Beef Wrap November 4

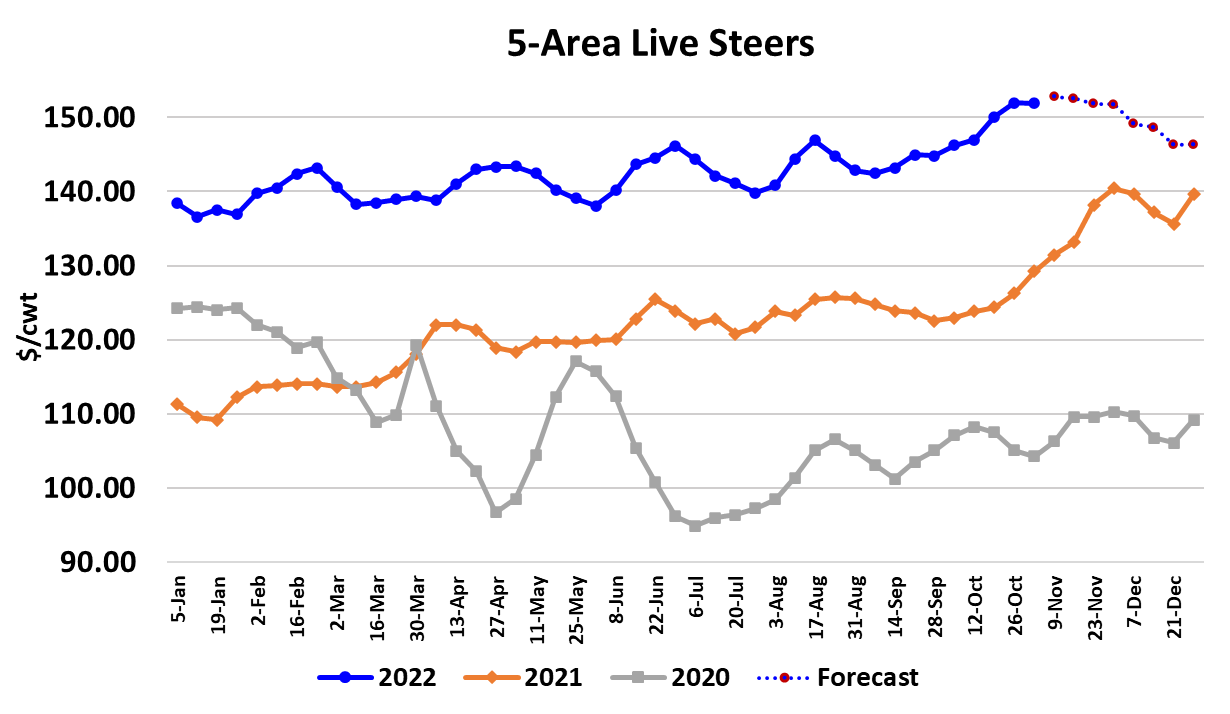

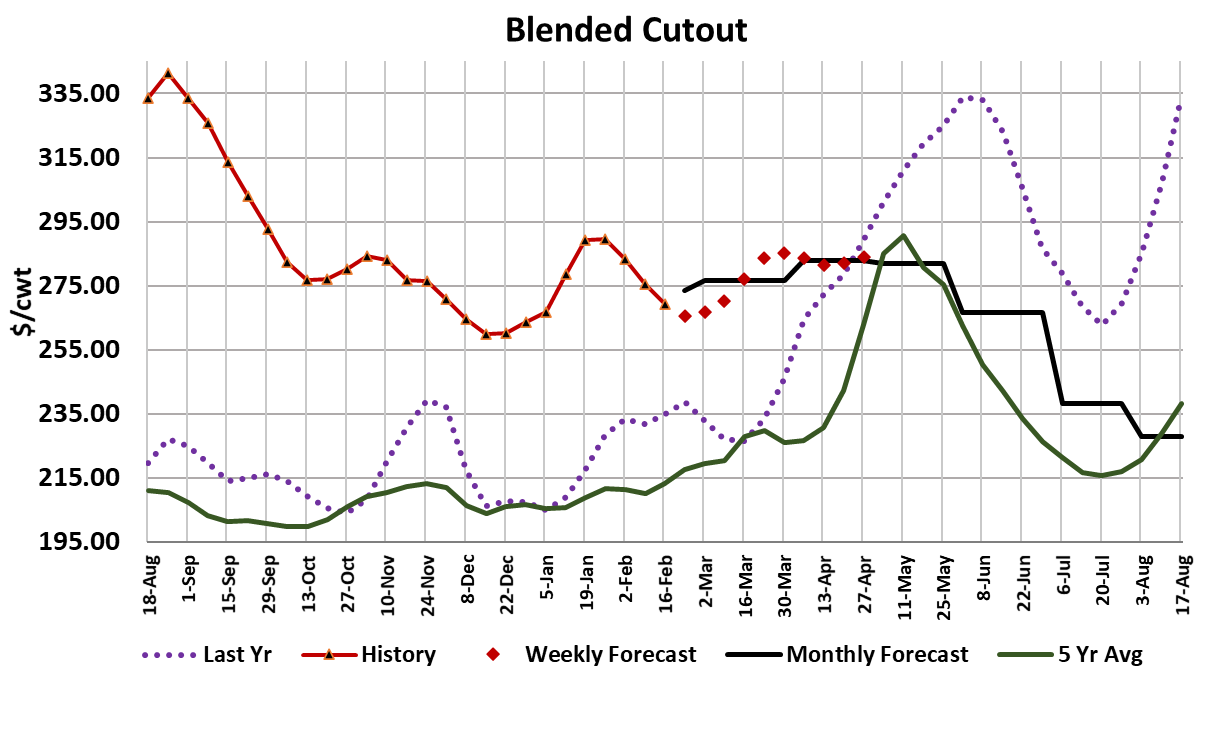

The cash cattle market took some time to catch its breath this week,

with prices almost steady with last week and near $152/cwt. At the

same time, the Choice cutout was up $2.54/cwt. and the Select

gained $3.47/cwt. Prior to this week, cash cattle were up a total of

$5/cwt. in the previous two weeks, so it isn’t surprising that the

market took a little pause. As always though, the big question is,

“Where does it go from here?” Cattle feeders still seem to be pretty

bulled up and they are of the mindset that they got trampled on by

the packers over the past three years and so now it is their turn to

take a bigger share of the margin pie. So, they will continue to

press prices higher and I’m not sure that packers have much power

to resist in the short run. They have a large book for forward-sold

beef to deliver on in the next 2-3 weeks and a lot of that beef will be

of the higher-quality variety, so cutting the kill to keep cattle prices in

check isn’t really an option right now.

However, the spot beef market isn’t really performing as strong as it

should be at this time of year, so continuing to pay up for cattle puts

them at risk of running their margins into the ground. I think that

packers hands are tied in the short run, so some further cattle price

increases are likely in the next couple of weeks and perhaps they

will be able to exploit the last minute spot beef buyers and keep the

cutouts moving higher to help cover those increased cattle costs.

So maybe we can get cash cattle up to $153-155 before

Thanksgiving, but I think that after Thanksgiving packers will have

more leeway to reduce the kill if cattle feeders want to continue to

press cash higher. As a result, I’d look for cattle prices to slowly

work lower from Thanksgiving until the end of the year. It seems to

me that there is a good chance the cutouts will be edging lower

during that period anyway. The forecast has cash cattle averaging

about $147/cwt. in the final week of the year when the Dec LC

futures expire.

I’d expect to see the Choice cutout back below $250/cwt. at the end

of the year also. This week’s fed kill came in the same as last week

at 515k. It still looks like packers are overkilling the available supply

by 5-10k per week, so while it seems they must be borrowing some

cattle from future time periods, the DTDS weights are indicating that

feedyards are slowly losing currentness. Perhaps cattle are

performing exceptionally well in the temperate fall weather and thus

are finishing ahead of schedule. That is one way to justify the

persistent over-killing. However, the fact remains that once an

animal is slaughtered, it won’t be available in a later period. So if

cattle are finishing ahead of schedule, it runs the risk of creating a

mini supply gap at some point in the future. And, if the winter

weather in cattle feeding country should turn nasty, it could be really

bullish for cash cattle prices because there isn’t a lot of slack in the

system heading into winter.

So far, the forecast for winter is relatively benign, but November is a

critical month when weather markets often get their start, so we

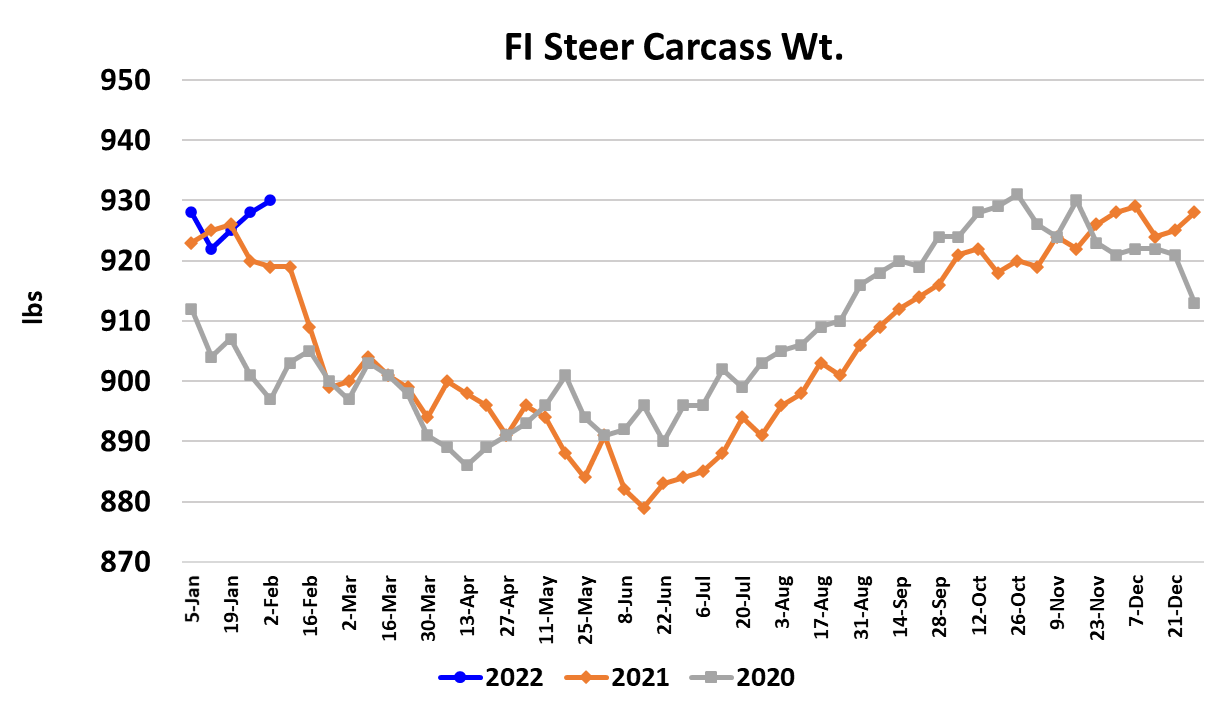

should be on alert for any changes to the forecast. Steer weights

were reported one pound higher this week at 925 pounds and that is

only 0.8% over last year and it is actually 4 pounds under 2020. So,

while the DTDS is creeping higher, it is coming up from some very

low levels and thus weights don’t seem to be a problem at present.

When we go into winter with weights a little lighter than they should

be, that makes every foul weather development just a little more

risky. Domestic beef demand seems to be a little tepid at present.

Yes, we are getting some lift in middle meat prices as we should at

this time of year, but the gains aren’t overly large and are more

concentrated in the better quality grades.

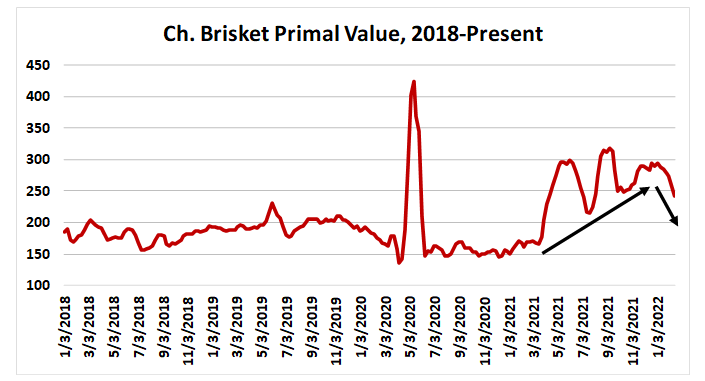

The end meats have seen some counter-seasonal price increases

over the past couple of weeks, but that now appears to be petering

out. Retailers are turning their focus to hams and turkeys ahead of

Thanksgiving and perhaps some beef middles. As a result, I don’t

think that we can count on the end meats for much more

contribution to the cutout from this point forward. Ground beef

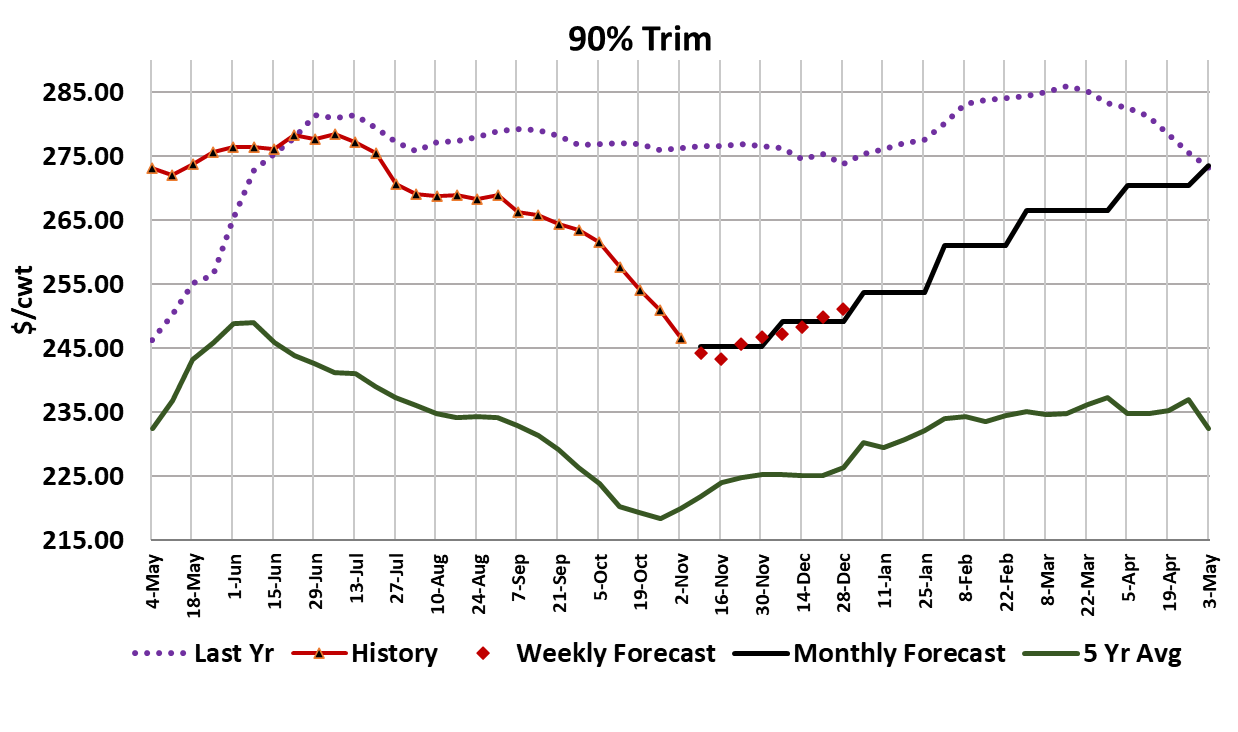

seems to be struggling also and fat trim averaged a little over $70/

cwt. this week. 90s keep tracking lower as well. So that really just

leaves the middle meats as a source of strength in the cutout over

the next few weeks. I suspect the middles will continue to move

higher, but probably not at the torrid pace we have seen in past

Novembers. International demand for US beef seems to be holding

together pretty well based on the weekly data that USDA reports.

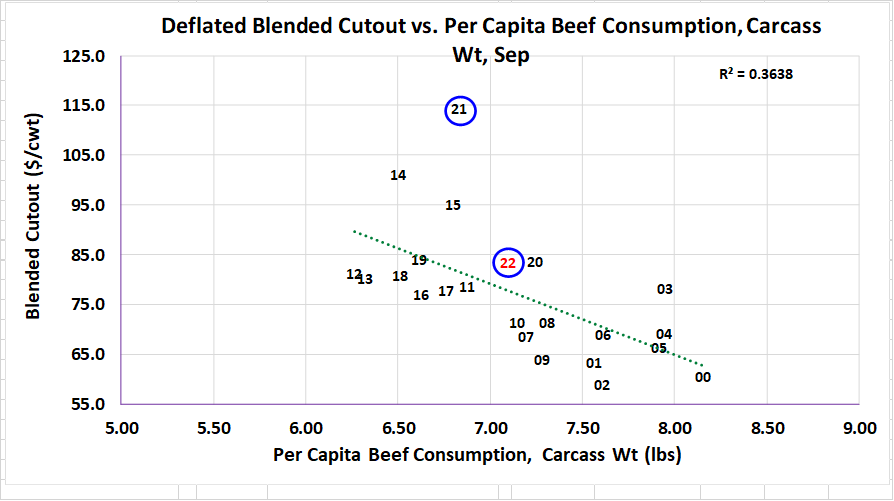

ERS gave us the official export numbers for September today and

that showed total beef exports down 4.5% from last year, so maybe

the weekly data are painting a more rosy picture than truly exists.

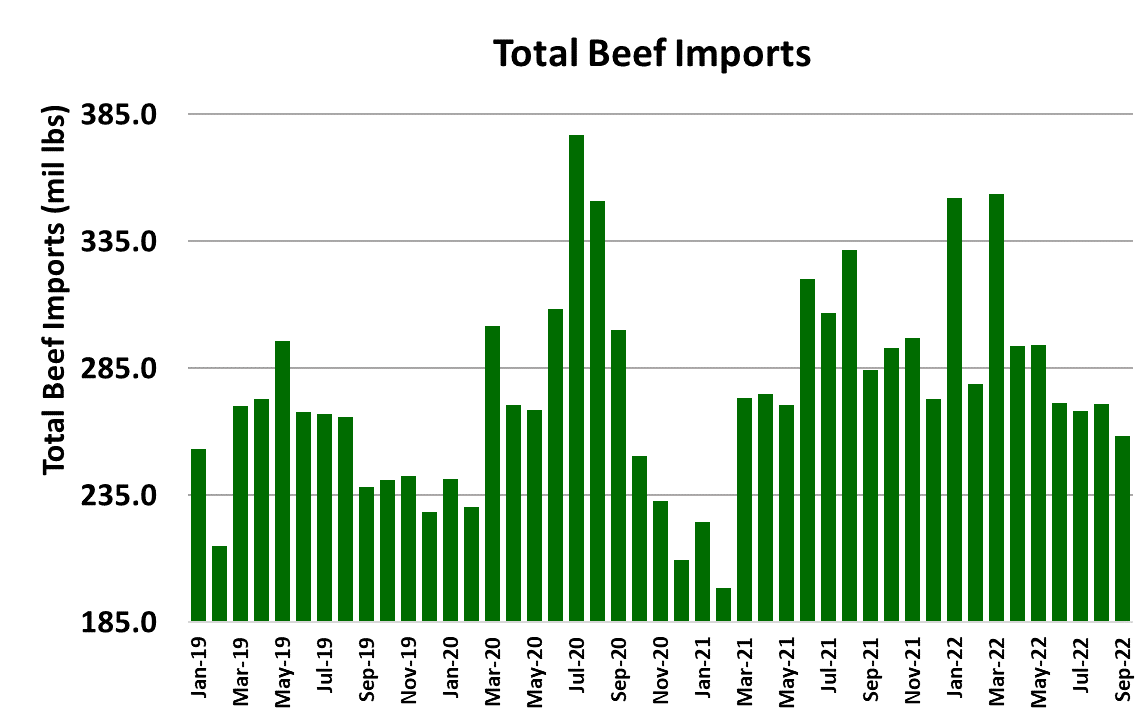

Beef imports during September were down about 5% from August

and were 9.2% below last year.

So far it doesn’t look like strength in the US dollar is benefiting beef

imports. Now that all of the trade data are in for September, we can

calculate a complete demand index and that came in at 1.046. Last

September, the demand index for the blended cutout was at 1.215.

Clearly, beef demand is running way, way below last year. The

Federal Reserve jacked interest rates up another 3/4ths of a percent

this week, adding to the risk that the economy will move into a

recession at some point down the road. I don’t hold much hope that

beef demand, either domestic or international, will strengthen much

from here. Sure, there will be seasonal ups and downs, but until the

macroeconomic storm clouds clear it is hard to see where the

demand improvement will come from. Next week, look for the

middle meats to be bigger leaders helping the cutout higher and

expect that there is a good chance cattle feeders will squeeze more

money out of packers in the cash market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}