Beef Wrap October 28

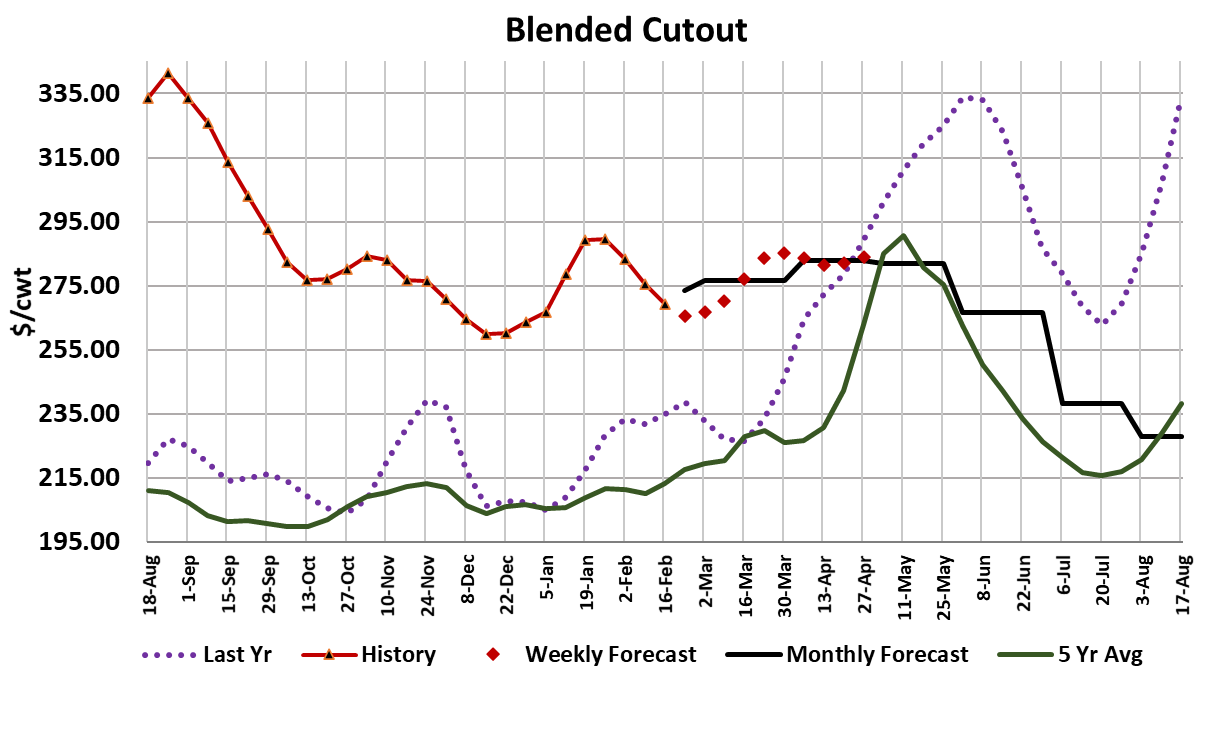

The seasonal increase in beef prices got underway in earnest this

week, with the Choice cutout gaining $9.26/cwt. and the Select

cutout up $7.69/cwt. Of course, when cattle feeders saw that,

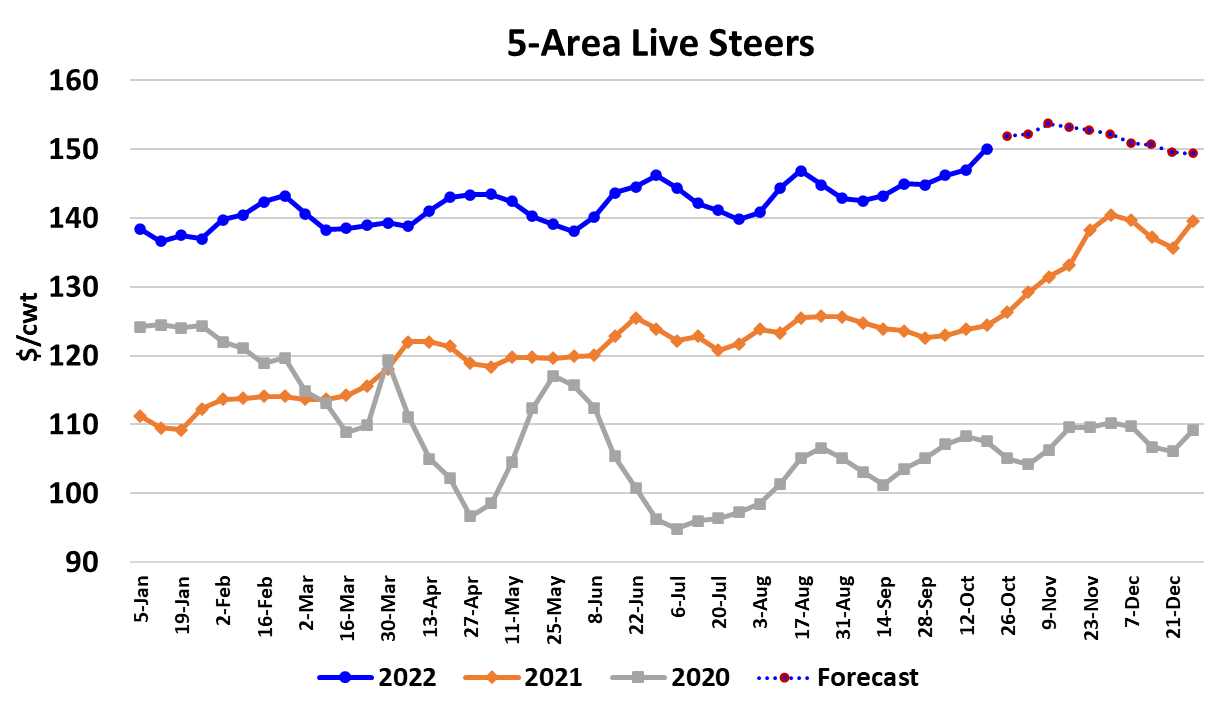

they wanted their piece of the pie, and they got it. Cash cattle

prices advanced almost $2/cwt. to finish the week very close to

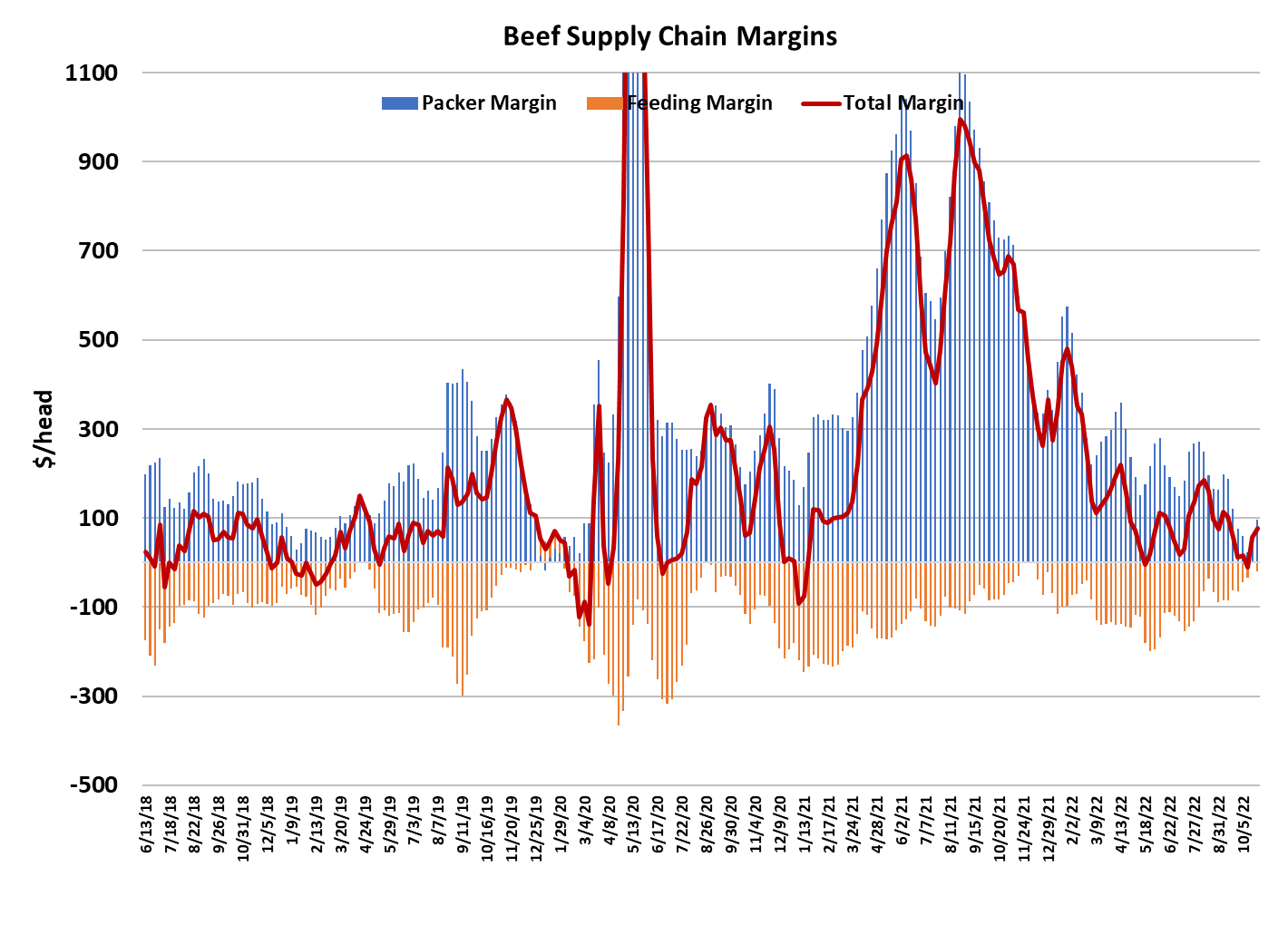

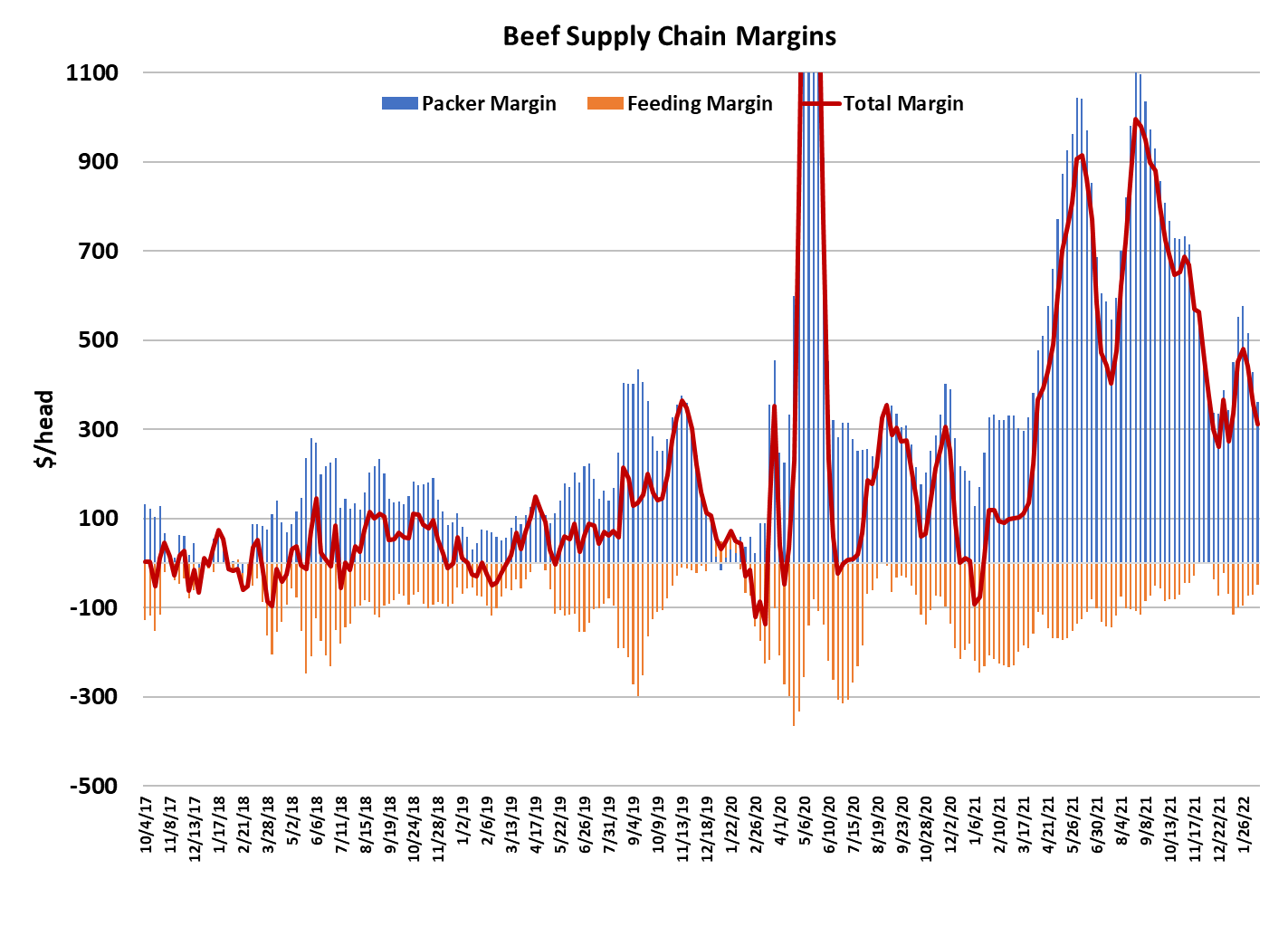

$152/cwt. Since the beef moved up more than cattle, packer

margins expanded and are now back close to $95/head. It is

considerably easier to get packers to pay up for cattle when the

boxes are advancing rapidly as they did this week, but I suspect

that when the boxes turn lower a few weeks from now, that cattle

feeders will not want to give back any of the ground they have

gained in the cash market. At the moment, neither packers or

feeders are too concerned about it because both markets are

rising, but the cutout normally makes its seasonal top just before

Thanksgiving and the calendar will turn to November next week.

That means there might only be 2-3 more weeks of seasonal

increases in the beef before the cutouts falter force packers to

make some tough decisions about how they are going to reset

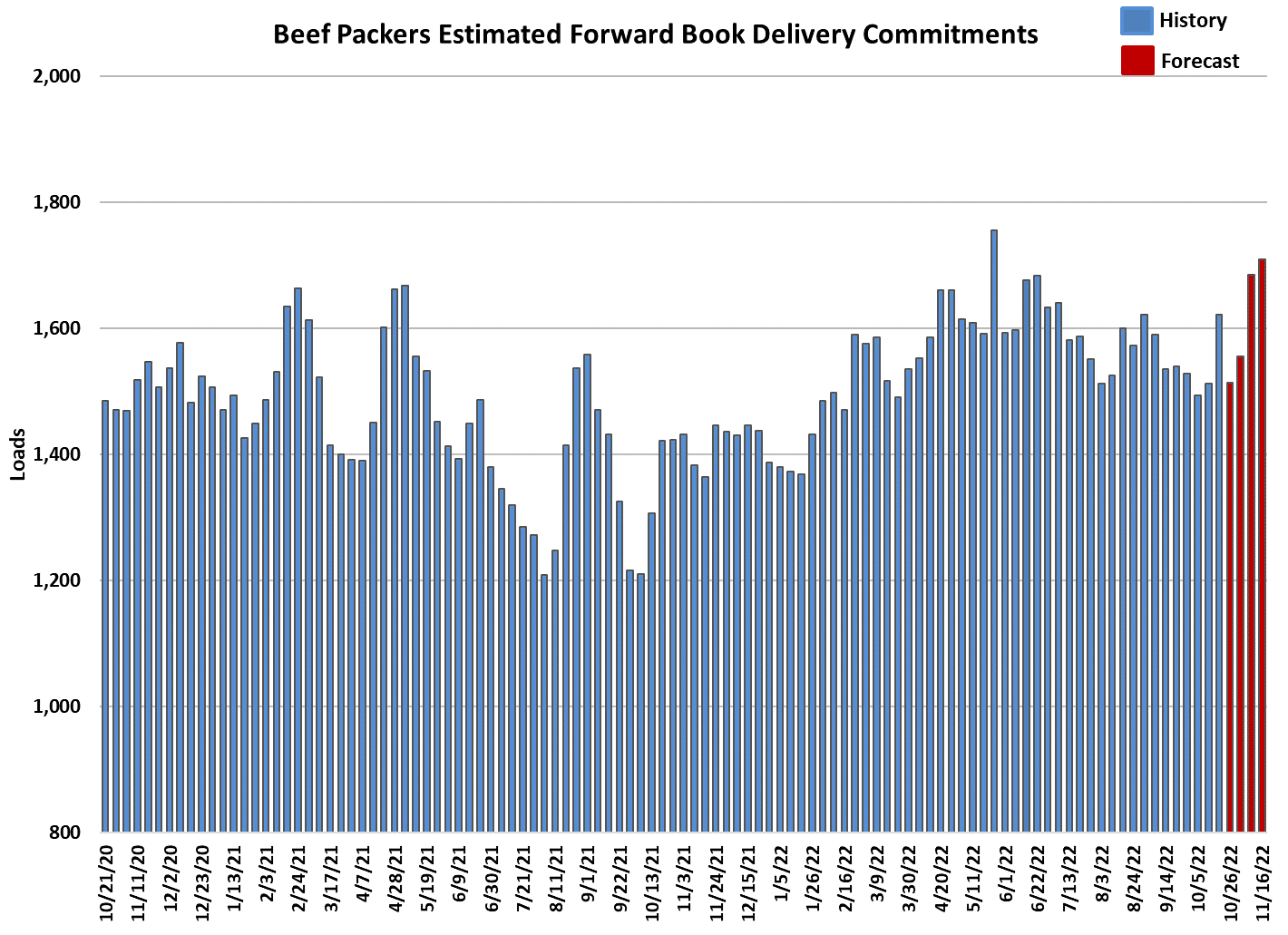

cattle feeders’ price expectations. I think that packers hands are

going to be tied over the next couple of weeks due to the fact that

they have forward sold a lot of beef that will beef that will need to

be delivered in the second half of November (see attached chart).

When packers have a big forward book to fulfill, slowing down the

kill is not a viable option so they normally end up paying what

cattle feeders want. That means we could be looking at another

couple of weeks where the cash cattle market advances $2 or $3

per week. However, once the orders have been delivered, the

cutouts are likely to be in the process of turning lower and that will

give packers a lot of financial incentive to reverse the gains in the

cattle market.

That is when the fight is likely break out. Normally, packers have

the upper hand in those types of price skirmishes because they

can always slash the kill, but for some reason packers have been

reluctant to bring out that powerful weapon in the last few months.

If they don’t get a better handle on the cattle market they are likely

to have some serious margin woes as we move into next year.

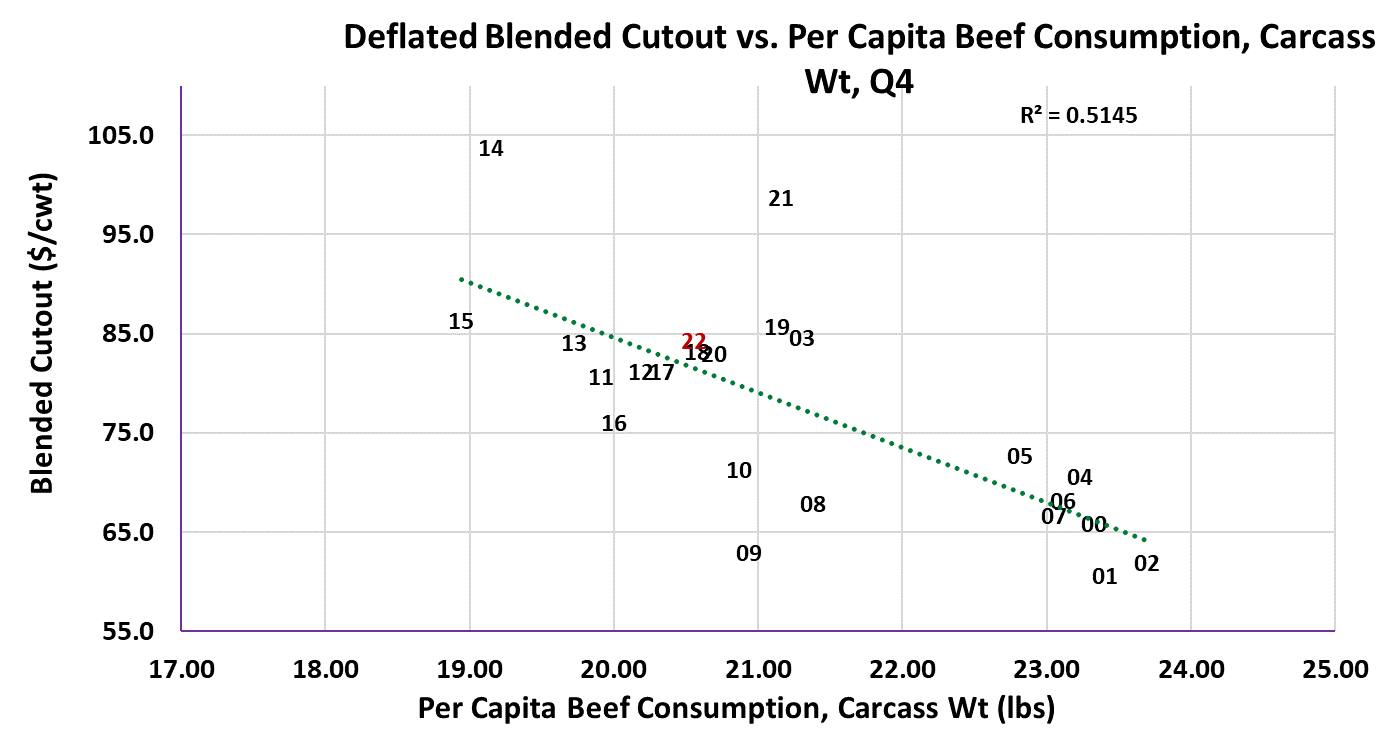

Beef demand in Jan/Feb is usually way softer than in Nov/Dec and

that means considerably lower cutouts early next year. However,

the futures market is now pricing cattle in February $3 higher than

in December. If packers allow that to come true, we could see

significant red ink on packer income statements in Q1. This

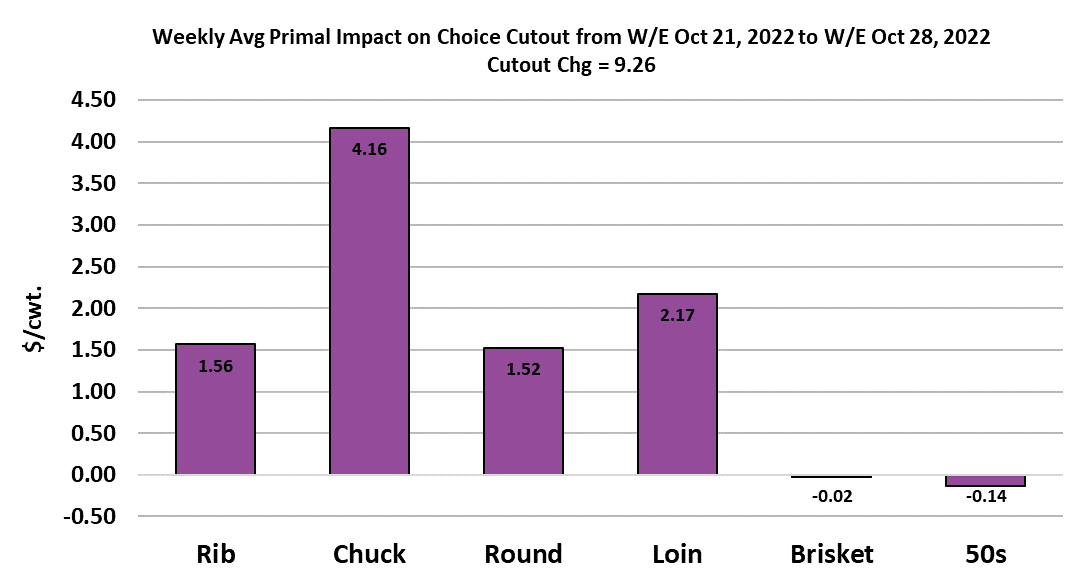

week’s gains in the cutout were more spread out across the

carcass than expected.

The middle meats were expected to contribute a nice chunk, and

they did, but the surprise was that the chucks and rounds also

showed strength. My feeling is that the ends won’t be able to

keep pace with the middles in the next few weeks and we will

likely see the ribs take a bigger leadership role. Beef demand is

in and upcycle now and the combined margin is confirming that,

but I’m a little concerned that this upcycle will be shorter than

most and fail to reach the tops that have been common in recent

cycles. Further, the next downcycle will likely coincide with the

completion of the holiday business and thus it might be deeper

than in recent lows. The macro picture still looks pretty dark and

the odds of a recession remain relatively high. The stock market

has recovered a bit lately, so that might help consumer

confidence heading into the holidays, but I’m more concerned

about what will happen once we are beyond the holidays.

The supply side of the market looks pretty good at present. This

week’s steer and heifer kill clocked in at 515k, still about 10-15k

more than what our model suggests should be available. Steer

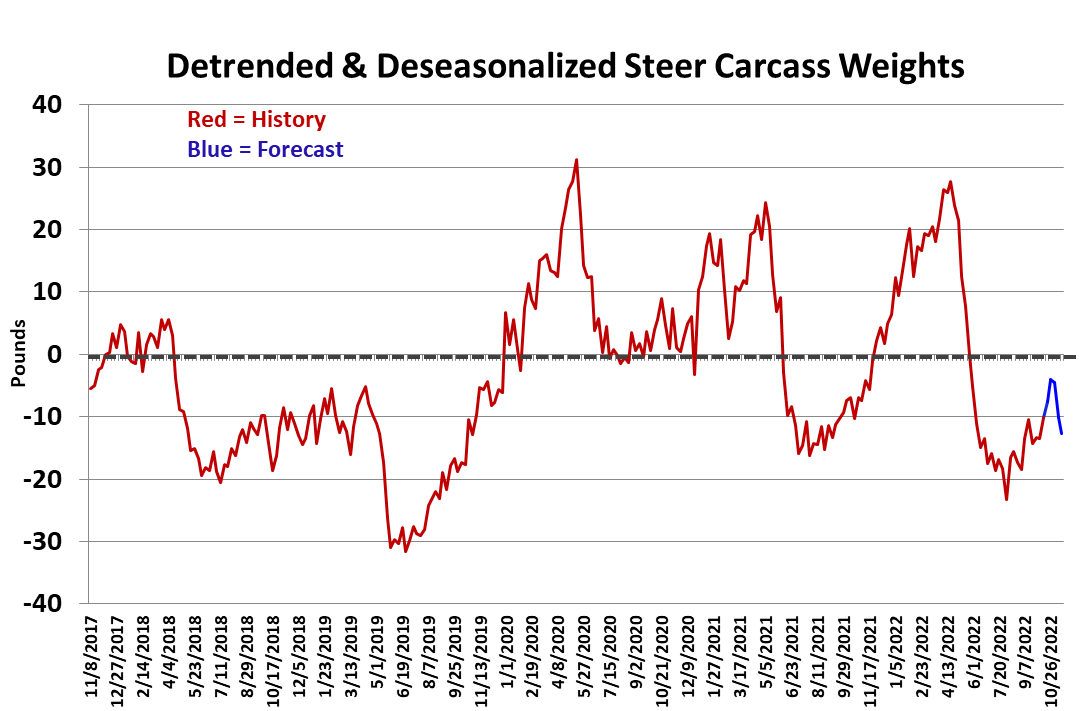

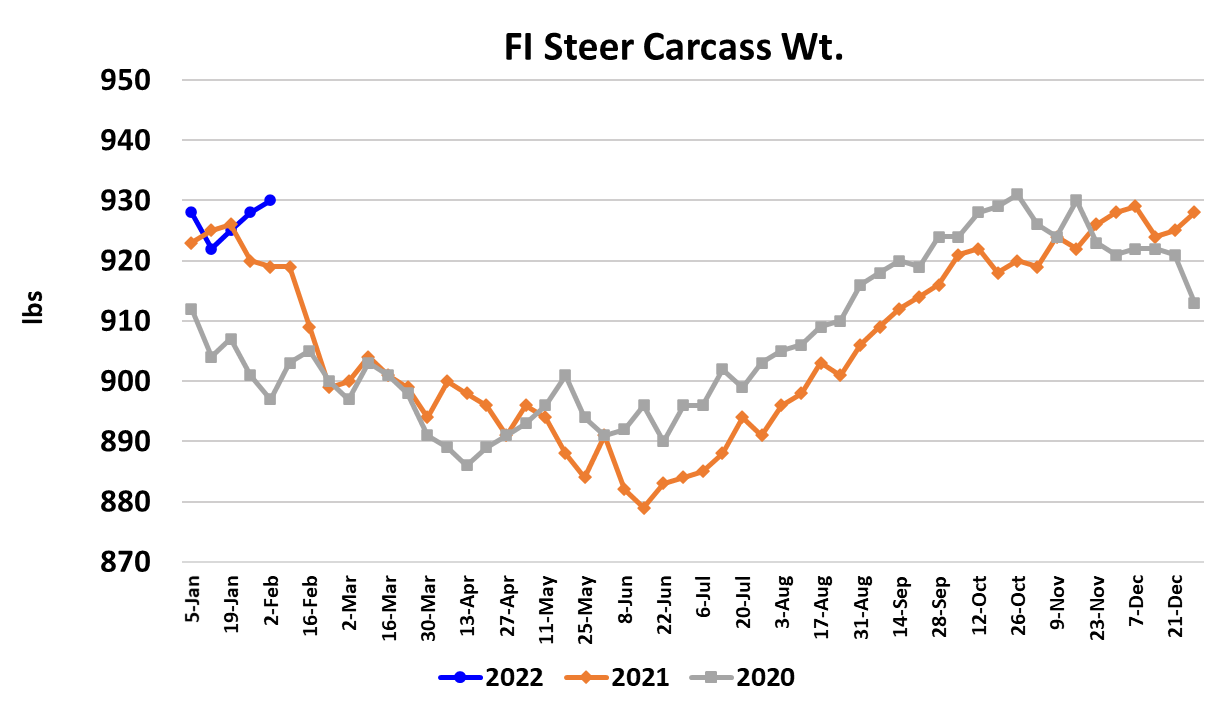

carcass weights were up four pounds this week and that is

helping add to the beef supply. However, weights are only a few

weeks from topping and turning lower. The DTDS weights have

risen a bit in the past few weeks and that seems to support the

idea that feedyards are becoming less current, but that is at odds

with the fact that we are seeing larger-than-expected fed kills

week after week. Maybe packers have been borrowing some

cattle from November to fuel big kills in October.

The flow model suggests that November fed kills should be

around 510k in the non-holiday weeks, but with the big forward

book coming due, there is a decent chance that early November

kills will exceed that level. Beef exports seem to be holding up

well and we will find out more next Friday when USDA releases

the trade data for September. Overall, I’d say the market seems

to be in good balance right now and behaving more normal than

it has in the past three years. There are still a few quirks that

seem odd, like packers refusing to cut the kill in the face of tight

margins, but taken as a whole the market seems to be performing

smoothly. Next week, watch for the gains in the middle meats to

outpace the ends and lead the cutout higher. Cash cattle are

likely to advance again and the futures market will probably

applaud again.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}