Beef Wrap October 13

If packers thought that

buying a lot of cattle last week was going to help them pressure the cattle

market this week, it didn’t work. Having no luck getting cattle bought at

steady money, packers upped the bid on Wednesday and trade occurred in the

South at mostly $183, $1 higher than the week before. The North waited

until Thursday to trade and prices there were in the $184-185 range, $1-2

higher than last week. When all of the dust settles, it looks like the

average across all regions for the week will be about $184.50, up $1.75 from

last week. Even though prices were higher, purchase volumes were

strong. Packer margins were already in the red, but this threatens

to make things worse unless they can substantially raise boxed beef prices next

week. I calculate this week’s packer margin at -$81/head, only

about $20 better than the week before. No doubt packers will be on

the phones trying to coerce higher prices out of beef buyers. The beef

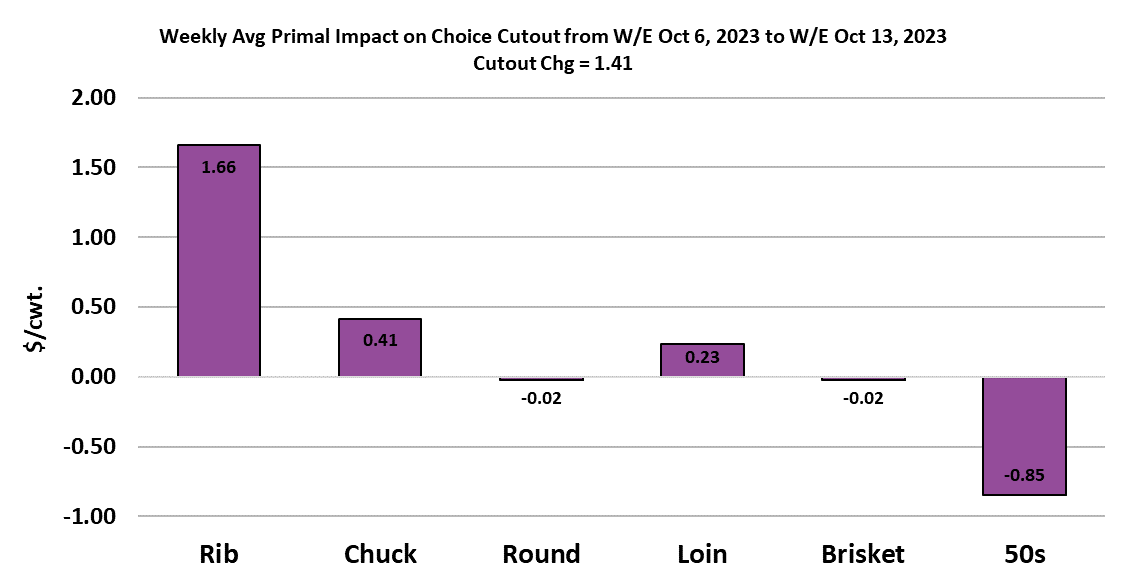

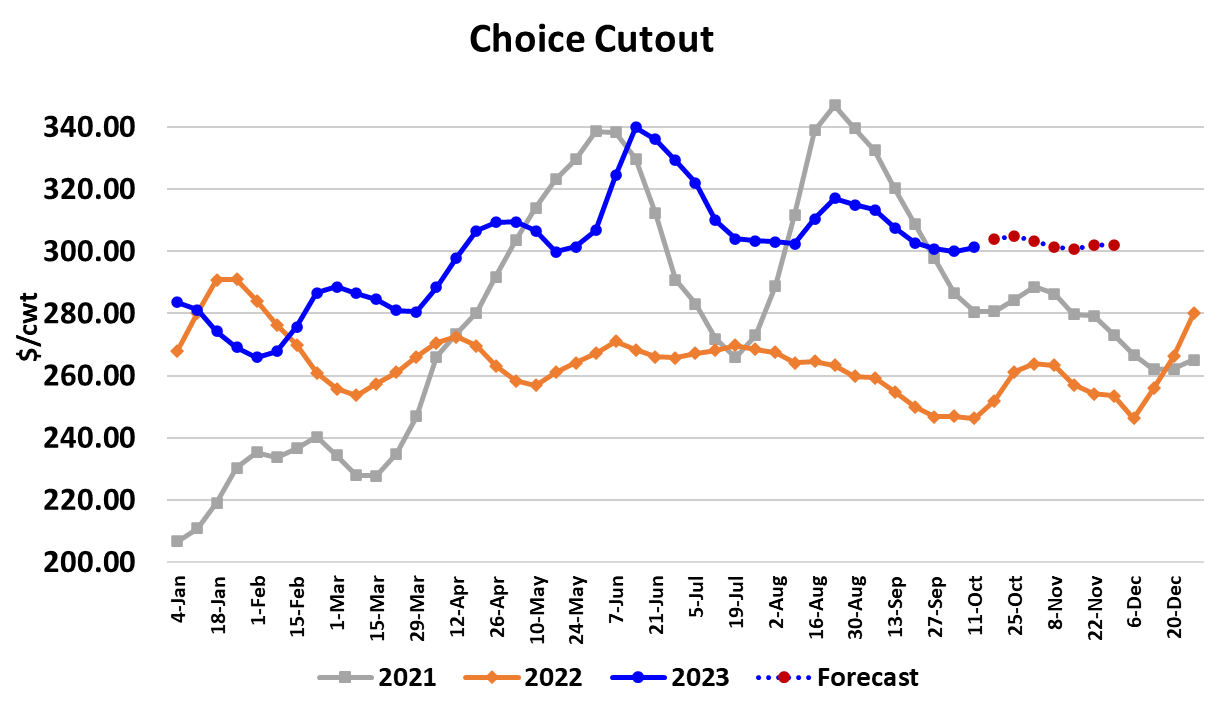

cutouts were a little higher on the week, with the Choice averaging

$301.35/cwt., up $1.41 on a weekly average basis and the Select averaging

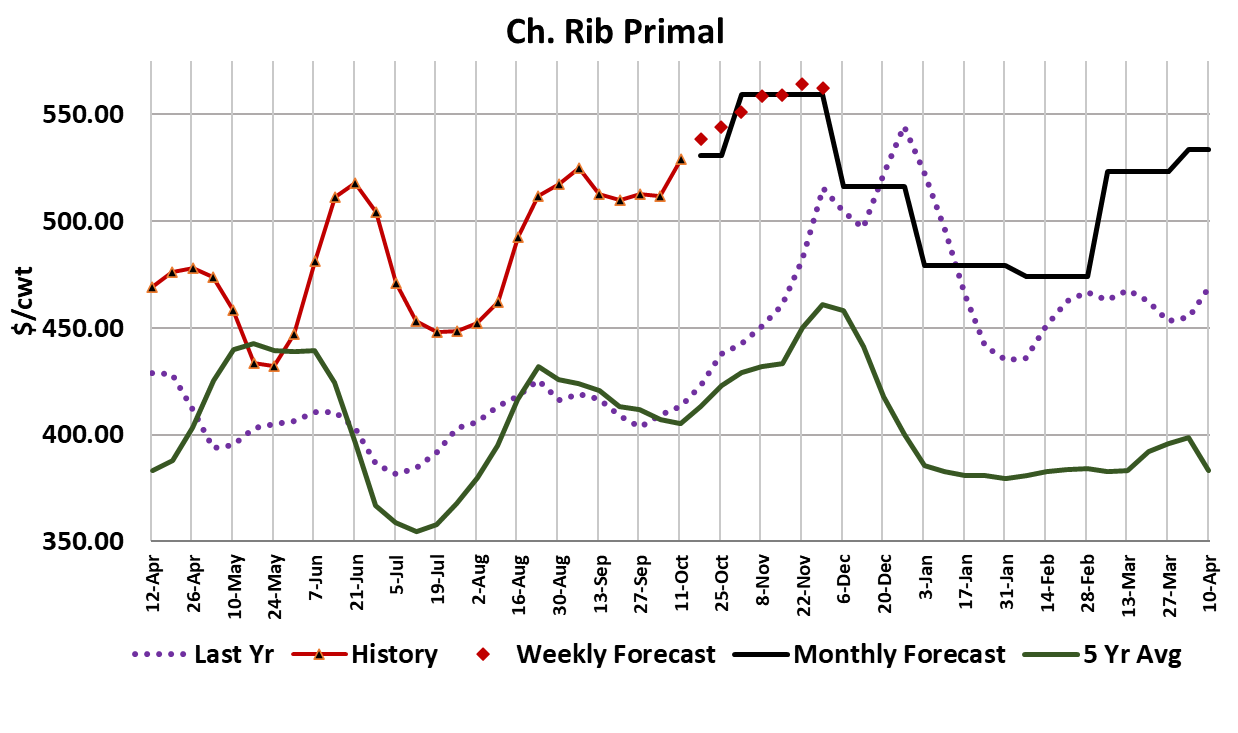

$279.89, up $0.29. A modest improvement in rib prices was largely behind

the Choice cutout’s gains this week, but it is clear that there are still some

buyers sitting on their hands with respect to middles for the holidays.

For that reason, packers might have some success in rallying the cutouts next

week as some of those short-bought users could panic when they hear the words

“kill cutback” coming from their packer representative. Or not, but

packers did step the kill down another notch late in the week, producing a

weekly fed cattle slaughter total near 480k, down about 6k from the week

before. Beef movement was fairly good this week and with the pullback on

the kill, availability could tighten up next week and allow packers to have

some success raising the cutouts. Whether or not it sticks remains

to be seen. There is a lot of uncertainty in the macro environment and

retailers are starting to report that consumer spending is slowing. Thus

beef users are being unusually cautious about loading up on expensive middle

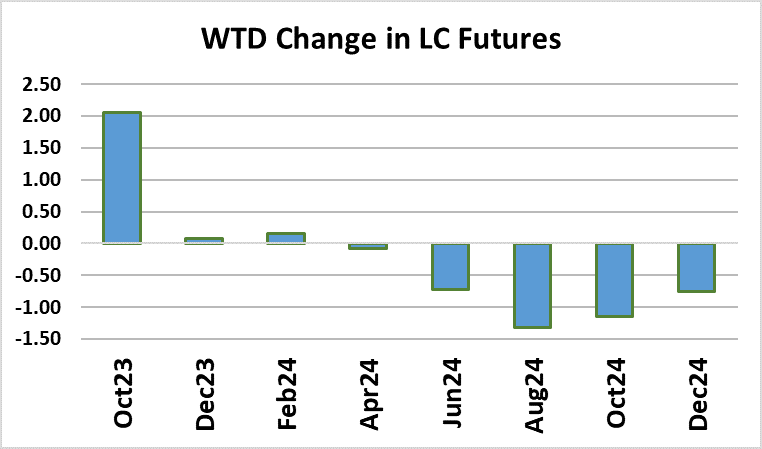

meats for the holidays this year. Cattle futures, which were beaten down

the week prior, could only manage a rally in the nearby Oct contract on the

news of higher cash trade. It is pretty unusual to see cash trade higher

and not get some rise in the back of the futures curve. I take that as a

sign of deteriorating faith in demand down the road because the supply

situation for 2024 is very bullish given where we are in the cattle cycle.

But let’s be realistic. The headlines might sound pretty gloomy with

inflation proving sticky and wars in Europe and the Middle East, but the US is

not in a recession. Heck, there are more jobs around than willing people

to fill them and the unemployment rate was just reported to be only 3.7%.

If the nation was in a deep, dark recession then there would be some reason to

be concerned about beef demand, but the data so far indicates that we are not

even close to that. Further, there is some debate about just how detrimental

a recession is to beef demand. It usually takes a pretty severe one

to dent beef demand enough for analysts to notice it in the data. True,

beef demand did get juiced by all of the pandemic stimulus and shift to

stay-at-home lifestyles, and that part has ended, so it is natural to expect

demand to fall from those lofty levels of 2021-22. But is there really

reason to think it is going into the dumpster? It may “feel” that

way, but so far there is little hard evidence of that. The performance

of the cutouts over the next couple of months will tell us volumes about the

state of beef demand. For the record, I’m not forecasting a huge holiday

price rally in the cutouts, but rather have the Choice cutout holding in the

low $300s through November. I think that we will see additional strength

in the traditional holiday middle meats that may be largely offset by softening

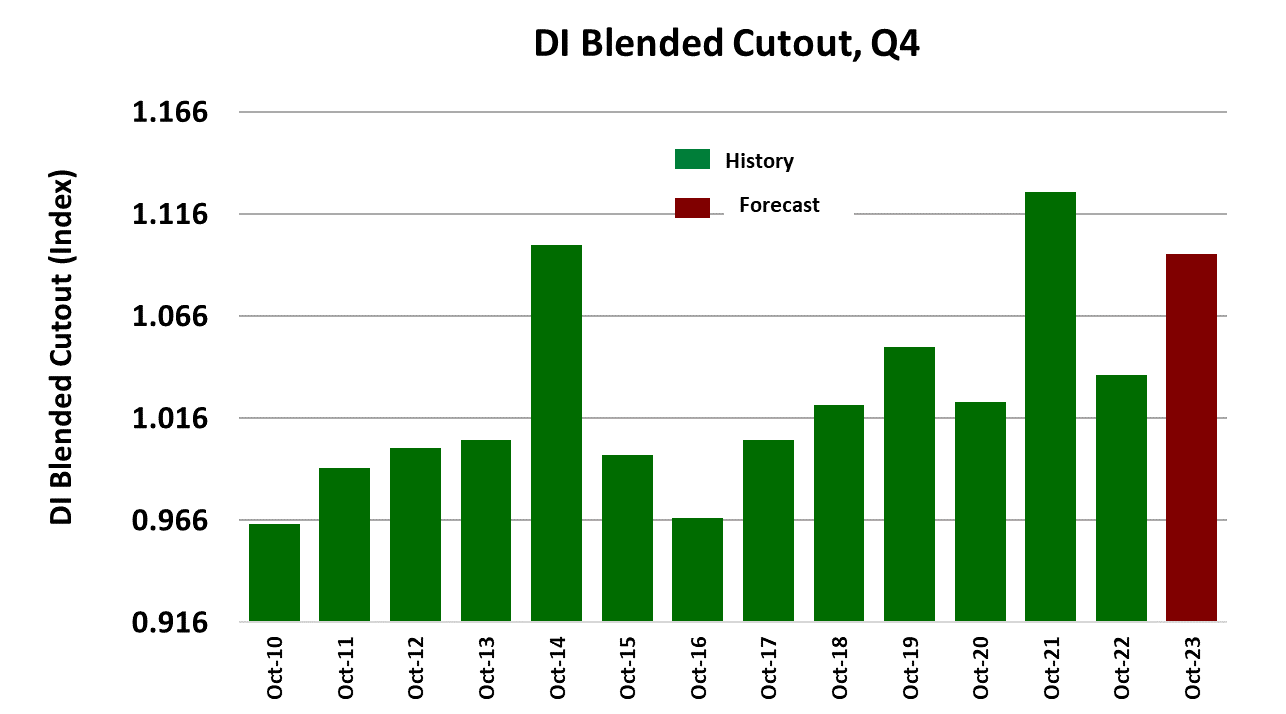

in the end cuts and grinds. That cutout forecast, if it is correct (and

that’s always a big IF), would be consistent with a demand index for Q4 around

1.095. Last year in Q4 the demand index was 1.037. Keep in mind

that these demand indexes take into account inflation in the general economy

and seasonality. So, it looks like demand stands a very good chance

of being much stronger than last year. Last year in Q4 the Choice cutout

averaged $262/cwt and this year I’m forecasting it to average $293/cwt.

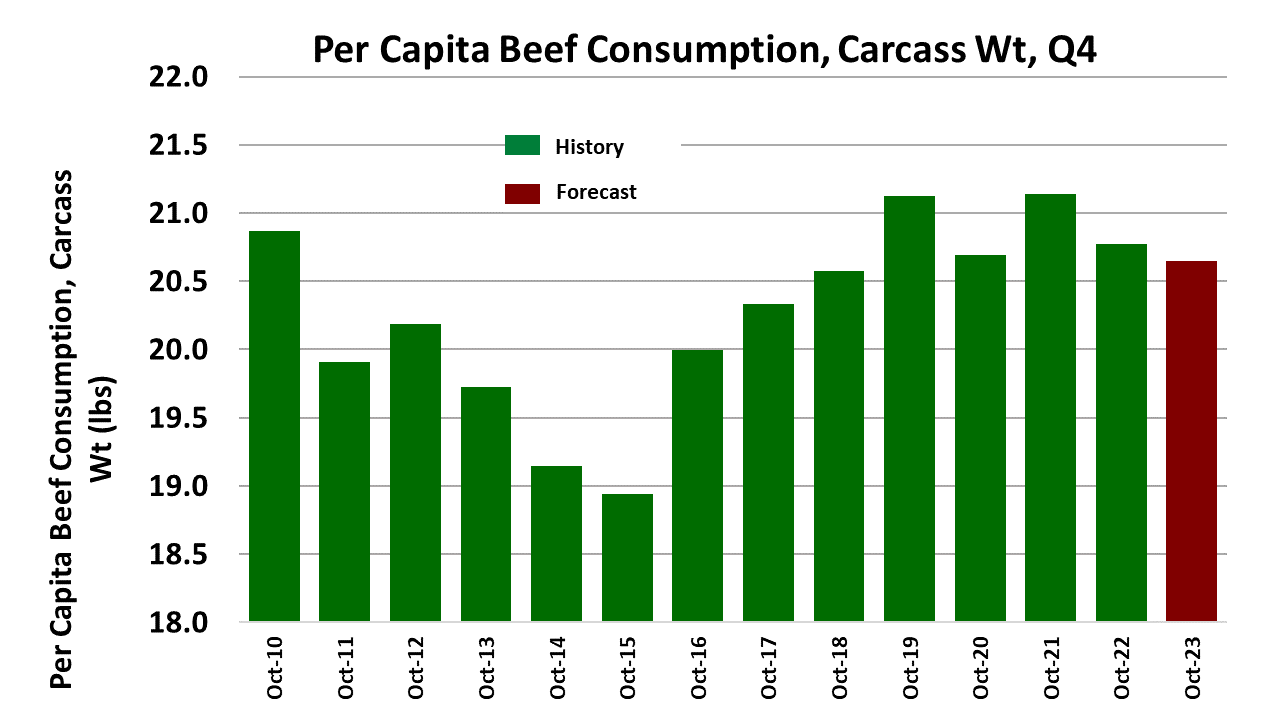

The $30 increase is solely coming from the demand side (and some general price

inflation) because I have per capita availability almost unchanged from last

year in Q4. So, this is not really a poor demand market that we are in,

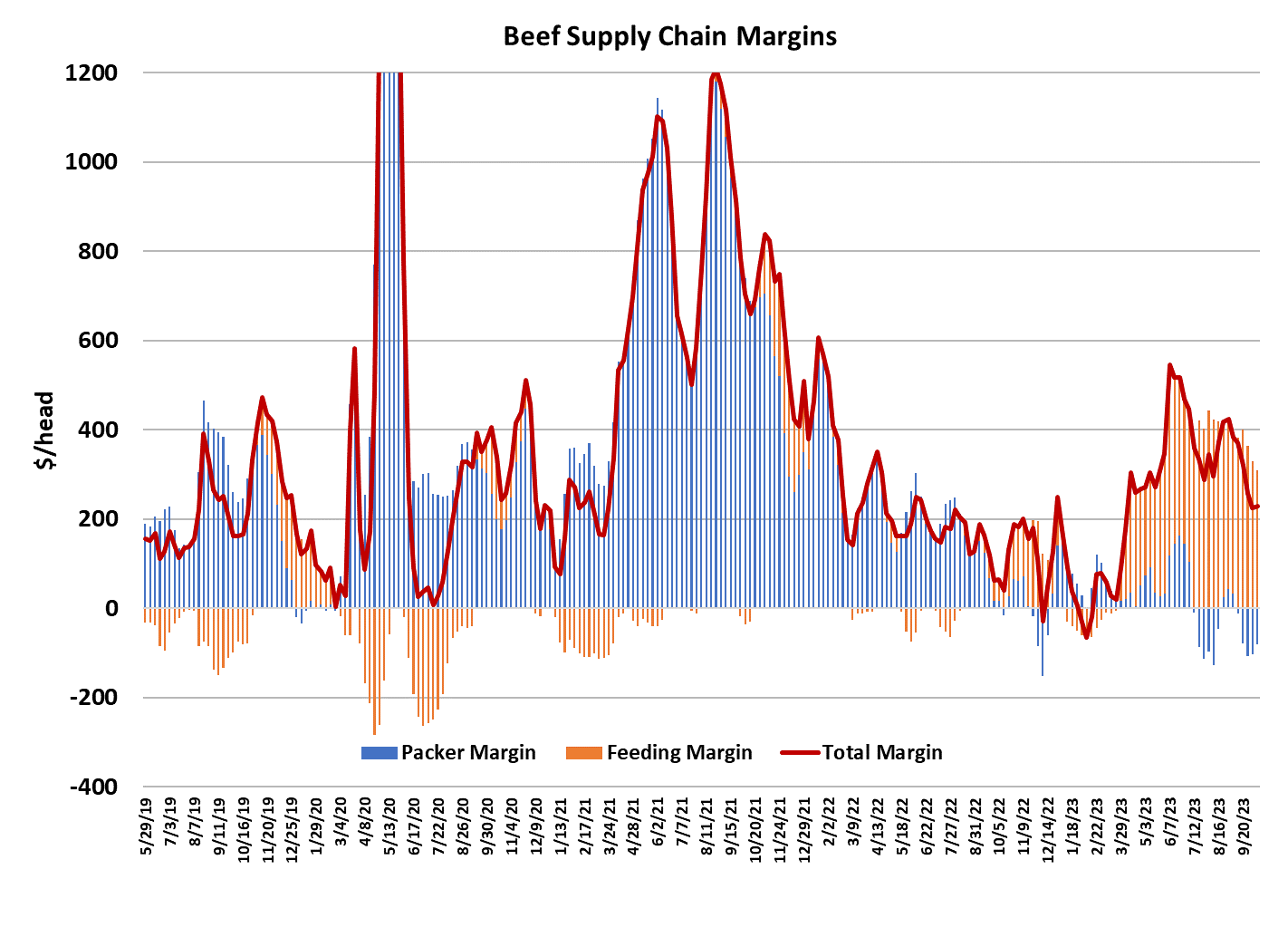

even if it may feel that way. Just look at the combined margin

chart. The combined margin is well above where it was last year—a indication

of stronger consumer demand. Part of the reason that this market feels so

bad currently is because packers are losing money on their beef

operations. We are not used to that. Normally, when demand is good,

packer margins are also good. But at this stage in the cattle cycle,

where animal numbers are tightening and packers have too much capacity for the

number of animals available, packer margins are supposed to go negative to

encourage them to scale back. Cattle feeders are making strong profits

currently—I calculate feeding margins this week at around $300/head—but their

turn in the barrel will come also. As animal numbers tighten further,

profits will migrate back through the supply chain until the cow-calf producer

holds most of the cards. Then the herd will start to expand and slowly

margins will move back up the supply chain, eventually making feeders and

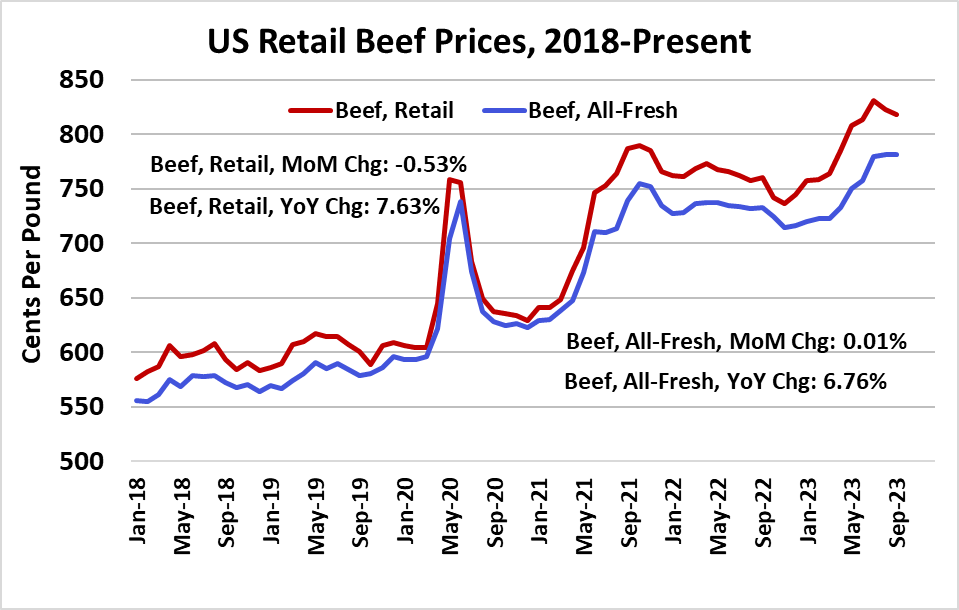

packers profitable again. And so the cycle repeats. This week, USDA

reported that retail beef prices during September were almost unchanged from

August. That was good news and, since wholesale prices in October have

been running a bit below September, there is probably a good chance that the

next report on retail prices won’t show an increase either. Of

course this is just a short term pause in price levels. As beef

production falls further in 2024, and barring a major collapse in demand, it is

highly likely that retail (and wholesale) beef prices will continue to

escalate. Next week, watch middle meat prices for signs that packer

jawboning and this week’s light kill is putting FOMO into the minds of retail

buyers. The cattle market is likely to take a breather and hold steady.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}