Beef Wrap November 5

Cash cattle prices took another step upward this week. Early in the

week, trade was occurring at mostly $128. Trade was rather light

because cattle feeders insisted on $130 for any additional cattle and

packers refused to pay it until Friday morning when they capitulated

and $130 was paid in all regions. When all was said and done, the

volume for the week was pretty good and it looks like the weekly

average price will be close to $129. That is up $3 from last week.

I’m sure that packers recognize prices are going to firm up, but want

to keep the process orderly and not give feeders the idea that prices

will start going up in $4 increments. Packers should now have

sufficient cattle inventories for next week’s kill.

Cattle supplies have tightened due to light placements back in May/

June/July and it just so happens that this tighter supply is coming

right at the time when packers need to fill orders for Choice middle

meats ahead of the holidays. Packers normal defense against rising

cattle prices is to scale back on the kill, but that isn’t a good option

when there are lots of orders to deliver on. Further, how could

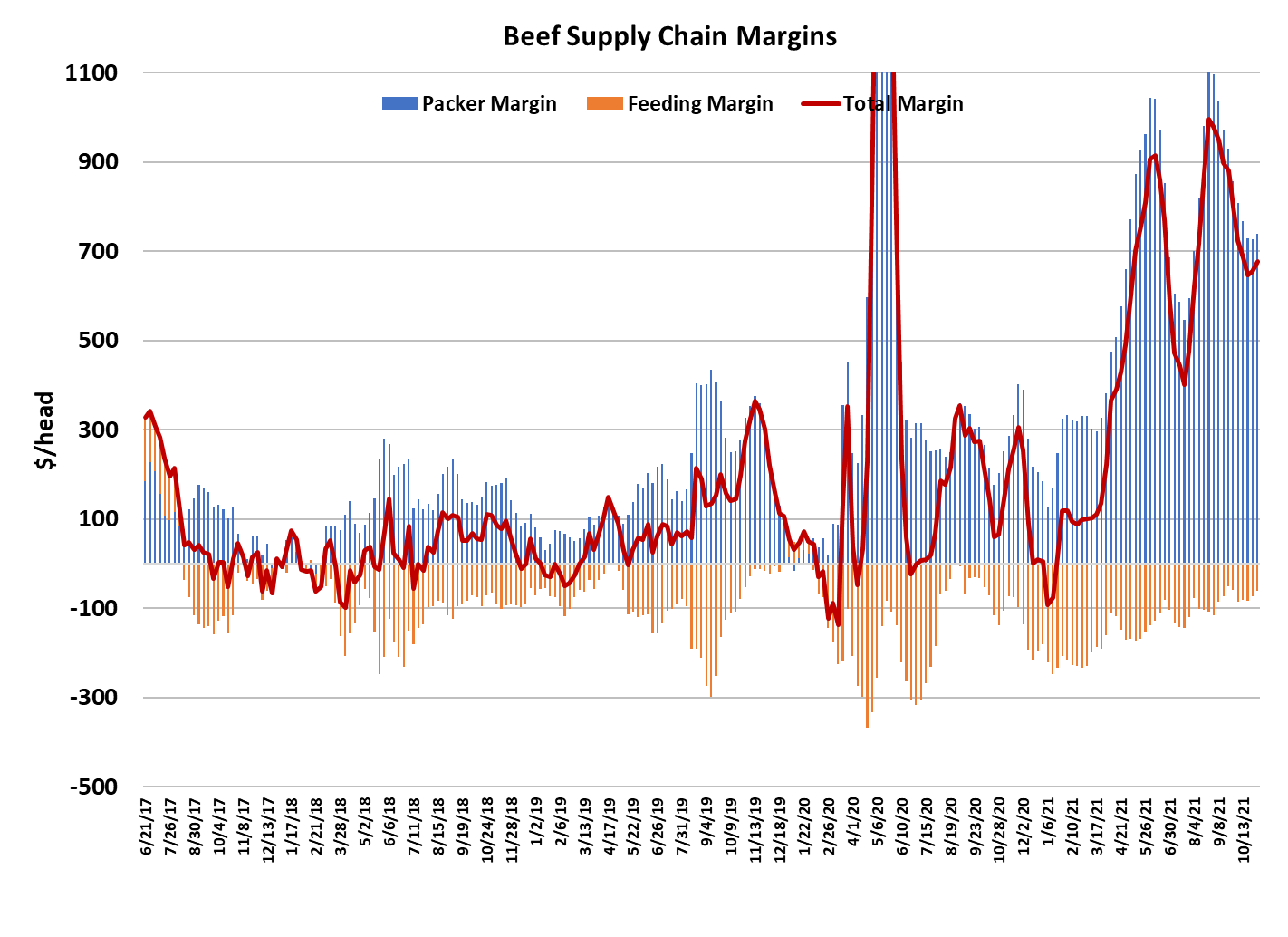

packers justify cutting the kill when their margins are $736/head this

week? No, they will pay up but they just want to keep the process

orderly. Now that we have some movement in cash cattle prices,

packer margins will no longer be determined solely by movements in

the cutout value. The cutouts are rising now, but packer margins are

not because cattle costs are rising. It looks to me like the industry

over-killed available supplies in October by about 180,000 head.

October was the first month of the 3-month stretch where supplies

should be tight.

By over-killing in October, packers have left themselves in an even

tighter supply situation here in November. By the middle of

December the supply situation could start to favor the packer again.

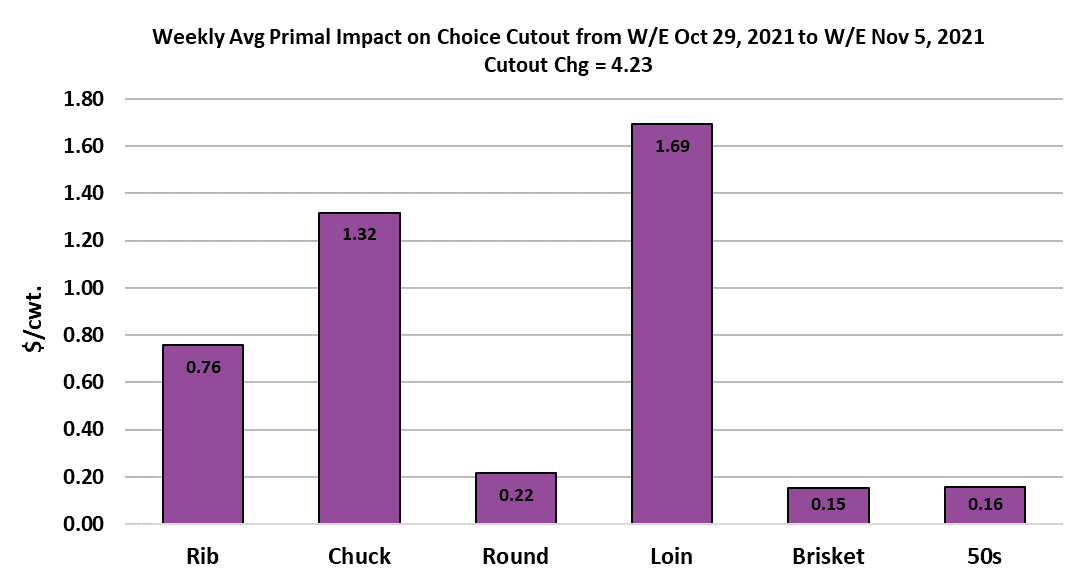

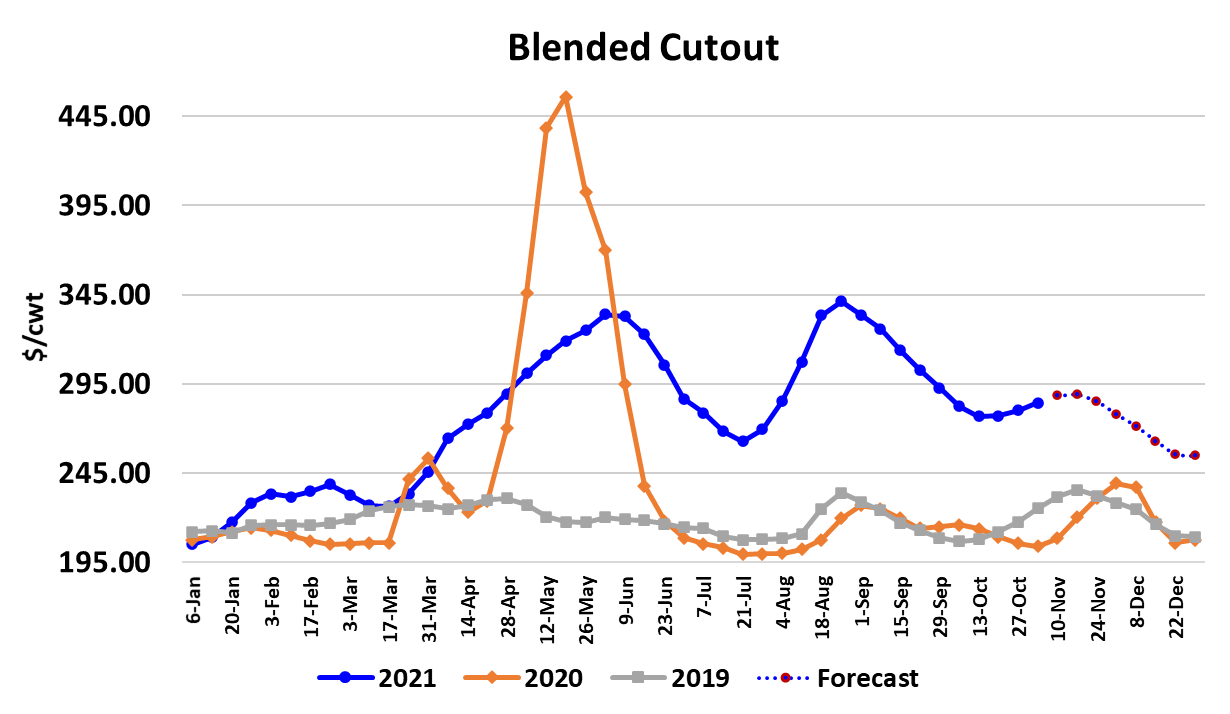

The Choice cutout gained $4.23 this week while the Select was up

$4.11. Surprisingly, gains were spread across the carcass and not

just concentrated in the middle meats as expected. In fact, I’d say

the ribs actually under-performed expectations for the first time in a

long time. The forecast still has the rib primal making gains over the

next few weeks as the final holiday push materializes. Beef is

featured prominently in retail ads down here this week, but if it clears

well the retailers won’t be looking to refill early next week. Instead,

they will use that bin space to begin staging turkeys and hams in

anticipation of the Thanksgiving ads that normally start to run about

mid-month.

So there could be a bit of a lull in demand by the retail sector in the

near term. Foodservice will likely continue to seek out those high

quality middle meats and pay up for them if need be. Foodservice

should experience stronger sales this holiday season than last due

to lower COVID infections and higher vaccination rates. However, in

the background there is the drumbeat of slowly softening beef

demand as consumers focus things besides cooking at home. That

may be masked by the holiday-driven demand, but I think it will

become much more apparent as we move beyond the holidays.

This week’s fed slaughter was only 501k, down 21k from last week.

Since June, the practical top in fed kills has been about 525k per

week and I wouldn’t expect packers to exceed that in November or

December, but they may test that level in the week’s surrounding

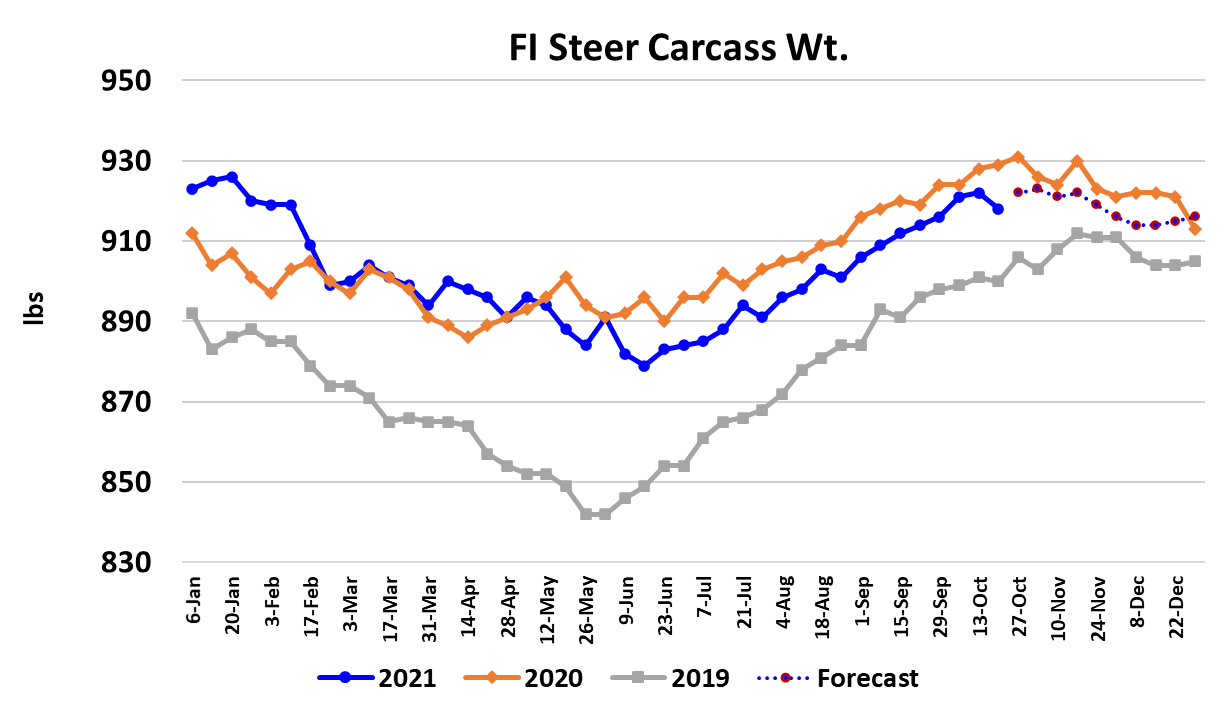

Thanksgiving. Steer carcass weights posted a surprise four pound

decline this week, but heifer weights were two pounds higher. I’m

not quite ready to declare that the top in carcass weights has been

made, but it will probably happen within a couple of weeks. The

surprise drop in steer weights this week pushed the DTDS lower, so

it is less of a concern now that it was the week before. USDA-ERS

released its official trade data for September today and it showed

total beef exports up 21% YOY. The weekly data had telegraphed

that this big increase was coming, thus it shouldn’t be much of a

surprise. The YOY comparisons get much tougher in the last three

months of the year and the weekly export data has been softer, so I

wouldn’t expect these big YOY export gains to persist.

Futures traders got excited on Tues and Wed at the prospects for

higher cash trade and pushed the Dec contact above last week’s

high. However, when cash cattle prices didn’t advance beyond

$128 at mid-week, traders expressed their disappointment by

pushing the futures lower on Thursday. When the $130 trade broke

out Friday morning, the board quickly lit up green. For the week, the

Dec contract gained a little over $2.50. The back months remain

strong. Right now the 2022 futures curve is projecting an average

cash cattle price of $136. Average prices in 2021 will be around

$122. In 2020 they were only $103. Next week, look for another

advance in cash cattle and some further gains in the beef cutouts.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}