Beef Wrap September 08

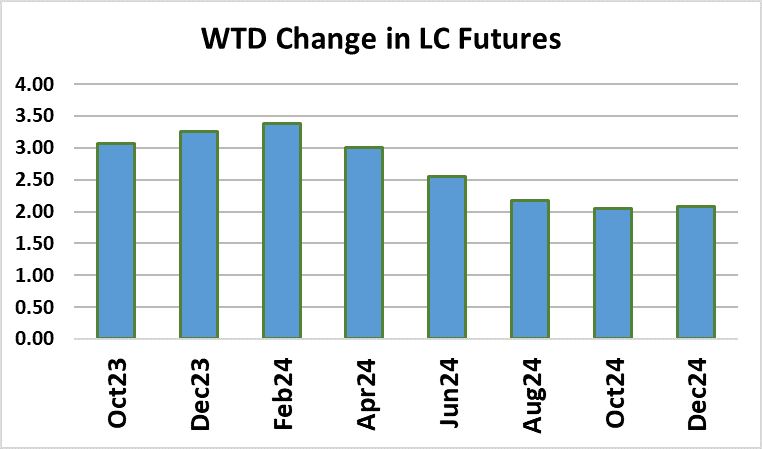

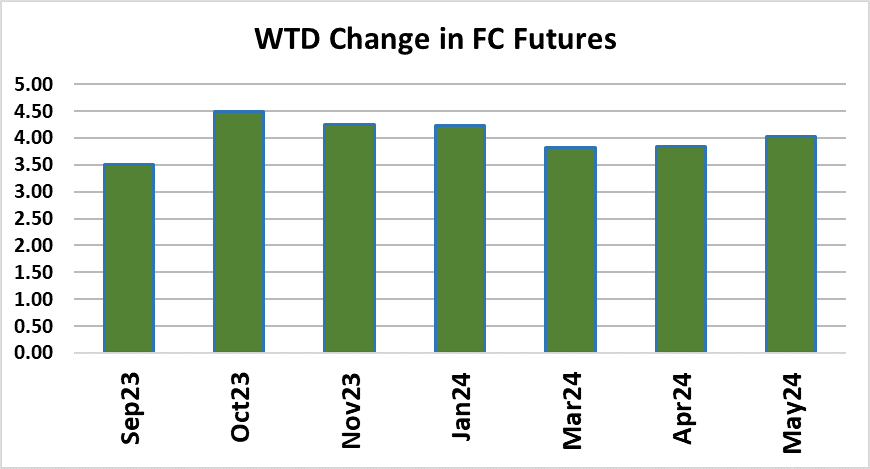

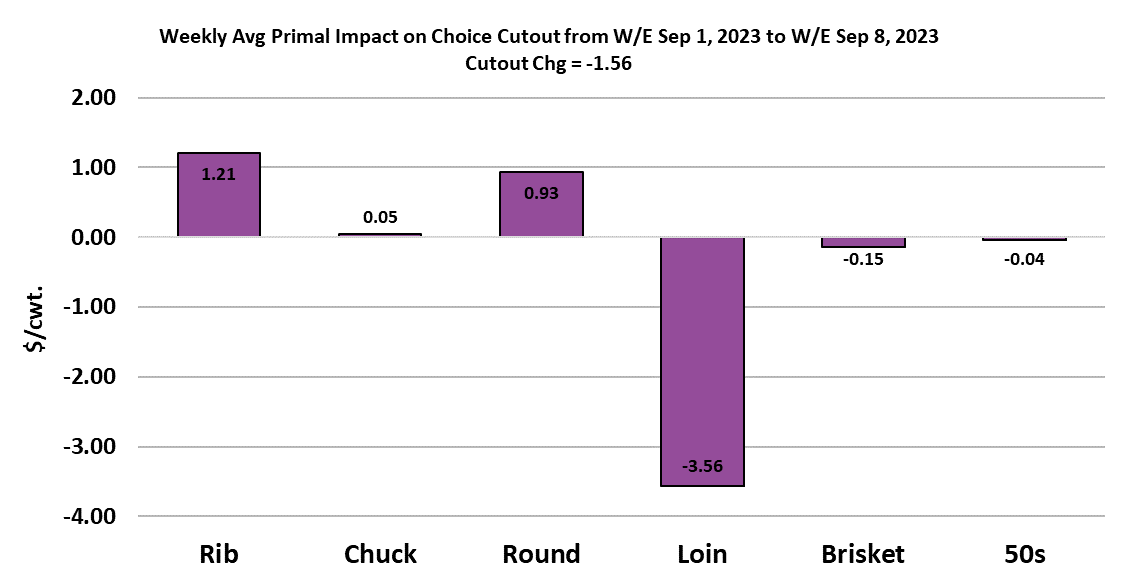

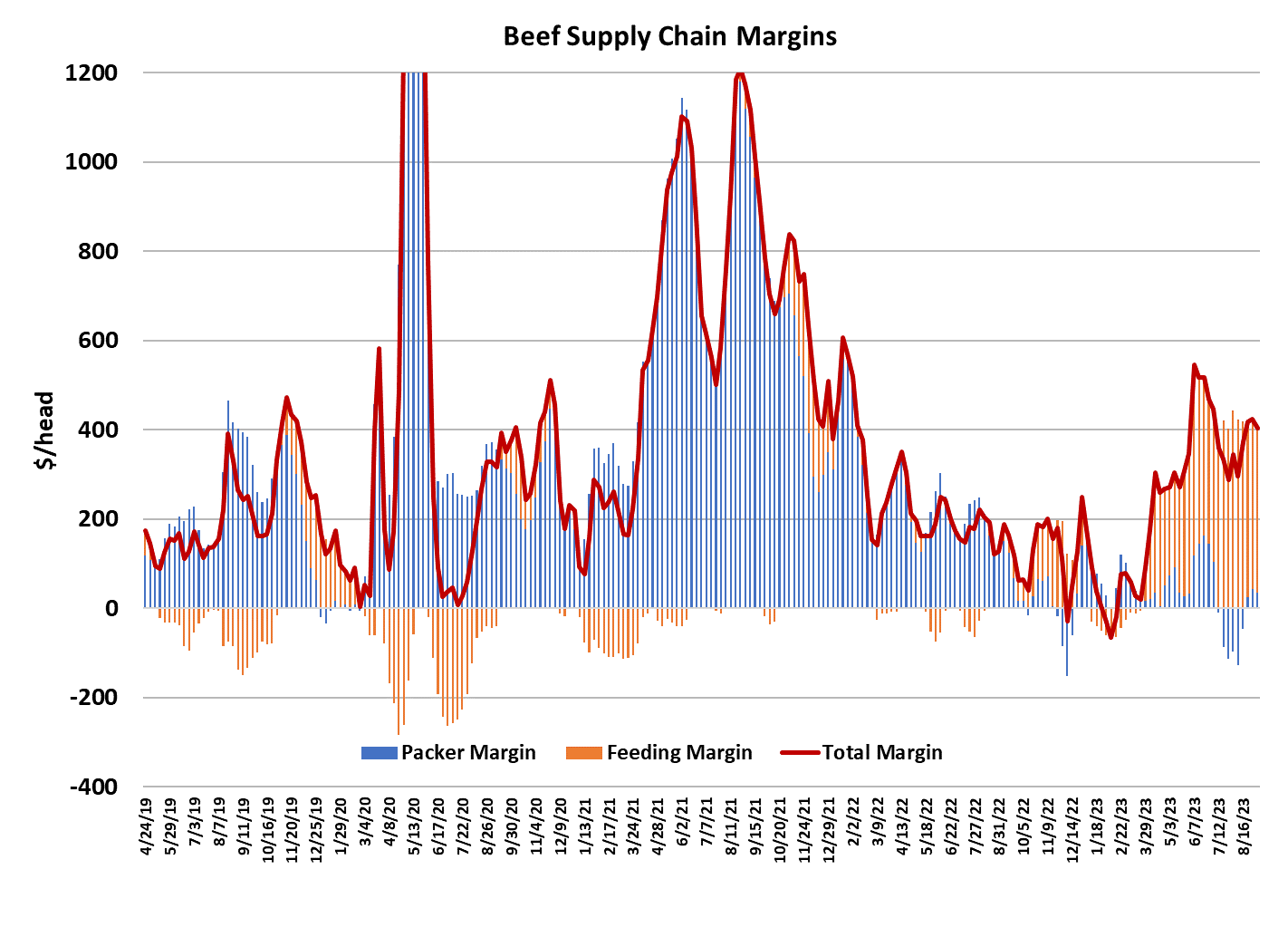

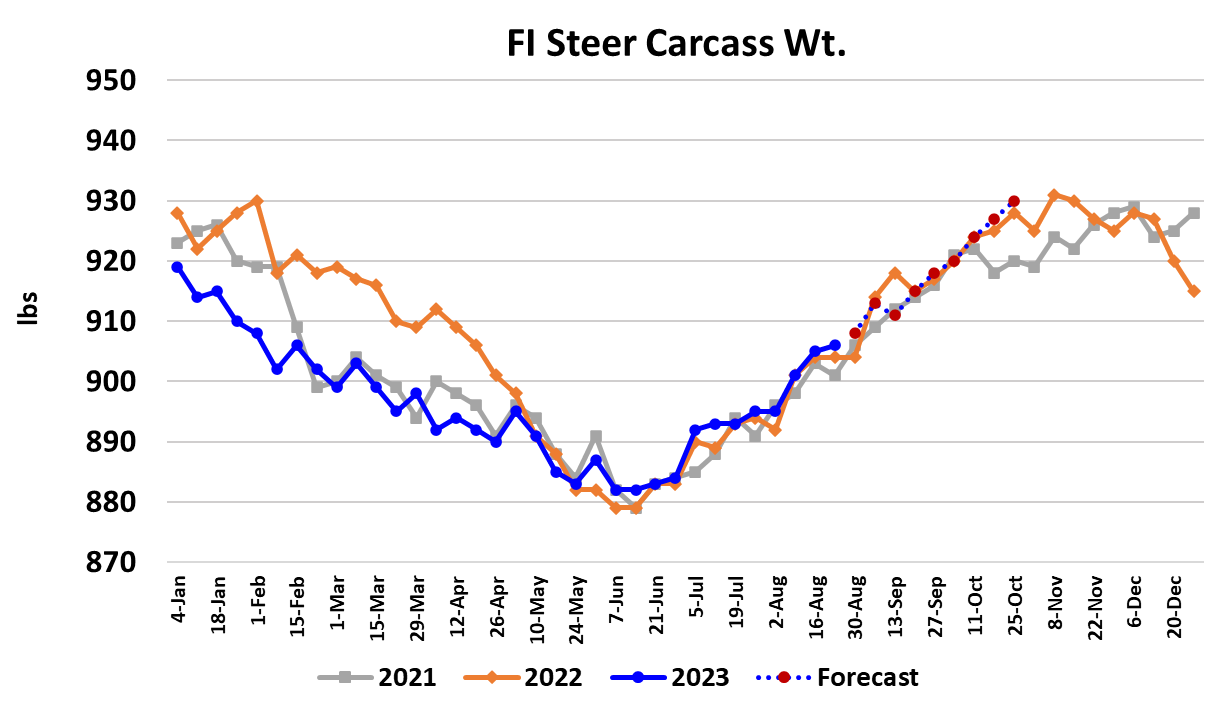

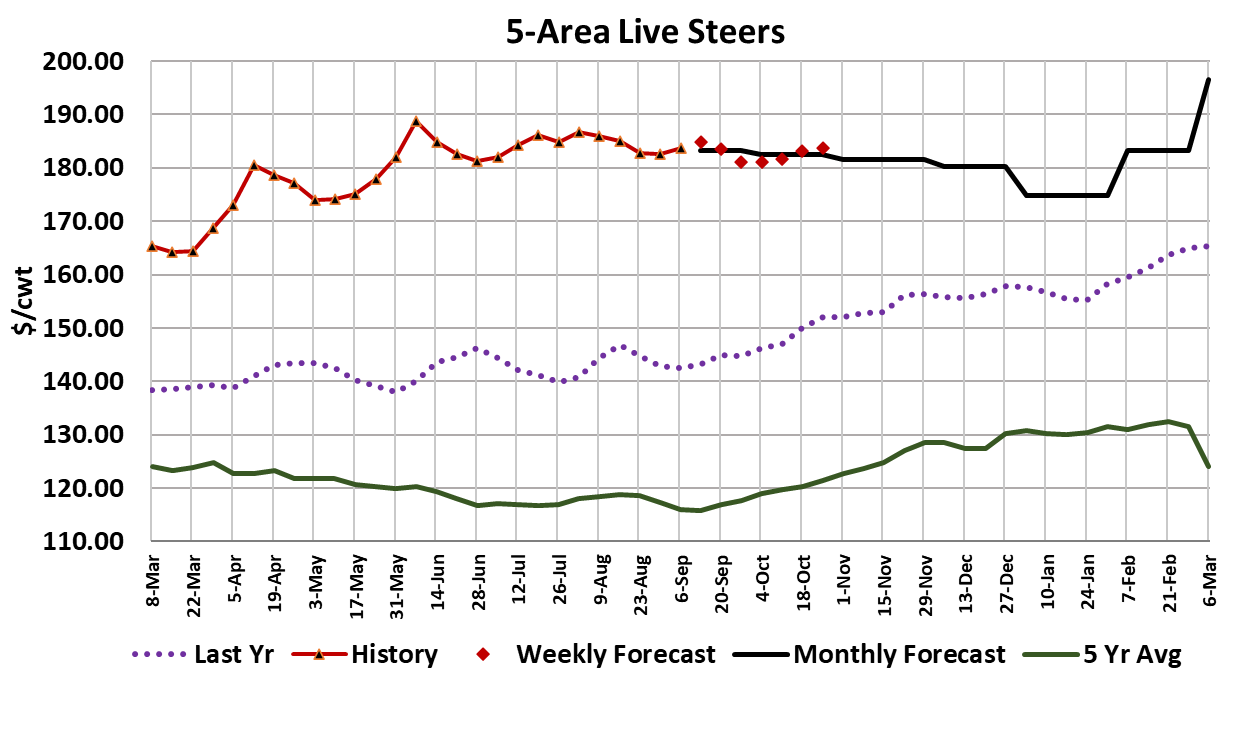

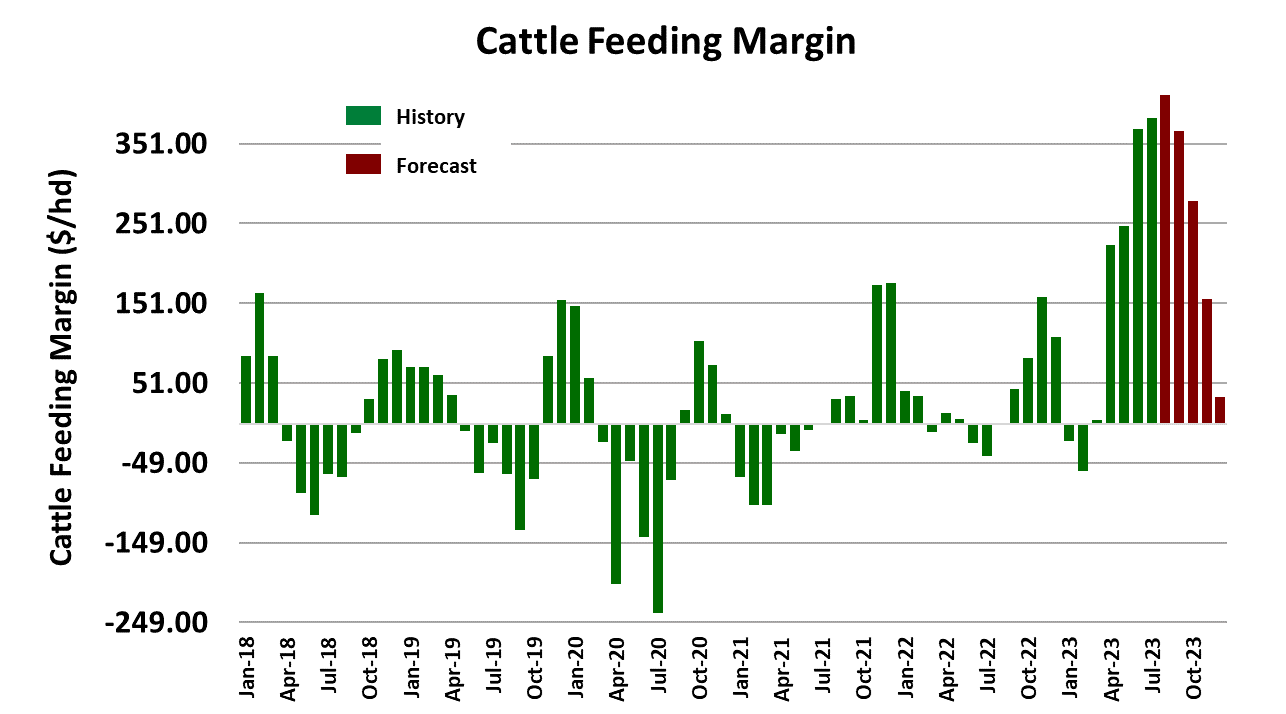

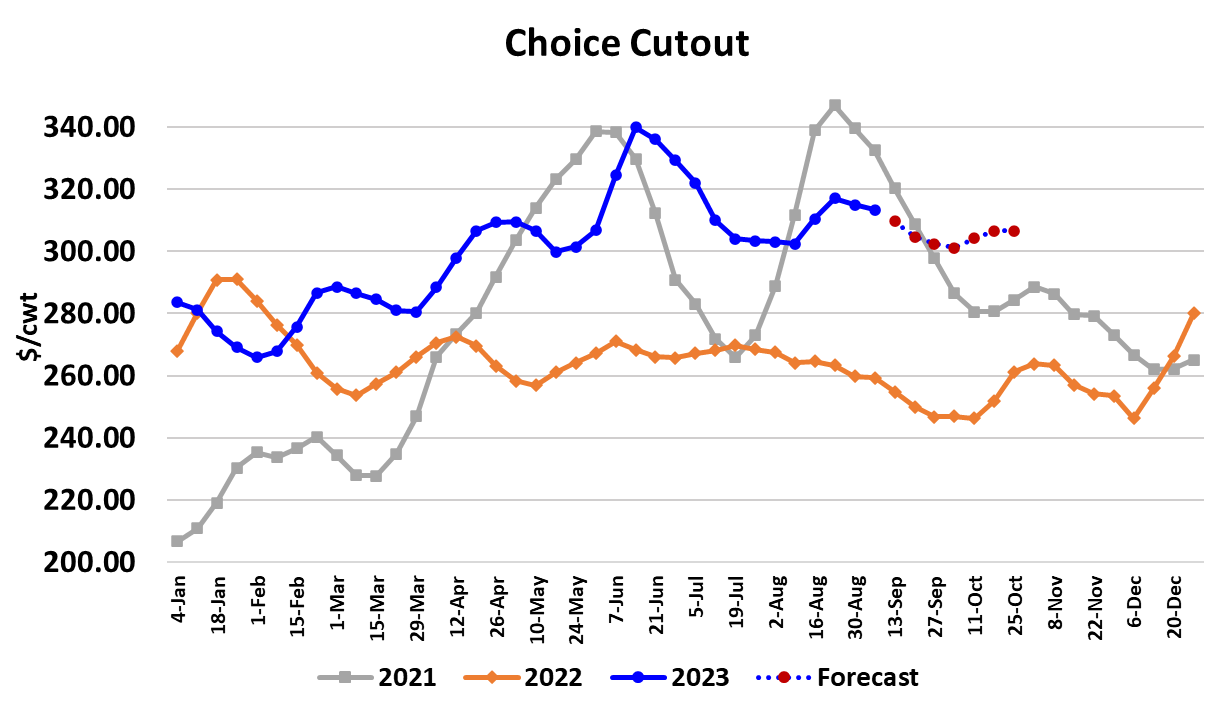

Last week’s short kill seemed to stabilize the cutouts, with the Choice only down $1.56/cwt to average $313.40 and the Select down $2.83 to average $287.34. The average cash cattle price appears as though it will be similar to last week’s $182.50, as packers were able to get cattle bought steady to a little cheaper in the North, but had to pay $180 in Kansas and Texas, which was up $2 and $1, respectively, from last week’s average. Unless a lot of additional volume gets reported on Monday, it appears as though packer purchases this week were rather light and that could have them back in the cash cattle market earlier than normal next week. The fed kill looks like it will register 439k, which is about 55k smaller than the week before. The fed kill scheduled for Saturday is only around 36k, which was way smaller than what I was expecting and could be a nod towards packers continuing to keep chain speeds slower than normal as they try to improve their margins. My calculation has packer margins this week at about $32/head, down about $11 from last week. If packers can’t get any additional lift out of the cutouts early next week, then their margins are likely to slip into the red once again. I think they feel that coming and will keep the kill constrained as a result. The flow model suggests that there should be enough cattle available to feed steer and heifer slaughter close to 510k per week, but packers probably know that if they push it that large the cutouts would crumble. Steer carcass weights were up one pound this week and continue to track very close to last year. The DTDS weights remain exceptionally low and that is an indicator that feedyards are very current in their marketings. Packers seem stuck between a cash cattle market that has been extremely difficult to pressure and a beef market that is well supplied and heading into a couple of weeks of likely softer demand. They will probably raise asking prices to buyers on Monday, citing the increase in their cattle costs at Southern plants this week, but I don’t really think they are going to have much success in talking the market higher—limiting production is the only path out of this mess for them. It appears that the worst of the heat wave is behind us now and cooler temperatures will prevail through September. There will also be some fresh, new crop corn entering into rations in the next few weeks. Those things together generally support faster weight gains and thus could cause feedyards to lose some currentness, especially if packers remain disciplined in keeping the kill down. USDA provided the trade data for July this week and it showed total beef exports down 21.8% and beef imports up 18.3%. As a result, the US was a net importer of beef during July. That pattern of small exports and larger imports is likely to remain in place for at least a couple of years as US beef production shrinks and there is a need to supplement domestic supplies. This week, cuts from the loin primal were the biggest drag on the cutout while both ribs and rounds were supportive. The price strength in the ribs continues to surprise and makes me wonder if there is going to be much of a set back in rib prices this month. The futures market was excited to see higher cash develop in the Southern Plains and that led to strong gains this week. Open interest surged higher, making it look like new money was coming into the market. I guess speculators don’t want to miss out on what some perceive as a very strong pricing environment in Q4. I’m not as optimistic because there are likely to be some headwinds on the demand side that could hold prices in more of a sideways pattern through the balance of the year rather than pushing them straight up. Consumers are getting stretched and gasoline prices are on the rise. Student loan payments restart in October. Retailers continue to raise the prices that consumers see and don’t seem to have any intention of lowering them. All of that could work together from the demand side of the market to neutralize the positive influence of reduced beef availability. I still have some modest declines forecast for the cutout over the next 2-3 weeks and then I think we could see them work higher as the holiday middle meat business starts to energize. Packers have shown a willingness to dial back the kill for margin reasons, and I suspect they will need to continue to employ that strategy for at least a couple more months. Next week, expect another sub-500k fed kill, moderately lower cutouts, and a steady cash cattle market. Packer margins should compress further, but cattle feeding margins should stay very lucrative.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}