Beef Wrap October 29

The cash cattle market finally made a move higher this week, with live

prices registering in the $126-127 range. It looks like the average for

the week is going to be just about $2 higher than last week. We’ve

known for a while now that smaller placements back in May, June and

July would hit the market in Q4, and so that time has finally come.

However, there is more to it than just an tightening of the overall cattle

supply. Packers are aggressively seeking out cattle that will grade well

in order to fill orders as the holidays approach. Most of the cattle that

sold at the top of the market this week ($127) were high quality cattle.

The Plain Jane cattle were the ones that sold at $125-126. The volume

of trade was pretty strong, so perhaps packers won’t need to be as

aggressive next week.

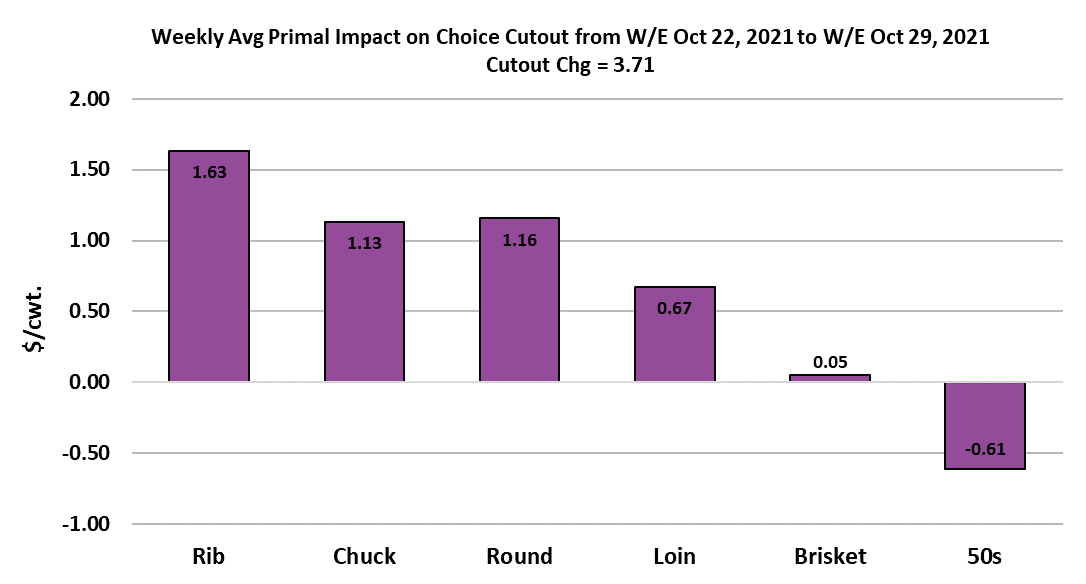

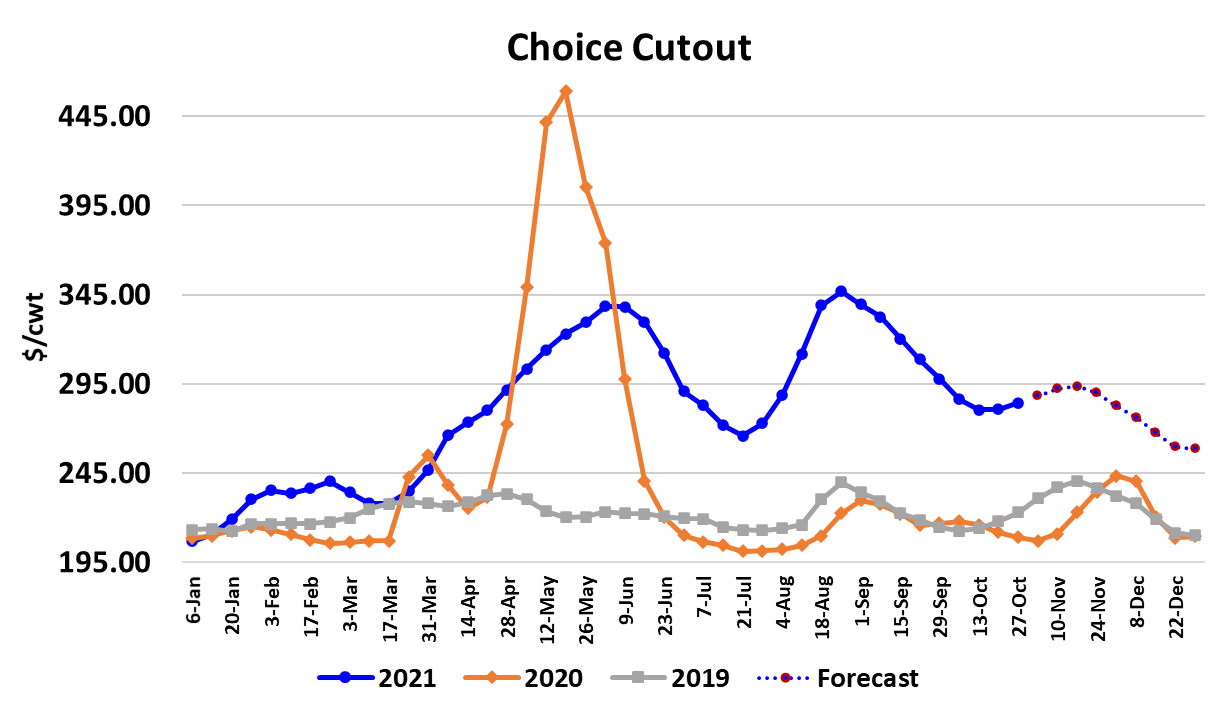

The beef cutouts were higher, with the Choice adding $3.71 on a

weekly average basis and the Select up $0.69. Nearly all of the

primals posted gains, with the end meats doing better than expected

and the middle meats gaining a little less than expected. The rib

primal took an unexpected drop during the middle of the week but then

recovered as the week came to a close. I’m looking for rib prices to

move higher for the next 3-4 weeks and then start to soften some after

Thanksgiving. The end meats are also forecast higher over the next

few weeks, but the price appreciation is not as large as for the middles.

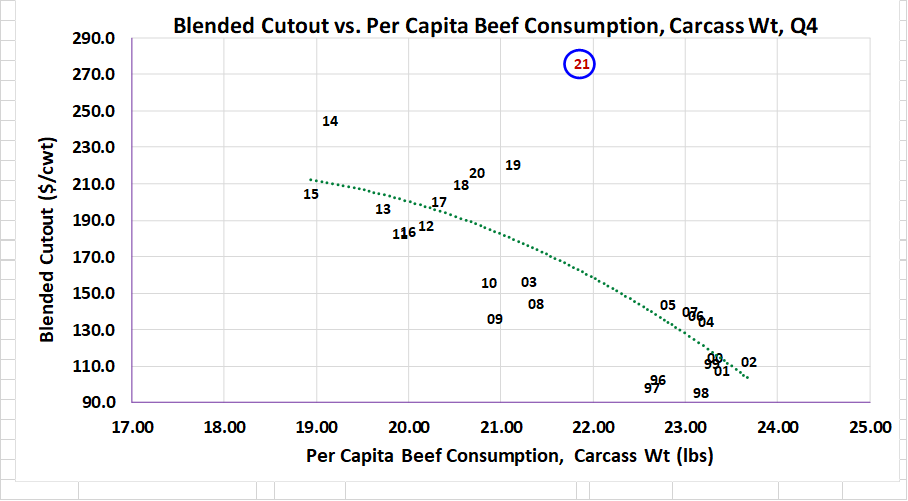

That gives me a Choice cutout forecast that tops out in the mid to high

$290s right around Thanksgiving. I’m still pretty nervous about that

forecast as I recognize the risk that the middles catch fire and drive the

cutout much higher than that. Beef production should be relatively

stable between now and Thanksgiving. This week’s fed kill came in at

520k, which was 5k greater than last week and a little above what the

flow model is projecting, so its likely that any backlogged cattle are now

getting cleaned up quickly.

That will help cattle feeders in their effort to raise cash prices, but after

November is done the expectation is that fed supplies will increase

again and thus some pressure could come back into cash cattle prices

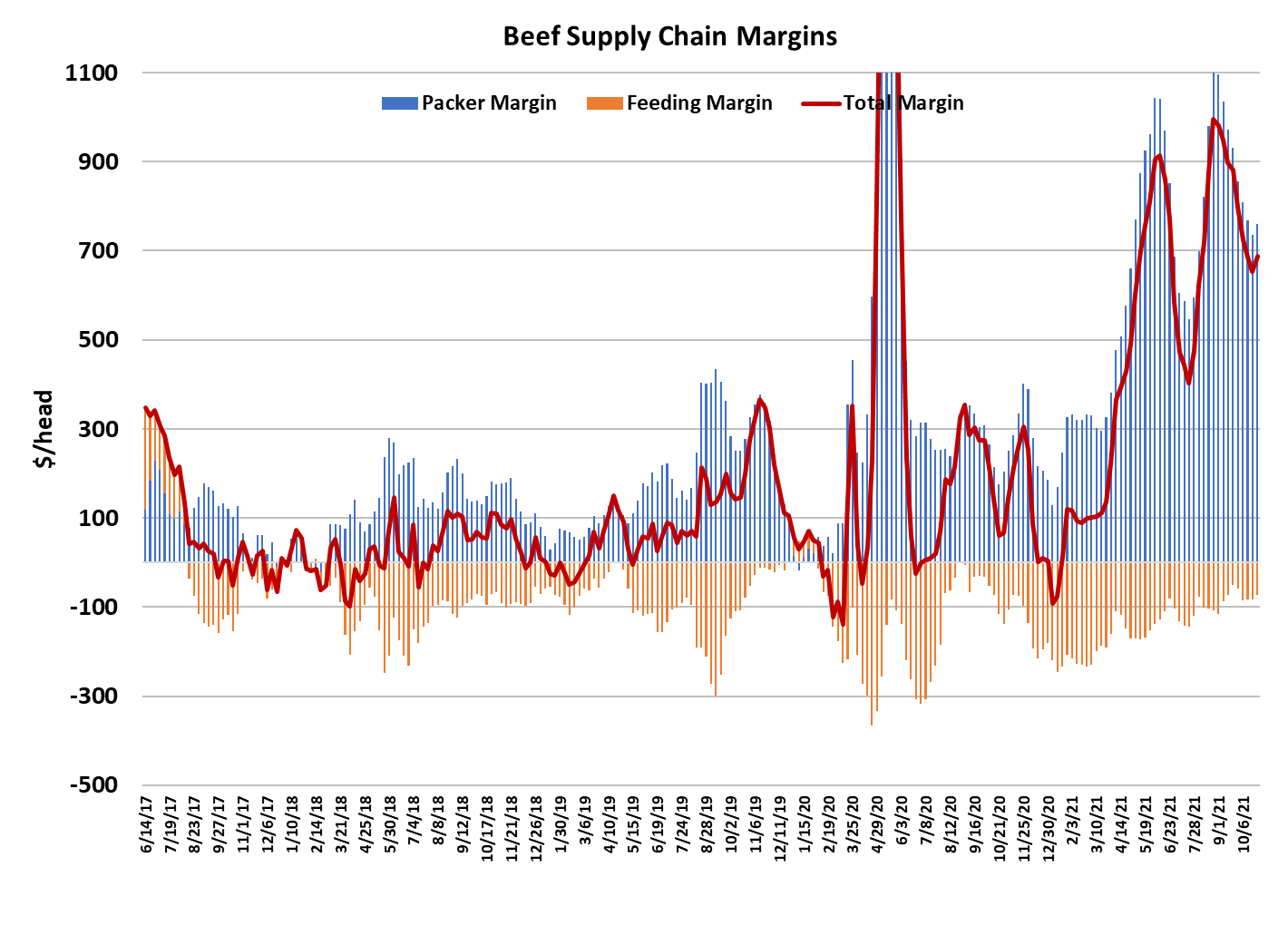

before the end of the year. Packer margins expanded a little this week

as the cutouts rose while packers were killing last week’s cheaper

cattle. I have margins now at $757/head. I think margins will stay in

the $700-800 range through November as rising cutouts help to offset

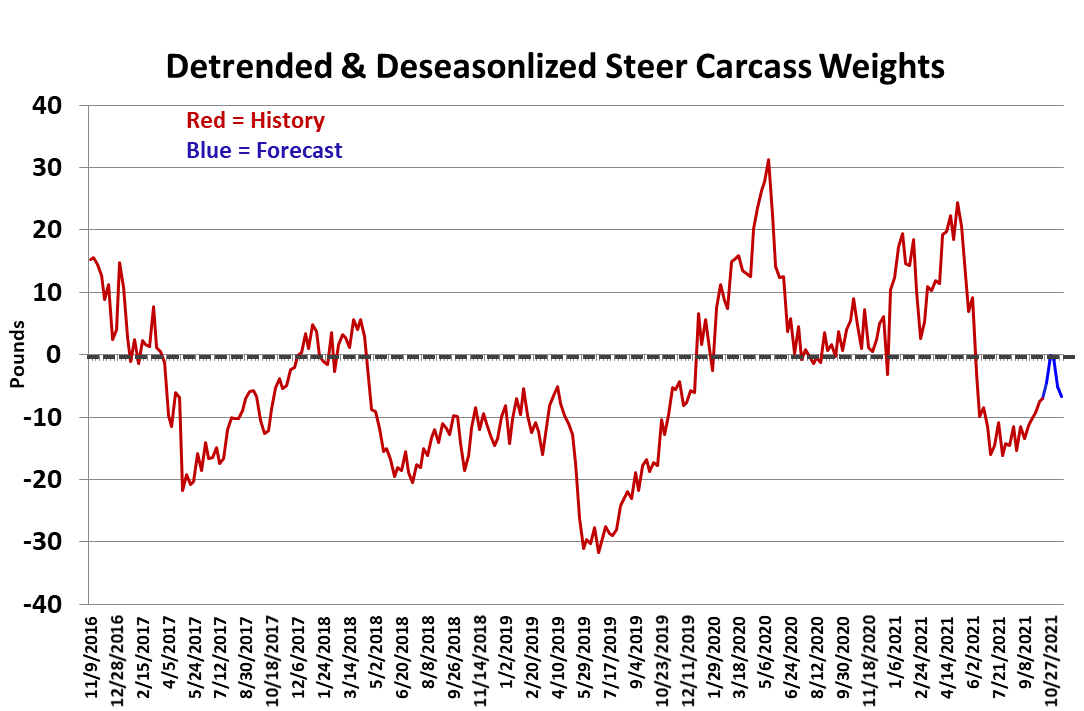

modest increases in cash cattle prices. Steer weights were reported

one pound higher this week at 922 pounds. Weights will likely make a

top sometime in the next 2-3 weeks and then start to work lower until

April. The DTDS weights are rising, which doesn’t fit very well with the

narrative that cattle supplies are tightening, but maybe they are rising

because cattle feeders are finally able to shed those heavy cattle that

were delayed in Aug/Sep.

Regardless, we need to keep a close eye on those DTDS weights

because they are right about feedyard currentness more than they are

wrong. On the demand side, it is easy to conclude that demand has

finally stabilized and started to move higher once again. We’ve seen

that in the daily demand scatters over the past week or so and the

combined margin chart below is also putting in a bottom. The real

question is whether or not this next upcycle in demand explodes

higher like it did this summer or if it’s a more subdued (and more

typical) improvement in demand. Retailers now have cheaper pork

and broiler meat that they can feature since wholesale prices in both of

those sectors are coming down. That may temper beef demand some.

The best opportunity for retailers to promote beef comes in the first two

weeks of November because after that, retailers are heavily focused

on hams and turkeys in anticipation of Thanksgiving.

Beef usually comes back to the forefront after Thanksgiving as

consumers, now sick of turkey and ham, want something different. So

I think that Thanksgiving, with its pork and poultry focus, is going to act

somewhat like a speed bump for beef demand and thus keep it from

running wild to the upside. COVID infections continue to trend lower

in the US and that, along with the proximity to the holidays, suggests

more beef being consumed in foodservice settings and less at home.

We already have ample evidence that kind of shift is not good for

overall beef demand. Retailers have pushed the price of beef at retail

to all-time record highs and they are not likely to back those down

much, especially now that they can see wholesale markets rising

again. So, there are a lot of factors that suggest to me this upcycle in

beef demand won’t be as strong as the ones this spring and summer.

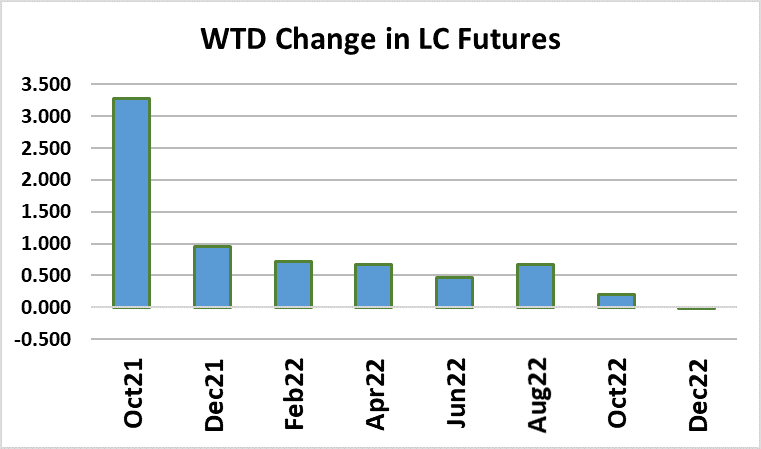

The futures market got excited this week by the higher cash trade, but

then pulled back some as the expiring Oct contract faced deliveries.

On Monday, Dec will become the nearby and will have to stand on its

own merits, without the benefit of a delivery period. Traders want to

be bullish cattle so bad it hurts, meanwhile corn futures are rallying

again and that has weighed on feeder cattle futures. Next week, watch

the primals, particularly the ribs, and keep an eye on those DTDS

weights. They might be trying to tell us something.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}