Beef Wrap October 22

The big news in the cattle and beef complex this week was the

stabilization of the cutouts. After declining for the past two months, the

cutouts actually posted tiny gains this week. The Choice was up $0.15

on a weekly average basis and the Select was up $0.99. To be sure,

those gains are really small, but after several weeks where the cutouts

fell $10 or more, these small gains were welcomed by market bulls.

The cash cattle market was a little higher also, with live prices adding

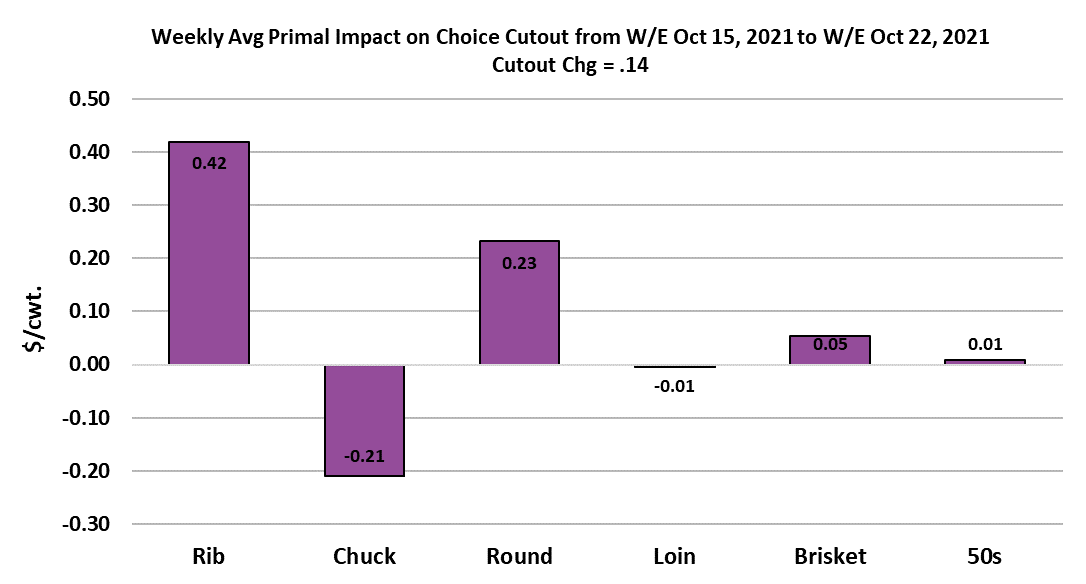

$0.48/cwt to $124.32. The chart to the right indicates that it was the rib and

round primals that were largely responsible for steadying the cutout this

week. The explanation for the ribs is easy—there is still some holiday

business to be done and price levels finally got down to a level that

enticed more buyers into the market.

The gains in the rounds are a little more difficult to explain, but this is

the time of year when retailers have traditionally featured beef roasts.

Also, the price of lean grinding beef remains very high and that is

probably helping to support both the rounds and the chucks. The

interesting thing about this bottom in the beef market is that it was a

much softer landing than what we saw earlier this summer when the

beef market made a more V-shaped bottom, bouncing $7 higher in very

short order once the bottom was made. This time, the demand side is

not as rosy as it was this summer and beef production is larger (owing

to seasonal increases in carcass weights). Thus we probably won’t

see the cutout start to gain $10/week anytime soon. Those that watch

the beef market are familiar with how quickly rib and tenderloin prices

can accelerate at this time of year, but this year it appears that a large

proportion of users planned ahead and put product away in deep chill

programs in late summer and early fall.

That should help bridle this year’s holiday rib rally and prices are

expected to rise at a more controlled pace. In fact, it is entirely possible

that price declines in parts of the carcass outside of the middle meats

could outpace the gains in the ribs and thus the cutout as a whole may

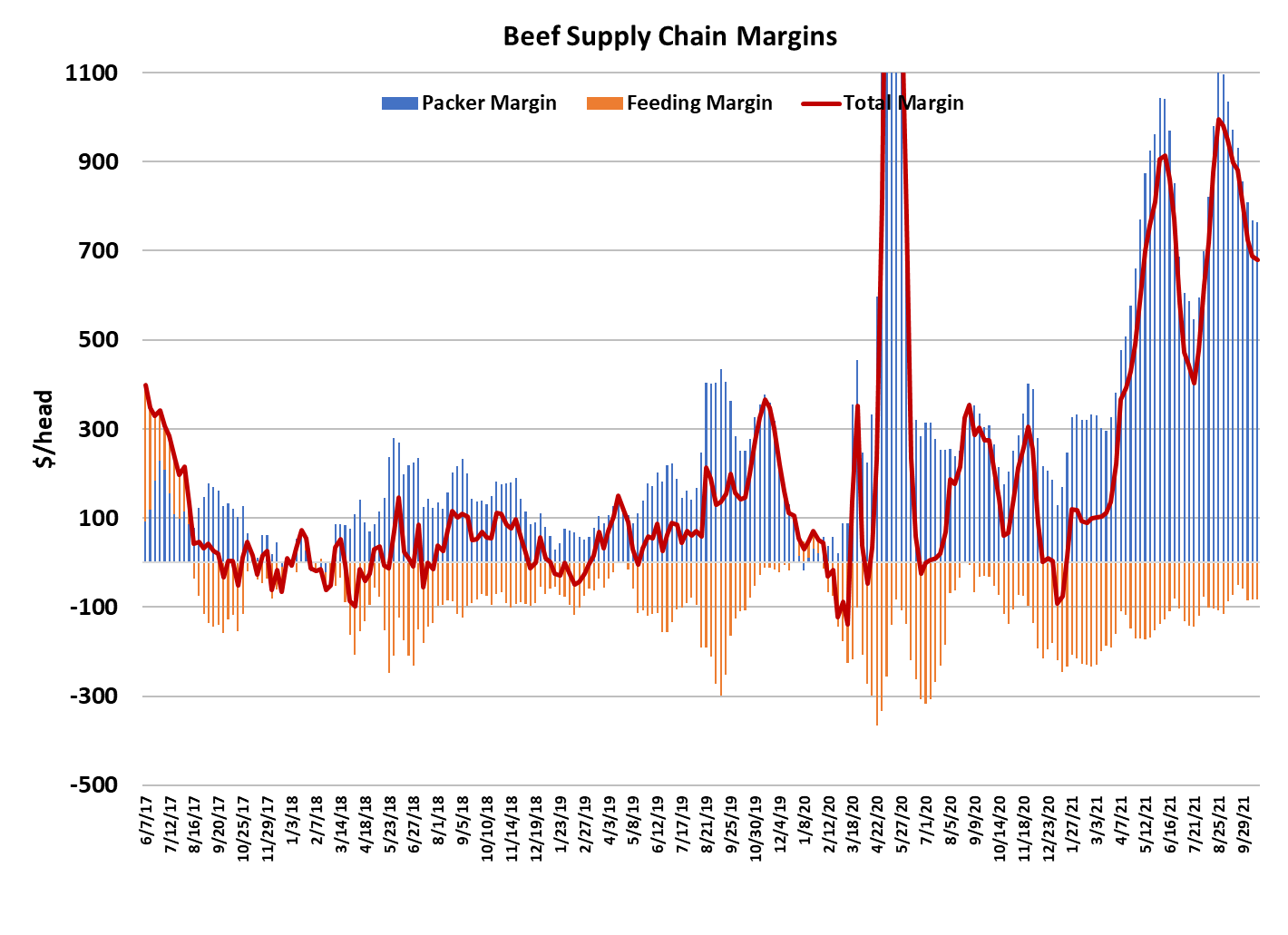

not show a huge amount of appreciation in the weeks ahead. Packer

margins only declined about $5 this week to $736/head and one would

think that if the cutouts are going to move higher then packer margins

should also expand because cash cattle prices don’t seem to be going

anywhere. However, I expect that as the cutouts improve in the next

few weeks that cattle feeders will manage to get a few more dollars out

of packers and that will help to constrain margin growth. I’m not looking

for a huge rally in cash cattle prices, perhaps only into the $127-128

range from today’s level near $124. If the cutouts can’t sustain

reasonable gains, then the outlook for an advance in the cattle market

dims. Beef demand appears to be slowly eroding in much the same

way as pork demand is slipping.

The free money from the government to consumers has slowed down

dramatically. Vaccinations are up and COVID infections are down,

thus consumers can get out of the house more and they aren’t as

focused on at-home meal preparation as they were when the

pandemic was raging. So it is reasonable to expect demand to be

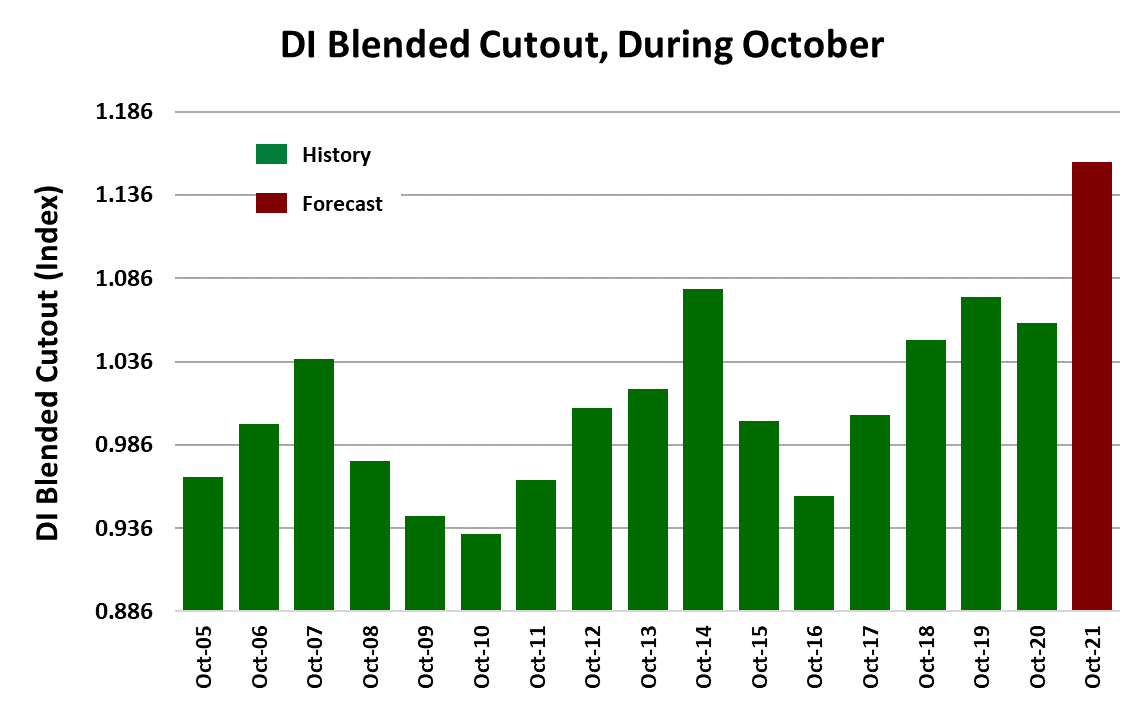

cooling down. It looks like the demand index for October is going to

come in close to 1.16 after averaging over 1.20 in June through

September. But don’t take that to mean that demand is poor. That

1.16 demand index for the blended cutout is the highest it has ever

been during the month of October, by a long shot. The next highest

was an index of 1.08 in October, 2014. The combined margin, which

had been trending lower looks like it may be carving out a bottom and

could turn a little higher if holiday demand for ribs turns out to be

stronger than expected.

International demand for US beef also seems to be waning a bit as the

recent weekly export numbers haven’t looked as rosy as they were

earlier in the year. China is still taking big quantities of US beef, but

movement to some of the more traditional destinations like Japan and

Mexico and even Canada seem to be running a little softer recently.

USDA released its cold storage survey results for the end of

September this afternoon and it showed that beef in cold storage grew

about 5% from August, but is still 6% below last year’s level. The

government economists also released a fresh Cattle on Feed survey

this afternoon, which showed September placements down 2.9% from

last year. That was bit of a surprise given that the average analyst

prediction was for placements to be up about 1.4%. This week’s fed kill

came in at 513k, up 7k from last week.

I expect the fed kill to remain in the 500-510k range for the next few

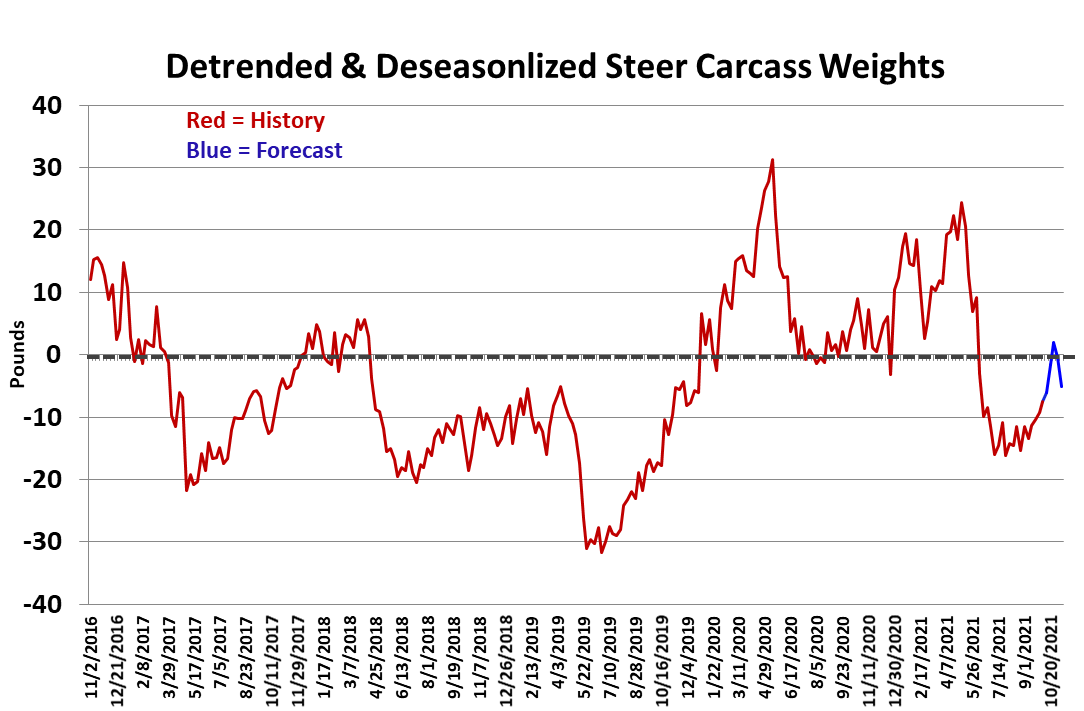

weeks before expanding some as December approaches. Carcass

weights are still rising seasonally and should top within a month or so.

The DTDS is also rising, which does raise some concerns about

feedyard currentness. Next week, watch the ribs and tenders for the

speed at which prices increase. The direction and velocity of those

two items will have a lot to say about the direction of the cutout, and

thus the market tone, in coming weeks. Cattle supplies are in the

process of tightening up right now due to relatively small placements in

May/June/July and we know that packers will start delivering on

holiday orders during November, so there will be incentive to make

sure that all of the beef that was promised to buyers is available. It

really won’t kill packers to pay an additional $2-4 for cattle in upcoming

weeks given how large their margins are. Much will depend on how

much lift buyers provide to the cutouts in the next few weeks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}