Beef Wrap October 27

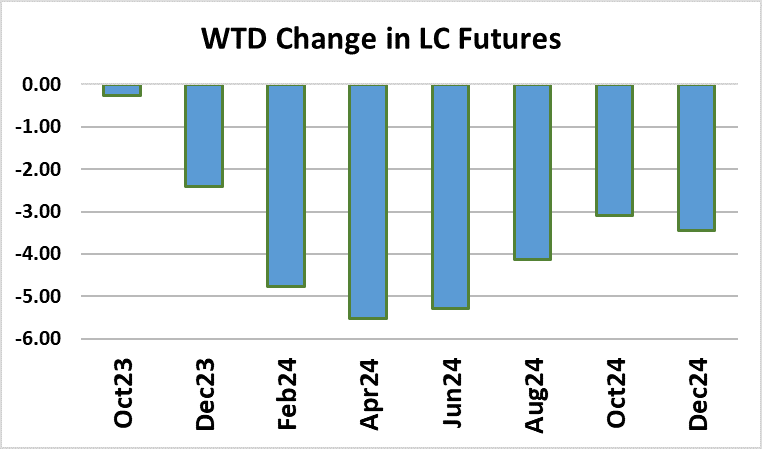

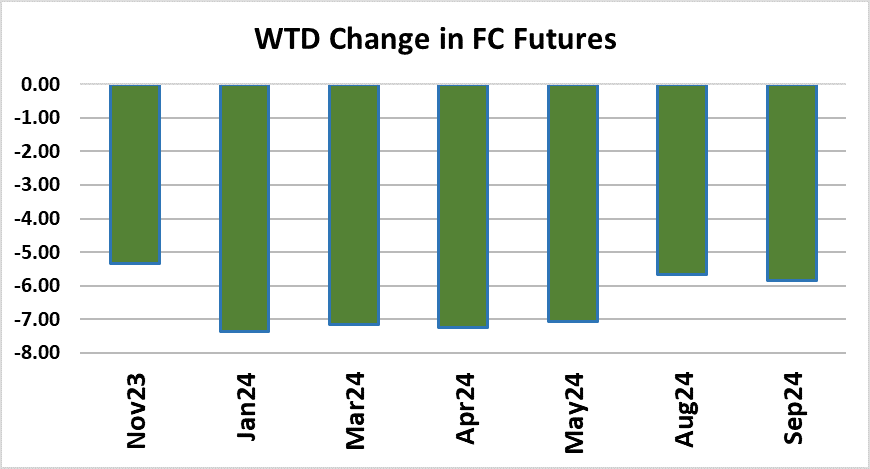

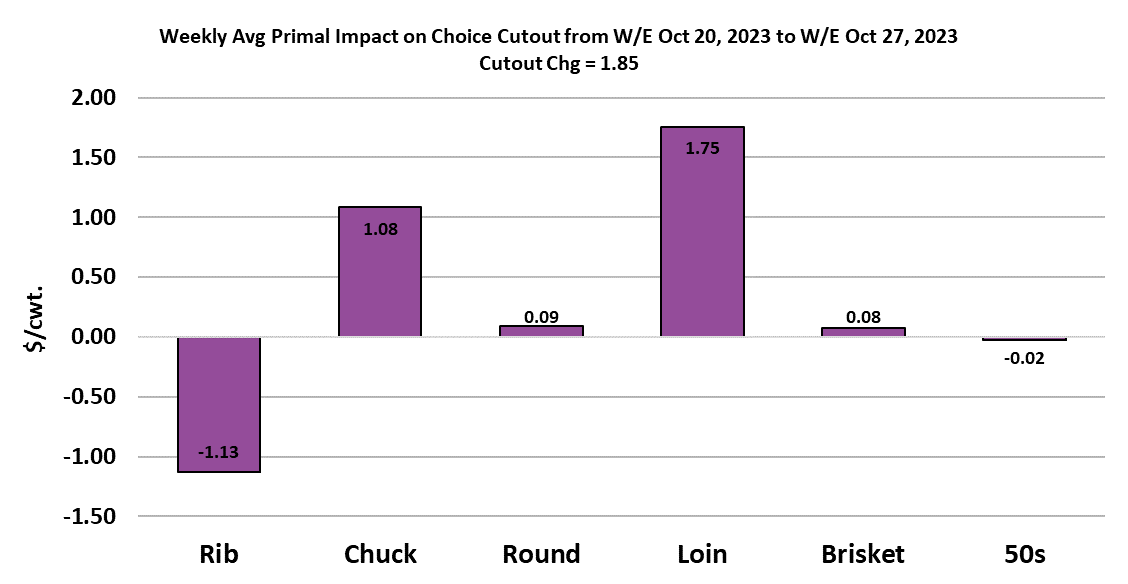

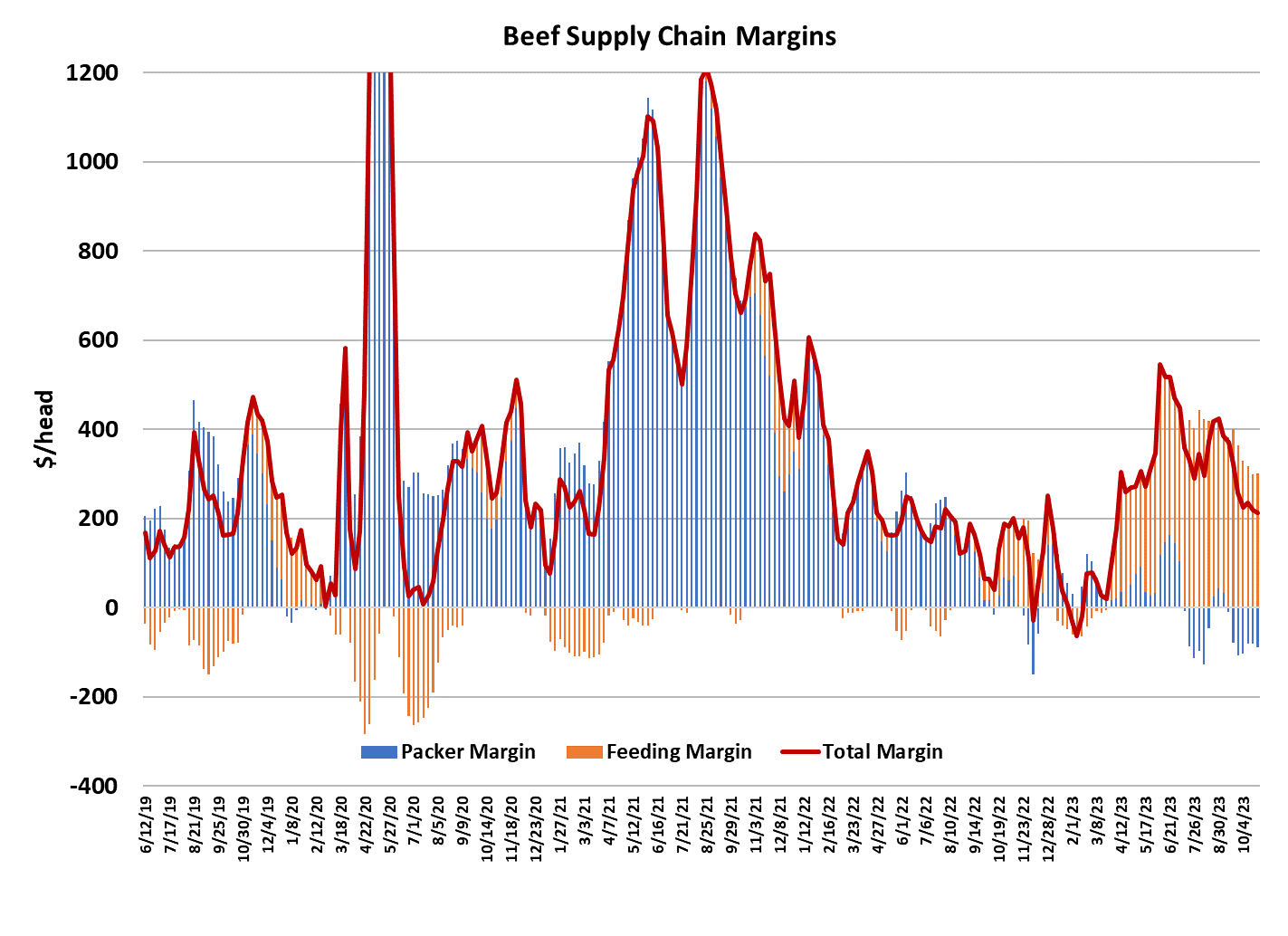

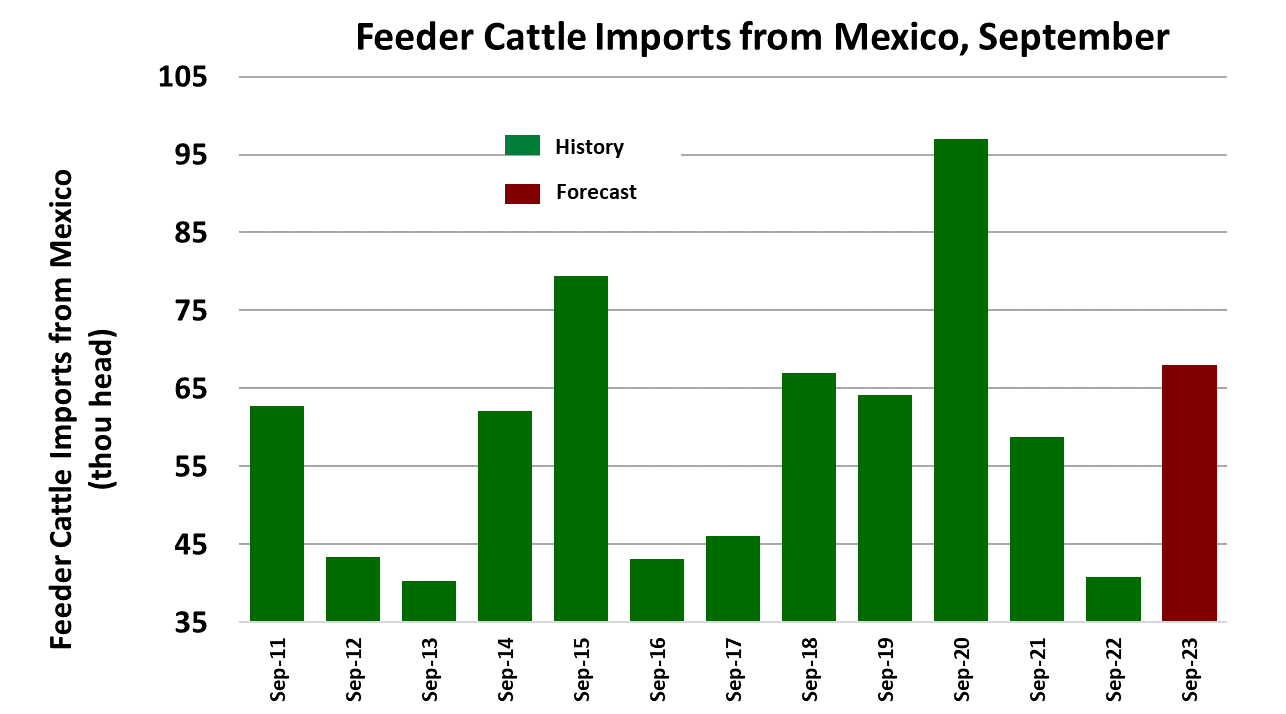

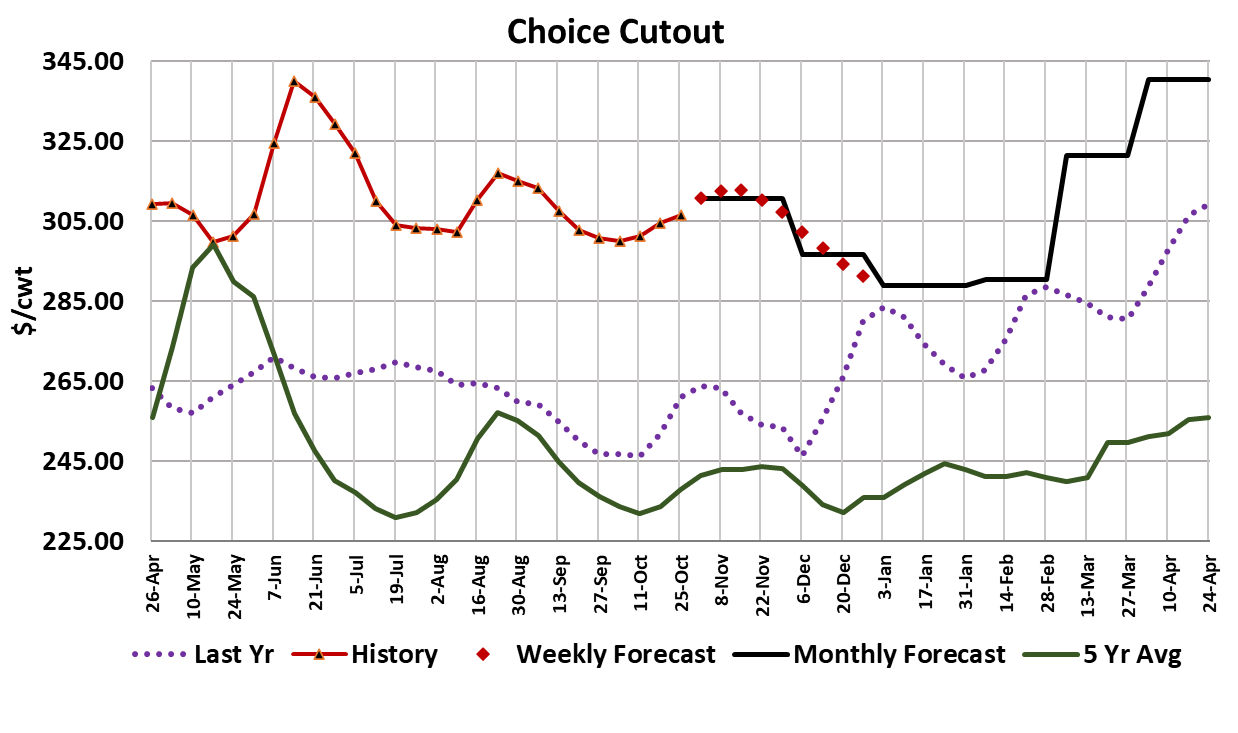

This week was highlighted by a massive selloff in cattle futures. On Monday, the Dec LC contract fell below its 100-day moving average and that triggered a wave of selling that took most of the curve down $5-6/cwt. The initial impetus for the selling was the previous Friday’s Cattle on Feed report which showed September placements much larger than expected. In most situations, that would have been worth a dollar or two decline in the affected contracts, but the breakdown of important technical levels fueled a massive amount of volume, much of it likely coming from computer programs. The soon-to-expire Oct contract settled on Monday at $178.25, which was particularly notable since the cash cattle market had averaged over $186 the week before. Clearly, the selling was overdone and the market spent the remaining four days of the week correcting that problem. By the finish of trading today, the Oct contract was back at $184, which was only a few cents below where it was before the COF report was released. The front of the curve had to rebound sharply because of the impending contract expiration, but the more deferred issues didn’t have to obey that constraint and many of the 2024 contracts lost $4-5 on the week. Feeder cattle futures also got slammed in the process and several of those contracts were down over $7 Friday-to-Friday. The cattle market has been trending higher for so long that it is easy to see why some traders panicked, thinking that this was the top in the market. I see it as more of a healthy correction in an otherwise uptrending market and don’t think we are anywhere near the cyclical price top. Some cattle feeders also panicked and sold cash cattle lower early in the week, but others held firm and were rewarded on Friday, when packers paid $185 for cash cattle in the southern region. My best guess at the average for the week is $184.60, which would be about $1.50 below the previous week’s average. The cutouts advanced a little this week, with the Choice up $1.85 on a weekly average basis and the Select gaining $3.23. Packer margins were similar to the week before at -$89/head, but that could improve to -$30/head next week as the cheaper cash cattle show up for slaughter. However, the higher late-week cash trade is a reminder to packers that the leverage meter is still favoring cattle feeders and, absent another futures market implosion, they may struggle to get cattle bought cheaper next week. This week’s fed kill came in close to 490k, down about 10k from the week before. That is probably not enough of a reduction in slaughter to improve the packer’s leverage materially however. Instead, packer margins are likely to benefit from some seasonal improvement in demand, but it may not come from the usual sources. Middle meats were mixed this week, with the rib primal moving lower and the loin primal moving higher. The real surprise has been how well end meat demand is holding up. The fundamental forecast didn’t change much this week and I still expect the Choice cutout to hold in the low $300s for the next few weeks before drifting lower in December. Beef demand continues to be strong and seasonally, demand should only improve in November. In the recent past, I’ve noted a lot of potential headwinds in the macroeconomy that could crimp beef demand, but so far the economy continues to hum along. GDP in the third quarter was estimated to be up nearly 5% YOY and consumer spending remains strong. So maybe beef demand will hold up better than expected as we close out 2023. On the supply side, there was a lot of focus on the surprise increase in September feedyard placements, but while that will result in larger near-term production, it portends smaller longer-term production since cattle placed now won’t be available to place in the future. We still haven’t seen any evidence of herd rebuilding in the data and it seems like this cattle cycle may see a very long liquidation phase that takes the herd down a lot more than what might be considered typical in recent cattle cycles. Erratic weather is a huge obstacle to expansion since it seems that drought conditions are cropping up more frequently than they used to in various parts of the country and producers are unlikely to consider expanding as long as they perceive a substantial weather risk environment. This week’s beef export data looked soft once again and that is likely to remain the case for a long time to come. At the same time, high US beef prices are likely to draw more imports. It seems that at least some of the increased placements in September resulted from strong imports of feeder cattle from Mexico. That too is likely to continue. Next week, look for some further modest gains in the cutouts and a cash cattle market that is probably no worse than steady. There is still time for a surge in holiday middle meat interest to take the cutouts substantially higher, so keep an eye on those ribs and tenders.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}