Beef Wrap November 11

Cattle feeders managed to press a little more money out of the

packers this week as average live steer prices were about $0.75

higher to $152.70/cwt. Packers did take on a large volume at that

price and should now be well positioned to run a big kill next week.

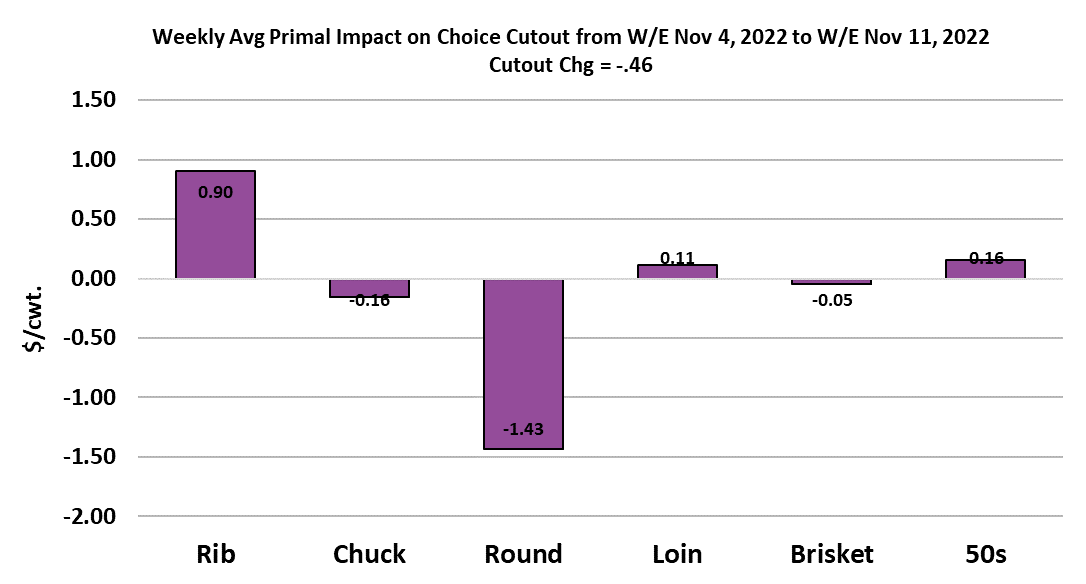

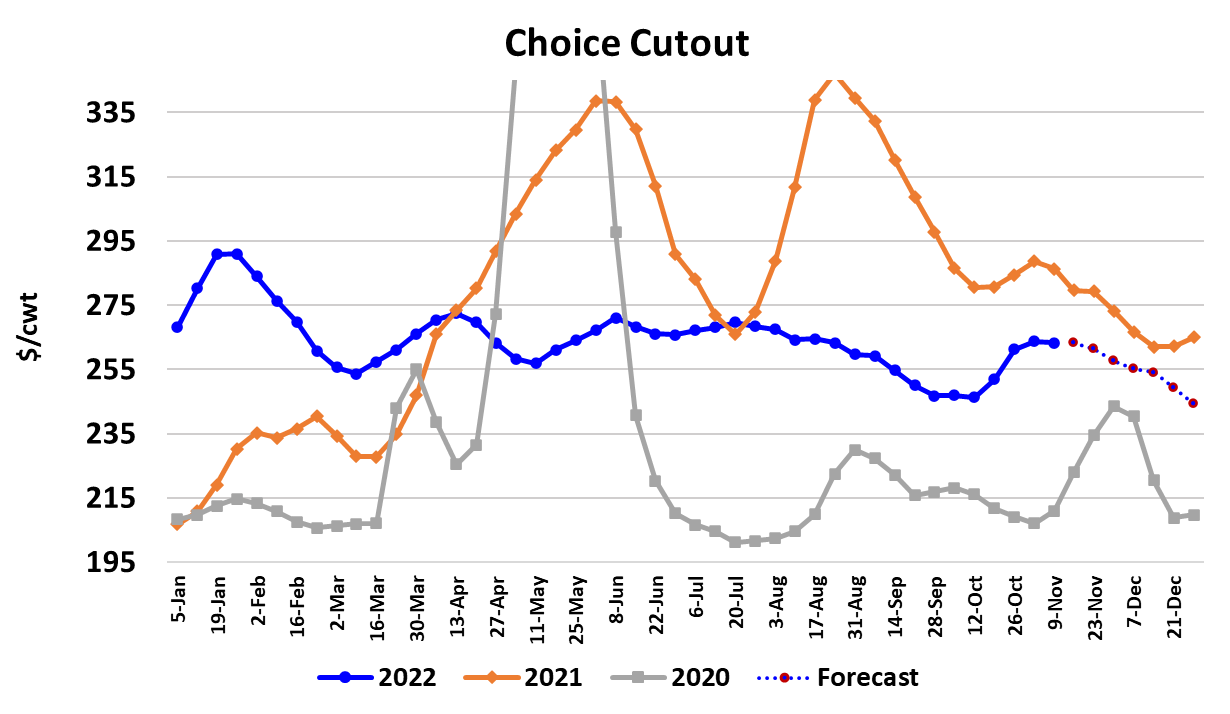

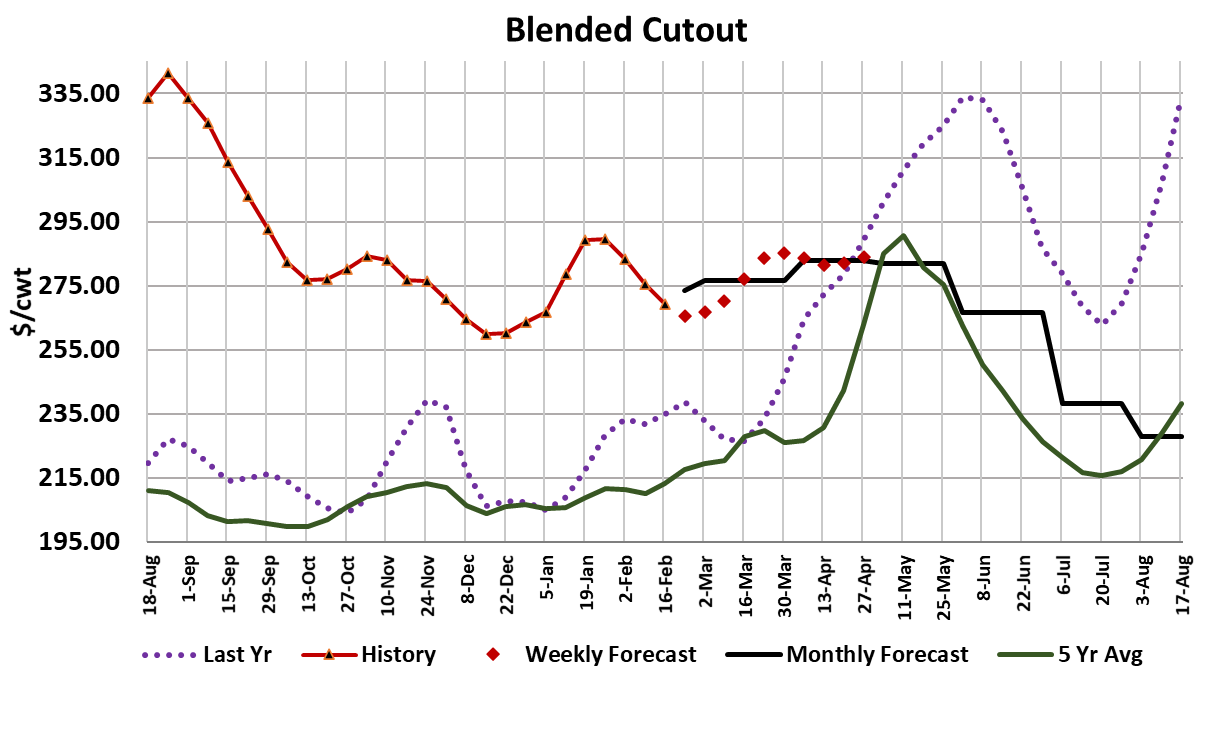

The cutouts were steady to slightly higher, with the Choice losing

$0.46 on a weekly average basis, while the Select was up $2.80/cwt.

That caused the Choice-Select spread to narrow by almost $3—

something that is very unusual for this time of year. Normally in early

November the Choice middle meats are racing higher and that causes

the Choice-Select spread to widen, not narrow. However, it is more

accurate to say that this year middle meat prices are crawling higher,

not racing. This has to be creating some concerns for packers since

the cattle that they will be killing next week cost about $7/cwt. more

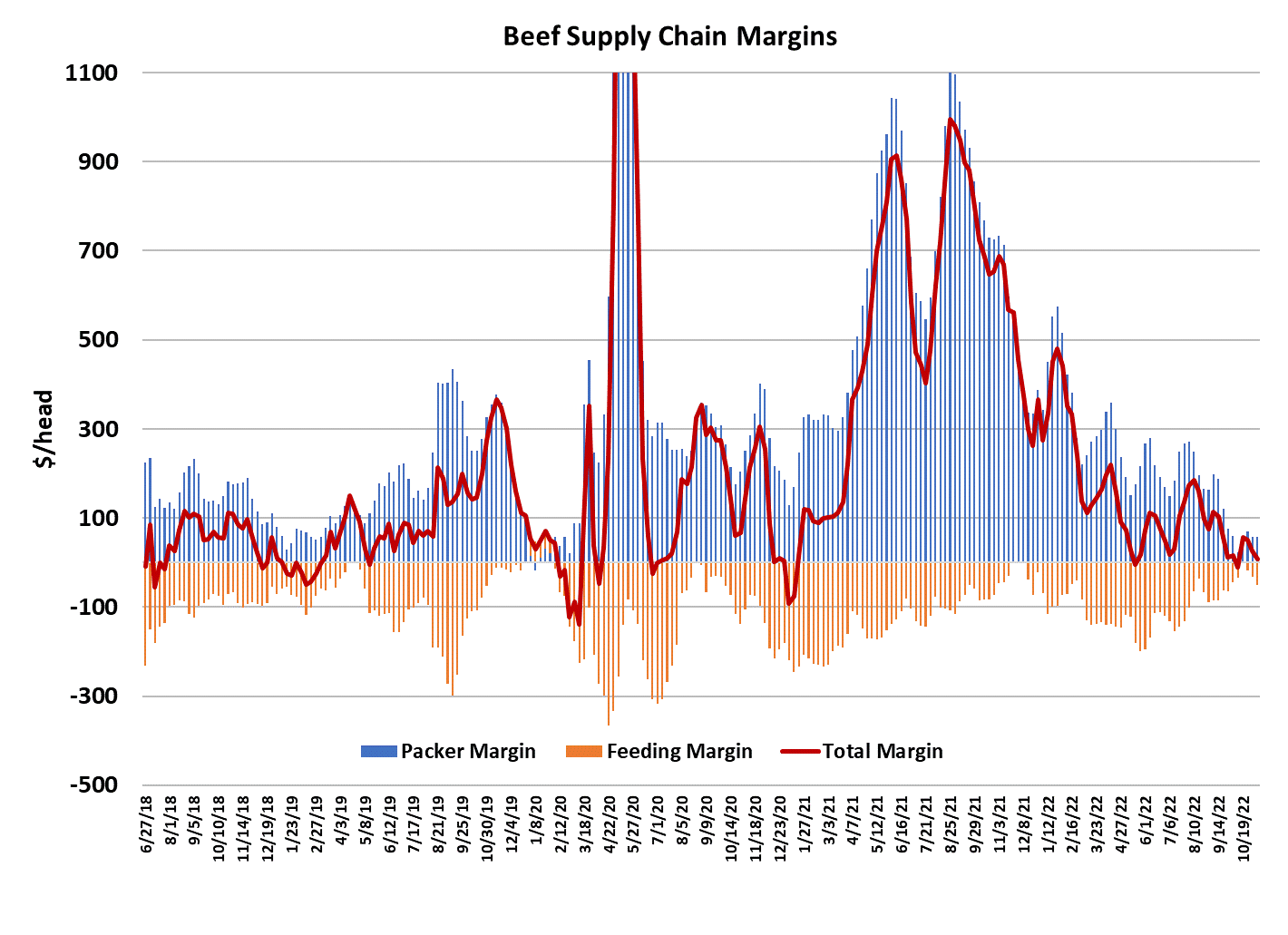

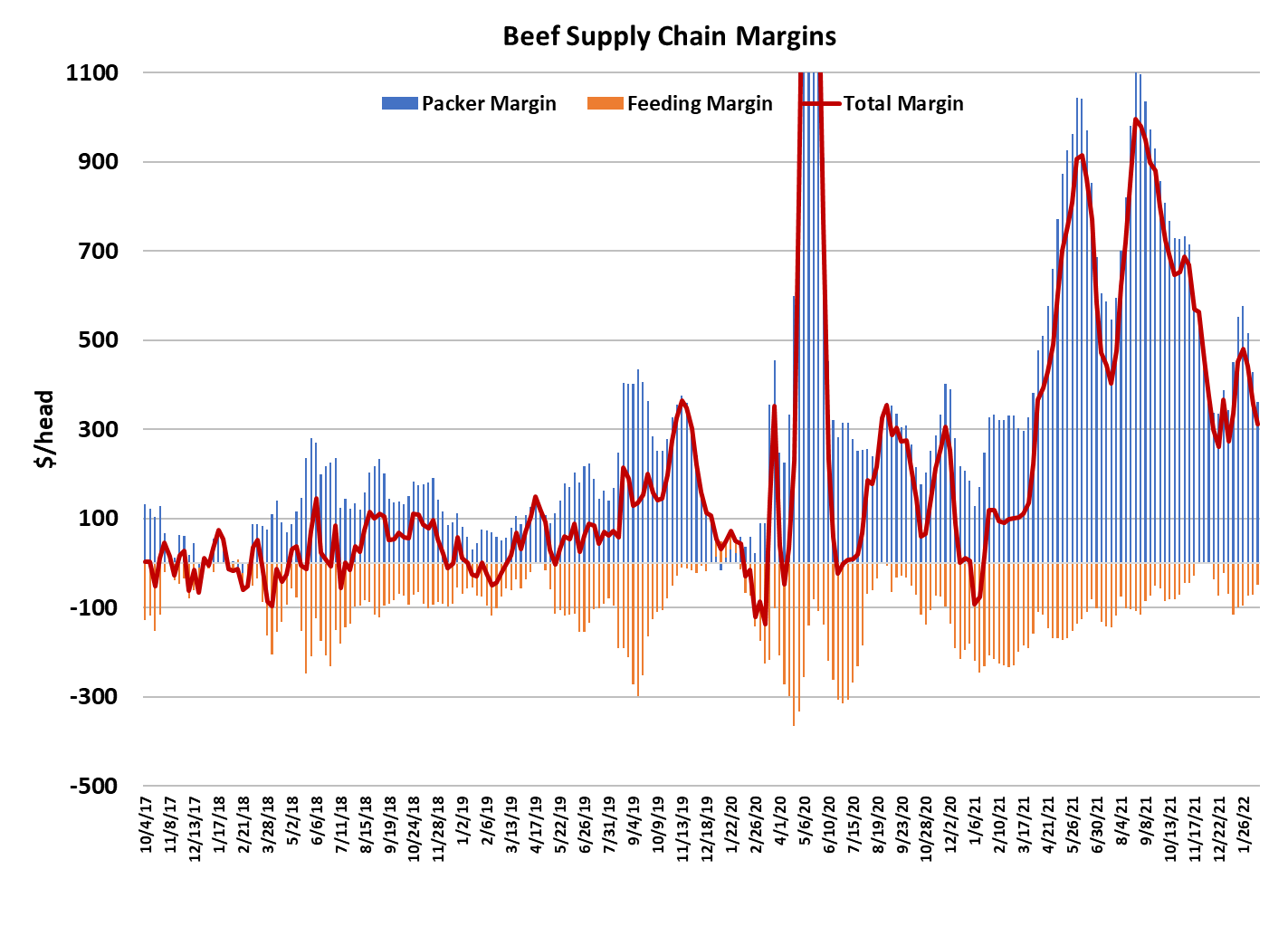

than what they were paying a month ago. Packer margins were

mostly unchanged this week at $57/head, so they aren’t getting the

type of margin gains that are typical at this time of year either.

To be sure, there is still time for packer’s fortunes to turn around, and

there is often a decent rally in middle meat prices during early

December as buyers finalize their Christmas purchases. But I’m not

very hopeful for that this year. It looks to me like the market may be

very close to topping the cutouts in the next couple of weeks. The

middles may still gain, but the end meats and grinds are starting to

slip lower and that could end up negating any benefits that middles

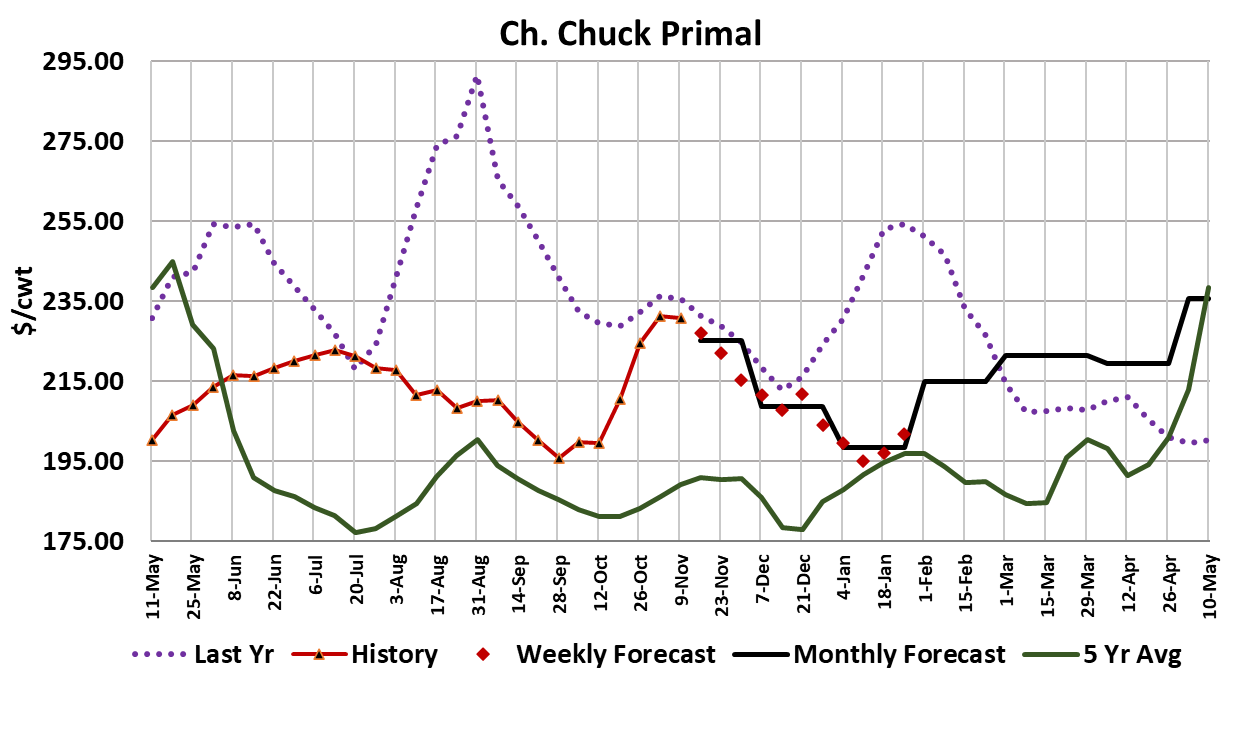

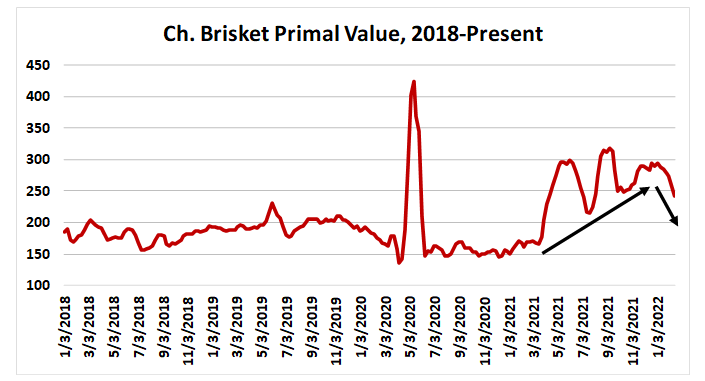

bring. The attached chart indicates that losses in the round, chuck

and brisket this week outweighed the gains in the rib and loin primals.

I’m afraid that story might repeat again over the next few weeks. Let’s

imagine for a moment that the cutouts can’t add much more value

than they have right now. What will happen to cattle prices and thus

packer margins? I really don’t think that cattle feeders are going to

show a lot of generosity to the packers and sell their cattle cheaper

just because beef prices are not rising.

I think packers would need to force the issue by cutting way back on

the kill for a few weeks to help improve their position in the

psychological chess match that is the cash cattle market. Will they do

that? So far they haven’t shown much willingness. There is just too

much forward contracted beef that needs to be delivered. As a result,

I’m not very bullish on packer margins. In fact, as I revised the

fundamental forecasts this week, I began plugging in negative packer

margins for late December and through January. If I didn’t do that,

then I’d have to have cash cattle prices in the $130s and no one is

going to believe that will happen given that we are sitting very near

$153 today. In fact, futures traders seem to believe that there won’t

be any concession in cash cattle prices between now and the end of

February. The demand side of the beef market feels very soft at

present. The combined margin has turned lower once again after

head-faking higher a couple of weeks ago. Trim markets are falling

fast and I’ve always taken that as a bearish sign.

I’m a little concerned that the combined margin might

be on its way to -$100/head, which is something that has only

happened a couple of times in the past five years. Inflation is still a

huge problem in the macroeconomy and there is no indication that

the Fed will stop raising interest rates anytime soon. The October

CPI, which was released on Thursday, showed a very slight easing in

inflation and that was enough to send the DJIA soaring over 1000

points in a single day. That should be good for consumer confidence

if it lasts, but the market could take that back in a heartbeat. The

University of Michigan Consumer Confidence Index released today

was down a little over five points from the previous month and very

near all-time lows. That doesn’t seem like the type of environment

that will generate robust beef demand. On the supply side, this

week’s steer and heifer slaughter clocked in at 518k, up 2k from last

week and still above the level that our flow model projects.

I’m looking for packers to do an even bigger kill next week, perhaps

as high as 530k, as they try and get ahead of the short kill that will

come in the following week. Next week USDA will provide the results

of their Cattle on Feed survey for October and I’m looking for

feedyard placements to be down almost 7% from last year. If that

prediction comes true, then it will create a situation where feedyard

inventories as of Nov 1 are down about 2.3% YOY. A couple more

months of YOY placement declines and we could have feedyard

inventories down 5-6% by February or March. Packers had better

keep their fingers crossed that there is no serious winter weather that

hinders cattle performance this year. Numbers are already going to

be tighter than what they are accustomed to in Q1, so any adverse

weather would just make the situation worse and could cause them

to have to pay up for cattle at a time of year when beef demand is

likely to be very soft.

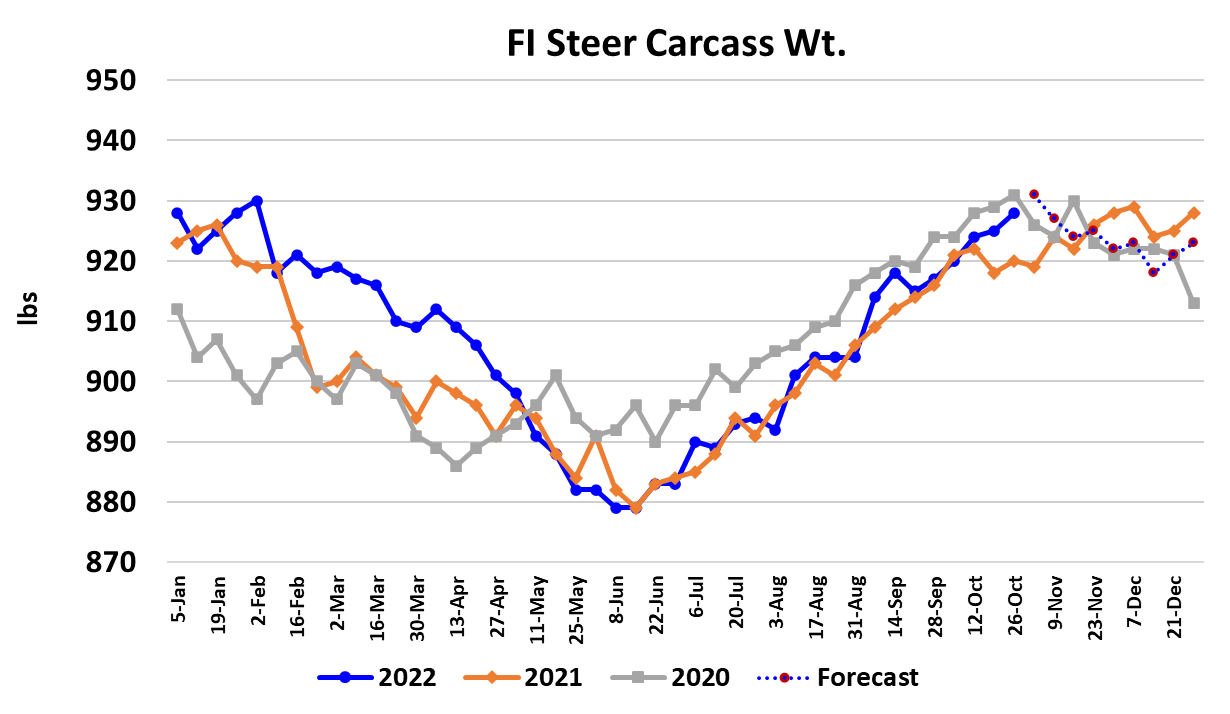

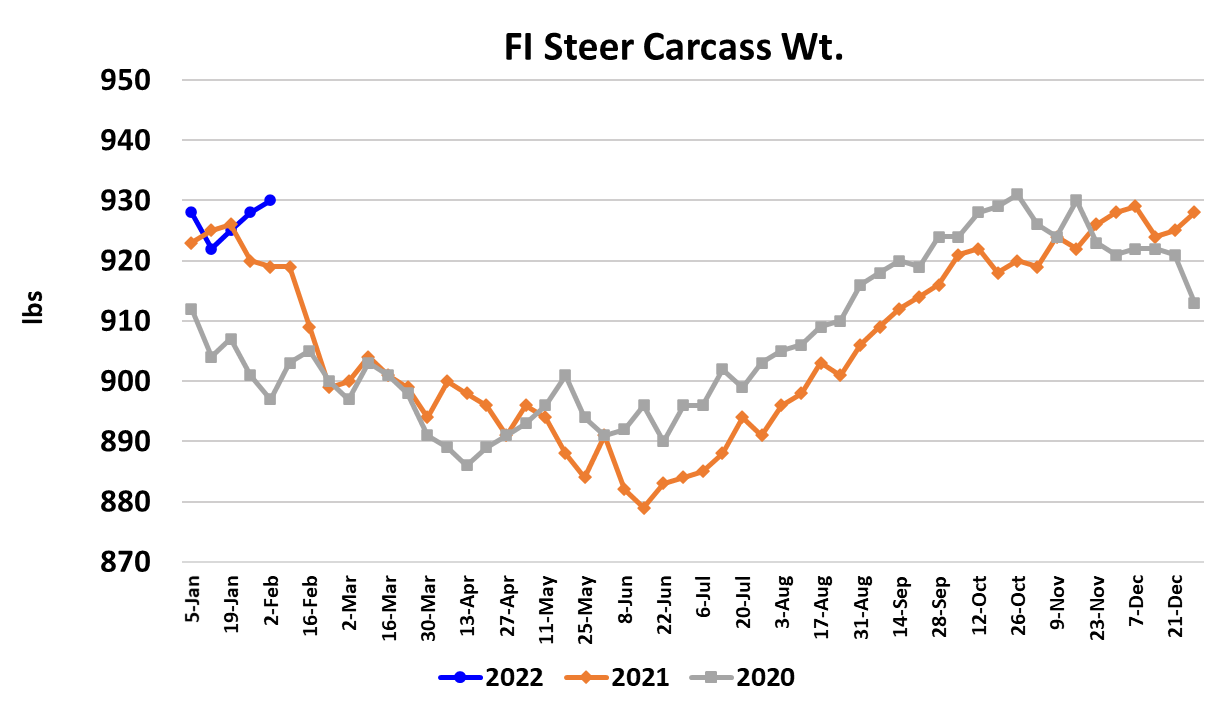

Steer carcass weights rose 3 pounds this week to 928 pounds and

are now 8 pounds higher than last year. The DTDS weights are

working higher and that normally signals a loss of currentness by

feedyards, but the DTDS is still at relatively low levels, so I don’t think

that weights are going to have much of a detrimental impact on cash

cattle prices in the near term. Weights will probably top sometime in

the next couple of weeks at just over 930 pounds. For now, the

supply side of the market appears well behaved and sufficient for the

level of demand. However, market-ready cattle supplies are likely to

shrink as we move into Q1, so things could get interesting, especially

if Old Man Winter turns angry. Next week, watch for the middle

meats to move a bit higher, but that could be offset by further

weakness in the end meats. Packers will be purchasing for cattle for

a short-kill the following week and they got a lot bought this week, so

they might not need to be very active in the cash market. Futures

could be vulnerable as the bulls get tired of waiting for the holiday

season rally to start.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}