Beef Wrap September 01

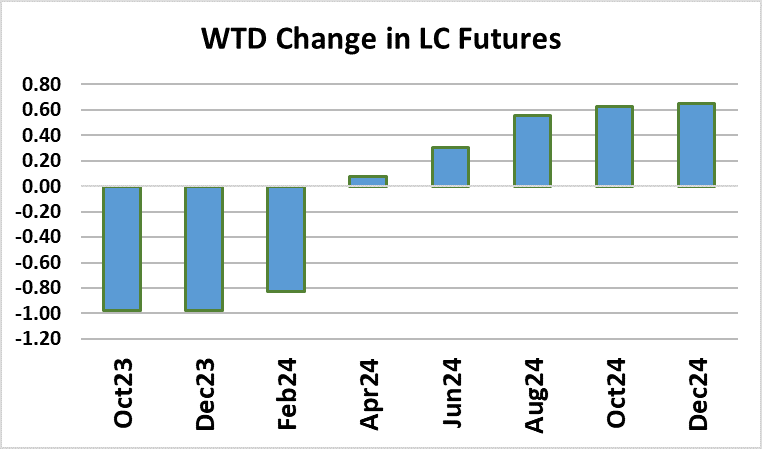

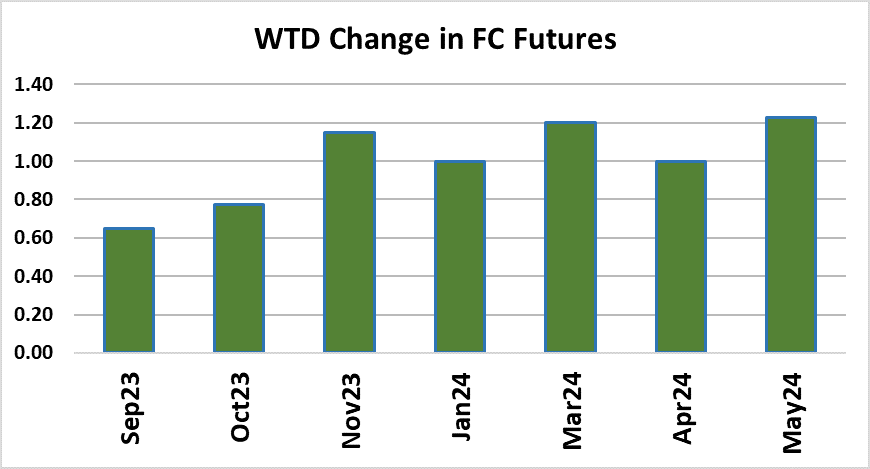

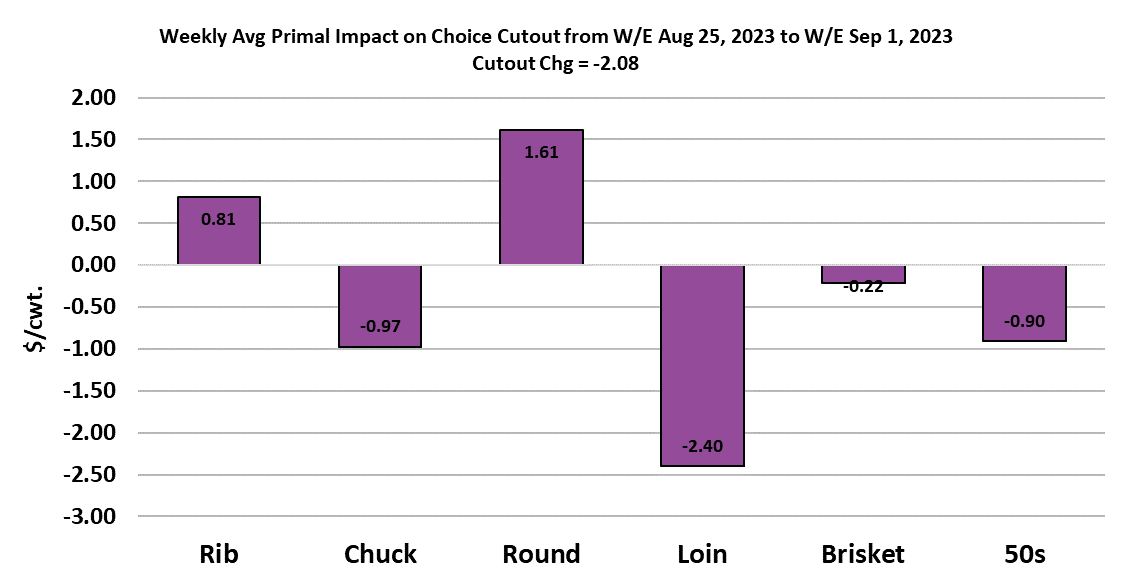

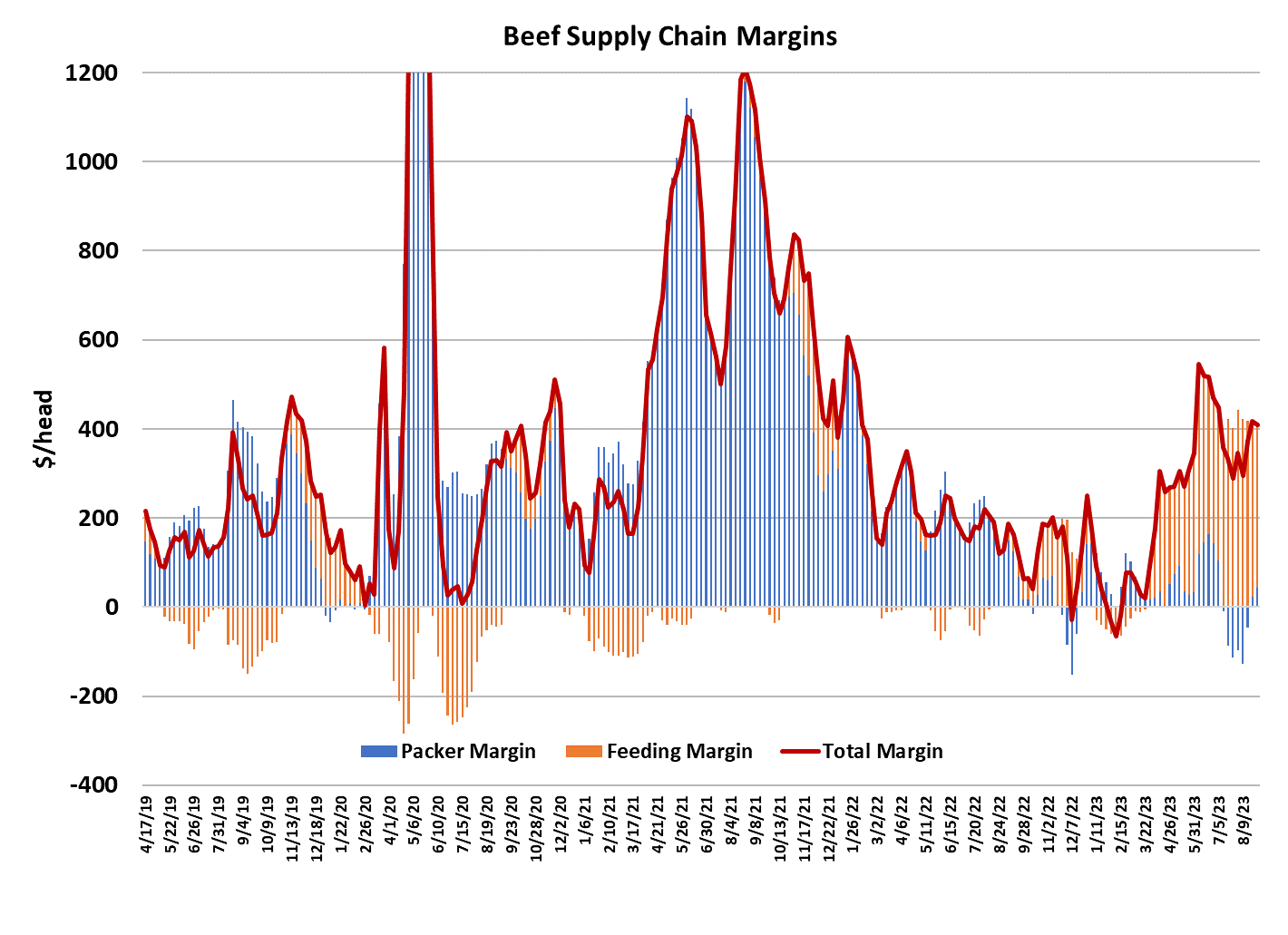

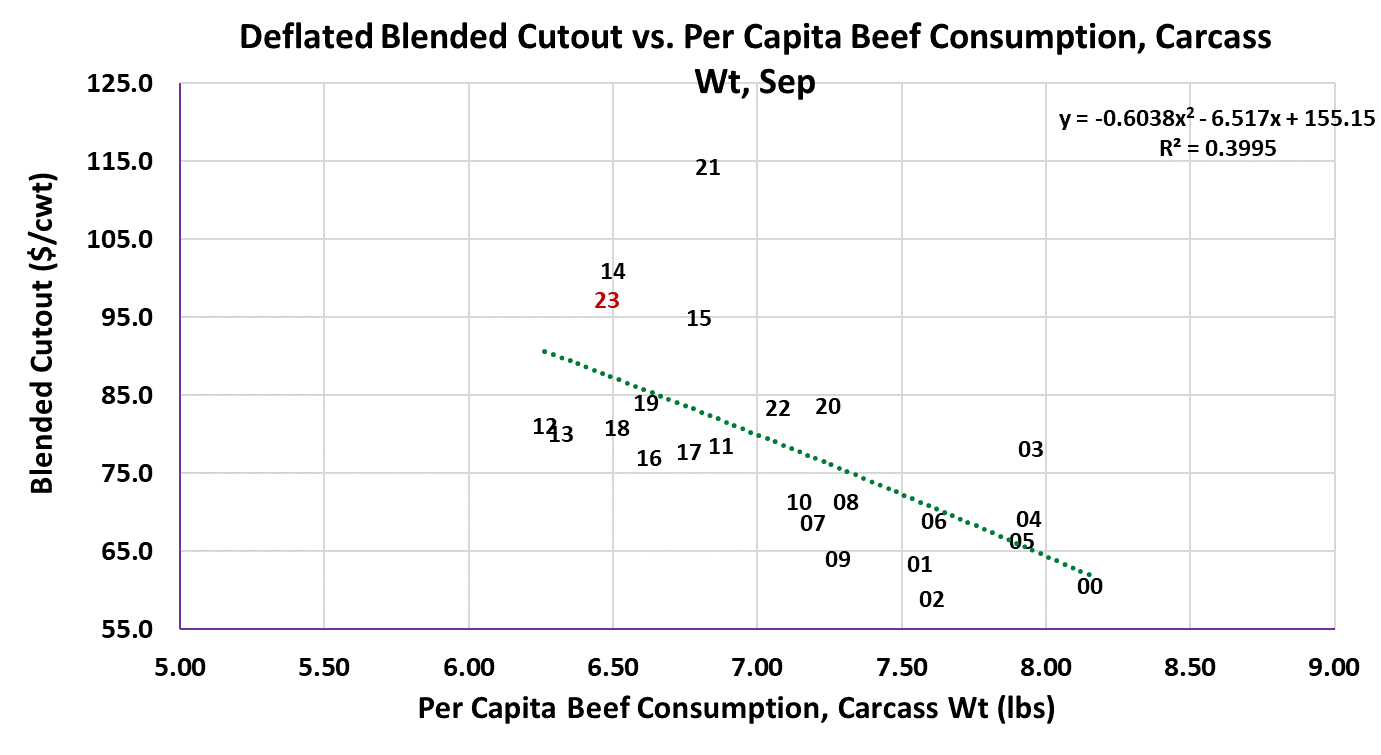

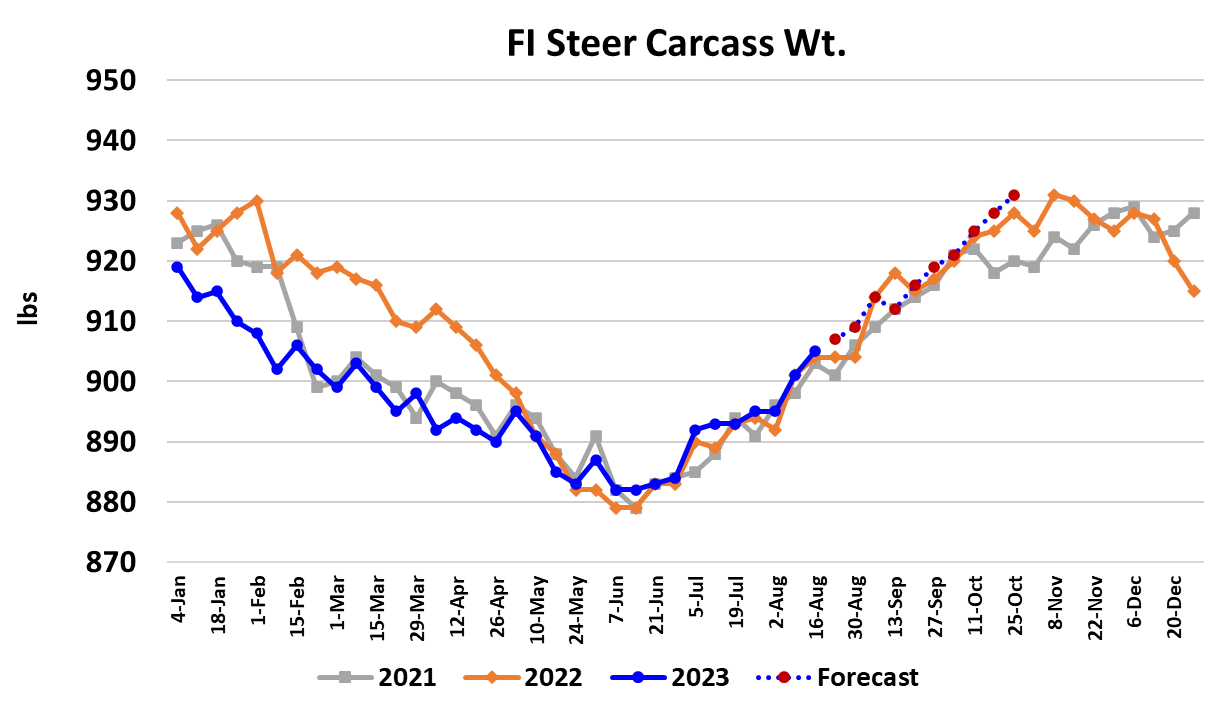

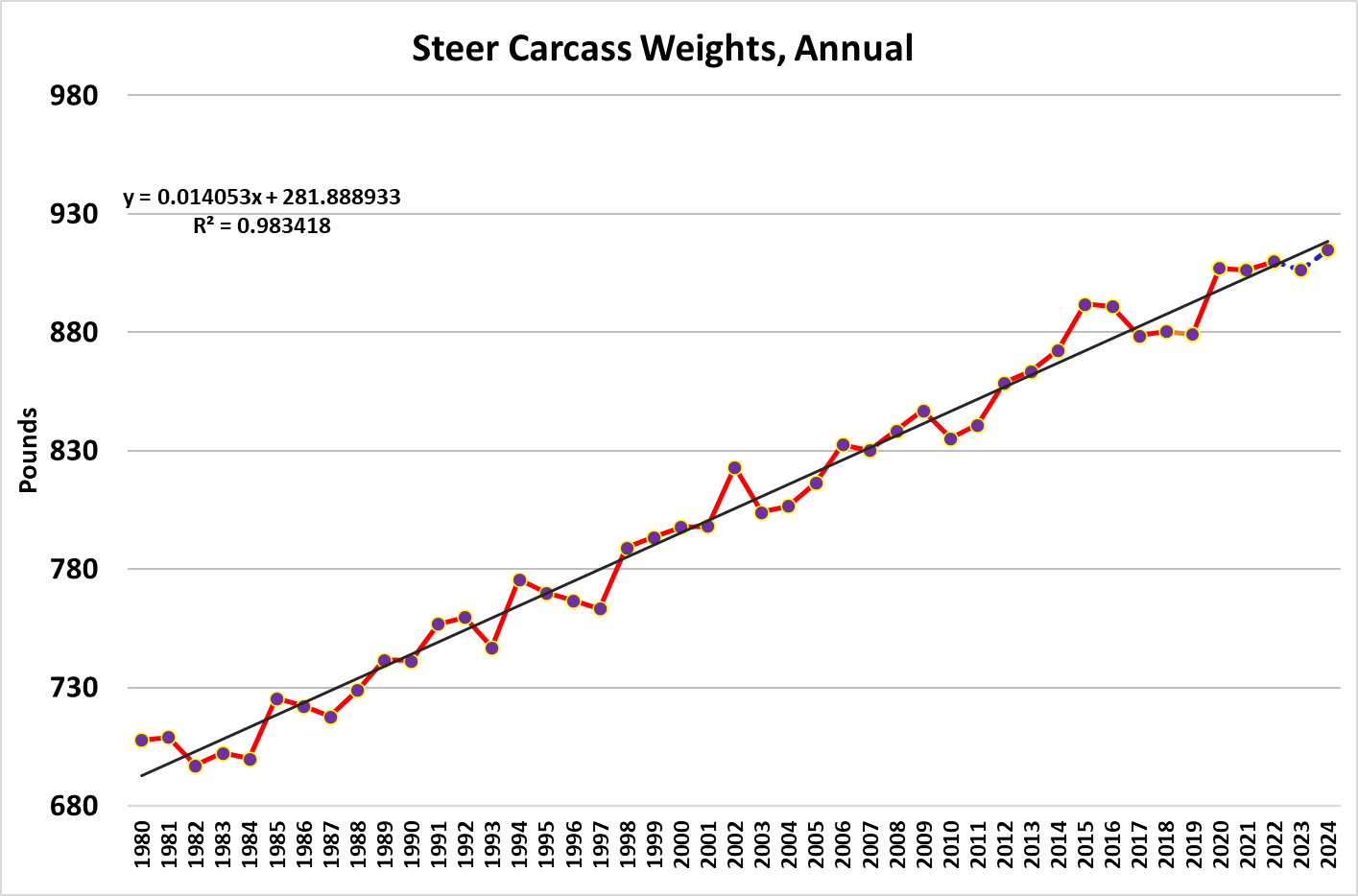

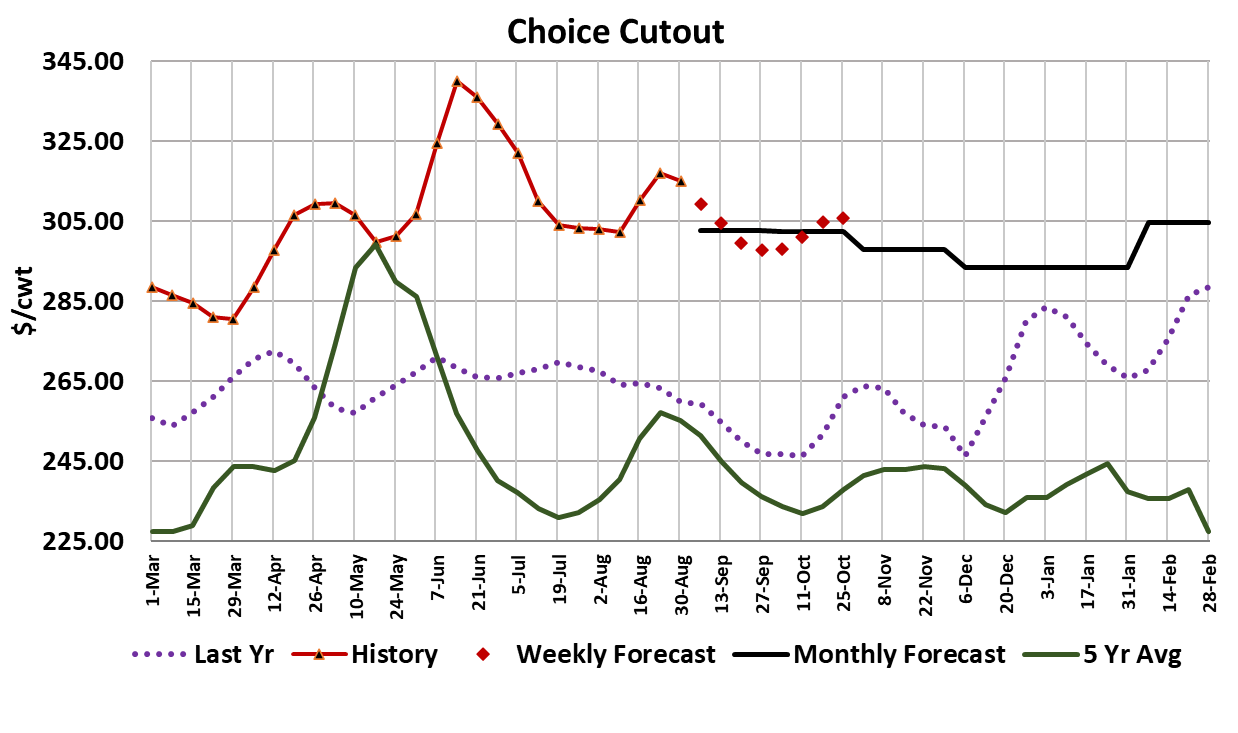

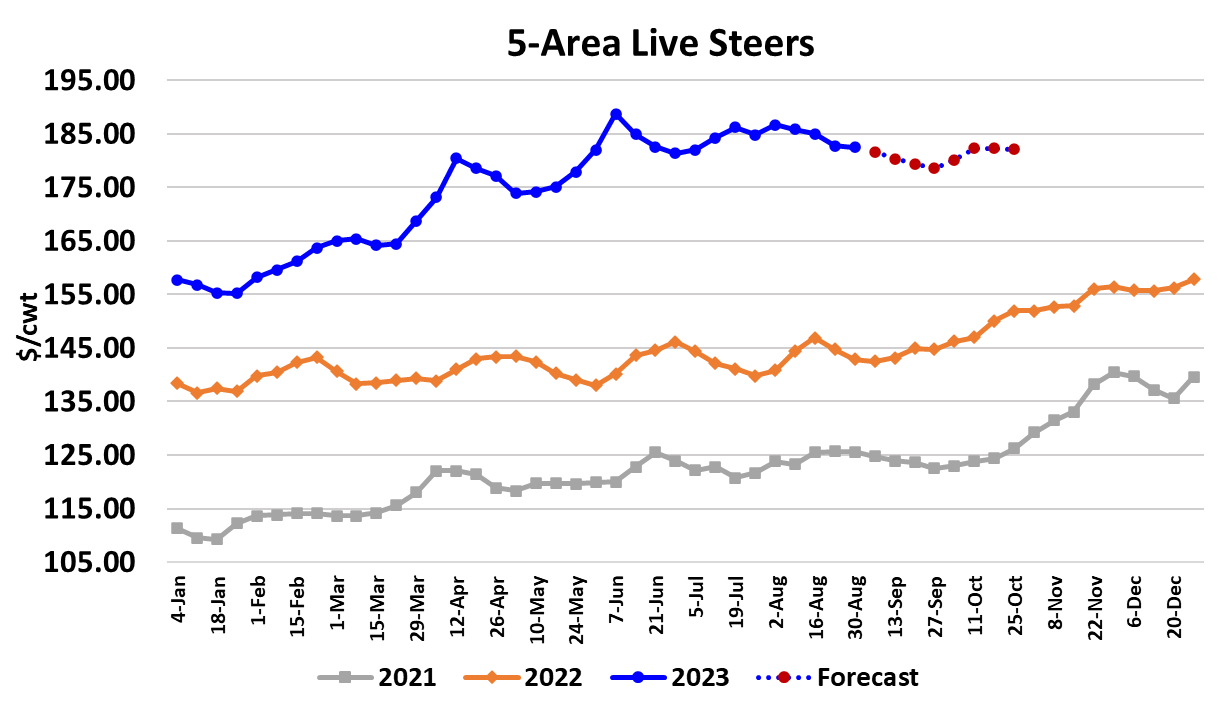

The beef cutouts eased a little bit this week, with the Choice down $2.08 to average $314.96/cwt. and the Select off $0.43 to average $290.17/cwt. That marks the first softening of the cutouts in four weeks and may signal that the restricted kill strategy packers’ have been employing is unable to lift beef prices much further. The strategy also seems to be less effective in the cash cattle market, where this week’s average across all regions looks like it will be close to $182.50, down only about $0.50 from last week. Trade in the South was mostly steady at $179, with a smattering of $178, but in the North, cash prices lost $1-2 on the week. Next week, packers will need to reload cattle inventories for a full kill week following Labor Day week, so that might have them bidding more aggressively than what we saw this week. I calculate packer margins this week at $43/head, but next week they could fall close to zero again if the cutouts continue to ease. The rib and round primals were a little stronger this week, while the chuck, loin, brisket and 50s were all lower. Interestingly, the ribs didn’t move lower following the completion of Labor Day buying and perhaps that is an indication that some buyers are already starting to think about, and prepare for, the holiday season. The drop in the 50s is just a return to more normal pricing following an extended period this summer where fat trim prices were through the roof. 90s continue to price very strong, with this week’s average coming in at $308.35/cwt. That seems to be related to smaller-than-expected cow kills near the end of summer that haven’t allowed the normal seasonal break in lean trim prices to happen. While the seasonal drop in 90s prices hasn’t happened yet, it probably will get started during September and should carry through at least November and maybe longer. However, the beef cow herd continues to shrink at a fairly rapid clip and thus cow slaughter in 2024 is expected to be lower than this year and that means higher lean trim prices in 2024. I’m currently forecasting about a 20% price increase in the 90s next year, which seems large on the surface, but we need to remember that back in 2014 during the last cycle when cow numbers were really tight, we saw a 32% YOY increase. As the calendar turns to September, we should expect retailers to place greater emphasis on the end cuts, but even so, I think that once kills return to normal after Labor Day, end cuts prices will come under modest pressure. The typical seasonal pattern has the cutouts working lower through September and then getting a boost in October as the holiday middle meat business starts to ramp up. I don’t see anything that would be contrary to that this year. Overall beef demand remains good and, as the attached scatter diagram indicates, my price forecasts for September impound a little stronger demand than last year, even though those forecasts point to declining cutouts this month. Also note on that scatter diagram how much per capita beef availability (consumption) has declined from Sep 2022 to Sep 2023. We are now very close to 2014 levels in terms of supply tightness. Of course, that has been helped along by packers’ scaling back on the kill as they try to limit the damage to their margins. It also remains to be seen if packers will have the discipline to maintain those kill cutbacks through September and if they don’t, then per capita availability will be larger than what the scatter indicates, with lower prices as a result. This week’s fed kill came in at 497k, up 3k from the week before. Fed kills have been slowly creeping up since they bottomed at 472k back in early August. Look for packers to do a large kill on the upcoming Saturday in an effort to partially make up for the lost kill on Monday due to the holiday. I’m projecting next week’s fed slaughter at 467k. The flow model suggests that cattle availability in September should be sufficient to fuel non-holiday fed kills in the 505-510k range, but if packer margins continue to struggle it is likely that they will restrict the fed kill to something below 500k per week. Steer carcass weights added four pounds this week to 905 and I expect to see another two pounds added in next week’s data release. The attached weekly steer carcass weight chart looks pretty normal in that this year’s data is tracking pretty close to the previous two years, but in reality, that is not normal. Fed carcass weights generally add about 0.6% per year and it looks like 2023 is going to fall below the long-run trend line and perhaps 2024 will also fall short of trend. High corn prices in the last couple of years have had a negative impact on carcass weights. Hopefully, the corn crop that is currently being harvested will be considerably larger than last year and help keep corn prices contained next year. If that’s the case, then maybe my 2024 weight forecast is a little low. Next week, look for some modest gains in the beef cutout early in the week that fade as we get near the end of the week. The cash cattle market could be a little weaker, but it wouldn’t surprise me if it held steady as packers reload.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}