Beef Wrap September 10

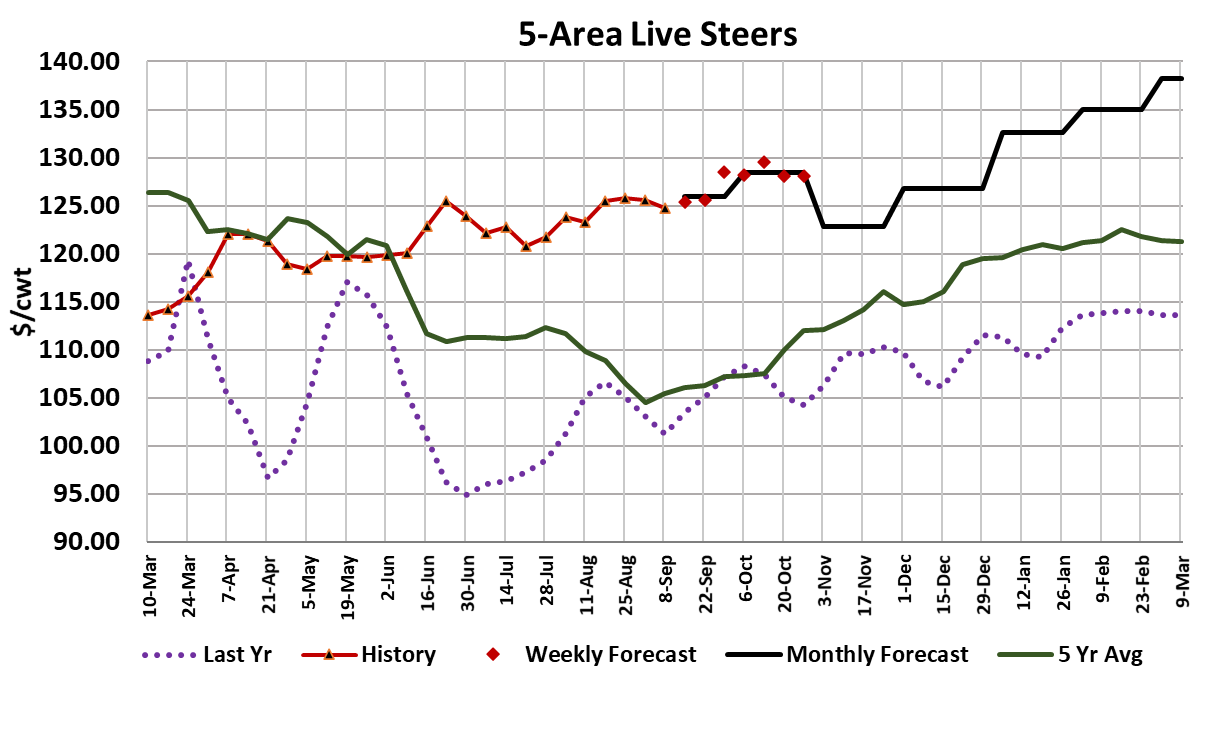

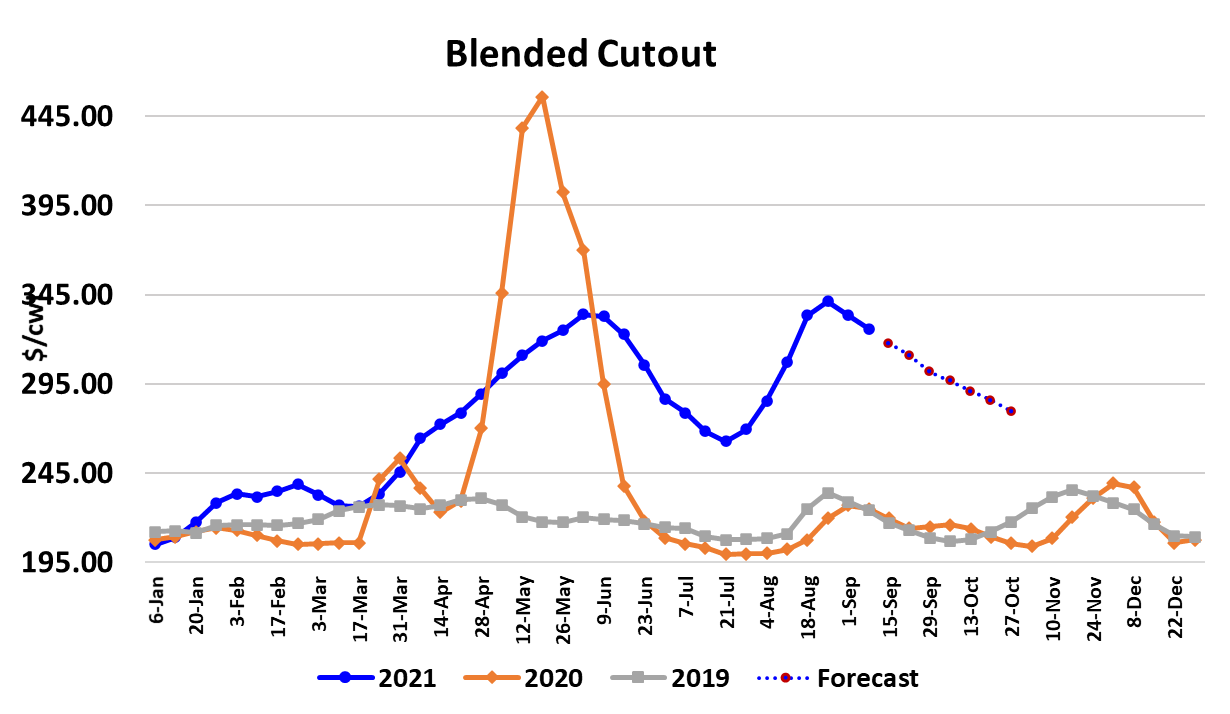

Cash cattle markets were about $1 lower this week to $124.73 and

the cutouts were also on the defensive, with the Choice losing a little

over $7 on a weekly average basis and the Select down almost $11.

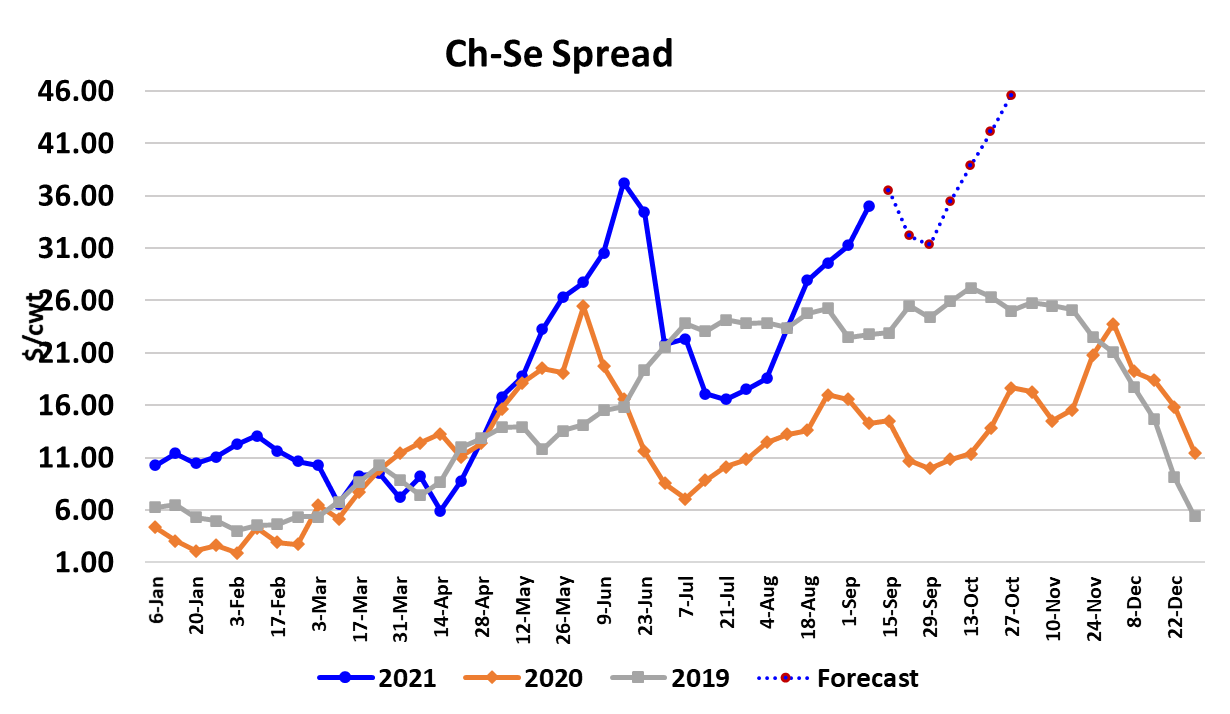

That really expanded the Choice-Select spread, which now sits at

almost $34—extremely wide for this time of year. Over the past five

years, the Choice-Select spread has averaged a little under $11 for

the second week of September. So, clearly there is a new dynamic

at work here. Beef buyers want Choice because their customers

want Choice. I don’t really think it is a supply-side issue since the

percentage of cattle grading Choice or better is near 81% and it has

been in that area since early June.

Over the summer, the spread ranged from about $17 on the low

side to $34 on the high side and the proportion of Choice or better

didn’t vary all that much. It is noteworthy that the middle meats are

still seeing strong demand while end meat demand has been softer.

Choice is more important in middle meats than in the ends, so

strong demand for middle meats is likely the biggest driver of the

spread at the moment. With beef prices falling more than cash

cattle, packer margins compressed this week, now at “only” $1032

per head. Meanwhile, cattle feeders need $131/cwt to break-even

on their cattle and they are getting about $6 less than that. The

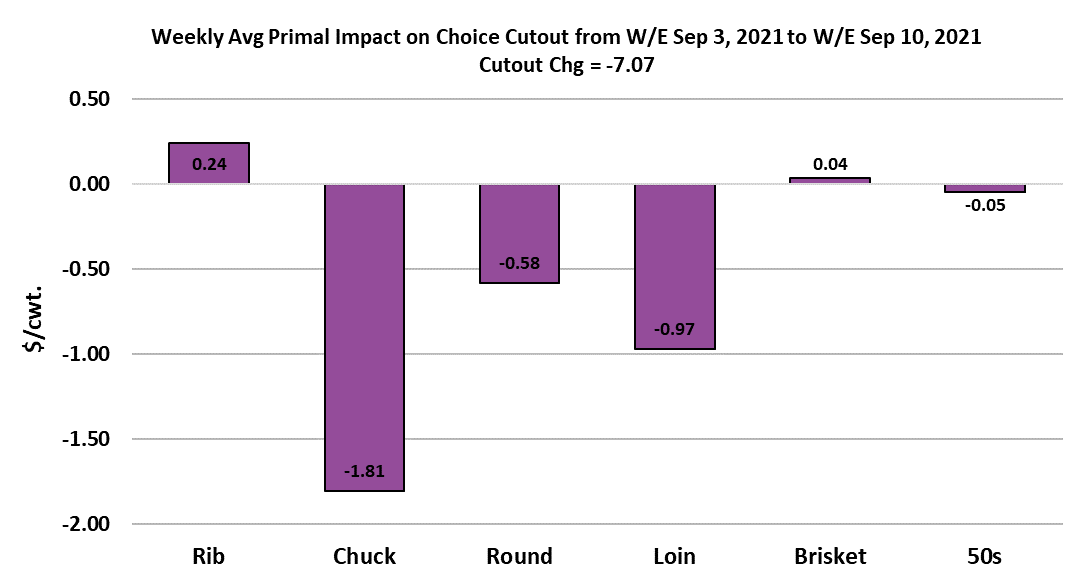

chart below indicates that chucks put the most pressure on the

cutout this week, while the ribs were actually a little stronger. That

is the exact opposite of what we normally see at this time of year. In

fact, the failure of the ribs to give up much ground in the two weeks

since Labor Day has me wondering if they will set back much at all

before the holiday buying starts.

It also makes me think we could be in for a super-strong middle

meat market in Q4. Buyers are forewarned. Beef demand is fading

somewhat now and that is evidenced by the turn in the combined

margin chart. The last time the combined margin peaked and

turned was just after Memorial Day and demand softened for five

weeks after that. This time, it turned at Labor Day and if it goes five

weeks this time, that would put the bottom in early October. Perfect

timing for the traditional surge in holiday middle meat interest. So,

the message to buyers is to use the price softness in the next few

weeks to your advantage and get positioned for the holidays as best

you can because after about mid-October, price levels could turn

higher again.

This week’s fed kill was right at 455k due to the holiday on

Monday. Next week, I’d expect it to bounce back into the

515-520k range. That increased availability should hasten the

retreat in the cutouts. At this point, the supply of beef available is

being limited by packer’s ability to process cattle, not a shortage of

cattle. However, as we move into October, the available supply of

cattle should be tightening up based on past placement patterns

and we stand a good chance of seeing fed kills at or below 500k

per week.

If demand turns higher in October also, then we could see prices

jump as smaller supply meets bigger demand. Right now, my

forecast has prices working lower through October, but I recognize

that the risk is to the upside. Maybe a lot to the upside. I think

traders are beginning to recognize that cash cattle prices are not

going to leave their trading range in the mid $120s until packing

plants shore up their labor force and can increase kills. That

means packer margins will likely remain incredibly wide. Strong

processing margins are not unique to the beef industry, we are

also seeing the same thing in pork and chicken. The fantasy of

$140 cattle at some point in the future has faded considerably.

That doesn’t mean that beef won’t get very expensive however. It

will. Everyone in the supply chain needs to adjust their

expectations on beef pricing higher for the foreseeable future.

Plant workers will need to be paid a lot more to keep plants fully

staffed and those costs will be passed along to consumers in the

form of higher beef prices and to cattlemen in the form of lower

cattle prices.

Wider margins will become the norm since that is necessary to

compensate the packer for his increased labor costs. The export

market for beef is looking a bit softer in recent data and I guess

that shouldn’t be too surprising given how high prices have been

recently. In fact, during July, the US was a small net importer of

beef. Our high domestic prices are attracting more imports. Next

week, watch the loin and rib primals for significant declines. If that

doesn’t occur, it will be time to get really worried about middle

meat prices this fall.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}