Beef Wrap August 26

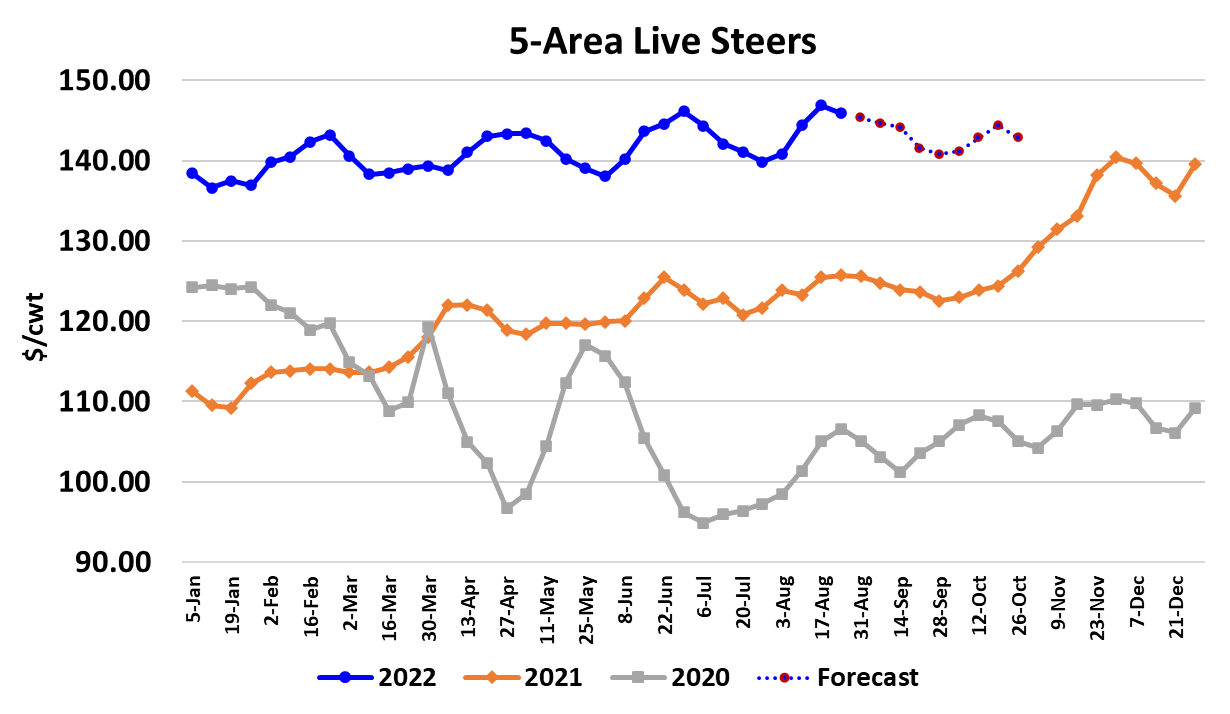

Beef packers finally found a way to cool off the cattle market—just buy a lot less cattle. It looks like this week’s average cash price is going to come in around $144.50, down a little over $2 from last week’s average. However, packers only bought about two-thirds of the volume that they purchased in the prior week. That suggests that perhaps they are planning on a pretty light kill next week as we head toward Labor Day weekend. A smaller kill might also help the cutouts, which were a little lower this week. The Choice cutout dropped $1.29/cwt and the Select was down $0.21/cwt. Cutout values are still not moving very much. This week it was strength in the ribs and rounds that was a little more than offset by declining prices in the loin and chuck primals.

Packer margins shrank to about $150/head since they were killing those expensive $147 cattle from last week. Now that they have succeeded in buying cash cattle cheaper, the challenge for packers will be to keep the beef from sliding lower next week. All of the Labor Day buying is now complete and if retailers are

gearing up for post-Labor Day features, they will likely be most interested in end meats and grinds. The middles will come back into focus around the beginning of October when the typical middle meat price run-up ahead of the holidays gets going. I am forecasting middle meat prices in Q4 well below last year on the idea that per capita consumption in Q4 will be close to last year, but demand will fail to live up to the strong showing in 2021q4. The demand picture got a little darker with today’s 1000 point selloff in the equity markets.

On the positive side, the data seem to indicate that inflation is cooling a bit, but equity traders threw a fit because the Fed indicated that it won’t back down from raising interest rates anytime soon. Traders want their punch bowl back. Competing

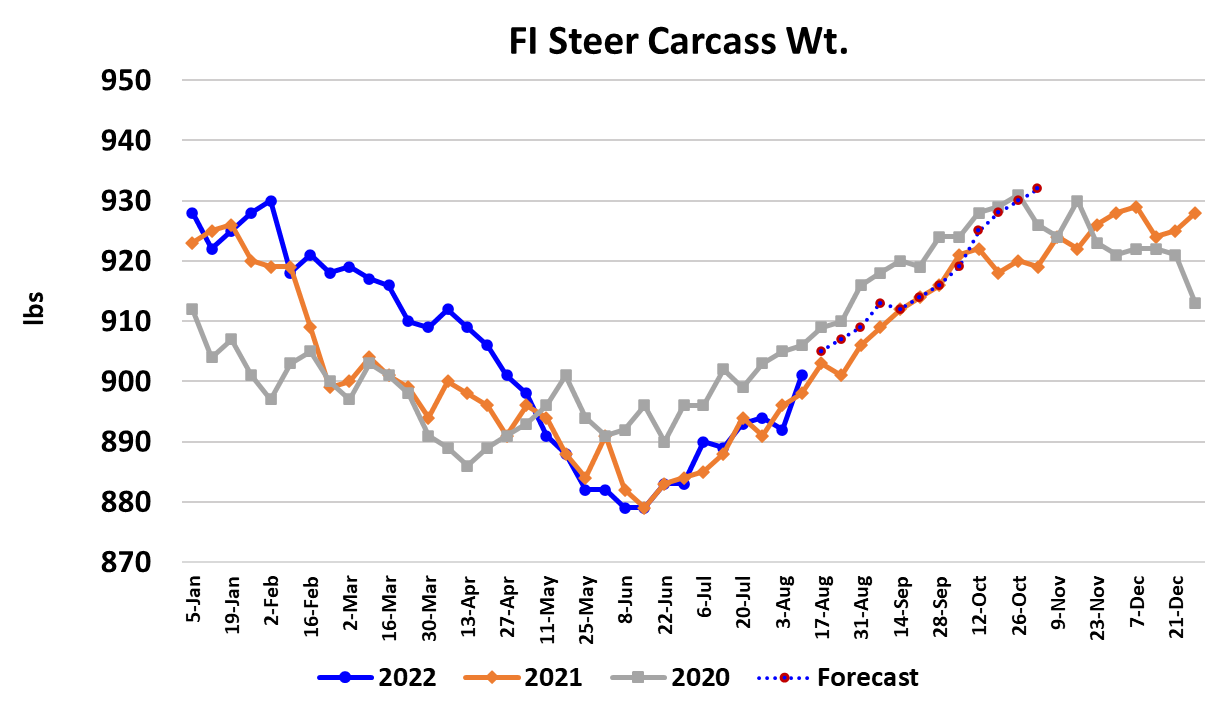

meats are also getting cheaper by the day. Chicken prices are moving steadily lower and it looks like production prospects could improve over the next few months. The pork cutout plummeted this week and that also will provide stiffer competition for beef in the retail channel. Sooner or later these macro headwinds are going to have an impact on beef demand. I’m amazed at how stable the cutouts have been this year and it almost gives an eerie feeling like the calm before a storm. When beef prices do shift, I don’t think it is going to be upward—at least not in the nearterm. Longer-term, the cattle supply is shrinking in normal cyclical fashion, so we are very likely to see higher pricingfor both cattle and beef at some point, but right now there are 1.4% more cattle in the nation’s feedyards than last year (and second largest ever for Aug 1) and the demand environment isn’t inspiring, so the path of least resistance should be lower. The one supply side variable that looked uber-bullish was carcass weights, but this week USDA reported steer weights up a whopping 9 pounds, so the carcass weight story has gotten a little less bullish. Steer and heifer slaughter this week registered a very healthy 535k. I have to go all the way back to May of last

year to find a fed kill larger than that. Surely some of that beef will be headed to grocery stores this week for Labor Day features, but how will the beef market perform under such large production?

Of course, the next two weeks will see reduced kills due to the

Labor Day weekend, so maybe packers are just trying to build

some inventory in advance. It looks like feedyard placements

during August will be down YOY by single digits, but cattle

feeders have surprised us for four months in a row with largerthan-expected placements. It may happen again in August.

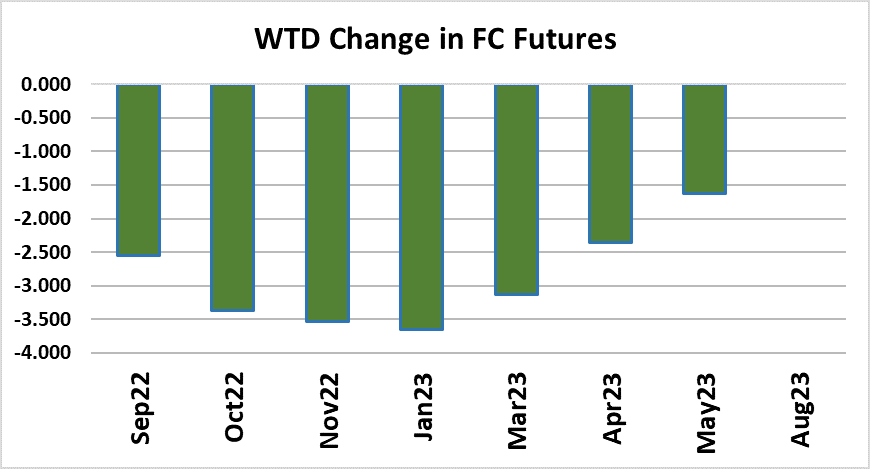

One positive development is that some of the premium came

out of the Oct and Dec futures this week and that might help to

discourage cattle feeders from hold back marketings in hopes of

realizing a higher price down the road. Cattle feeders are

already paying crazy high prices for feeder cattle and that is

likely to come back to bite them later this year.

The CME Feeder Cattle Index is now over $182 and this

happened in an environment where corn prices have been rising

day after day. Cattle feeders who paid $182 for feeder cattle

will need to sell the finished animals for about $165 near the end

of the year just to break even. The all-time high price for live

cattle was $169/cwt back in Jan, 2015. Today, the Dec LC

futures settled close to $149, so there is about $16/cwt worth of

disconnect between the futures and the bullishness in cattle

feeders’ minds. I get it that cattle feeders have had a rough go

of it financially for the last few years and they really want to

believe that their day in the sun is coming soon. It probably is

coming, but not nearly as soon as they think. Next week,

watch the cutouts for signs that the market is having trouble

digesting this week’s big production. Also keep an eye on

carcass weights because if they continue to move quickly

upward then that takes away one of the most bullish

fundamentals in the complex.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}