Beef Wrap September 3

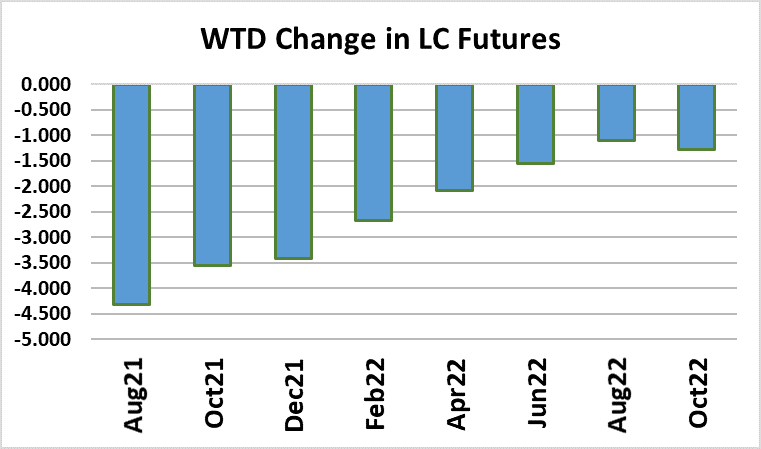

Live cattle futures traders seem to have lost their optimism for the

future. The Dec LC contract, which traded over $138 at one point

last week, closed Friday just a little under $131. Why the sudden

shift in expectations? Well, at least part of it has to be due to the

fact that the futures got way overdone following last month’s Cattle

on Feed report. Traders saw the 8% YOY drop in placements and

couldn’t buy the Dec futures fast enough. It didn’t matter to them

that the beef market looked toppy and was about to turn lower.

Now it does seem to matter. They realize now that the cash cattle

market isn’t going much of anywhere as long as labor is limited in

packing plants, making it difficult for packers to kill all of the

market-ready cattle each week.

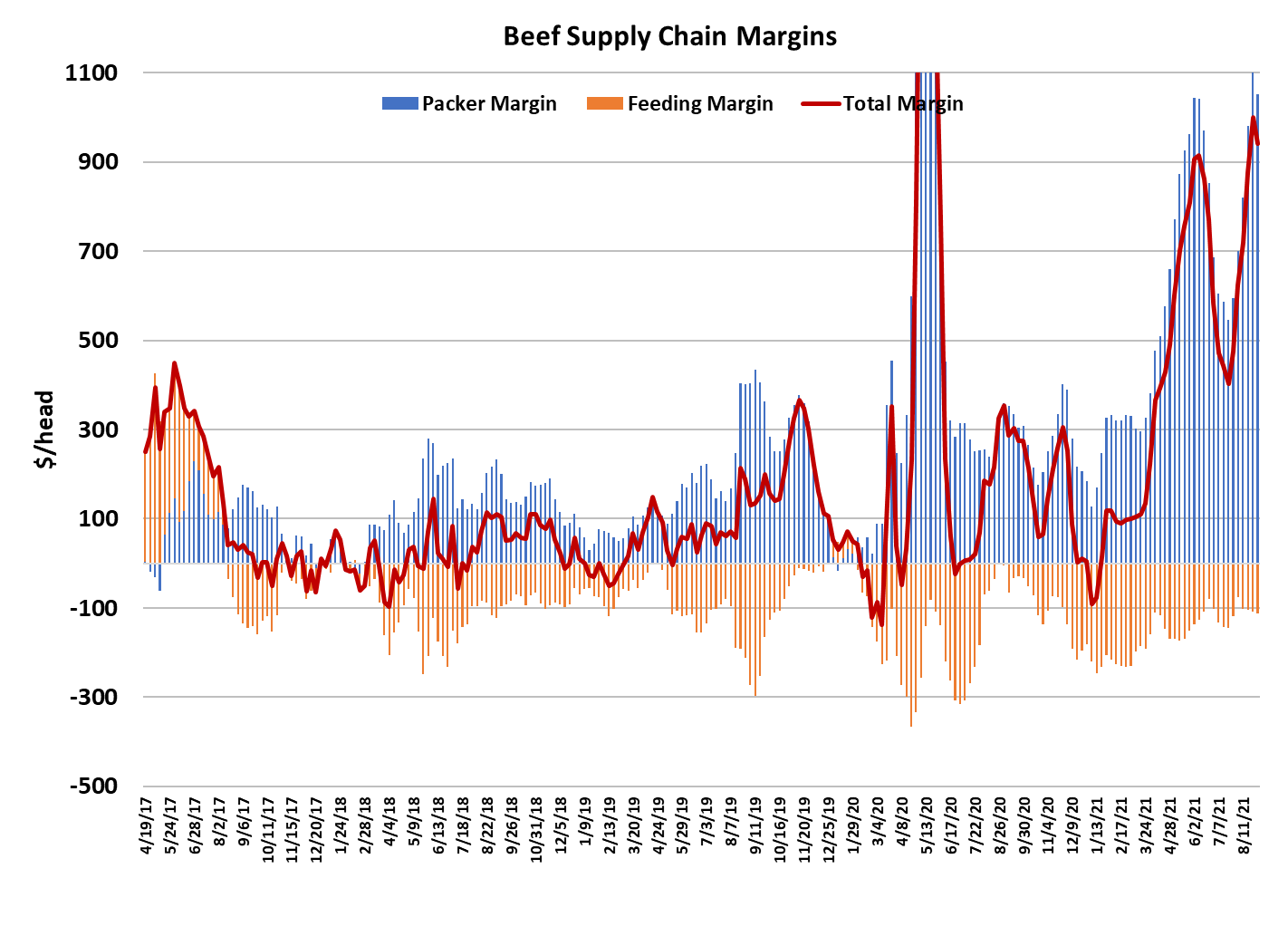

Packers would really love to kill a lot more cattle since their margin

this week came in at $1050/head. That margin should start to

shrink now that the cutouts have turned lower, but even if it were

reduced by 50% it would still be a huge margin in a historical

context. To their credit, packers aren’t expending any energy to

push down on the cattle price. This week’s cash cattle average is

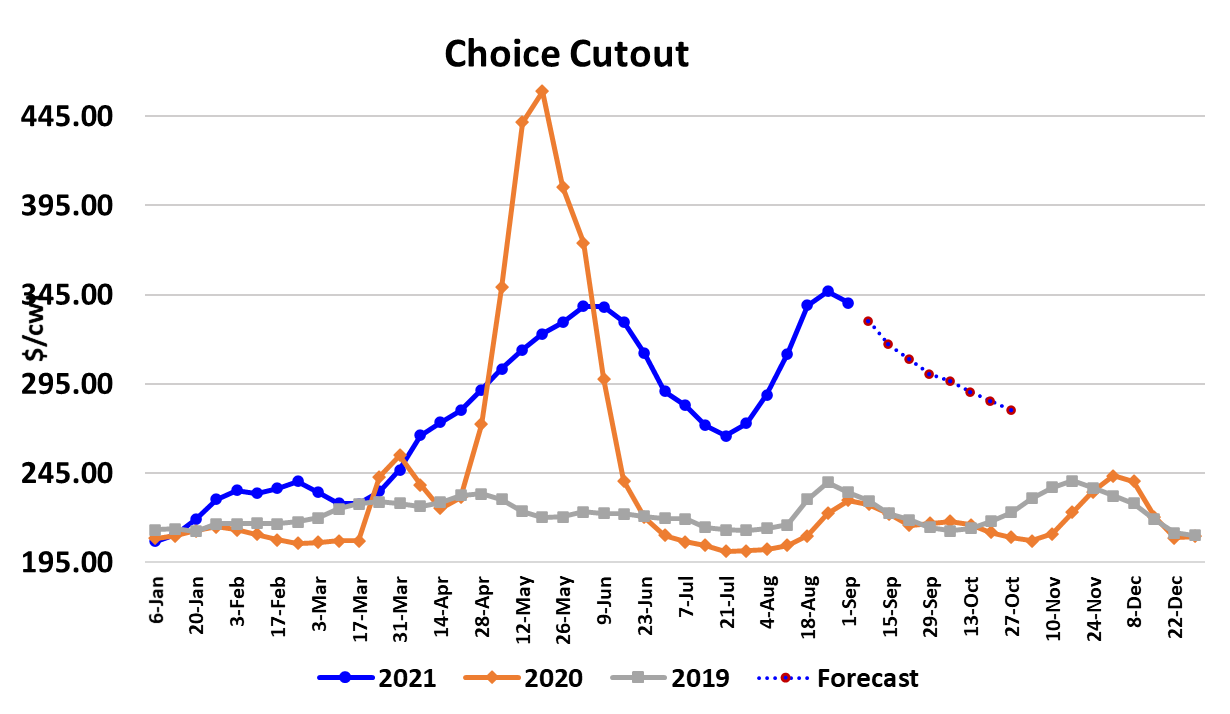

$125.93, only a few cents higher than last week’s average. As far

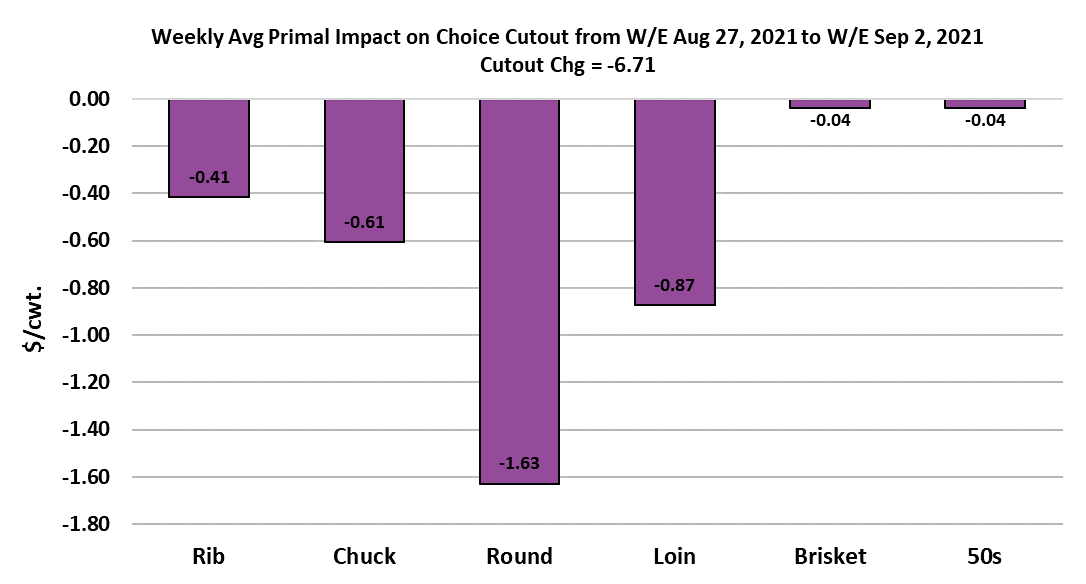

as the cutouts go, the Choice has dropped about $7.50 this week

and the Select is down a little over $9. Beef buyers recognize the

turn lower and are trying their best to stay out of the spot market

while price levels adjust downward. This registers as a decline in

demand and the combined margin chart below indicates that

demand is indeed headed lower now after making a top last week.

Both middle meats and end meats contributed to the cutout’s

softening this week, but I’m really surprised that the middle meats

haven’t dropped more. The rib primal was down only about $4

this week and is acting like it doesn’t want to give up any more

ground.

So much for the theory that it was Labor Day buying that was

supporting the ribs. It seems like there is much stronger demand

for middle meats even outside of the holidays now. I guess it

doesn’t have to be a special occasion now to justify throwing a

ribeye on the grill. Retailers are not aggressively featuring middle

meats either and that means a lot of consumers must be stepping

up to pay non-feature price for middles. Those non-feature price

levels in the US for boneless ribeyes are now typically over $15/

pound.

Clearly someone has extra money they didn’t have at this time

last year. I do think that once retailers have finished restocking

after Labor Day, that wholesale middle meat prices will come

under greater pressure, but for now it is simply amazing how well

those prices have held up. I’m forecasting the Choice cutout to

come off in big chunks over the next few weeks and thus

perhaps reach the $300 level by the end of September. What

happens after that is very uncertain.

In normal years, we would see increased buying interest in

middle meats for the holidays kick in around early October and

thus lift the cutout. The big question in my mind is whether or

not that will happen this year. If it does, the normal fall rally in

the ribs and tenders will be starting from a very high level and

thus it would be reasonable to expect them to move to all-time

highs that exceed what we just saw in August. I just can’t

imagine it will go like that again, so I’ve got the rib primal

declining from now to December. Even using that very unusual

price pattern, I end up with an average price for the rib primal in

Q4 that is $83 higher than last year’s big number. If I went the

other direction and forecasted rising rib prices from October

onward, I would probably end up with price levels in Q4 that were

at least $300 higher than last year.

That is just too much for me to buy into at this time, but I wouldn’t

discount the odds that it may happen. This is 2021, after all.

Steer and heifer slaughter this week is projected at 500k since

packers are likely to keep the Saturday kill light in order to give

more workers a long weekend. Next week’s fed kill could be

closer to 465k. Those two short kill weeks will tighten up beef

availability some, but I don’t expect it send the cutouts suddenly

higher. What it will do is backlog several thousand head of cattle

and thus just prolong the wait for cash cattle prices to rise. Next

week, watch the middle meats for evidence they will move

rapidly lower and look for the futures to rebound somewhat from

its current oversold condition.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}