Beef Wrap October 6

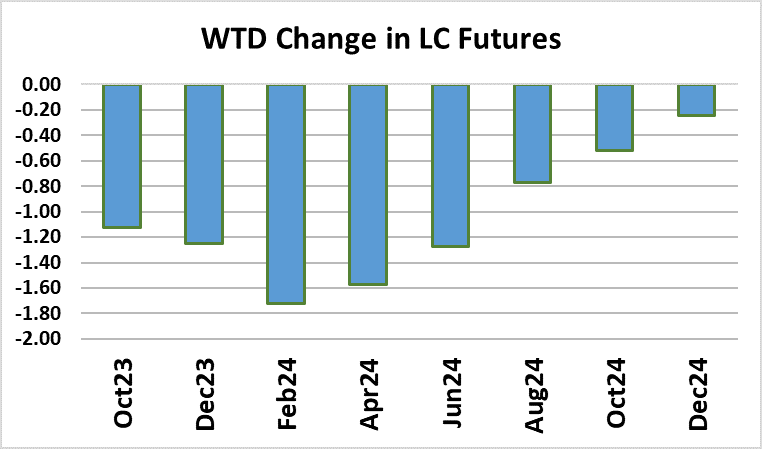

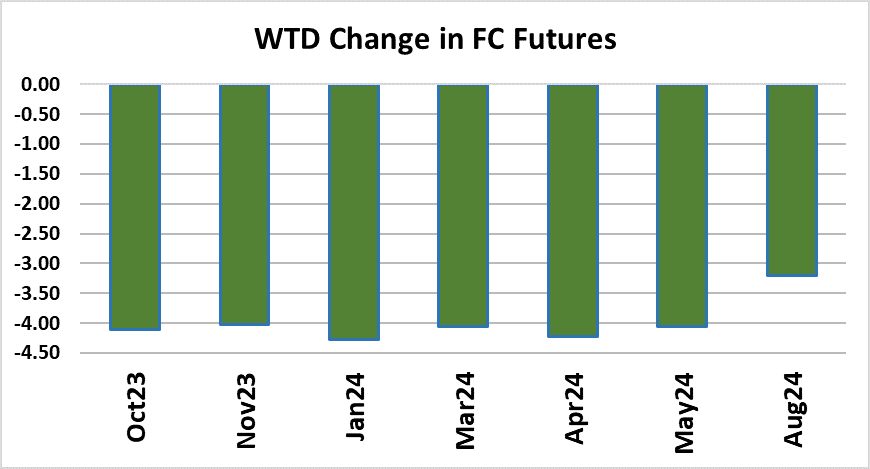

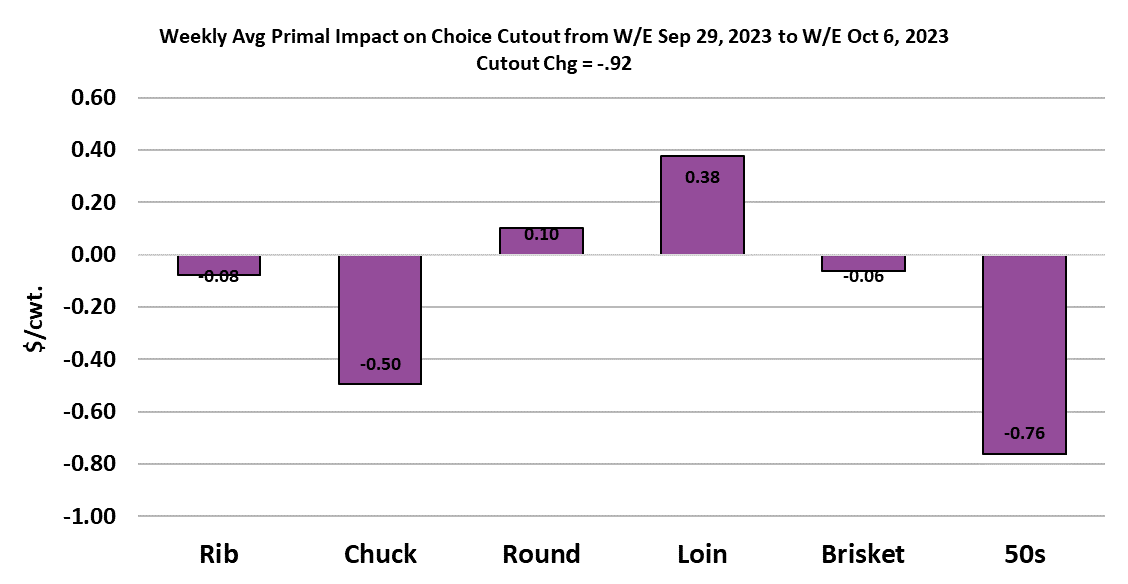

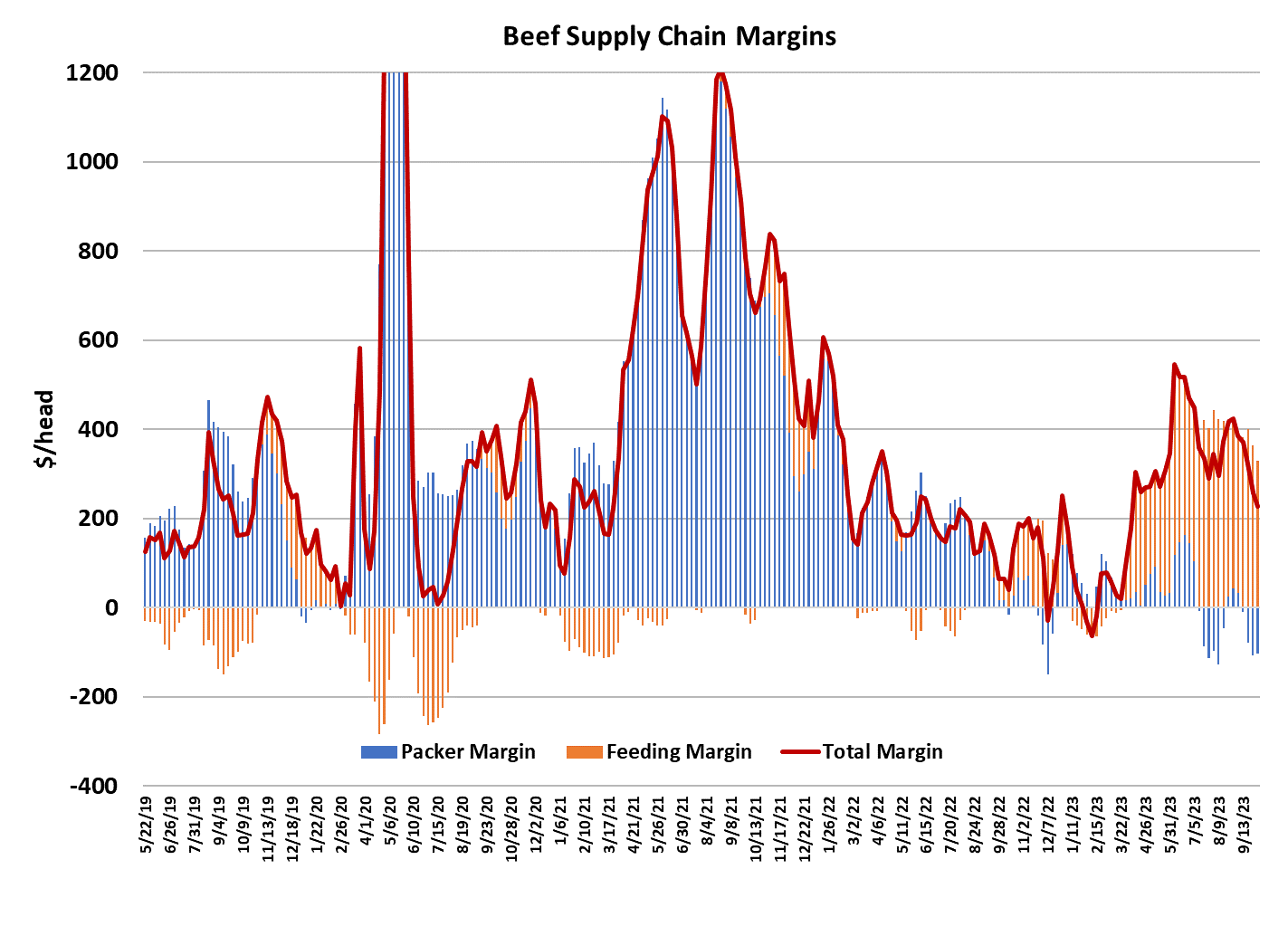

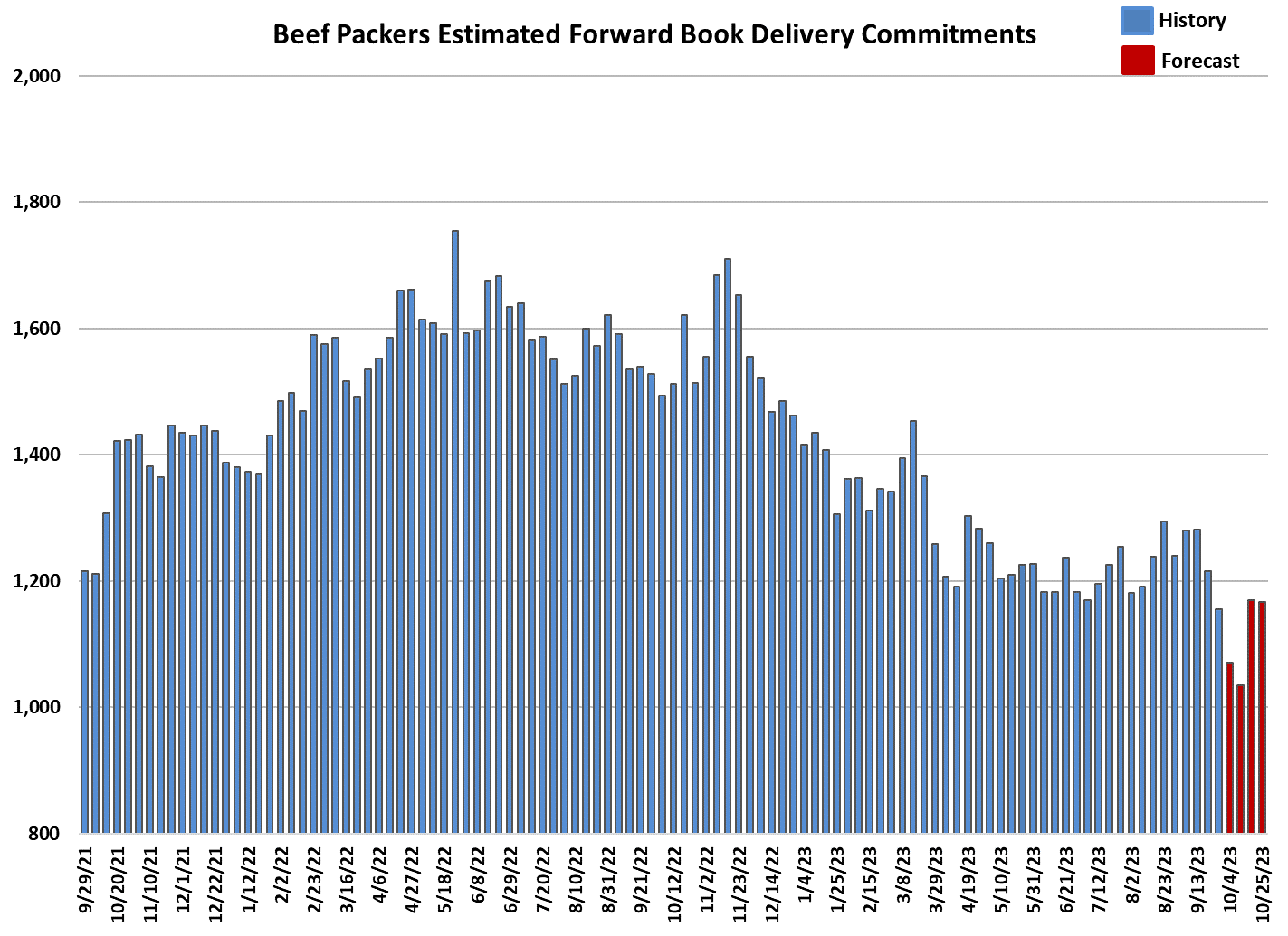

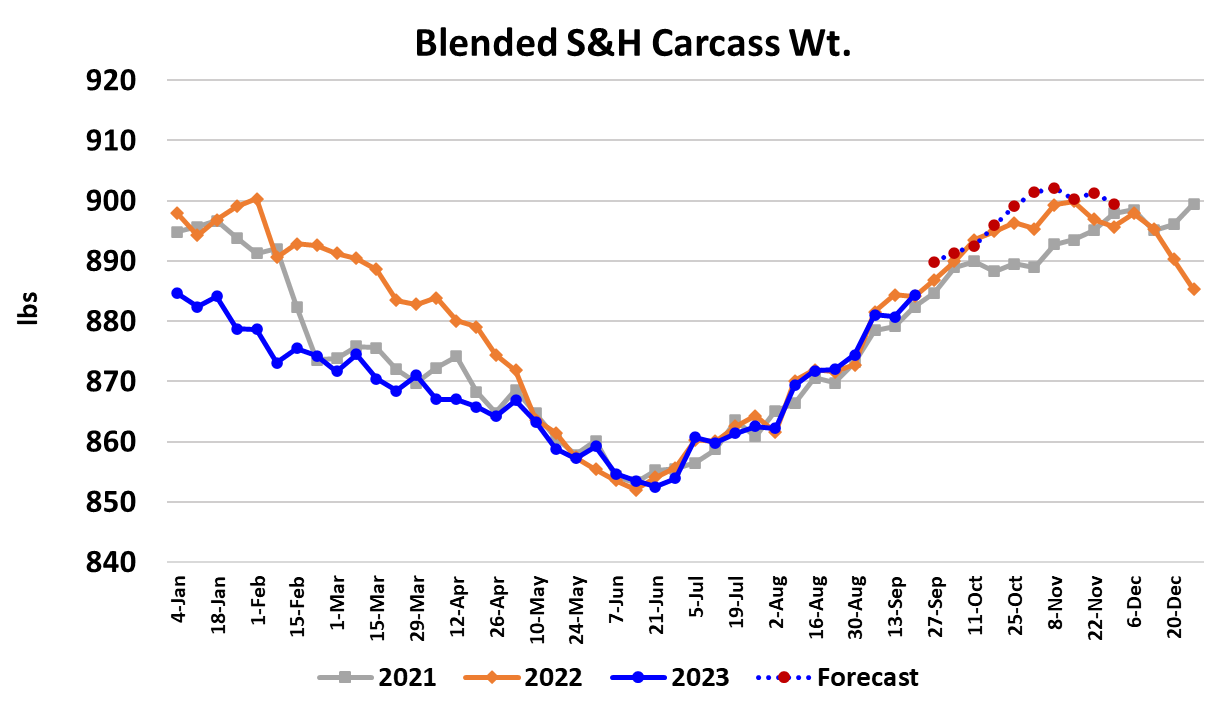

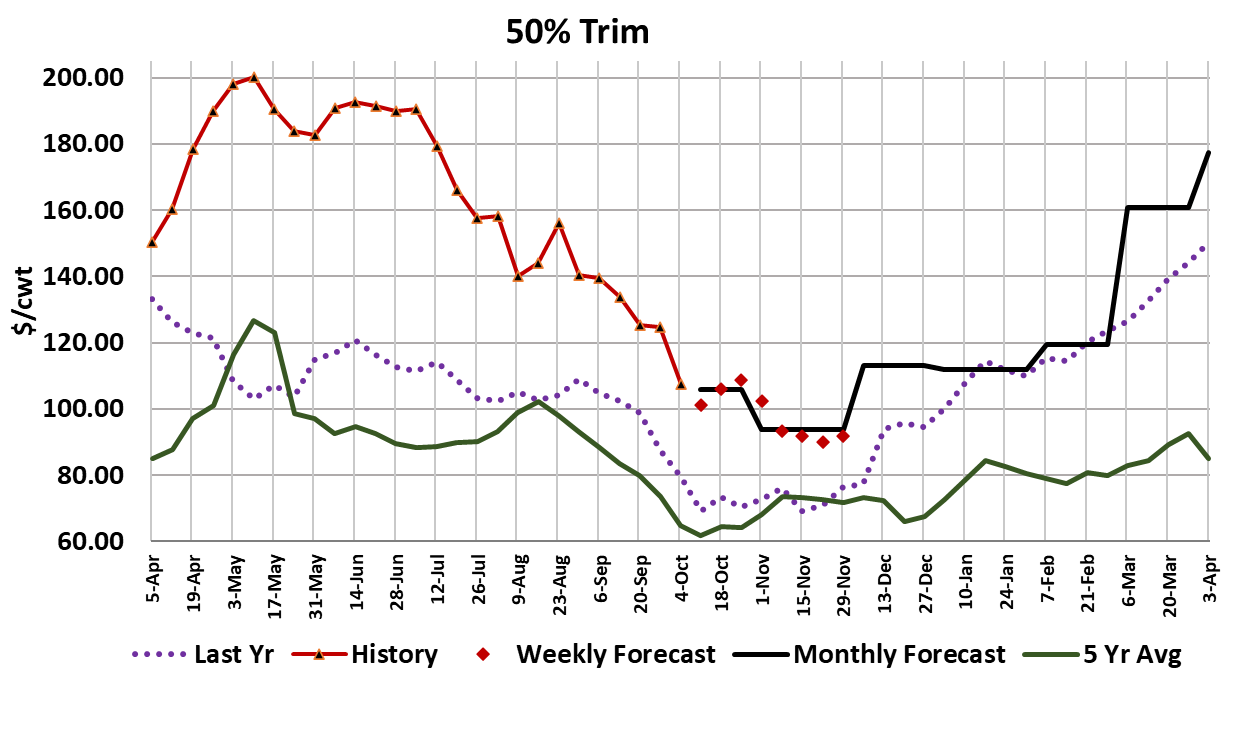

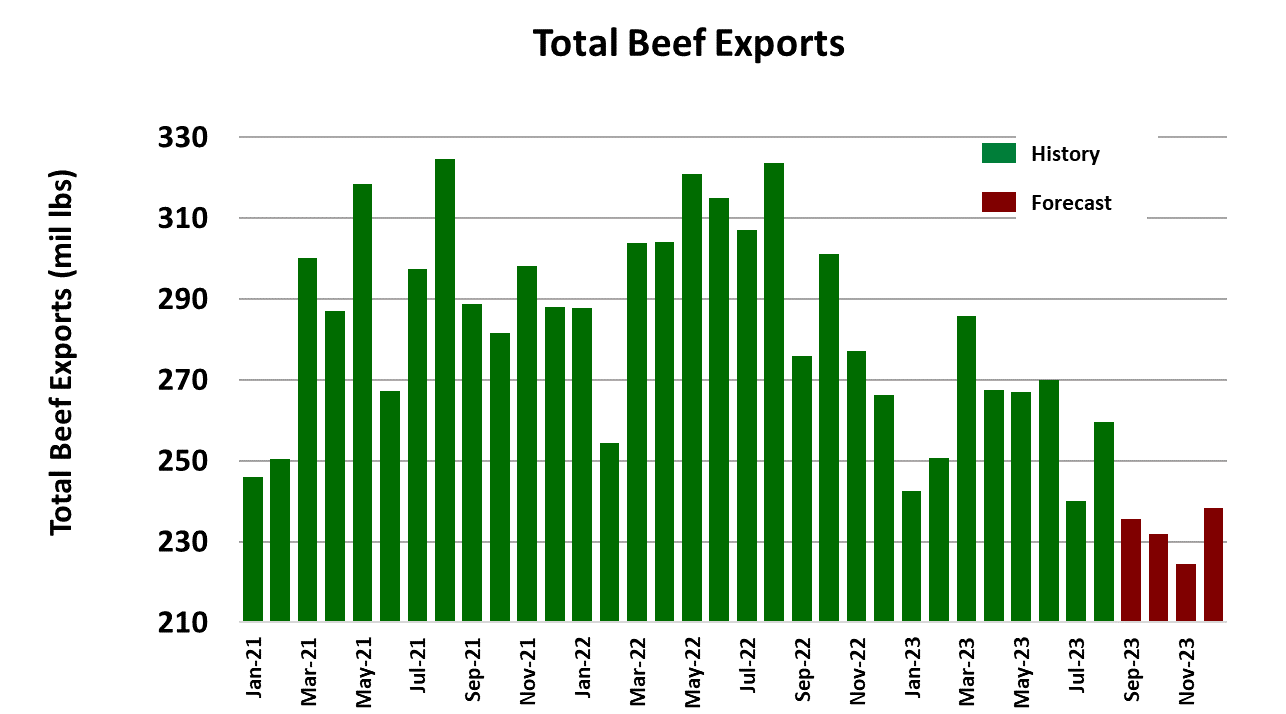

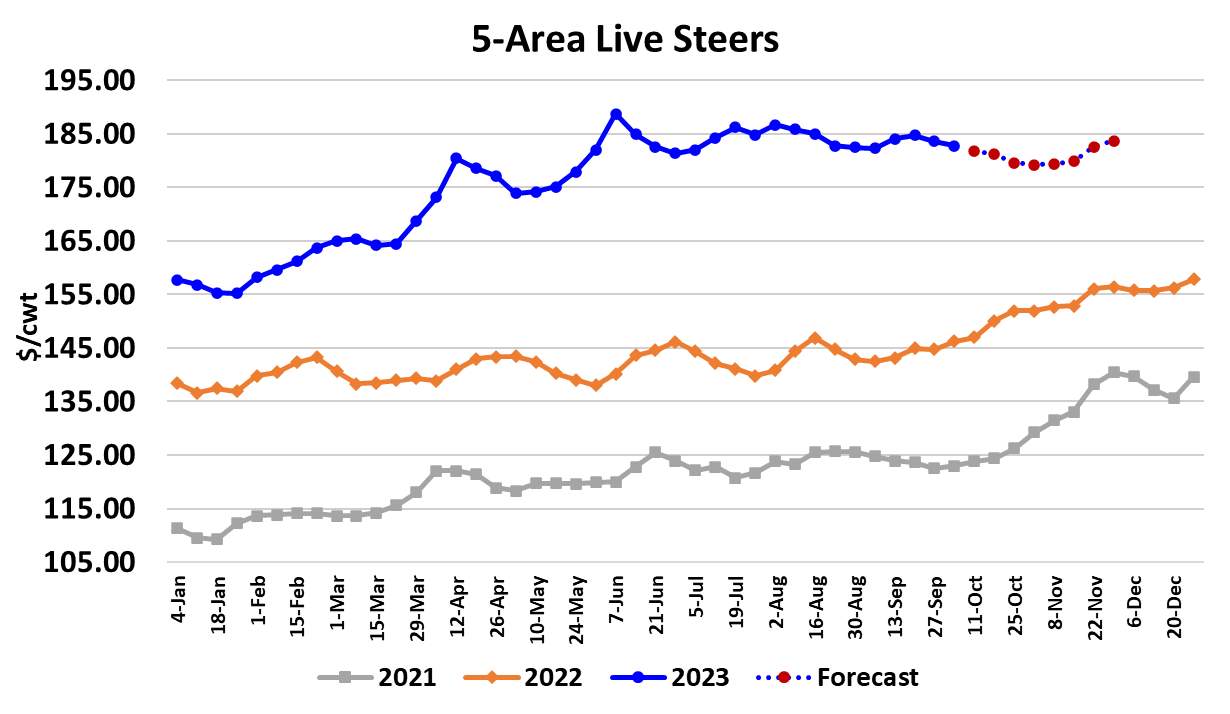

Prices in the beef complex eased a little lower this week with the Choice cutout losing $0.92/cwt. and the Select cutout dropping $2.71/cwt. The Choice cutout averaged $299.94 for the week, the first sub-$300 average since mid-May. The cash cattle market reacted very similarly to the week before when a downdraft in the equity market on Tuesday prompted packers to swoop into the cash market and bid lower for cattle in hopes that producers would bite. They did. In the South, the cash trade was at mostly $182, a full dollar lower than last week. The North traded a little lower on the week also with prices down $1-2 at $183-184. The average cash cattle price will likely be close to $182.75/cwt. when all of the data for the week is reported on Monday. However, it wasn’t all negative in the complex this week because USDA reported prices for the rib primal up sharply near the end of the week. The rib primal printed $535/cwt. on Friday afternoon, up $20 from the previous Friday. Does this mean that holiday buying is now underway? Possibly, but I don’t want to read too much into one data point. Let’s see how the rib behaves early next week. The loin primal provided the most support to the cutout this week and it was the tenderloins and butt tenders that were responsible for most of the gain, so that also looks like holiday buying. The 50s were the biggest drag on the cutout as they came crashing down to average $107/cwt., a full $17 below the prior week’s average. Cattle are getting heavier in normal seasonal fashion and that means greater quantities of fat trim are being produced. This week the blended steer and heifer carcass weight increased three pounds and may still have another 20 pounds of upside potential before they top and start to trend lower in late November. So, it is likely that the 50s have further to fall and may drop below the $100-mark next week. Fat trim hasn’t traded below $100 at all during 2023. I expect this trip below $100 to be brief and by December or January prices should be on the rise again. Packer margins were slightly better this week at -$103/head, up $4 from last week. If the holiday business is starting to happen, then we could see packer margins move quickly back into the black as middle meats carry the cutout higher. Light kills could help that process along. This week’s fed kill registered 487k, up 12k from the week before. I’m somewhat surprised that packers let the fed kill increase that much but maybe they are anticipating having to deliver on some booked orders. The forward sales report has been pointing to an increase in booked order delivery starting around the middle of October, but the near-term commitments look pretty dismal. A large forward book makes it difficult for packers to slash the kill in response to poor margins. Still, the increase in booked commitments is pretty small compared to historical norms so it might not have much of an impact this time around. Why have forward beef bookings fallen so hard since the end of summer? It probably has to do with uncertainty surrounding the general economy. Beef buyers are fully aware of all the potential macro headwinds that are currently in place and that likely makes them cautious about booking product in advance. That may mean that more buyers head into the holiday season with less coverage than normal because they are unsure whether or not consumer demand is going to hold up. Beef is a very expensive and perishable product. Getting stuck with product that won’t sell is a nightmare for retailers, but it is even worse to run out of product during the holidays and risk alienating customers. Beef buyers will need to be on their toes as they walk the fine line between too much and too little this holiday season. The combined margin is in decline once again, but that could quickly reverse if the holiday business heats up. Export demand remains very light as one might expect when supplies are tight, and prices are high. USDA reported August beef exports at 260 million pounds, down almost 20% YOY. Expect big YOY deficits to continue for the foreseeable future. The current forecast has beef exports down almost 15% YOY in 2023. The last time that we saw YOY exports decline more than that was back in 2004 after a BSE case in the US sent exports down a whopping 82%. The correlation between LC futures and equity markets seems to be very high these days and that is likely a reflection of the nervousness that market participants have about the macroeconomy and its impact on beef demand. Consumers have worked through most of their pandemic savings and are now dealing with high interest rates and price inflation. The sense of impending doom is palpable in the equity markets these days. Hopefully, it will pass without a significant market collapse. Next week, watch those ribs and tenders. It looks like they are finally getting going, but we need to see more data points to confirm. Don’t expect cattle feeders to willingly take lower money, but if the equity market turmoil intensifies, they might not have much choice.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}