Beef Wrap October 20

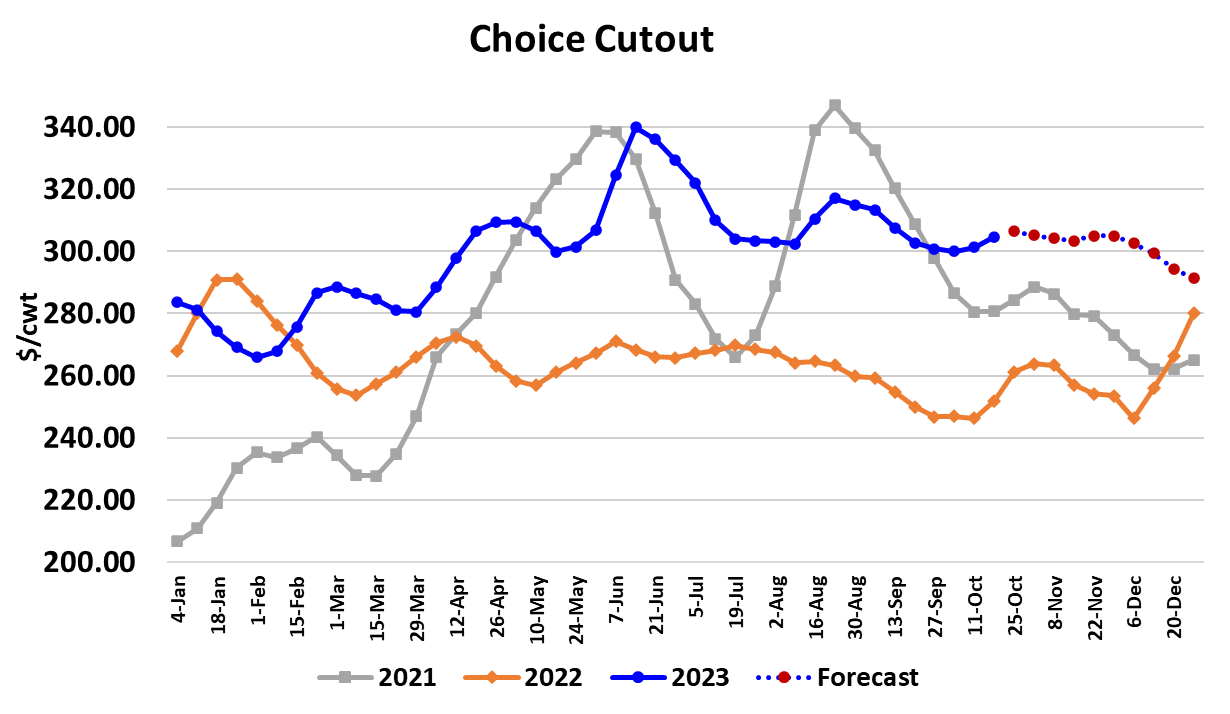

Packers did manage to achieve

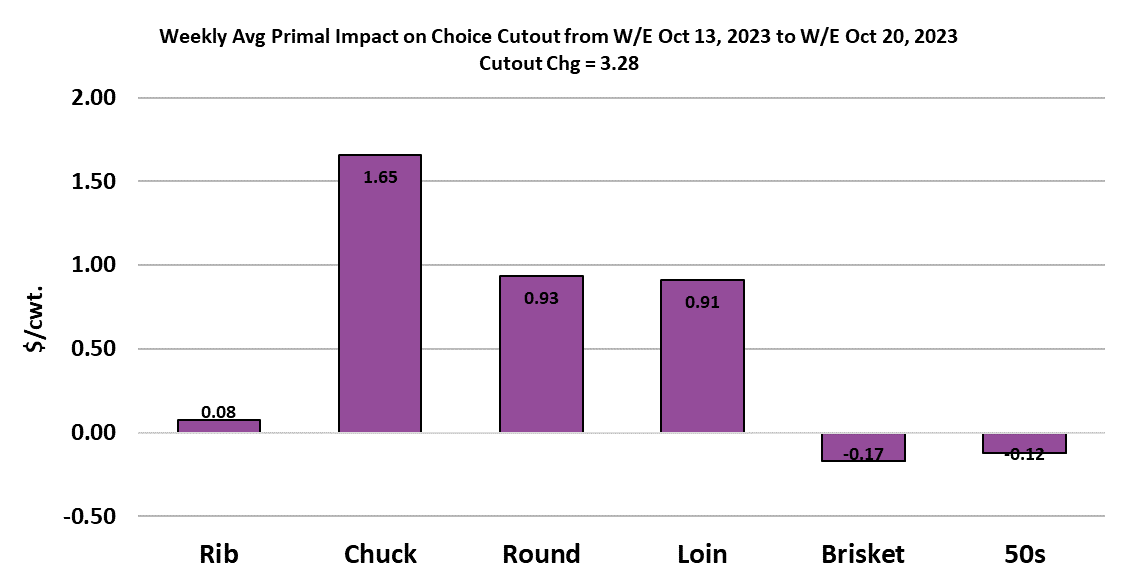

modest increases in the cutout this week with the Choice gaining $3.28/cwt. on

a weekly average basis and the Select adding $2.18/cwt. Unfortunately for

packers, that probably won’t help their bottom line much because they ended up

pay more for cash cattle once again. In the Southern Plains, cash trade

was mostly in the $184-185 range, up $1-2 from last week. In the North,

cattle changed hands at $186-187, also $1-2 higher. When all of the data

is in on Monday, I’d expect the average for the week to be just a little north

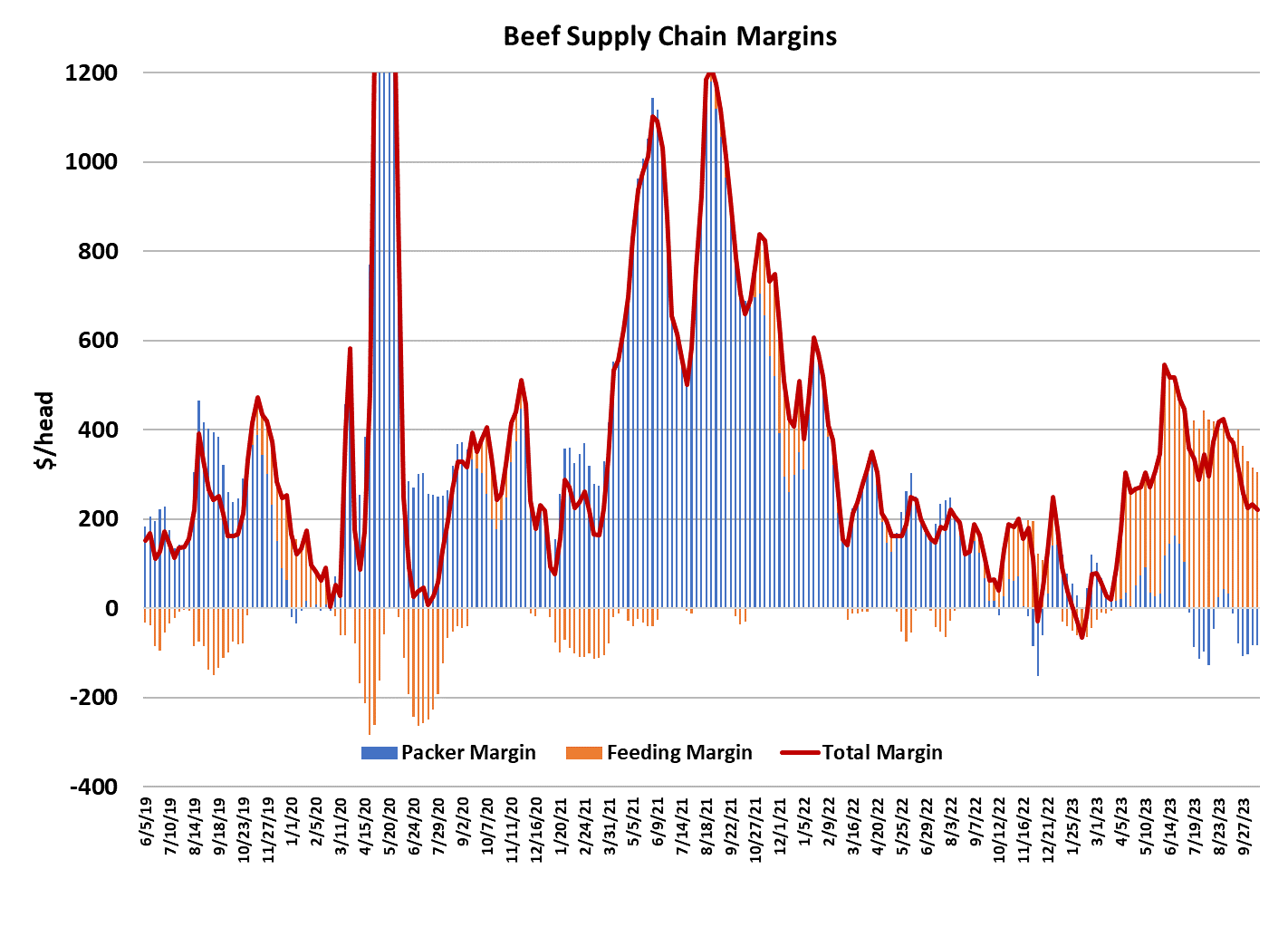

of $185. Packer margins clocked in at -$82/head, very similar to the week

before. When this week’s more expensive cattle show up for

slaughter next week, we could see margins move to -$100/head unless packers are

able to get some meaningful increases in beef prices. Surprisingly,

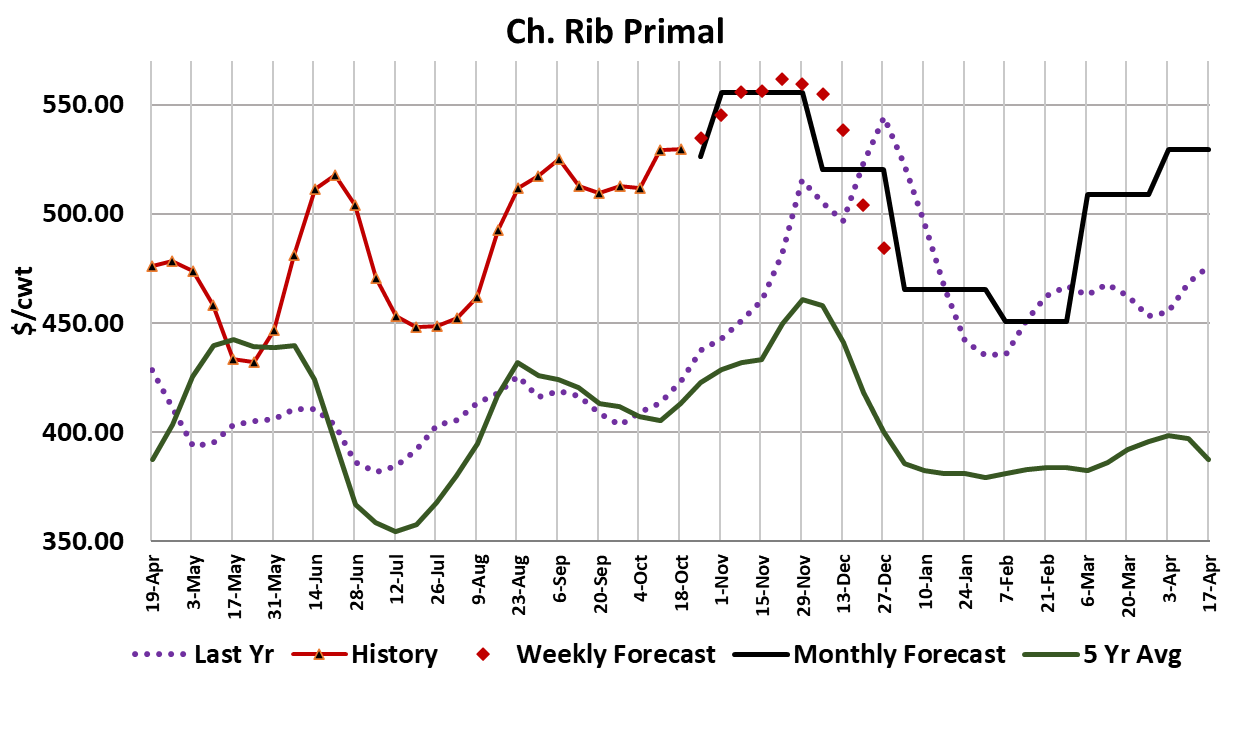

the biggest contributor to this week’s gains in the cutout was the chuck

primal. Ribs had almost no impact on the cutout, but the loin primal

did. Even so, it seems as though the cutouts have struggled just to add a

few dollars. I’ve been scaling back the price forecasts for the rib and

loin primal since it appears that they are not going to live up to expectations

this fall. The forecast still has the Choice cutout holding in the low

$300s through November and then moving lower as the holiday business dries

up. One of the reasons that the cutouts haven’t moved much higher this

fall is because packers can’t seem to keep the kill contained at low enough levels

to tighten up beef supplies and thus create supply concerns among beef

buyers. This week’s fed kill registered 498k, up 8k from the week before

and 24k higher than it was in the last week of September. Packers

remember how hard it was to find qualified workers during the pandemic and with

the unemployment rate still very low at 3.8%, they might be reluctant to run

fewer hours and risk losing employees. Many of the union contracts

contain a clause for how many 32-hour weeks a packer can run per year and they

may be out of ammunition on that one too as the year draws to a close.

Thus kills remain larger than they “should” and packer margins remain in the

red. The ultimate solution to this margin problem is for one or more

packers to close a large harvest facility, but we are still probably a long way

off from that. In the interim, packers likely will continue to lose money

as they all secretly hope that the other guy will close a plant first.

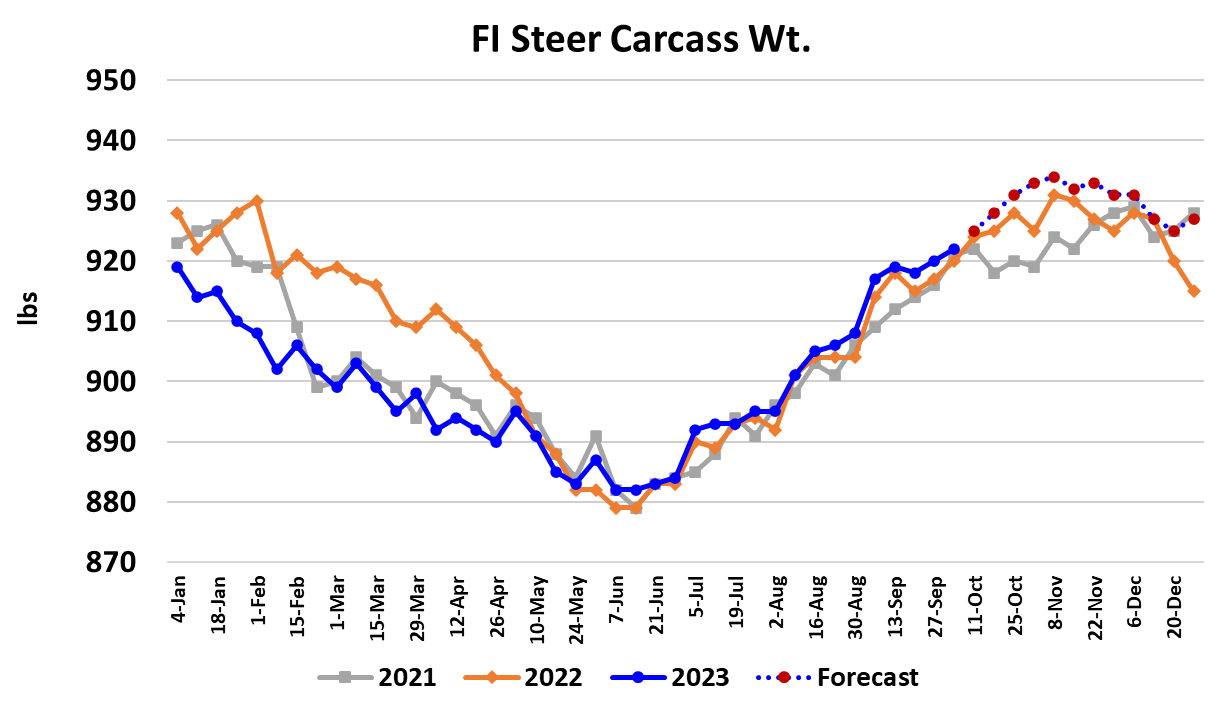

Steer carcass weights were reported 2 pounds higher this week and seem to be

following the normal seasonal pattern that would have weights topping sometime

in late November or early December. Fed beef production was down 18.3%

from last year, but that is mostly due to smaller kills, not any problem with

carcass weights. Export volumes continue to look soft in the weekly

data. USDA provided the results of their Cattle on Feed

survey this afternoon and it showed September placements up 6.1% YOY. The

average trade guess was for a 1.2% increase, so it is pretty clear that this new

data will be bearish for prices as it points to bigger-than-expected supplies

of fed cattle in Q1. Marketings were reported down 10.6% YOY due to

one less marketing day and kill cutbacks by packers during September. All

of that combines to give us a 0.6% YOY increase in the number of cattle

that were standing in feedyards as of Oct 1. Futures traders will likely

interpret that as very bearish when the market opens on Monday.

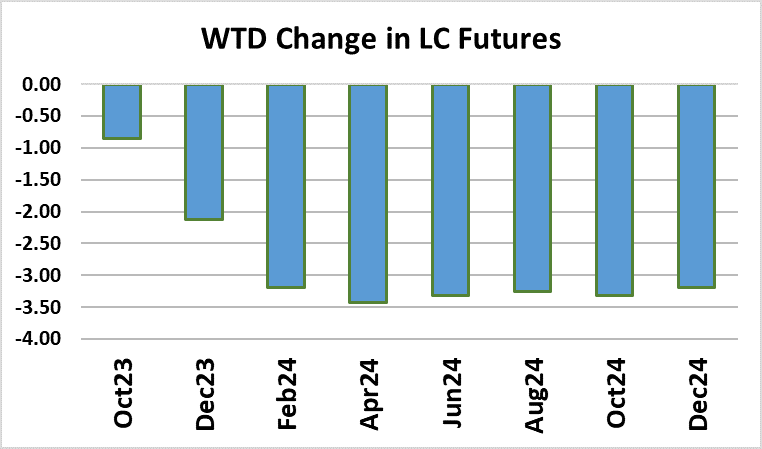

This fresh bearish news comes on top of what was already a bearish week

for the futures. Traders punished all of the 2024 contracts with losses

greater than $3/cwt. That was a little surprising given that cash cattle

prices actually advanced this week, but it reflects nervousness about the

future of the macroeconomy in general and what that could mean for cattle and

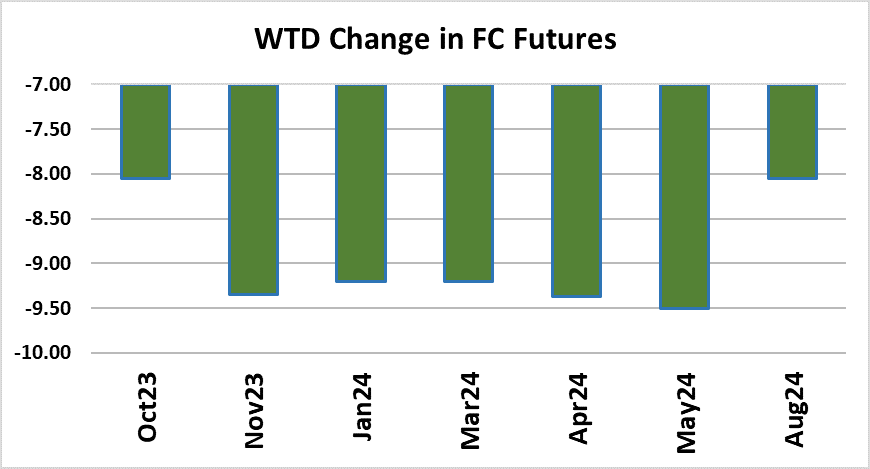

beef prices down the road. Feeder cattle futures got slammed even

harder this week with the Nov-May contracts all losing more than $9/cwt.

Feeder futures had gotten somewhat frothy, so a big correction there wasn’t too

much of a surprise. This week and next are likely to mark an important

reset in the fed cattle and feeder cattle futures, that will allow the market

to resume its uptrend at some point in the future. I’m looking for the

market to remain in a sideways to lower pattern until February and then we

could see some prices accelerate higher next spring and summer. It

is important to remember that all of the margin contained in the beef supply

chain ultimately flows down from consumer demand. Right now that demand

seems to be holding up well, so there isn’t reason to panic. Let the

futures do what they will in the short run, but eventually the futures will

conform to the underlying market fundamentals. Next week, expect more

selling pressure early in the futures and a beef market that trades sideways to

modestly higher unless the ribs catch fire. Cash cattle should trade no

worse than steady unless the carnage in the futures gets so bad that it forces

a lower cash trade early in the week.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}