Beef Wrap September 17

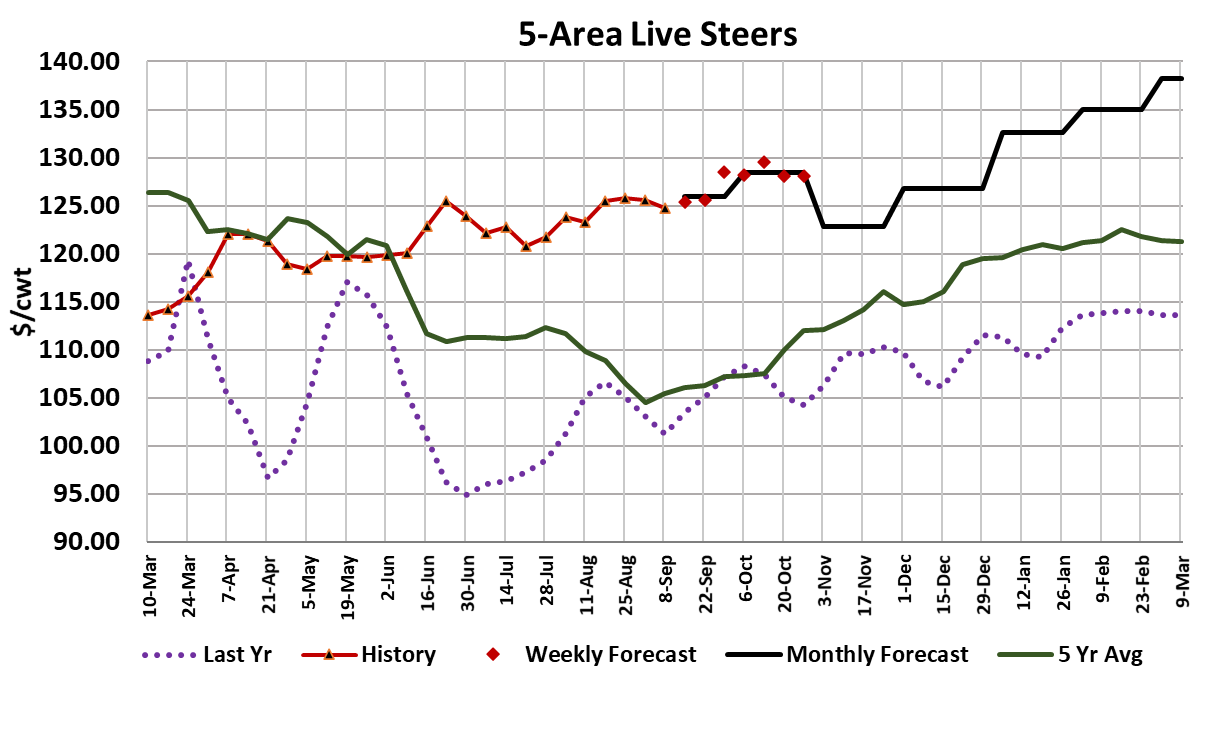

The cash cattle market was a little lower this week, with the average

live trade done close to $124. In the prior four weeks it had been

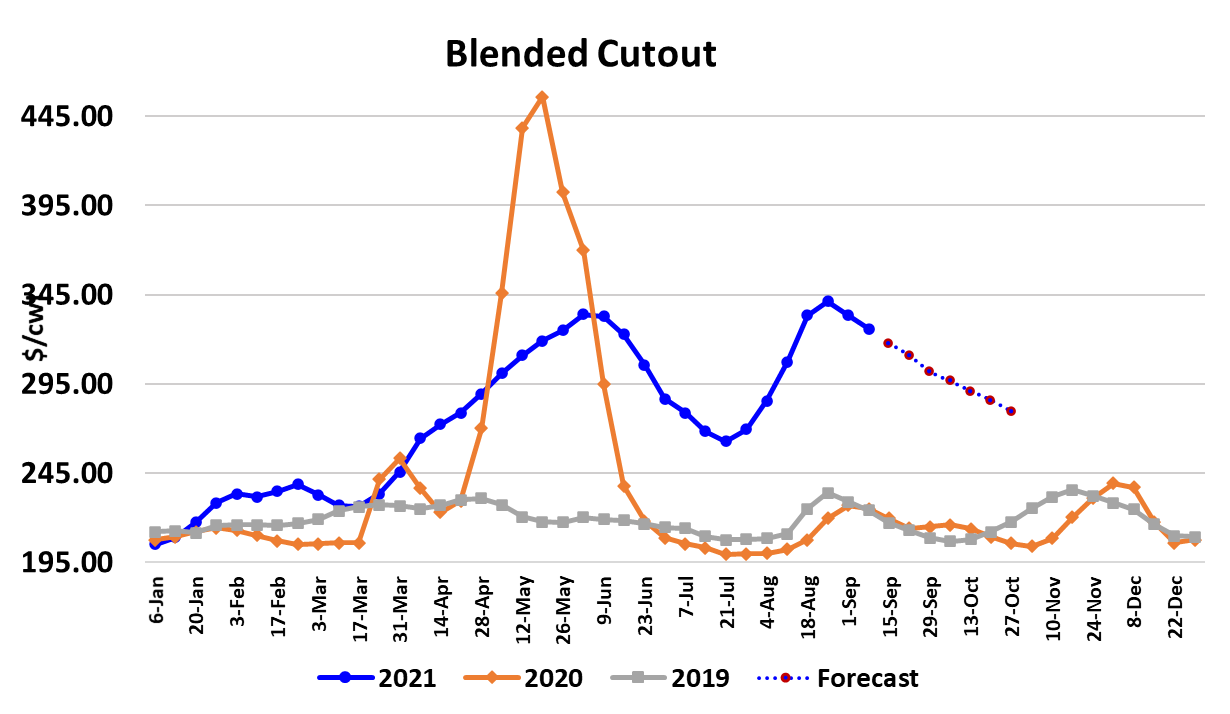

closer to $125. The beef market continued its retreat with both

cutouts down about $12 on a weekly average basis. That said, the

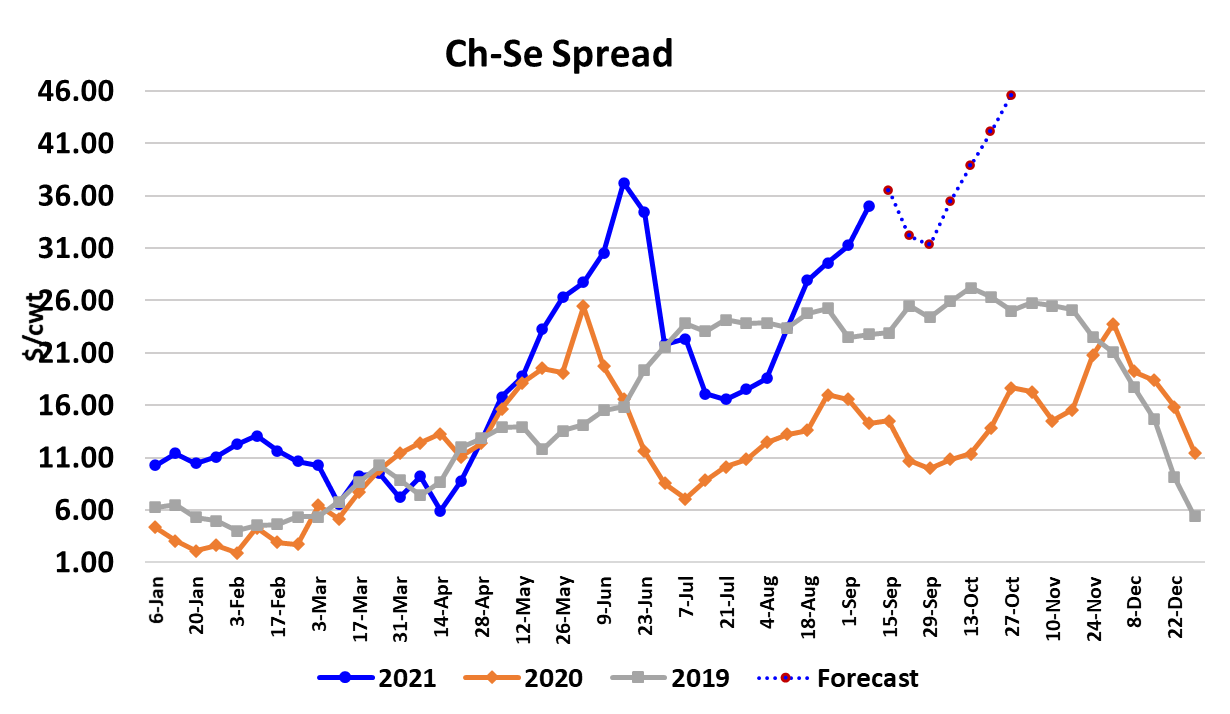

Choice cutout finished up on Friday at $314, so it is not cheap by

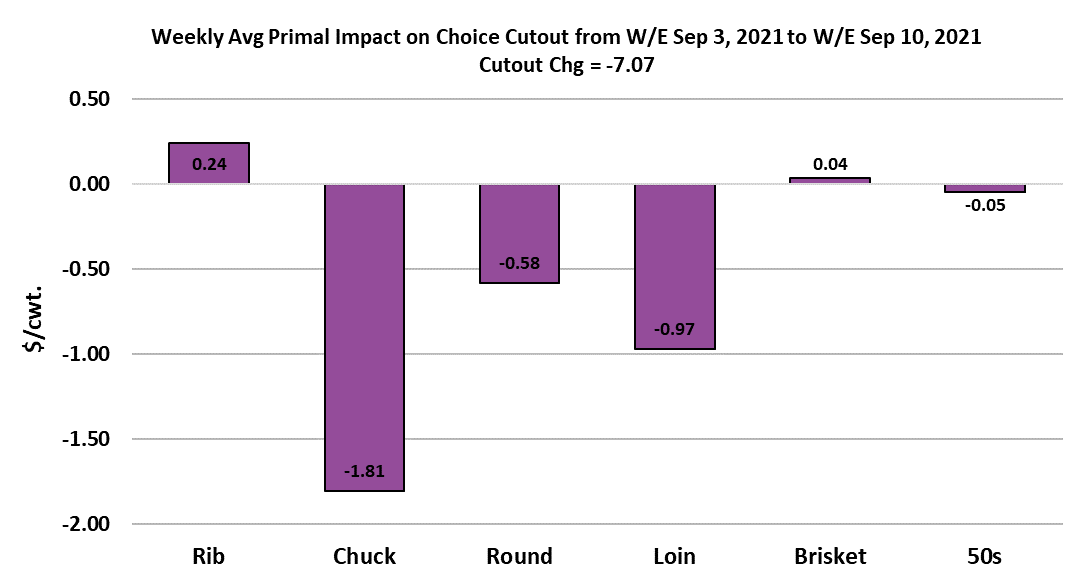

any means. Last week I said we should keep an eye on the middle

meats to see if they were going to give up any ground before the

holiday buying season starts. The chart below shows that the rib

primal was almost unchanged from last week, but the loin primal

was the biggest loser on the week.

So, there is no clear signal. Well I guess it is pretty clear that

something extraordinary is going on with the ribs, but that is not

transferring over to the loin cuts. Traditionally, the loins trend lower

throughout the fall, with the possible exception of tenders when we

get into November, so the action on the loins isn’t all that surprising.

The ribs being this strong in September is very surprising. End

meats are starting to give up ground in big chunks now and I would

expect that to continue for several more weeks. Packer margins are

compressing as the cutout falls. This week they came in at $945/

head. It doesn’t really look like cash cattle are going to move much

in the coming weeks, so further erosion in the cutouts implies further

erosion in packer margins. The extreme persistence of super-sized

packer margins has forced me to raise my margin forecasts for Q4

and Q1. Packers haven’t faced a margin less than $300/head since

January. That is pretty amazing. The chart below shows the

exponential growth in packer margins since 2016. Packers must

have found the secret sauce in 2016, because before that average

annual margins were mostly negative.

That chart is exactly the kind of picture that government officials are

looking at when they say something is badly amiss in the packing

segment. This week’s fed kill came in at 517k, which was up about

60k from the previous week’s holiday-shortened kill. Cow and bull

slaughter totaled 143k, up 20k from the week before. My model

suggests that packers will need to kill around 520k steers and

heifers in September to keep animals from backing up, but when we

get to October a 500k kill should be sufficient. If fed kills do fall

below 500k in October, then I suspect that packers will become a bit

more competitive in sourcing cattle and thus there is a chance that a

few dollars could be added to the price of cash cattle.

Right now, the fundamental forecast has cash at $127 near the

end of October. The carcass weights that were released this week

were a good bit heavier than I was expecting and thus had to

increase the carcass weight forecasts. It occurs to me that, with

labor limited in packing plants, one way to get more beef output for

roughly the same amount of labor is for cattle feeders to make the

animals heavier. Of course, that is a tough sell when corn is over

$5/bushel. Cattle feeding margins are still moderately in the red

and I calculate that cash cattle prices would need to move into the

$128-130 range to erase that red ink. Domestic demand is slowly

deflating, but remains way above historical levels.

The scatter below for September shows just how strong domestic

demand is currently. Here is a guessing game we can all play:

When do you think will be the next time the data point on the

scatter falls below the regression line? 2022 or 2023 or never? I

certainly don’t think it will be any time in 2021. International

demand for US beef continues to look healthy, but it is pretty clear

that high US pricing during Aug put a dent in export volumes. The

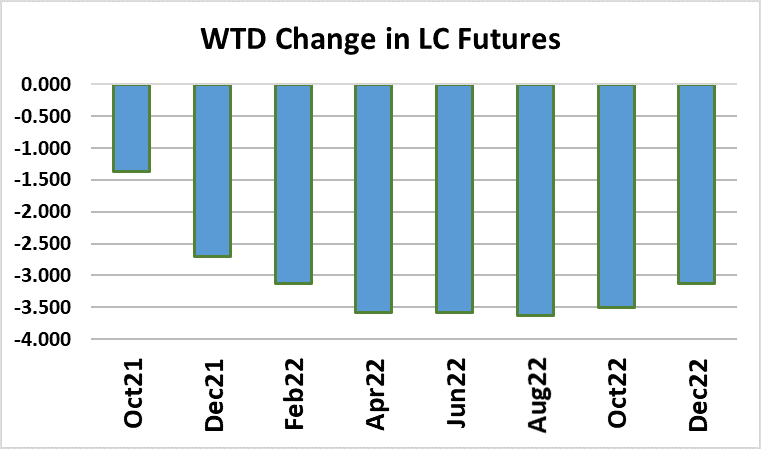

futures calmed down somewhat this week after a strong downtrend

in the previous two weeks. I think we are back into a trading range

type of market for live cattle because there is not much hope for a

big change in the cash cattle market over the near term.

Next Friday we will get another Cattle on Feed report and I expect

that it will peg August placements down 2%. That is smaller than

most of the other estimates I’ve seen. Actually, my models were

pointing to a much larger decrease than what I put down on paper,

so I wouldn’t be surprised if USDA printed placements down 5% or

more. Next week, continue to watch the middle meats and

particularly the ribs. I’m concerned that primal could go to the

moon once the holiday buying kicks in.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}