Beef Wrap October 21

The cash cattle market surged higher this week, jumping $3/cwt. to

average just over $150. Packers were short on cattle due to having

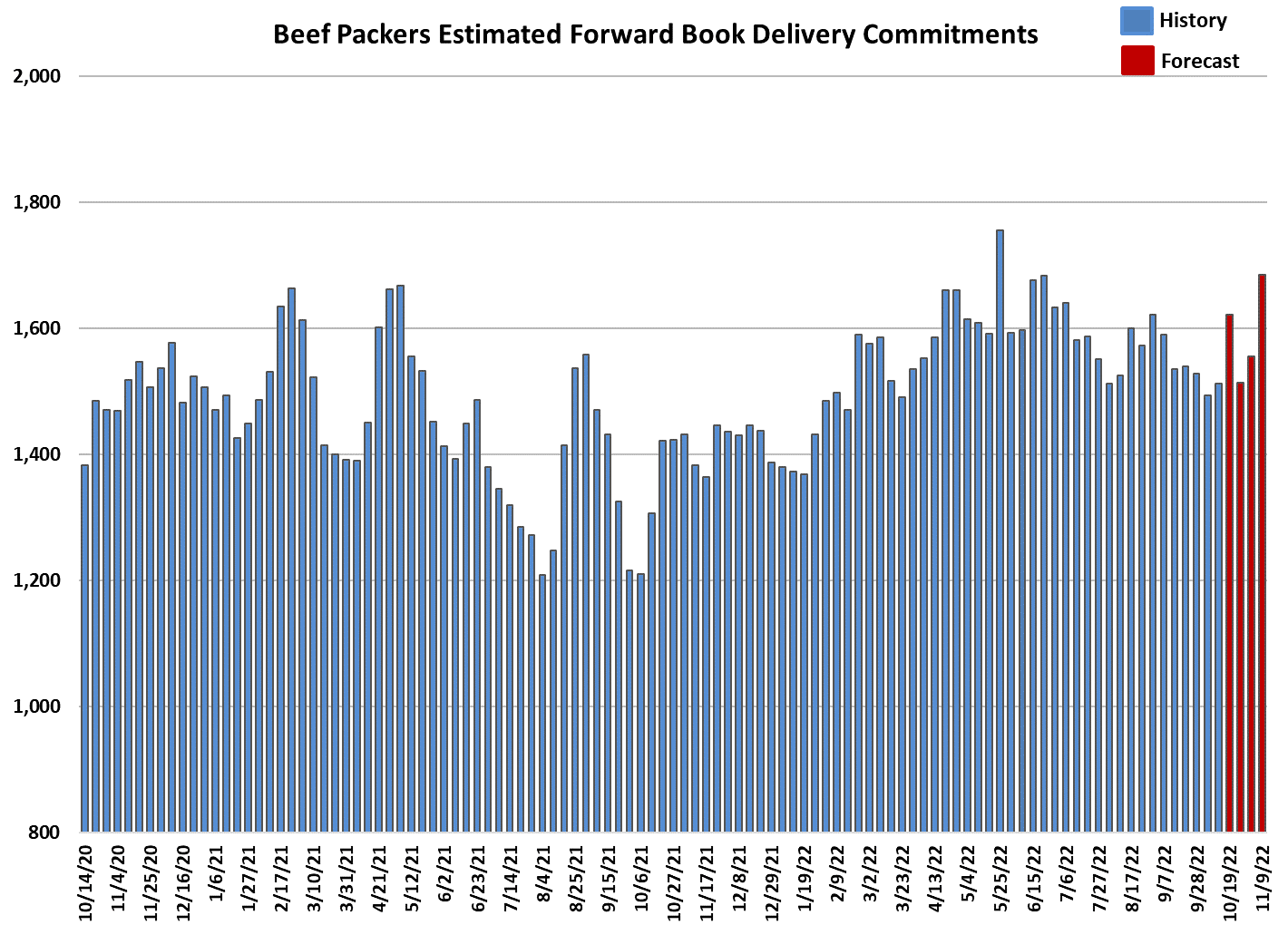

purchased a rather light volume the week before. It also looks like

they are holding a relatively big forward book that they will need to

deliver on in the next few weeks, so that probably further motivated

them to increase their purchased cattle inventory. Packers also got

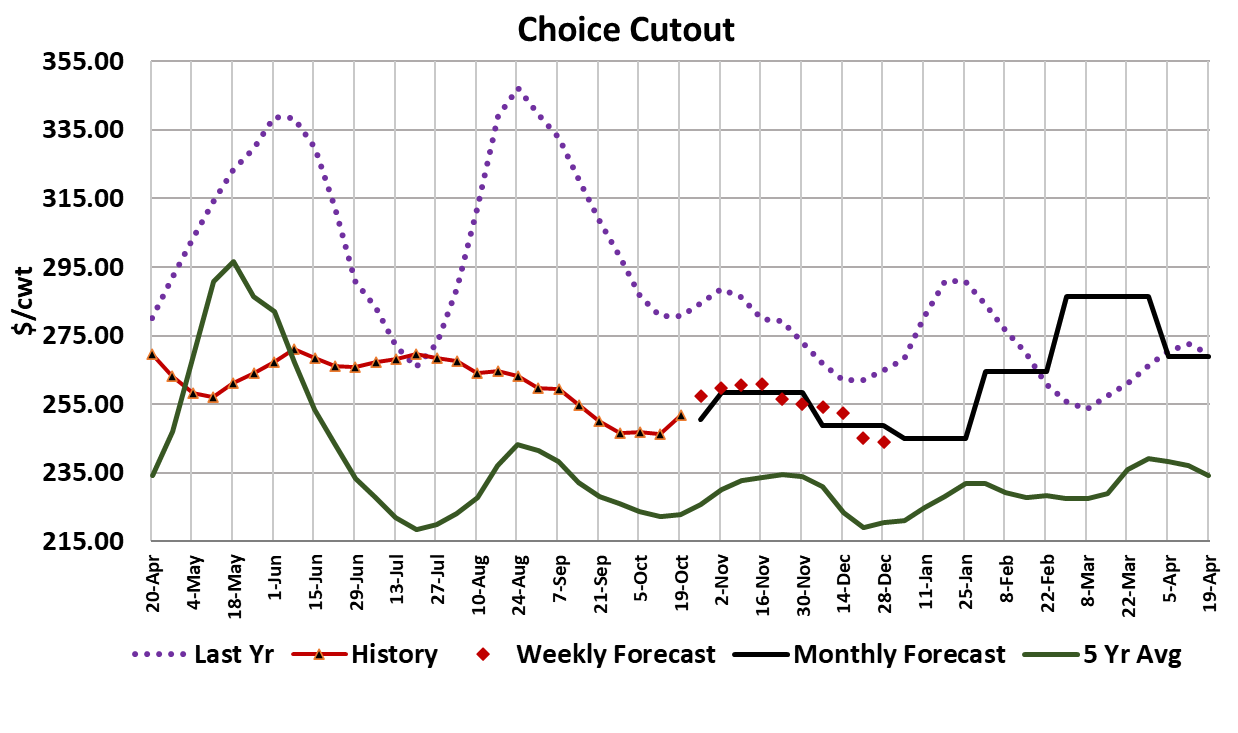

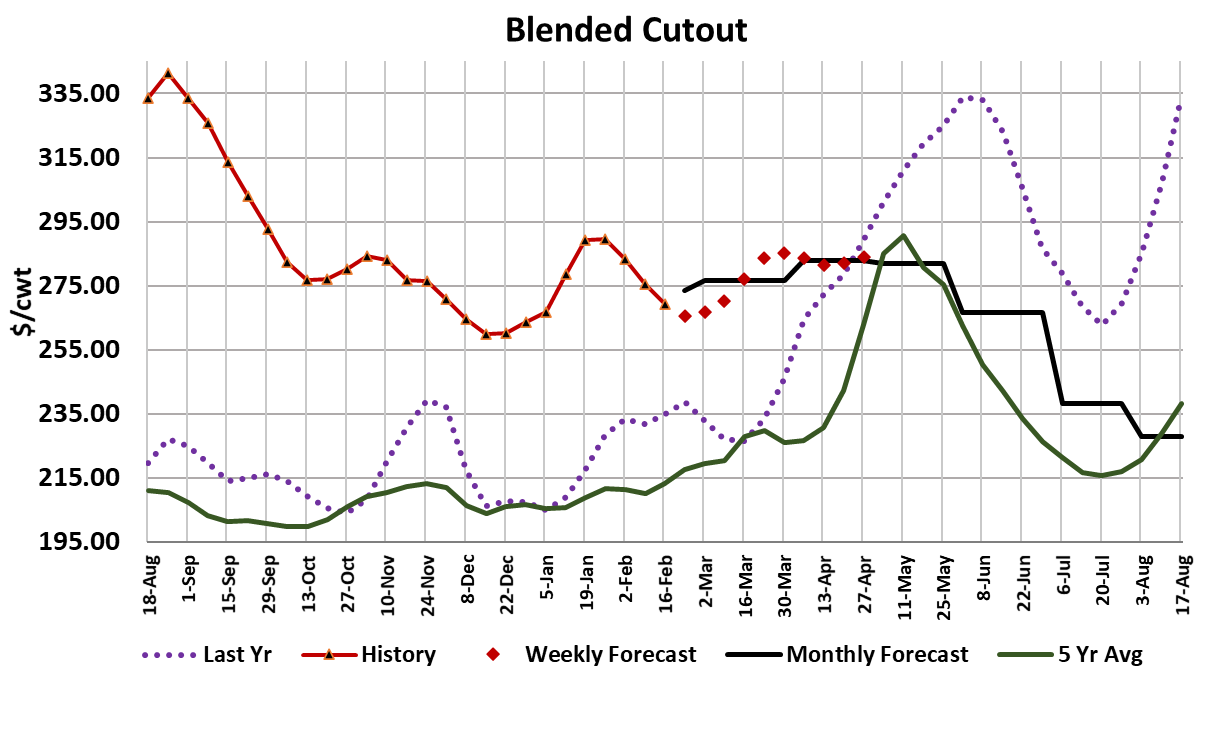

some lift out of the cutouts this week, with the Choice gaining $5.62/

cwt. and the Select adding $7.16/cwt. Interestingly, the biggest

gainer in the carcass this week was the chuck primal. That is

consistent with the normal seasonal pattern prior to the covid years

when end meats normally added value as the weather started to

cool. We also saw the Choice-Select spread remain firm, averaging

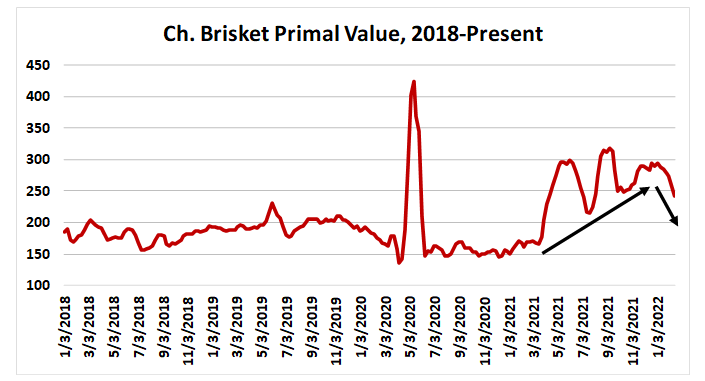

close to $30/cwt this week. The middle meats also finally started to

move higher, likely on buying in anticipation of the upcoming

holidays.

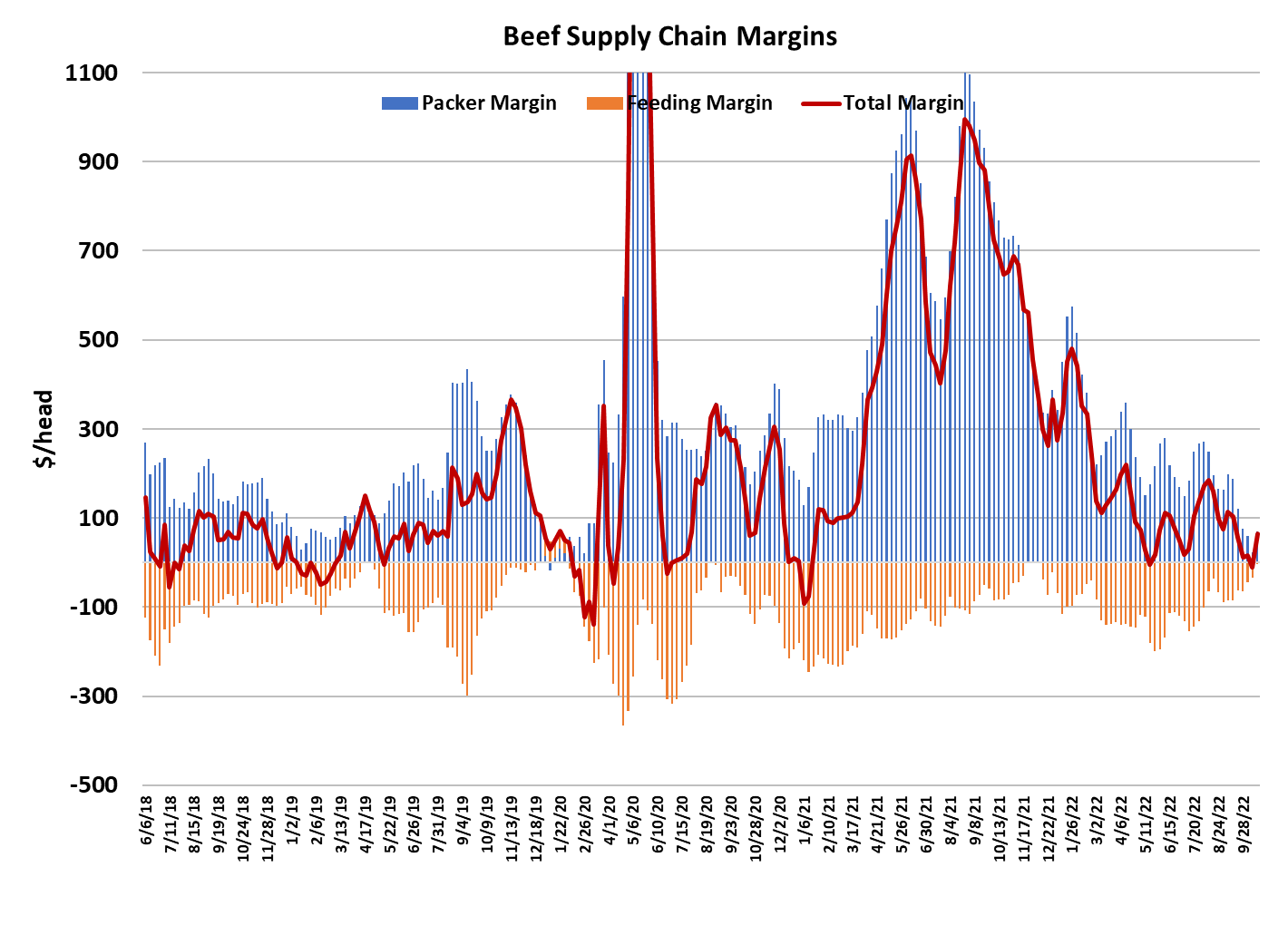

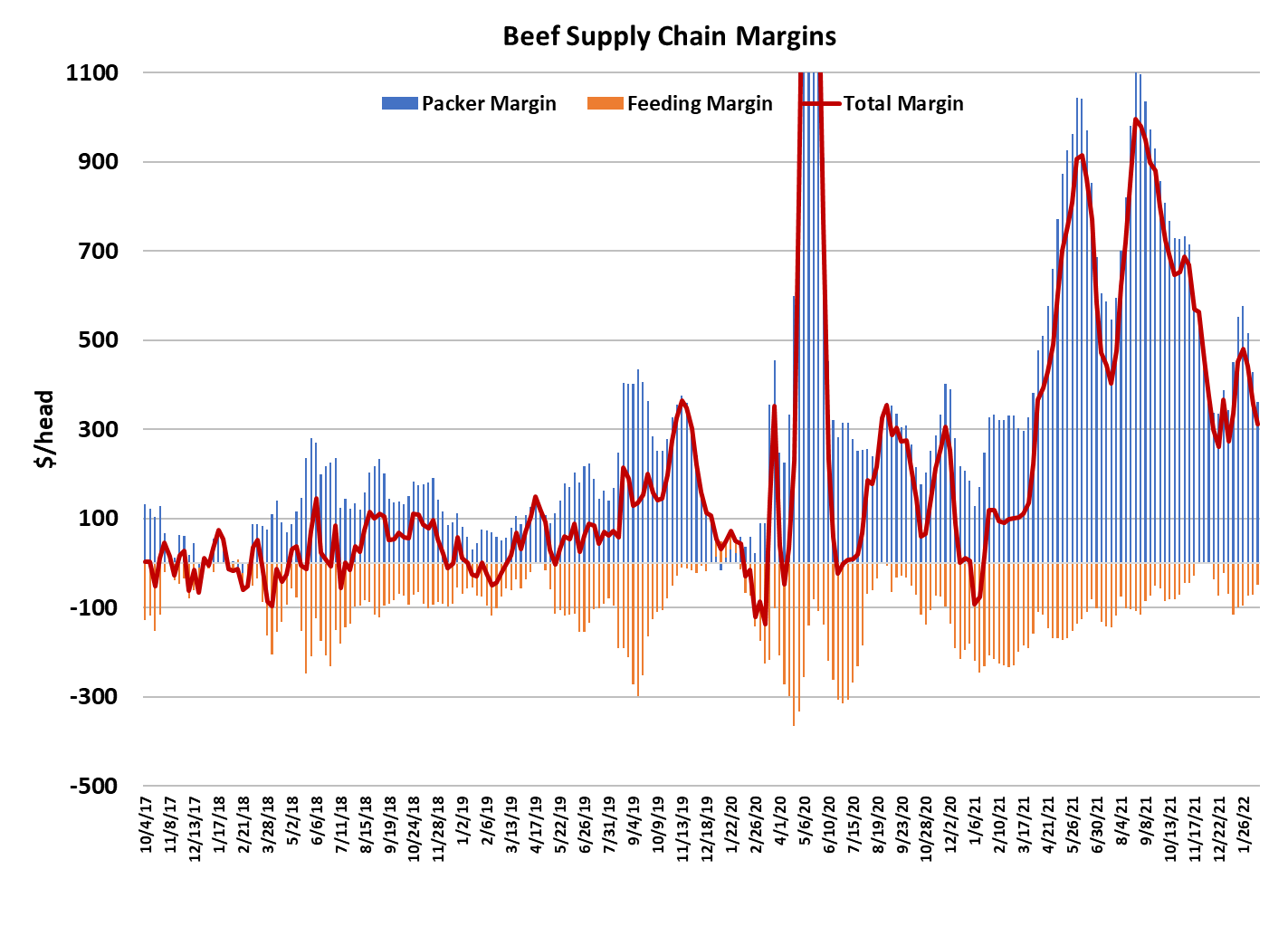

The cutout gains enabled packers to expand their margin out to $69/

head this week, up from $24 the week before. However, next week

those more expensive cattle will show up for slaughter, so packers

will need to keep beef prices moving higher in order to keep their

margin from shrinking once again. My guess is that they will be

successful in that, and the gains will be more focused on the middle

meats next week. This week’s forecast revisions now have the

Choice cutout moving just over $260, mostly on holiday rib demand,

by the middle of November and then stalling before moving lower in

December. There is some risk that the end meats will continue to

show more strength that I currently expect and that would increase

the odds that the cutout overshoots the forecast. In any case, I don’t

really look for packer margins to get much stronger than they are

right now. Cattle feeders seemed to realize that they had packers in

a bind this week and weren’t afraid to press them until they got a

strong increase in cash cattle prices.

Feedyards are still relatively current and packers seem to be

insistent on keeping the kill larger than what the cattle supply can

comfortably support, so cattle feeders have been able to retain the

upper hand. This week’s fed kill is estimated at 520k, up 8k from the

week before and about 25k more than what our flow model

suggested should be available for slaughter. That has perhaps been

the biggest mystery in the complex this fall—Why are packers

slaughtering so aggressively? It may be partly related to them

carrying a strong forward book that they need to deliver on. Some

have suggested that they are having to slaughter a lot of cattle just to

find the ones that will grade well. I think that as we move beyond the

pandemic, the market is returning back to “normal” where cattle

supplies are roughly in line with slaughter capacity and thus packers

are having to compete harder now than anytime since the Tyson

plant fire three years ago.

This could go on for several months and will likely result in small

packer margins while it is in progress. At some point however,

packers will implicitly recognize that this strategy of maintaining

market share isn’t working for anyone (except the cattle feeders)

and then we will see them slowly back off the kill more or less in

unison. It has been a long time since packers have needed to alter

slaughter levels to manage their margins, so perhaps they are a

little rusty at it. One thing that could speed the process is if beef

demand falters. At the moment, packers are being saved by the

fact that beef demand is turning seasonally higher and that gives

them some cover to pay up for cattle. Note that the combined

margin appears to have bottomed this last week and is now moving

higher. That is a sign of stronger demand.

If demand should suddenly soften, and that could easily happen

given the storm clouds in the macroeconomy, then packer margins

could quickly go red and thus add a sense of urgency to correcting

their over-killing ways. Cattle feeders, for their part, really need

packers to keep pulling hard on the cattle supply because weights

are still trending higher and cattle are performing well. If the

packers’ demand for cattle softens once they get their booked

orders filled then that creates a risk feedyard currentness will fall

rapidly. Today’s Cattle on Feed report put September feedyard

placements down 3.8% and was right in line with the pre-report

estimate, so it should have very little impact on the futures next

week. Still, on-feed inventories are only 1% smaller than last year,

so it isn’t like we are running out of cattle and cattle feeders would

be wise not to expect cash cattle prices to keep going up week after

week. In fact, cattle prices are likely to take a bit of a breather next

week after this week’s sharp increase.

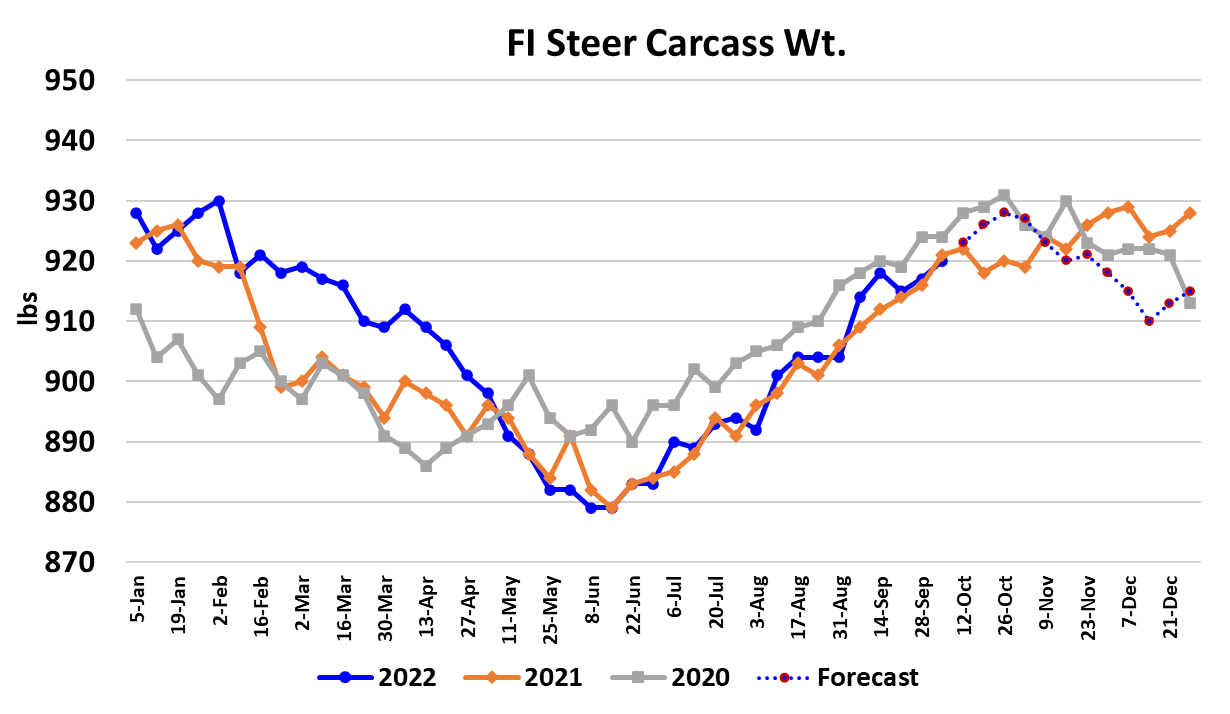

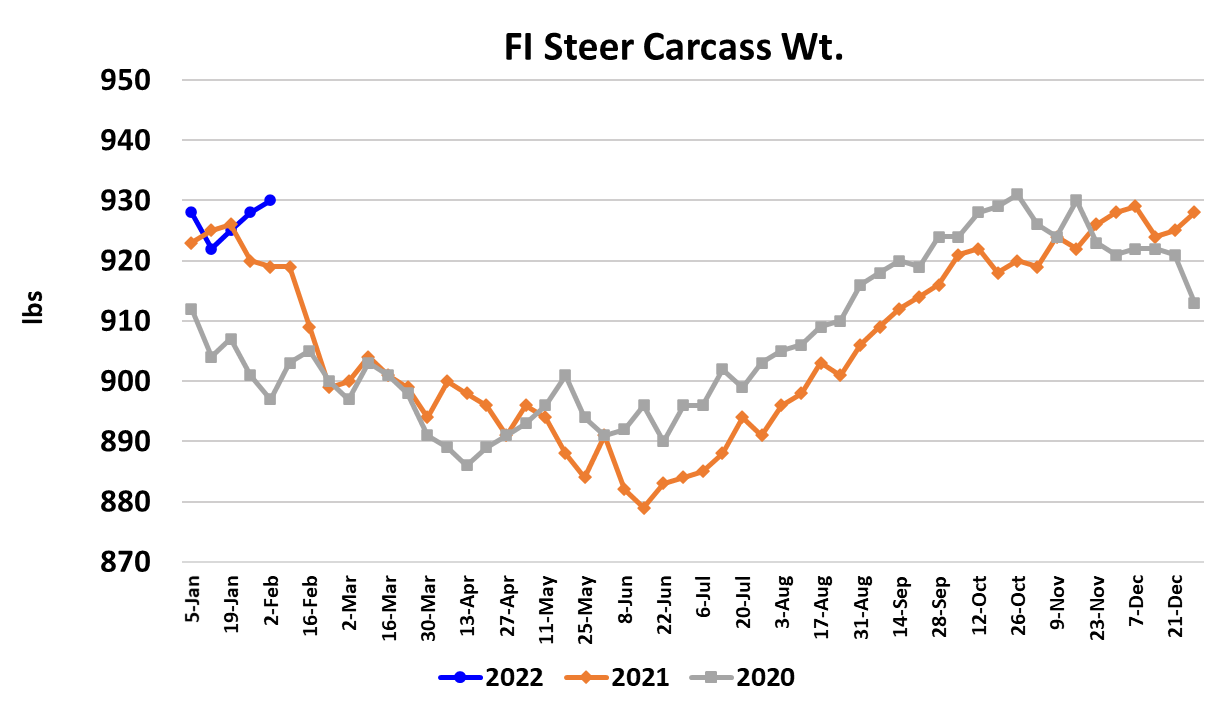

Steer weights increased 3 pounds this week and still probably have

another 6-7 pounds to go before they reach the seasonal top. The

DTDS weights are still pointing to relatively current feedyards. The

weekly export data continues to look encouraging and is not yet

showing any serious problems in international beef demand that

might arise at some point due to a very strong US dollar and

deteriorating economic conditions in the destination countries.

Next week, look for more cutout gains, with the middle meats

moving into the driver’s seat. Cash cattle might gain a little more

also, but not like they did this week. Without a red hot cash market,

futures could retrace some of the strong rally from this week. They

would all be better off if they all slowed down they kill in unison, but

at this early stage in the process they are keen on maintaining their

market share and all are hoping that their competitor will reduce

their slaughter level so that they don’t have to.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}