Beef Wrap October 14

The beef market just seems to be going nowhere. This week, the

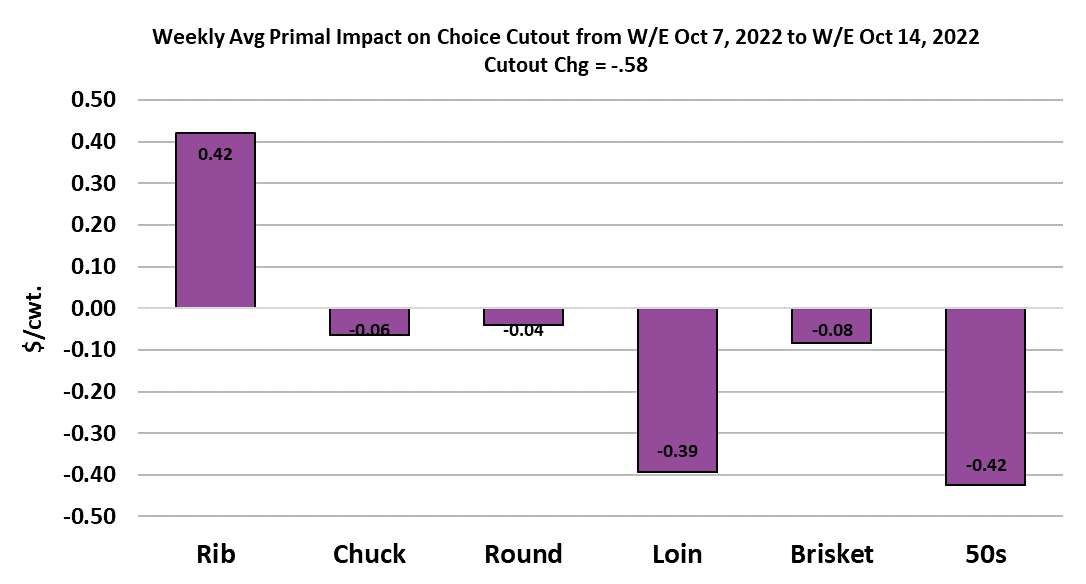

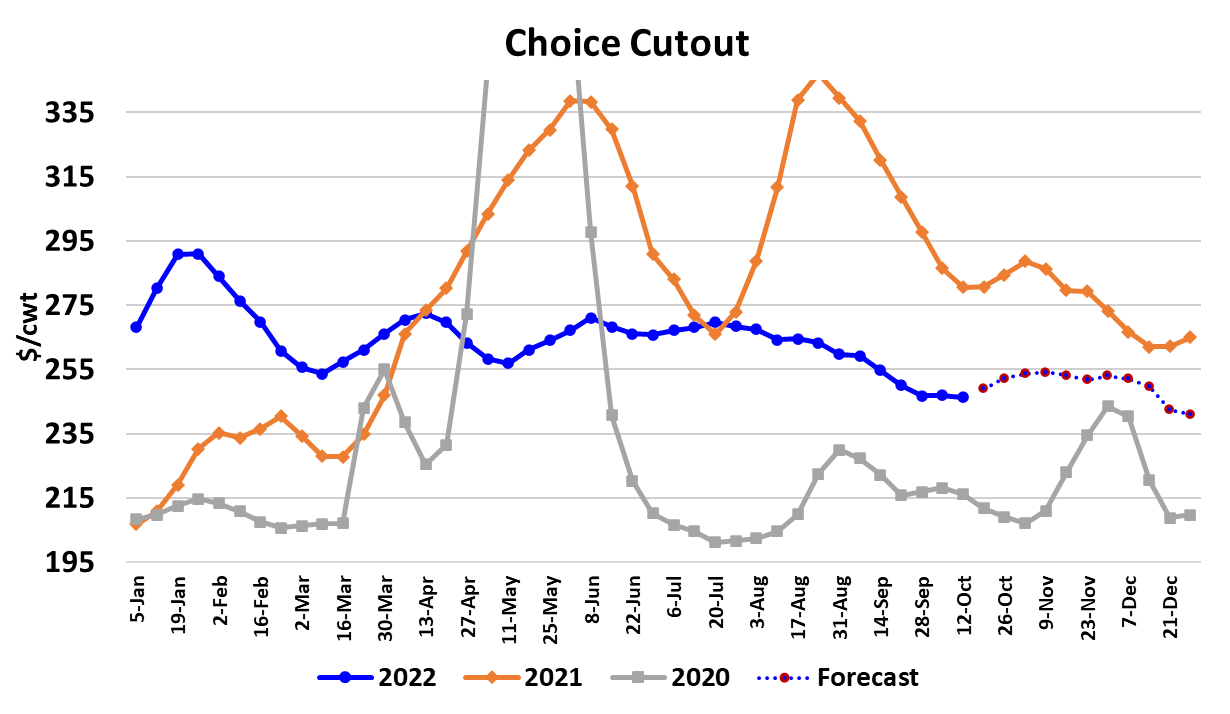

Choice cutout averaged 246.31/cwt, down $0.58 from last week.

This is the third week in a row that the Choice cutout has been

stuck at $246+change. The Select cutout was a lot weaker

however, down $4.37 on the week. Apparently no one wants

Select grade beef. They all want Choice. This caused the

Choice-Select spread to move out to $31.56/cwt. Further, the trim

markets have been on the defensive. 90s lost $4 this week and

the 50s have dropped about $30 over the past four weeks. Select

grade beef and trims (i.e., ground beef) have something in

common. They are both lower-priced alternatives that normally

see strong demand from lower income consumers. Is the market

signaling that the lower income consumers are struggling?

It has occurred to me that perhaps the beef market is becoming

more bifurcated in recent months, with the upper income

consumers still doing well and still demanding the high quality

Choice+ beef while the lower income brackets are struggling and

possibly starting to trade out of beef to other proteins. That could

be a problem because close to 40% of all beef consumed in the

US is in a ground form. That is something to keep an eye on. It

is also a little concerning that we have made it to the middle of

October with the rib primal showing very little price gain. Maybe

the holiday buying is slow to get started this year, but the rib

primal only added $4.20/cwt. this week and is only $5 higher than

it was a month ago. The Choice loin primal is dripping lower

week after week, so its not like rib demand is shifting into loins. In

fact, this week the loins and 50s were the biggest drag on the

cutout.

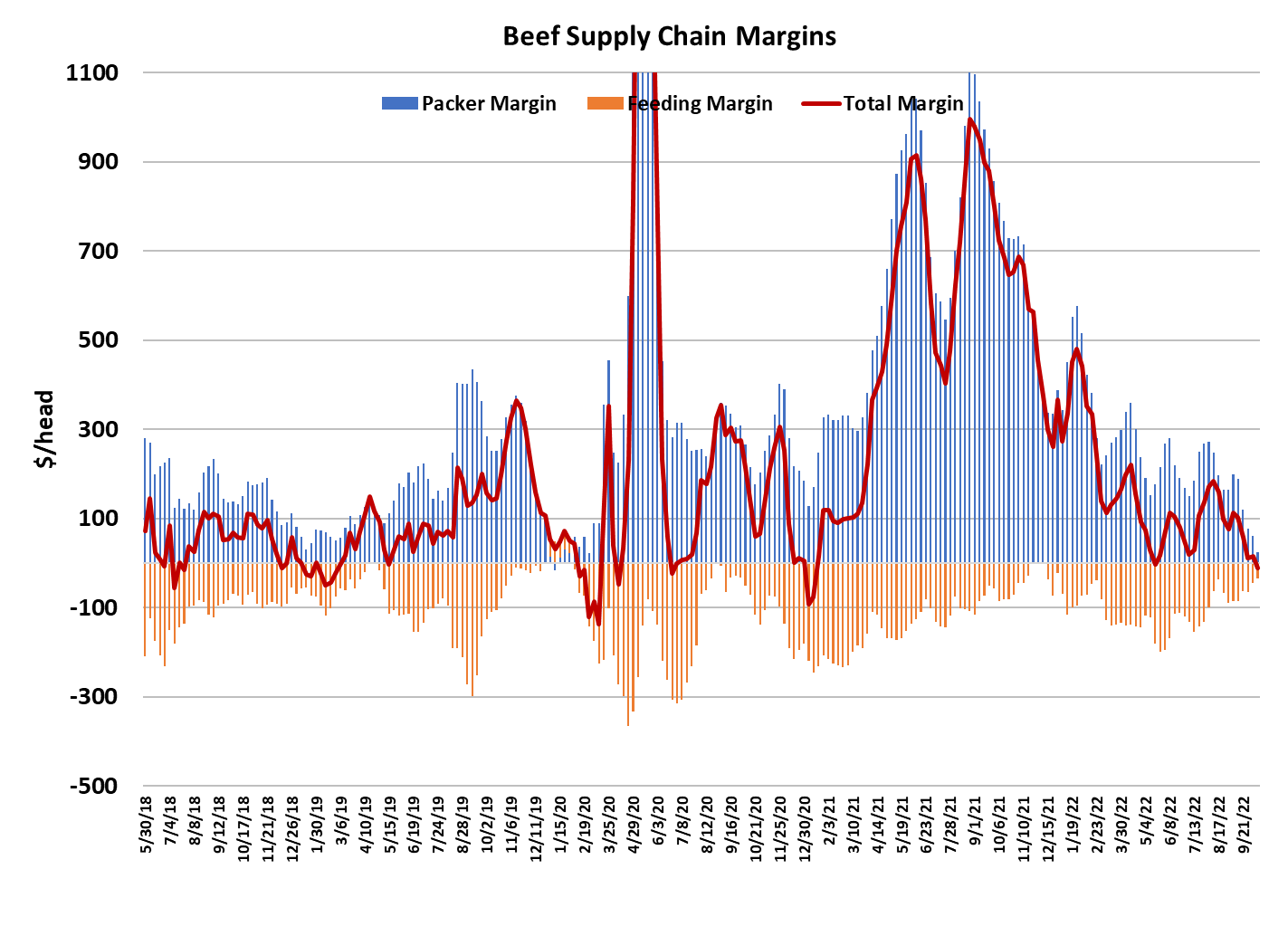

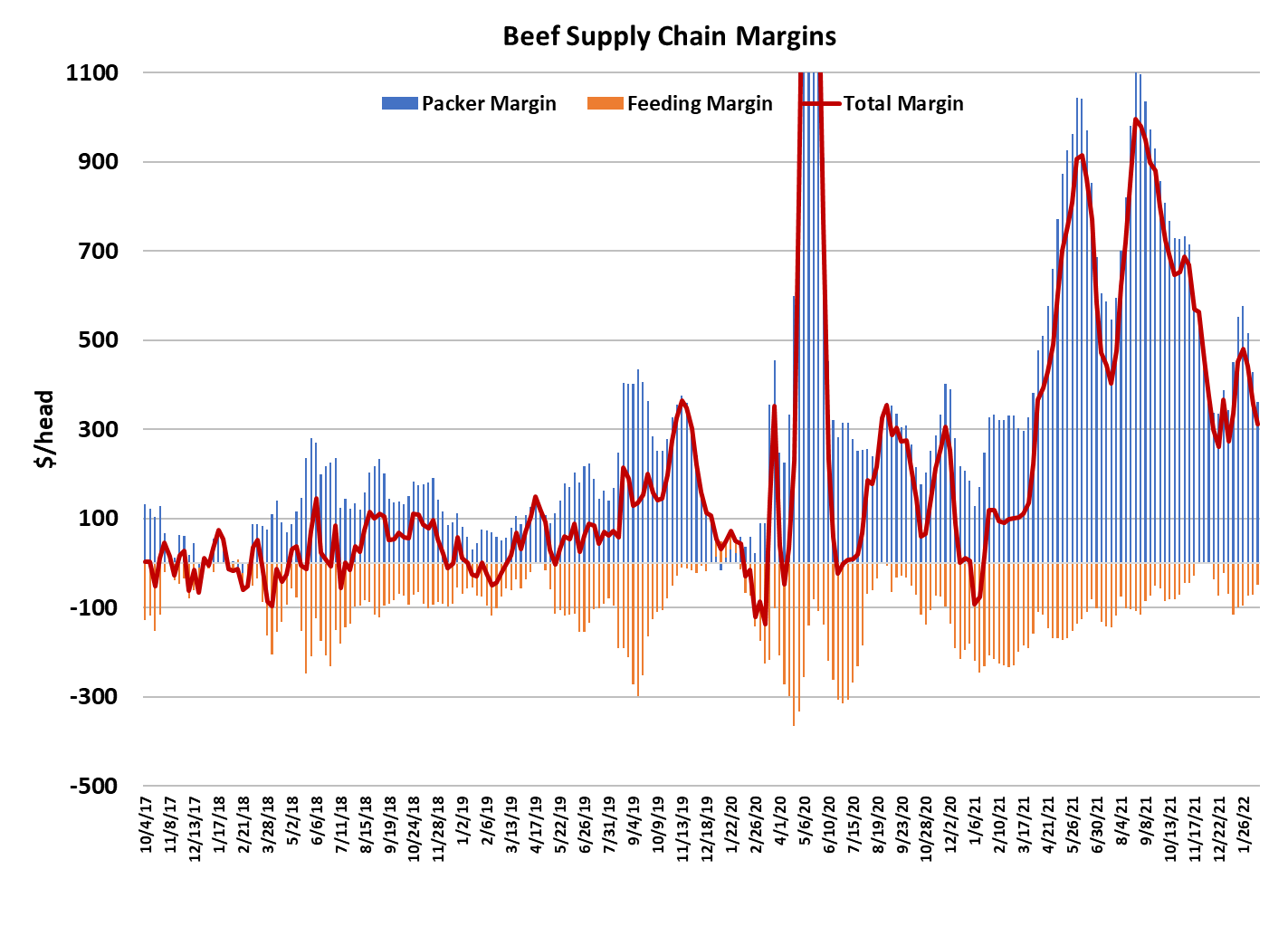

I am definitely concerned about beef demand. The combined

margin pushed into negative territory this week and isn’t yet

showing signs of turning higher. Meanwhile, cattle feeders are

acting like beef demand is strong and demanding more money for

cattle week after week. Cash cattle averaged $146.77 this week,

up about $0.50 from the week before. That pushed packer

margins down to about $25/head. Oh, how the mighty have

fallen. Gone are the days of $500+ packer margins that were

common during the pandemic. The interesting thing about that is

that packers don’t really seem to care that their margin has nearly

vanished. They aren’t making any significant attempt to restore

margins by cutting the kill. This week’s steer and heifer slaughter

totaled 513k, down only 3k from the week before. The base

numbers out of the flow model suggested that the available fed

cattle supply in October would only be about 490k per week, but

packers are definitely over-killing that target and that is helping to keep feedyards very current and give cattle feeders

the leverage they need to keep cattle prices moving upward.

Available supplies during November and December shouldn’t be

much larger than in October and we may actually be “borrowing”

some Nov/Dec cattle right now to fuel big kills. That sets up a

situation where, between now and the end of the year, packer

margin improvement is going to have to come from raising beef

prices more than pushing down on cattle prices. That probably

means that margins will stay relatively tight for at least a couple

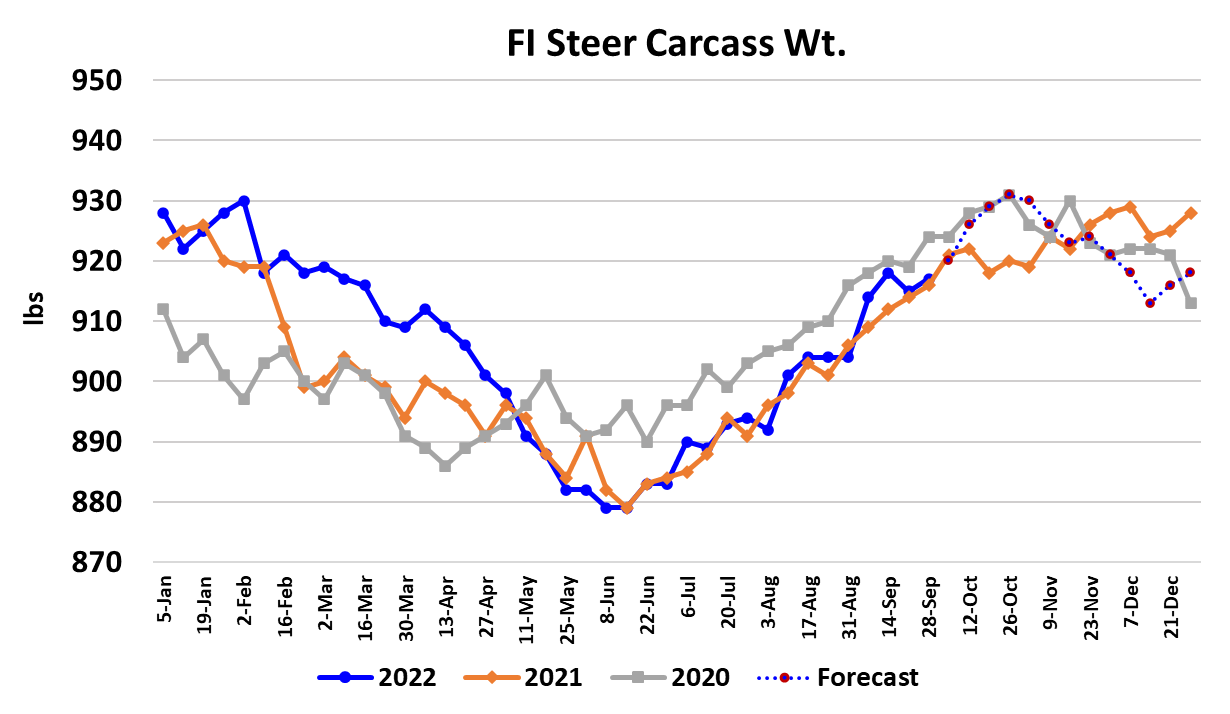

more months. Carcass weights were reported a little higher this

week, but they went up a little less than the normal seasonal

would imply, so weights continue to suggest feedyards are

staying current.

Quality grading on carcasses also improved a little bit this week,

but remains well below the historical average. USDA released its

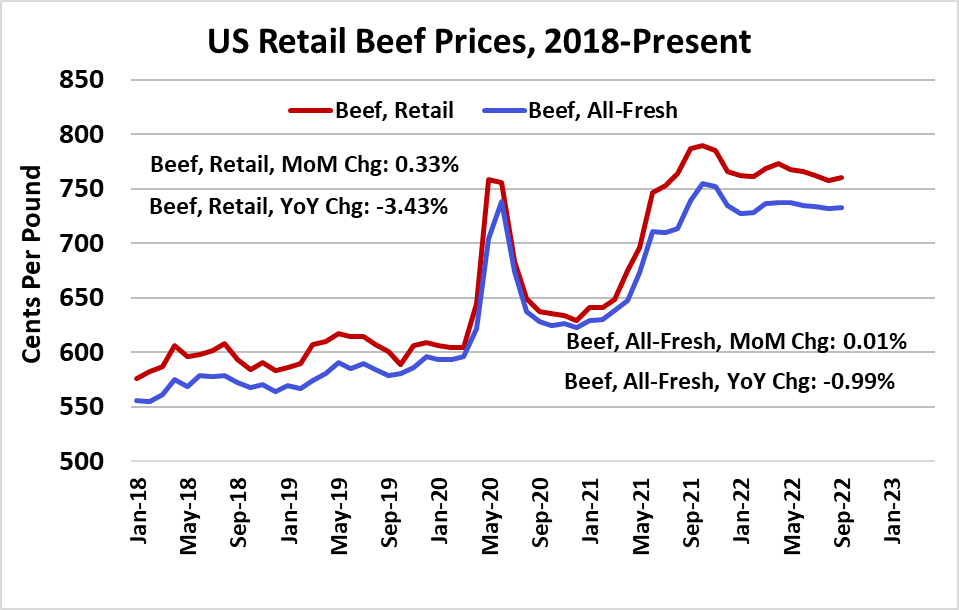

retail beef price data for September this week and it showed a

small decline from August, but still very close to last year’s level.

If retail beef prices aren’t moving much, then perhaps that is why

wholesale beef prices have been so stable recently. Regardless,

it is clear that the consumer isn’t seeing much relief from high

beef prices at the meat counter. The weekly export data for beef

continues to look relatively good and the forecast has exports

remaining strong through the balance of the year. Domestic

consumers are a bigger threat to demand than international

consumers at this point. The Consumer Price Index for

September was released this week and it was up 0.22% from

August and 8.2% higher than last year.

So price levels in the macroeconomy are still rising, but at a

much slower rate than earlier this year. That has led some to say

that inflation is receding, but I don’t think a rapid reduction in

price levels will happen anytime soon. Given that our beef

demand indexes now incorporate the CPI, this means that it is

necessary to forecast inflation levels well into the future in order

to arrive at the fundamental beef price forecast. That adds to the

complexity and definitely increases the potential error. The Fed

appears to be dead set on continuing to raise interest rates until

the labor market cools down in a meaningful way. That could

take a while and require forcing the economy into a recession in

order to achieve that goal. Recessions are never good for beef

demand. Next week, fingers crossed for a bigger gain in some of

the middle meat items, because without that packer margins

could easily move into the red. Also watch trim prices because

they seem to be indicating that the value-conscious consumer is

becoming less interested in beef.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}