Beef Wrap October 15

The live market for cash cattle was up a little less than a dollar

this week to $123.85. That puts it about right in the middle of the

trading range it has been stuck in for the last several months.

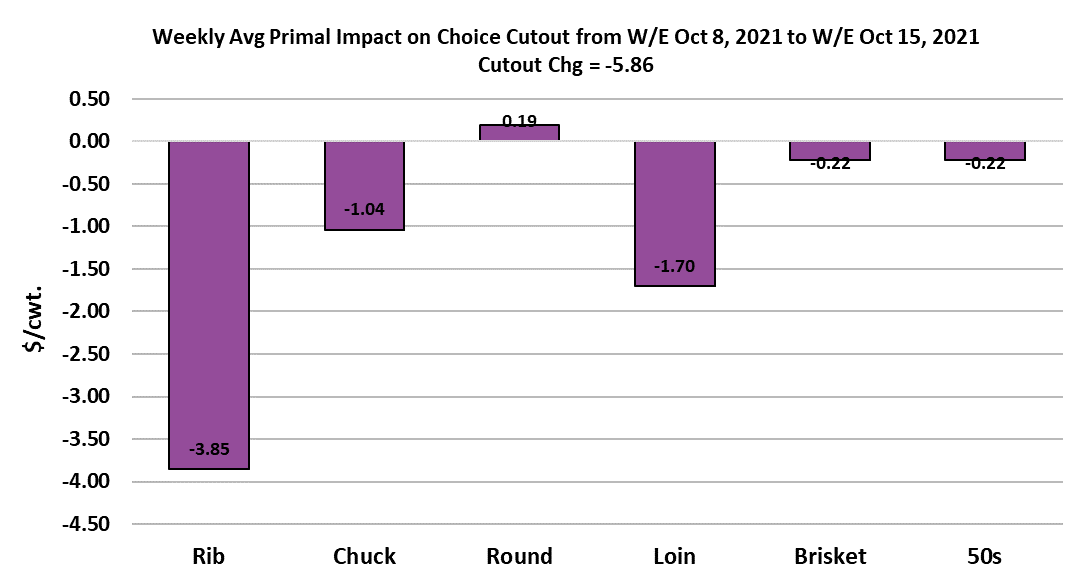

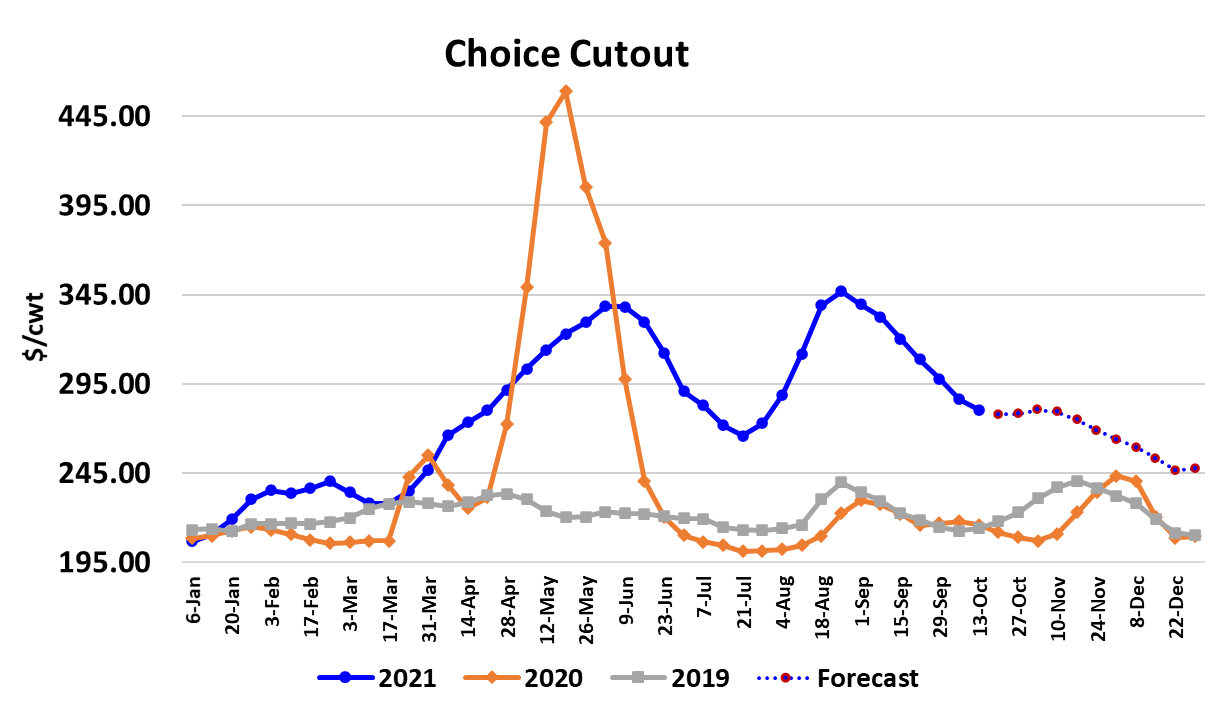

The cutouts continued lower although the losses were very small

near the end of the week. The Choice lost $5.86 on a weekly

average basis while the Select was down $3.61. I’d say the

biggest news in the complex this week was that the losses in the

beef market really slowed down and that could be an indicator

that a bottom is near. The all-important rib primal was down

about $28 this week, but most of that came early in the week. By

the end of the week small price gains were noted.

It may be late getting started, but it looks like we are going to see

at least a modest price rally in the ribs heading into the holiday

buying season. That should be enough to turn the cutouts

modestly higher for a few weeks, but I’m not looking for the

Choice cutout to move back over $300 again in 2021. End meats

are projected lower between now and Christmas as retail feature

interest will shift toward hams and turkeys. Ribeyes and

tenderloins should help to lift their respective primals some over

the next few weeks. Briskets are also called higher into

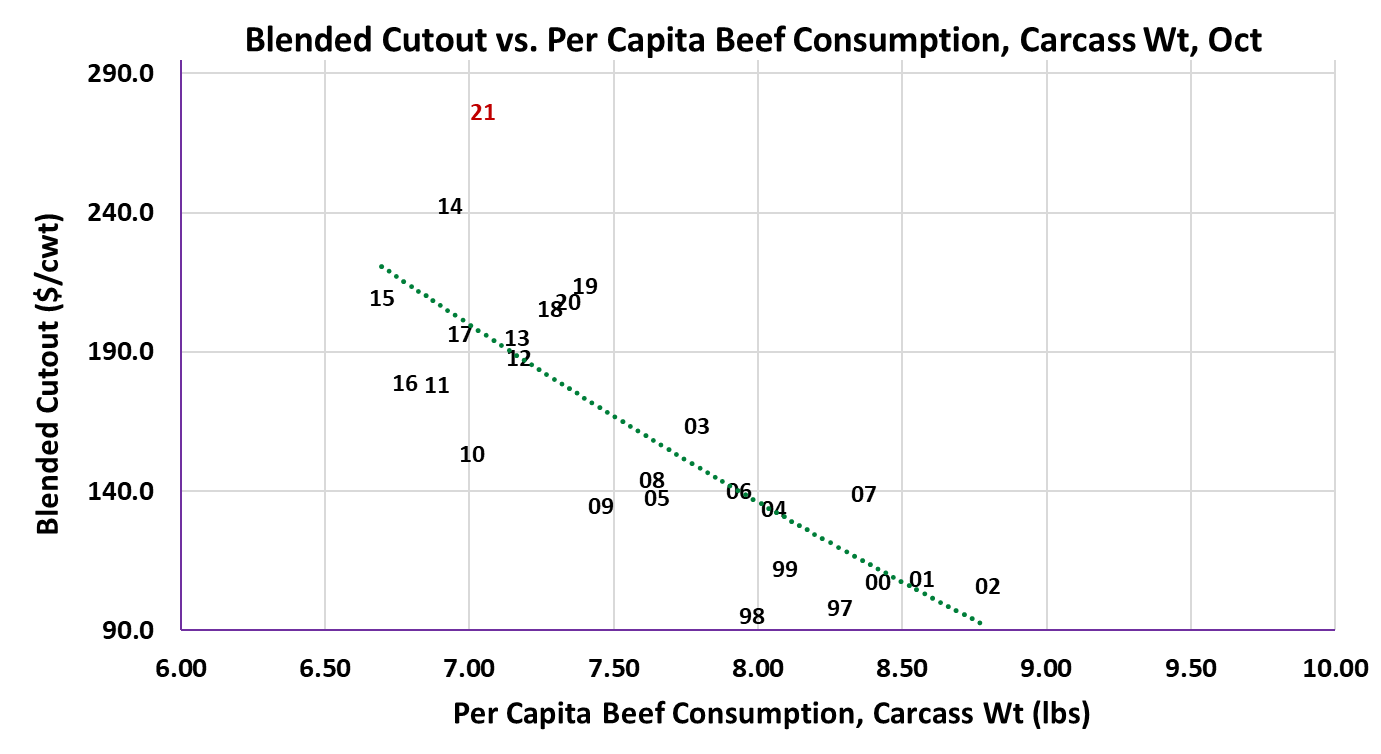

November. The scatter diagram below confirms that beef

demand is still exceptionally strong relative to past Octobers. I

look for that to continue, but expect the current data point to

slowly move back down closer to the regression line. It may take

many months before it gets back down to what could be

considered a normal level. Unless we have another unforeseen

shock to the system, I’m expecting beef prices to work lower over

the next year or so as demand fades and packers find solutions to

the labor bottleneck that has kept beef production constrained.

This week’s fed kill registered only 501k, down 15k from the week

before. That was a disappointing development that was driven by

at least a couple of plants not operating on Friday and there was

no attempt to make up the volume on Saturday. A 501k fed kill

likely is close to sufficient to process all of the cattle that were

targeted for this period, but it doesn’t help to dissipate any of the

carryover cattle from August and September. As such, it makes

it likely that cash cattle prices won’t have a huge rally as we move

through the fourth quarter.

I do have cash cattle working up to $127-128 in November when

cattle supplies should be the tightest, but my expectation is that

won’t persist for long and by the end of December we can expect

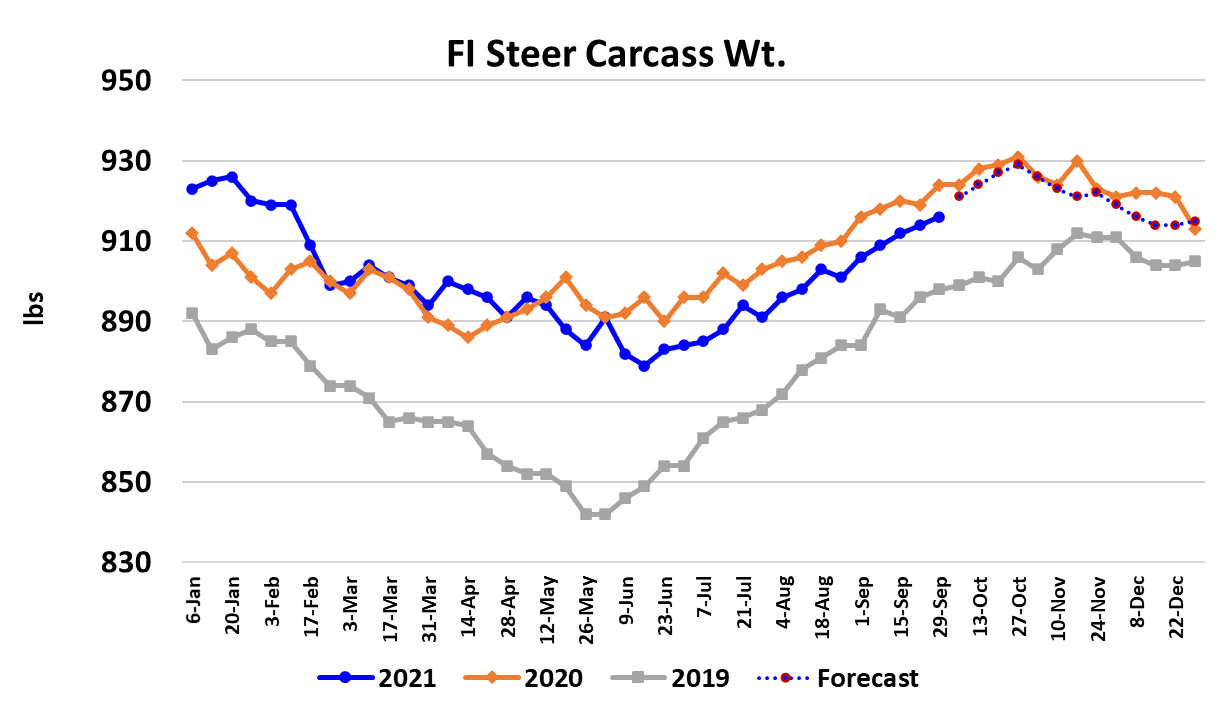

cash cattle back down around $125. This week’s carcass weight

data indicated weights are still trending seasonally higher and

are narrowing the gap with last year. I’ve got weights peaking in

the last week of October, but they have been known to peak

later than that.

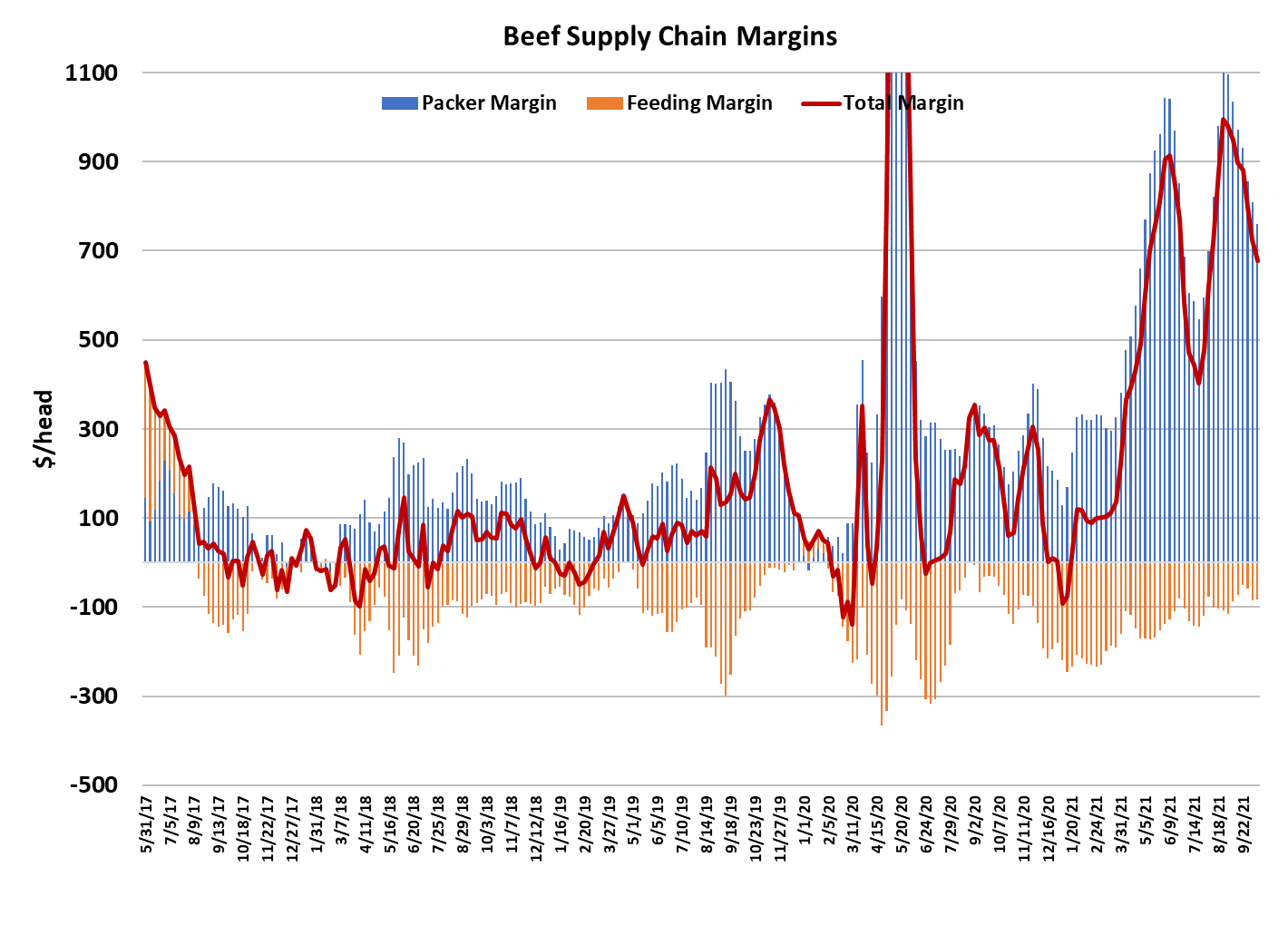

Packer margins fell $48 this week and now sit at “only” $760/

head. It took five weeks to reduce margins from $1000 to $800.

I expect margins to continue to compress, but at that rate it will

be sometime next year before they get back to more normal

levels. Cattle feeding margins appear to be about $90/head in

the red. That’s not enough of a loss to prompt feedyards to

slash placements and packers probably want it to stay that way.

In fact, the data lead me to believe that September placements

are going to be reported about 5% over last year when USDA

releases their Cattle on Feed report next Friday. October

placements could be up that much or more also. So it doesn’t

look like cattle feeders are undertaking any serious effort to

place their way out of negative margins. The only other way out

of negative cattle feeding margins is for packers to find and train

enough labor to remove the bottleneck in plants.

Perhaps that is what cattle feeders are hoping for, but it seems

kind of foolish to hand over one’s destiny to packers. It would be

much better for feedyards to take corrective action themselves.

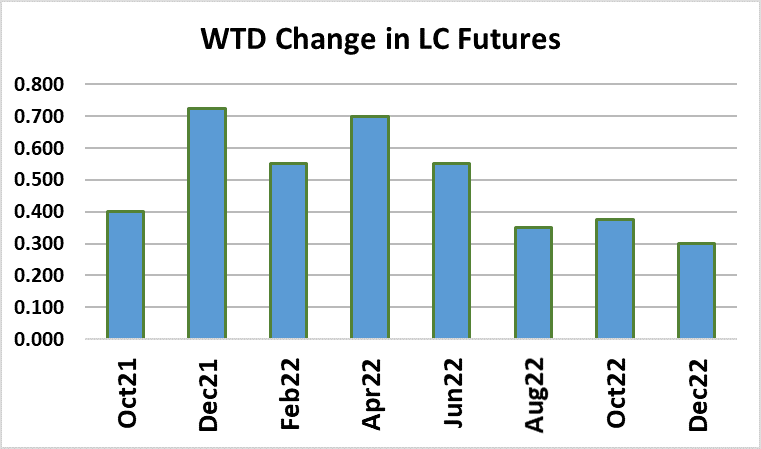

Futures were modestly higher this week, building on last week’s

gains, but as the Oct contract started to approach $126 late in

the week it drew 25 deliveries on Thursday and another 31

deliveries on Friday. Next week, look for further improvement in

rib prices to turn the cutouts modestly higher. Because of the

bottleneck, that won’t matter much for cash cattle prices, but it

will raise costs for those beef buyers still short on holiday middle

meats.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}