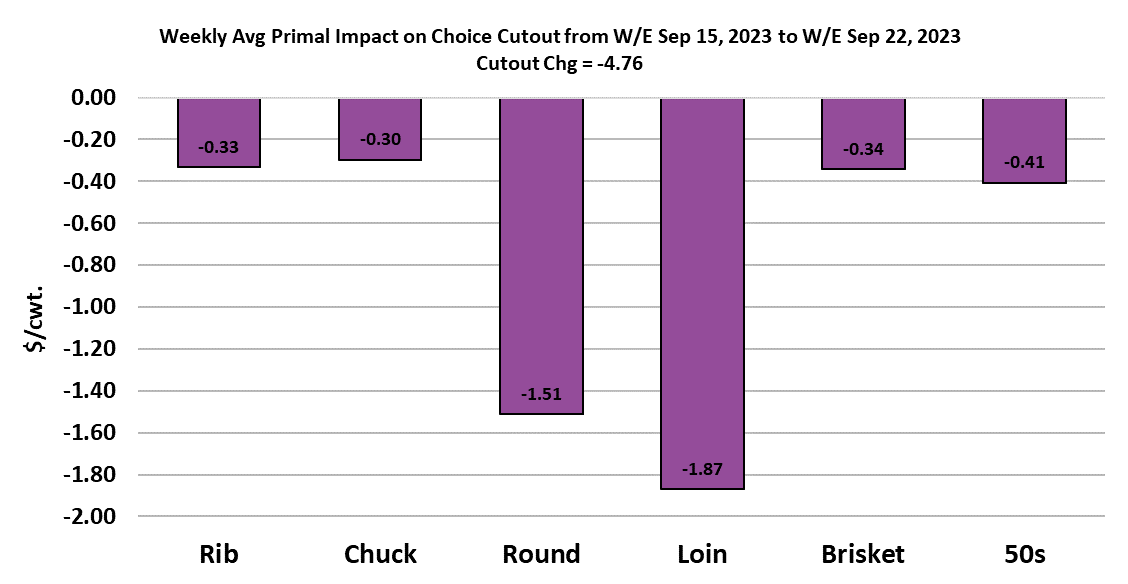

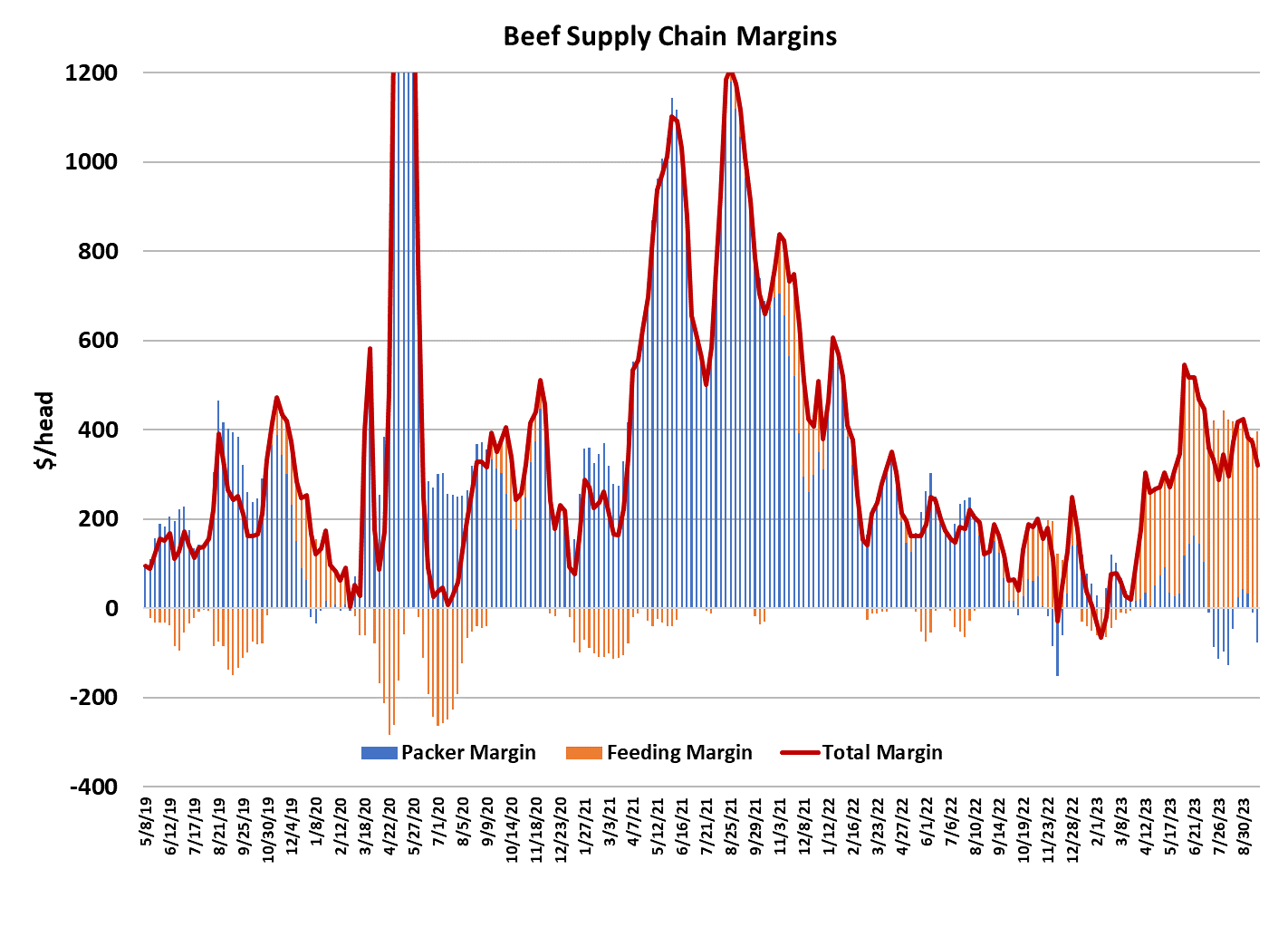

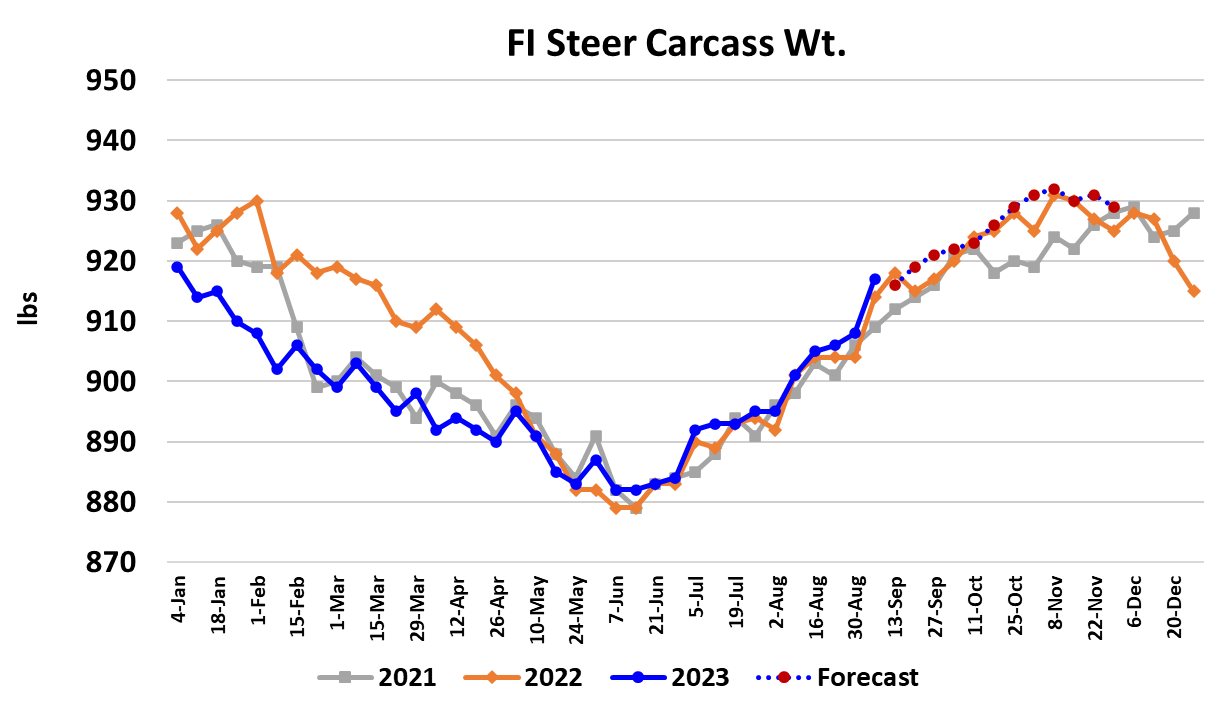

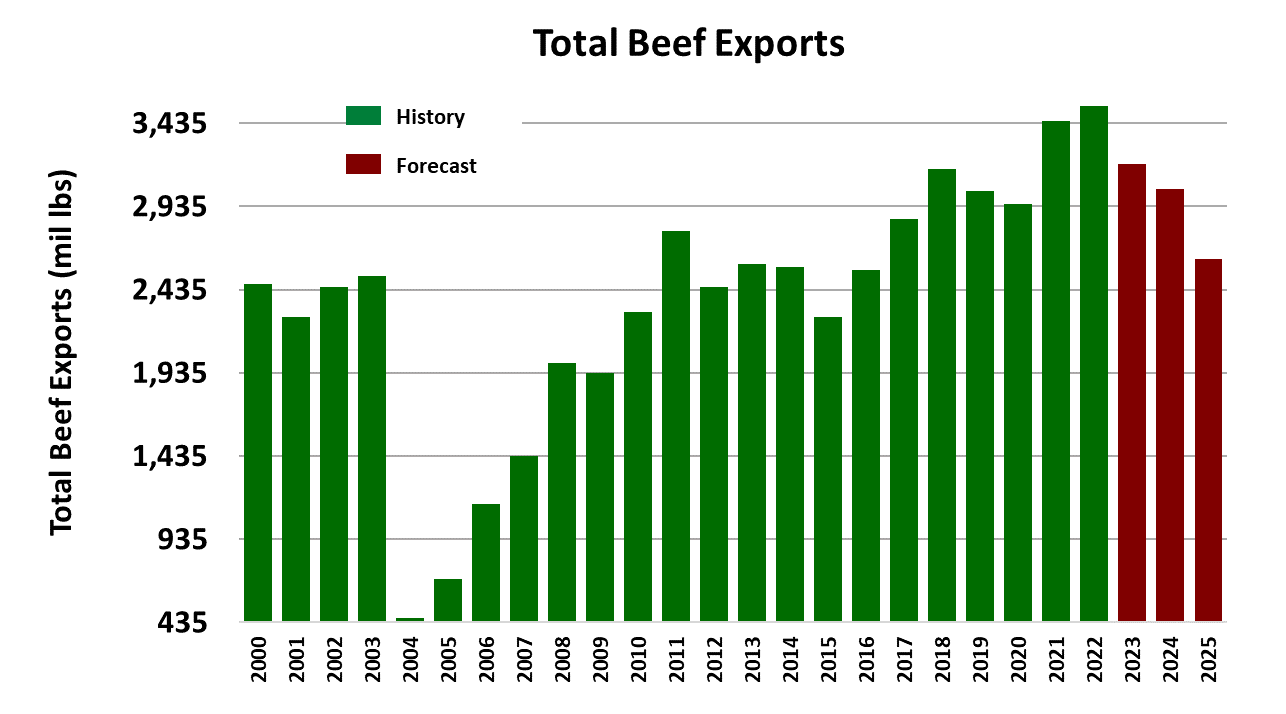

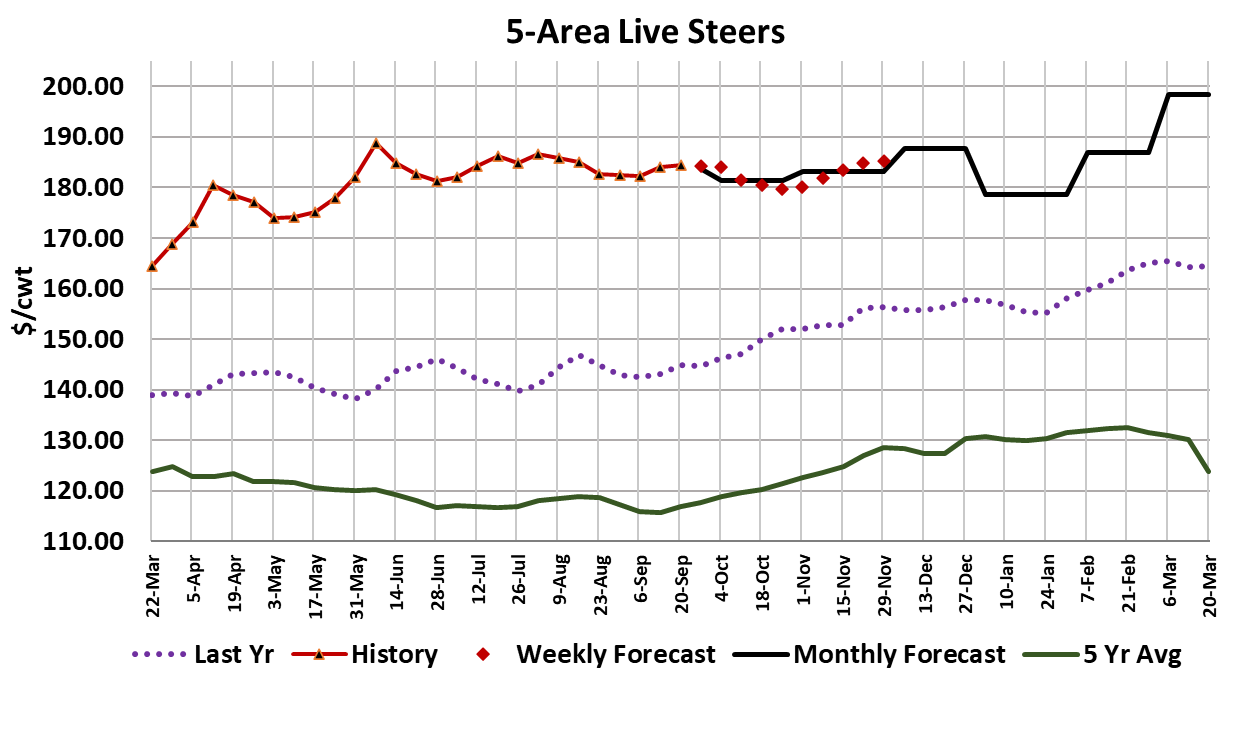

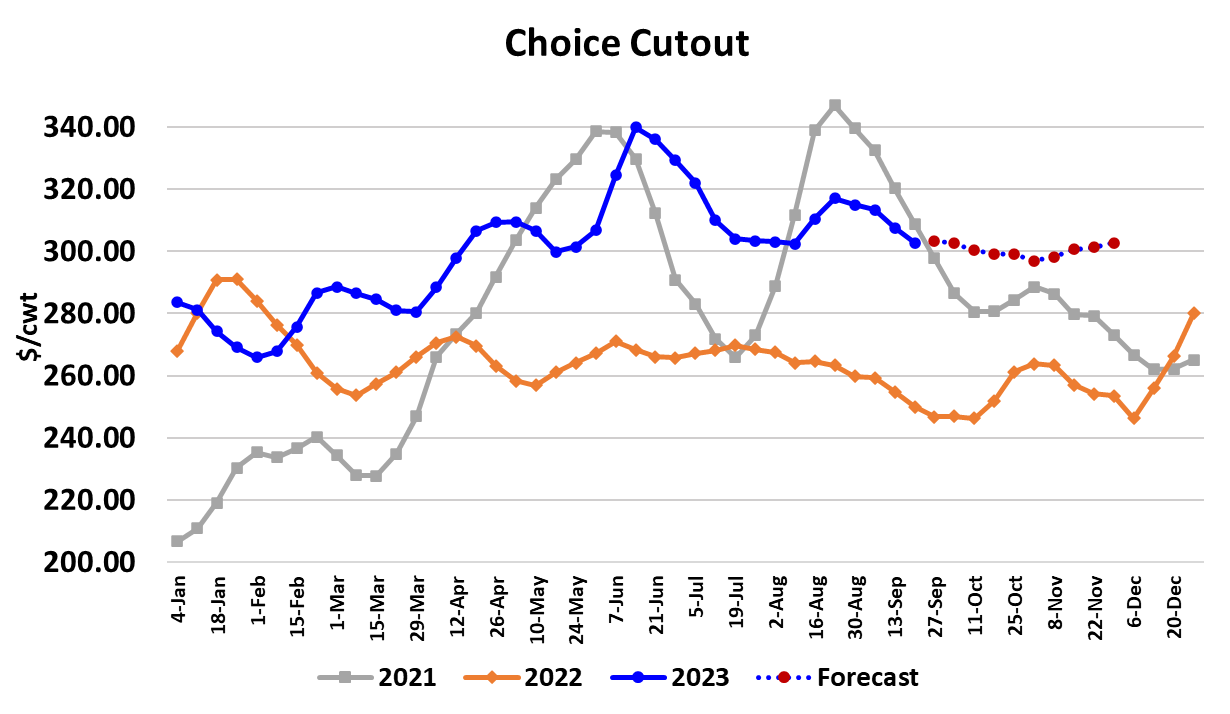

Packer margins sank deeper in the red this week as the cutouts moved lower while cash cattle traded a little bit stronger. The Choice cutout dropped $4.76/cwt. to average $302.79 and the Select cutout was down $4.62/cwt. to average $280.66. Rounds and loins were the biggest hinderance to the cutout this week, but all of the primals were lower to some degree. However, toward the end of the week, the cutouts started to firm, suggesting that packers’ kill cutbacks are beginning to get results in the beef market. The kill constraint hasn’t yet put downward pressure on the cash cattle market, with this week’s average live price coming in close to $184.50/cwt., up about $0.50 from the week before. In fact, I suspect that the average would have been higher had it not been for a general meltdown in commodity markets on Thursday, which drove the LC futures board sharply lower and thus probably softened producer attitudes enough that a steady cash trade became possible. Interestingly enough, the nearby Oct contract was nearly unchanged this week compared to last, but the deferred contracts were down, particularly the late 2024 issues. The Oct 2024 contract settled this week only about $7/cwt. over the nearby Oct 2024 contract. At this point in the cattle cycle, it is hard to believe that the shrinking cattle herd doesn’t warrant more than a $7 gain over 12 months. Maybe traders are expecting a much softer demand environment next year to weigh on prices. That certainly is a possibility, but it is very hard to forecast demand that far out with any degree of certainty. What is much easier to forecast is that cattle supplies and beef production will be lower in 2024. We are starting to get near the point in the calendar when buyers start to cover their middle meat needs for the holidays and that should help to shore up the cutouts, assuming that the end cuts don’t fall out of bed at the same time. The forecast suggests maybe a little more downside risk to the cutouts in the near-term, but I wouldn’t be surprised if they started working higher from here. This weeks fed kill registered 487k, down 12k from the week before, and probably reflects a renewed effort on the part of packers to restrict the kill in order to improve their margins. I calculate the packer margin at -$76/head and that is the worst margin since early August. That event back in August is what set packers on a margin improvement mission that resulted in restricted fed cattle slaughter for several weeks. However, since that time, packers let the kill creep back higher and now they are paying the price for that. I do think that the kill reductions will have a greater price impact this time around because beef buyers’ needs are more pressing at this time of year. As always, when the kill gets restricted, the beef market feels the impact very quickly, but the cattle market takes longer to respond. USDA reported steer carcass weights up 9 pounds this week, which might also have spooked some traders, but the report was for the week that included the Labor Day holiday and thus that probably goes a long way to explaining why the increase was so large. Heifer weights were reported three pounds higher. It sure doesn’t feel like cattle are backing up in feedyards, especially when packers have not had much success in turning cattle prices lower. The volume of cattle packers bought this week and last was a bit larger than normal, so that may help keep cattle prices contained next week, but I doubt that it will be enough to turn the cattle market lower. USDA released it’s monthly Cattle on Feed report this afternoon and it showed August placements down 5.1%, not too far off of the average analyst guess of -5.7%. Marketings were reported down 6% YOY, reflecting kill slowdowns that we saw during August. Expect the market to treat the report as neutral on Monday. The weekly trade data didn’t hold many surprises and beef exports continue to run soft compared to last year. That is to be expected given the smaller production and higher pricing that has materialized this year. Weak exports are likely to be a regular feature of the market for the next couple of years as cattle numbers dwindle cyclically. Next week look for the cutouts to be steady to perhaps a little higher and the cattle market to hold steady as well. Futures will likely remain range bound until something changes in the balance of power between cattle feeders and packers.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}