Beef Wrap November 03

Cash

cattle trade was slow to develop this week and as of press time, packers and

feeders in the Southern Plains remained in a standoff. Some light trade

did occur in the North, with reported prices at mostly $185, which was steady

with the week before. It was widely expected that cash trade in the South

would be higher than last week’s $185, but packers, who were dealing with a

stagnant boxed beef market, have so far refused to cooperate. Late

Friday, packers were bidding a steady $185 in the South, but cattle feeders

wanted more. It seems as though packers need the cattle more than cattle

feeders need to sell them, so a higher cash trade may yet develop over the

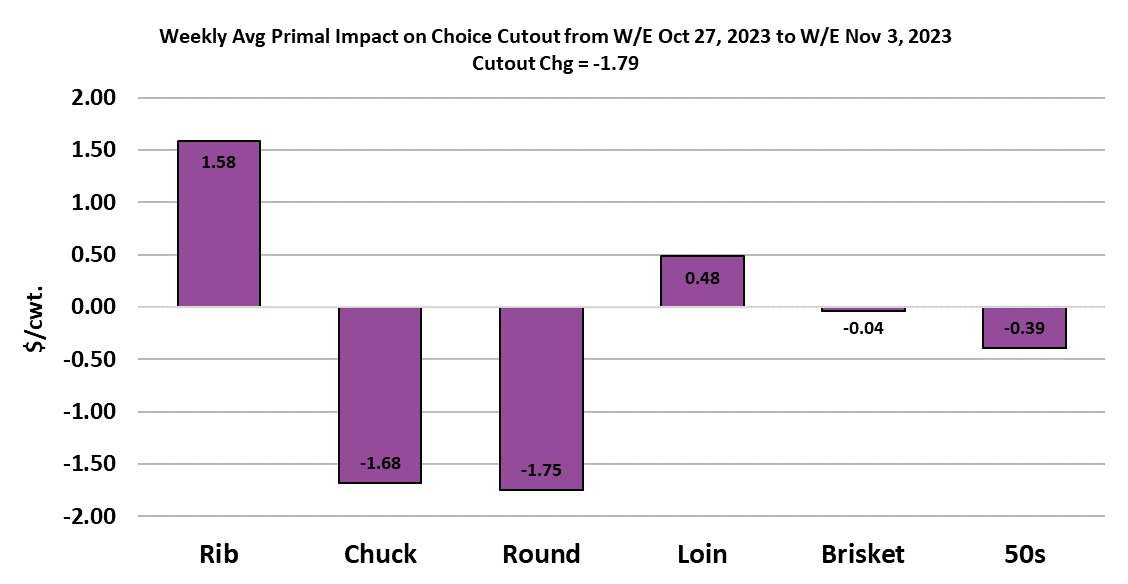

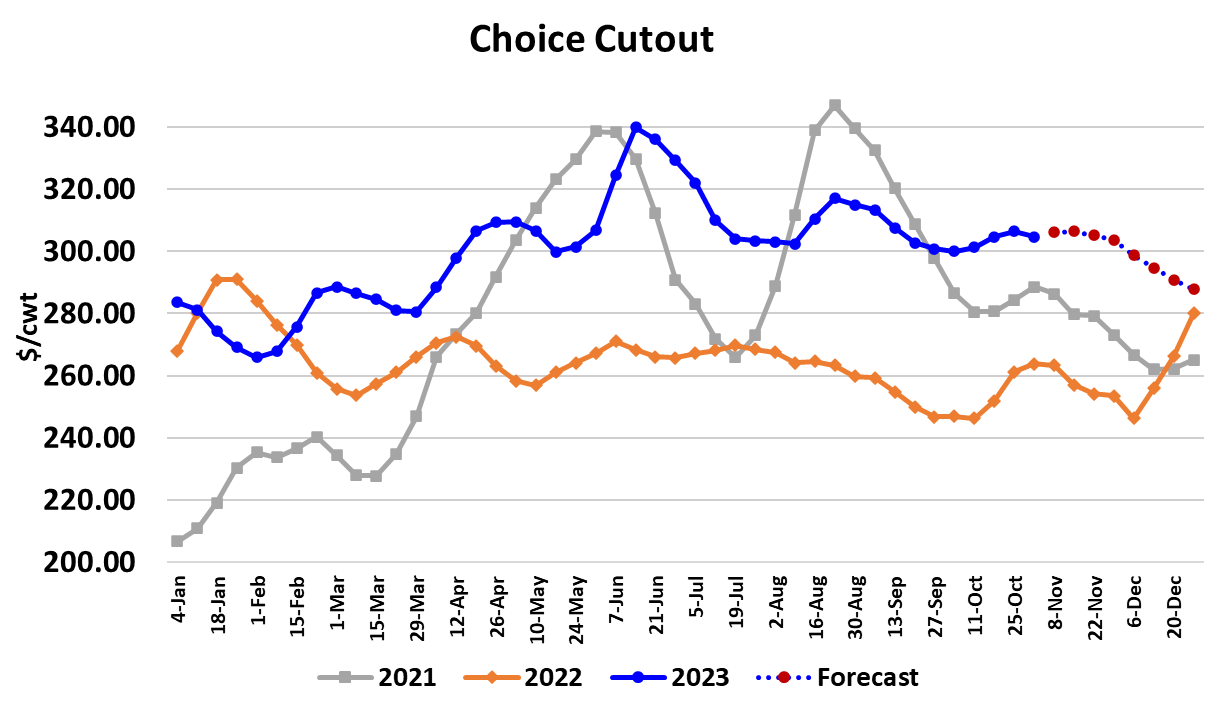

weekend or early next week. In the beef market, the Choice cutout was

down $1.79/cwt. on a weekly average basis to $304.70 and the Select cutout

dropped $4.24/cwt. to average $277.06/cwt. It was the chucks and rounds

that pulled the cutout lower this week, while the middle primals were a little

higher. Fat trim also softened and was quoted near $63/cwt. on

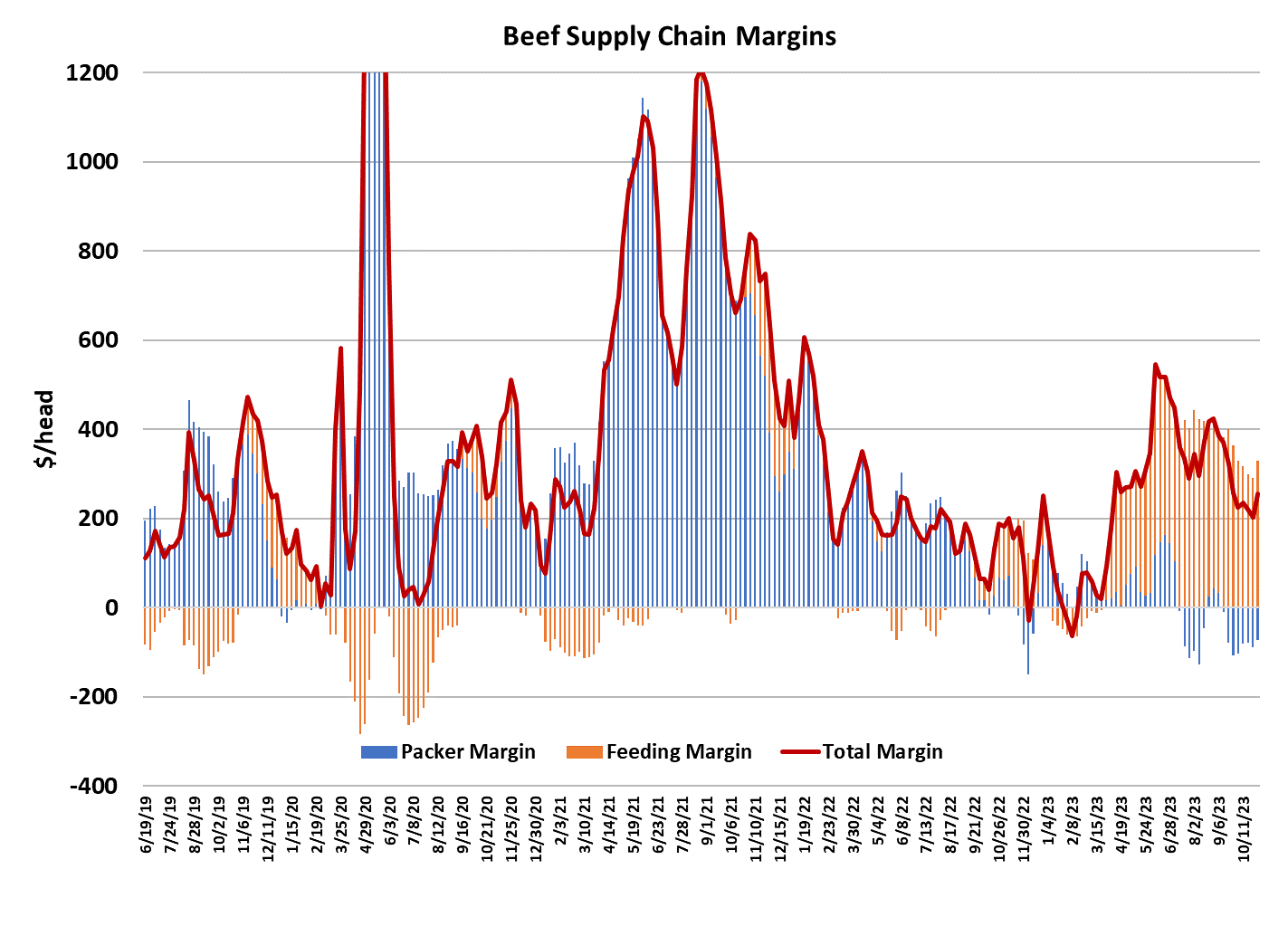

Friday. Packer margins improved slightly this week, averaging close to

-$73/head, but that marked the eighth week in a row of negative margins for

packers and there seems to be no end in sight to their margin problems.

Packers are likely to continue to bleed red ink until the supply of

market-ready cattle expands and better aligns with packing capacity. That

might not happen until January, and by then packers could be dealing with

seasonally soft demand that tempers margins from the revenue side of the

equation. So, the outlook doesn’t look good for packers. They

haven’t been able to scale back the kill enough to make a difference in

market-ready cattle supplies. This week’s fed kill came in close to 485k,

down 6k from the week before. The problem for packers is that soon they

will need to begin delivering on holiday orders and that will force them to

kill more than they might want to. One sign that the margin bleeding has

packers concerned is their reluctance to buy any cattle this week in the South

because they were priced higher than last week. In previous weeks, the

packers just paid up, but this week they dug in and refused to do business.

The strategy of refusing to purchase cattle is unlikely to work for them

because they will need additional cattle within a few days, but it would take

at least a couple of weeks before cattle feeders would likely feel a need to

get cattle sold quickly. My guess is that trade will eventually

occur in the South at $186 or better. Steer carcass weights were reported

unchanged this week and that was somewhat of a surprise. Weights should

still have another 2-4 weeks to increase before they make their seasonal

top. The DTDS weights are still relatively low and that is a good

indicator that packers are not in a bind to sell cattle right away. One

piece of good news for the industry is that the combined margin appears to be

turning higher after being on the defensive since early September.

Perhaps that is giving us advance warning that demand is starting to pick up

and the timing would be appropriate given that the holidays are just around the

corner. It is easy to believe that middle meat demand will pick up in the

next few weeks, but I’m not so sure about demand for the end cuts. On the

supply side, it does appear that placements during October ran above last year,

maybe by as much as 5%. Given that September placements were up 6% YOY,

the Sep/Oct placements have the potential to create a bulge in Q1 fed cattle

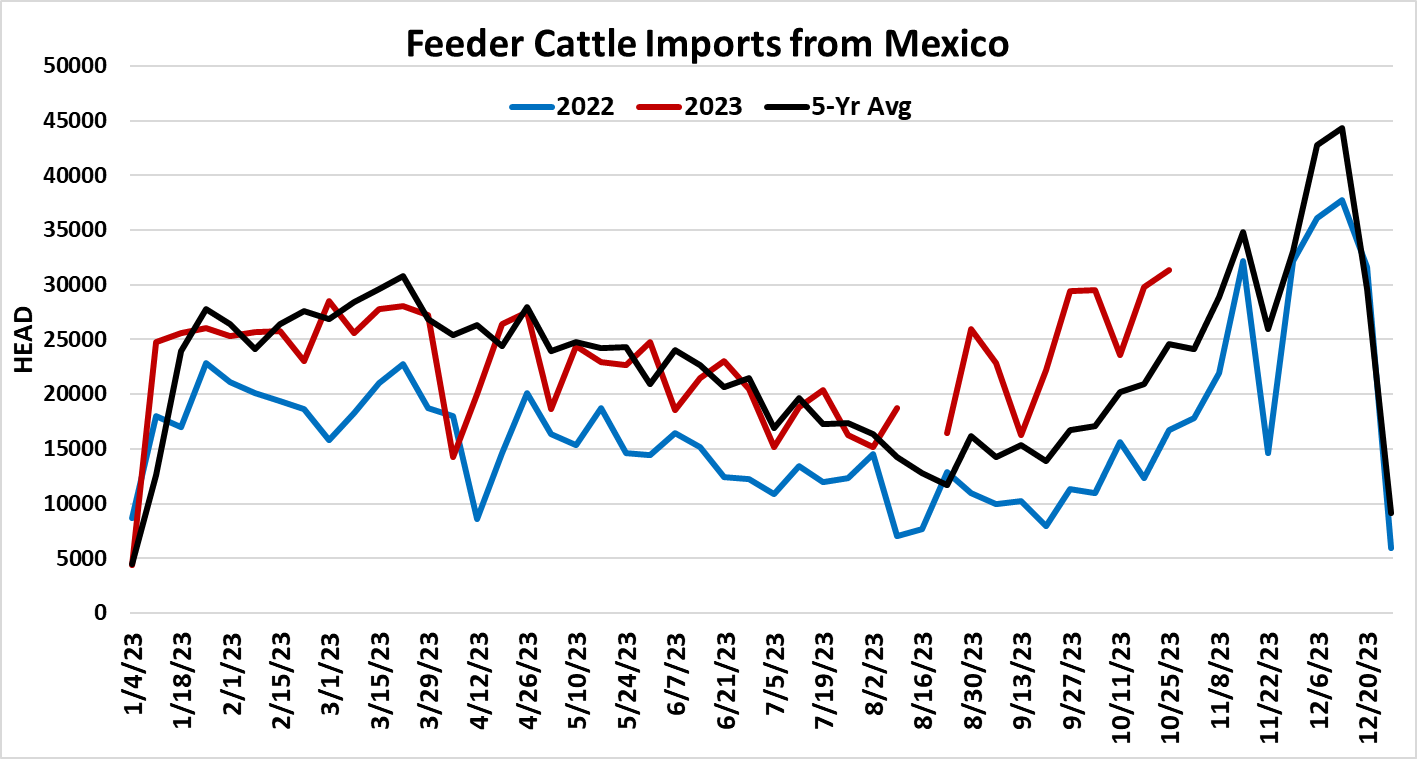

supplies. Feeder cattle imports from Mexico have been above last year

since January, but they have really ramped up since the end of summer (chart

attached). That is evidence of cattle feeders in the Southern region

seeking out cheaper alternatives to sky-high domestic feeder cattle

prices. However, those Mexican cattle are a lot less likely to make grade

than domestic-sourced animals and so won’t help to address the one area of the

market where it appears that demand is resilient—high quality middle

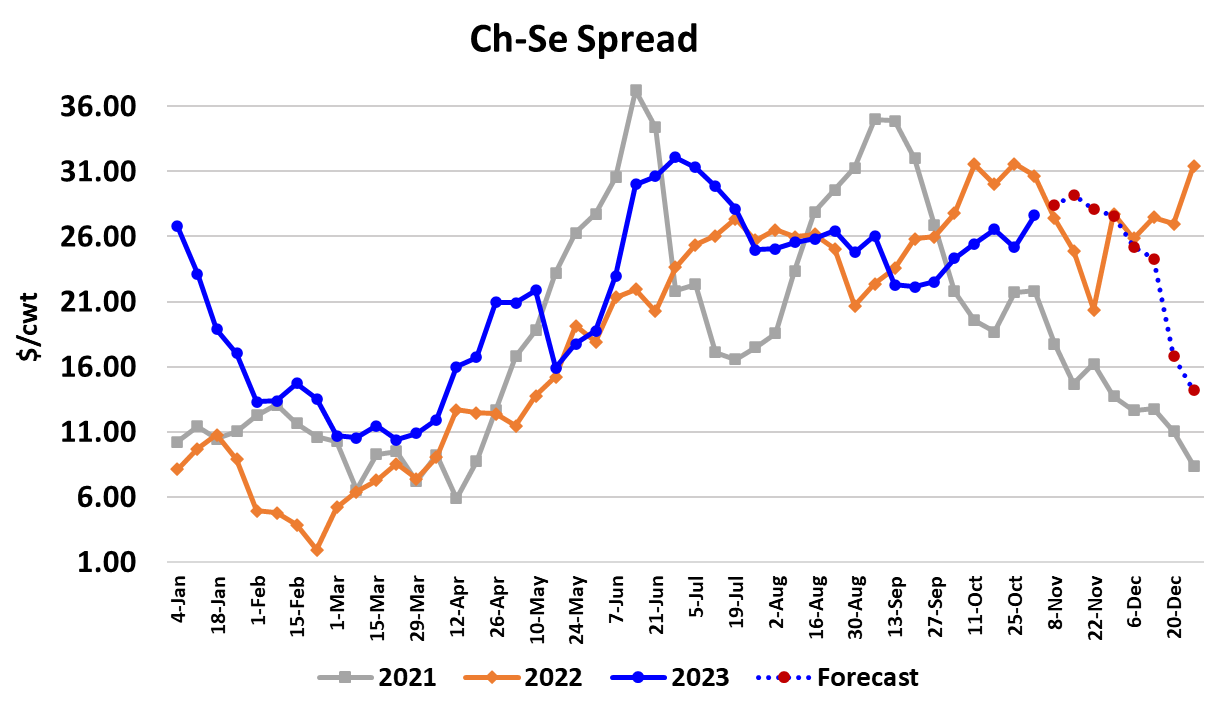

meats. This week we saw the Choice-Select spread widen to over $30/cwt.,

a sign that demand for better-quality beef is holding up well. The bubble

in placements this fall could temper cattle prices next spring, but as I’ve

pointed out before, cattle that are placed today can’t be placed in the future

and so at some point we are likely to see sharp YOY declines in placements

reappear. Next week, watch for some early week trade in the South at

higher money to keep packers’ plants running and then a standoff until Friday

when the whole process could repeat. The Choice cutout should continue to

hold in the low $300s as holiday-driven gains in the middles are offset by soft

pricing in the end meat segment.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}