Beef Wrap November 24

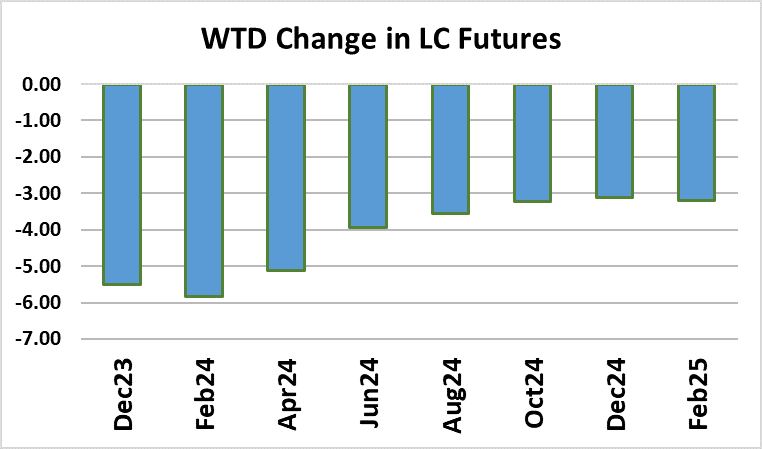

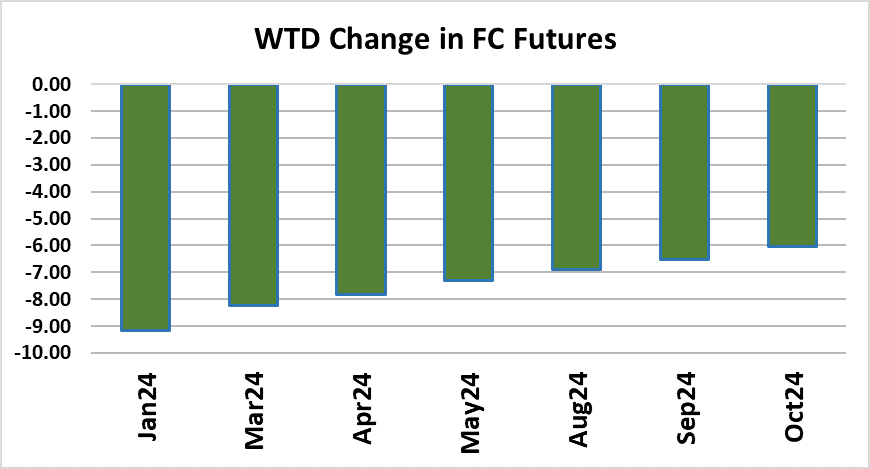

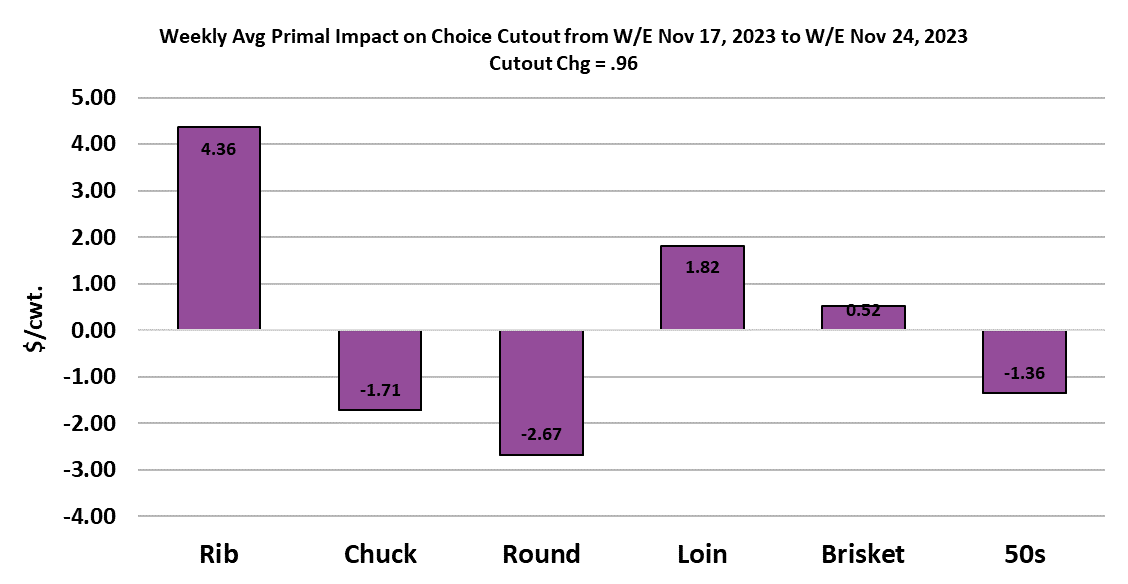

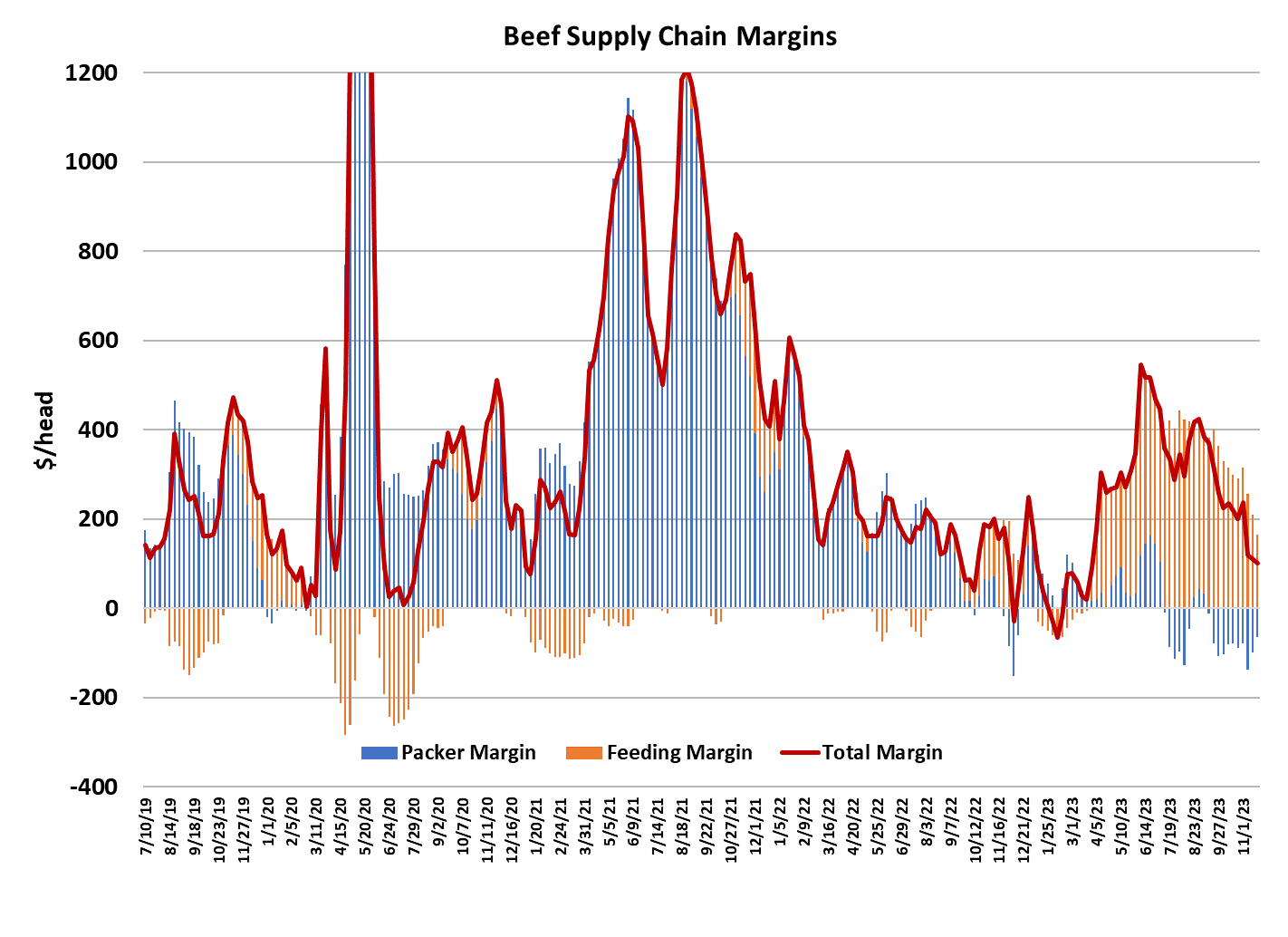

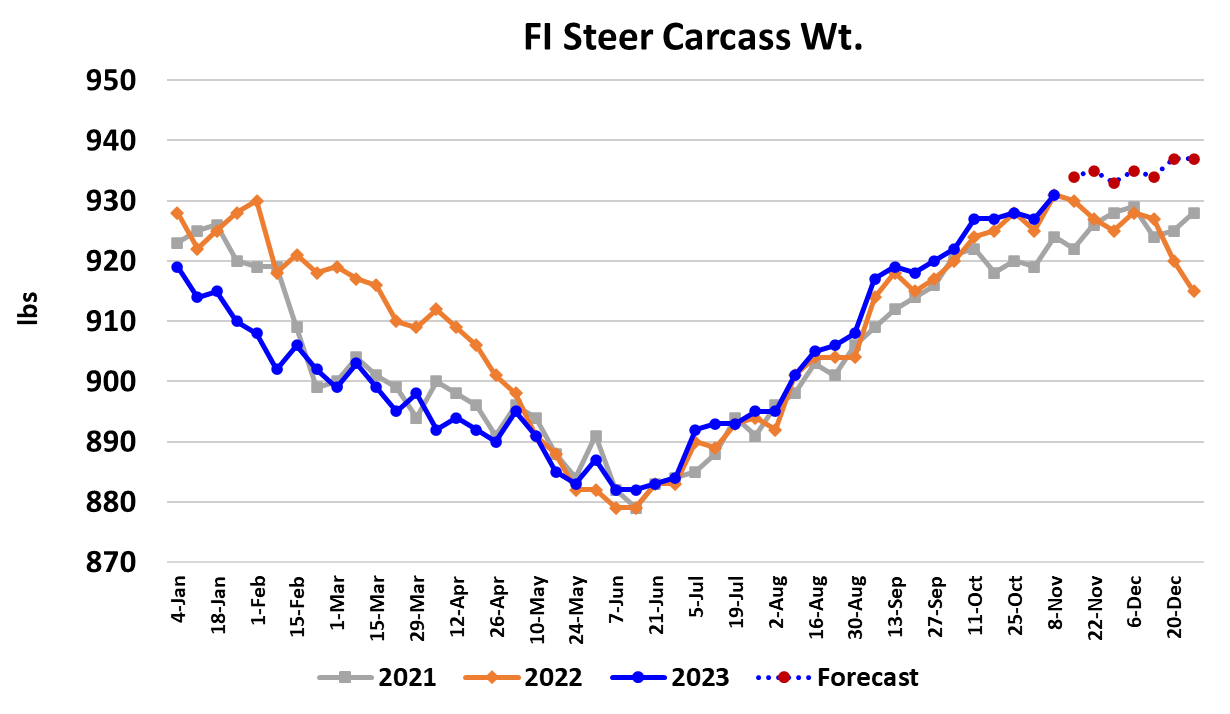

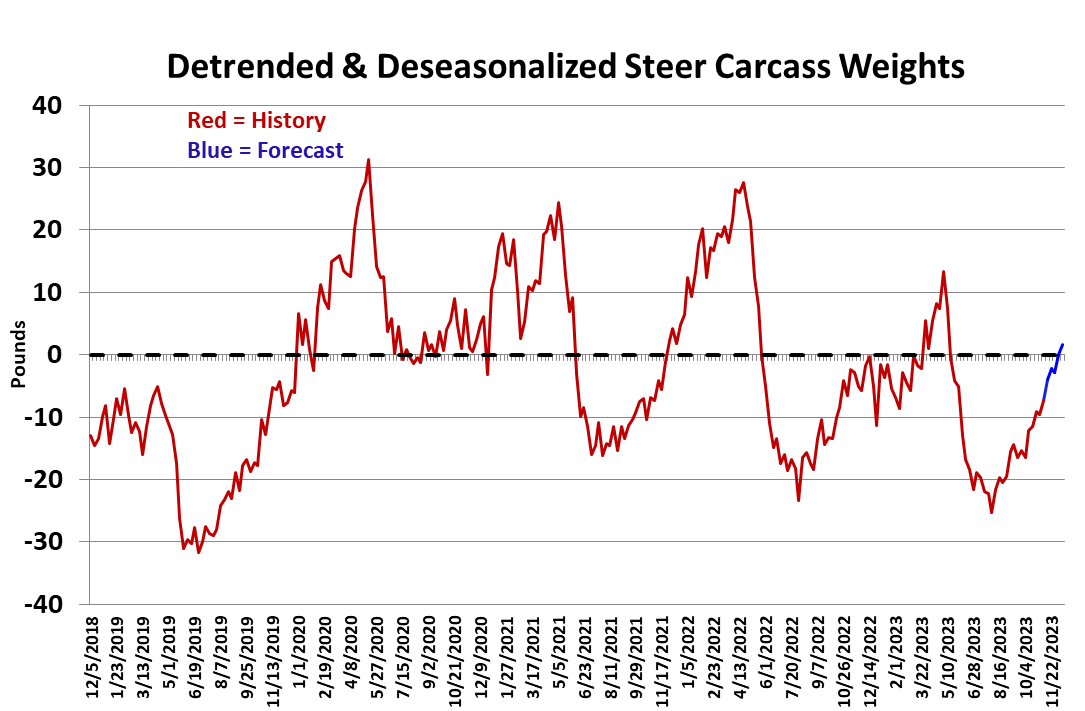

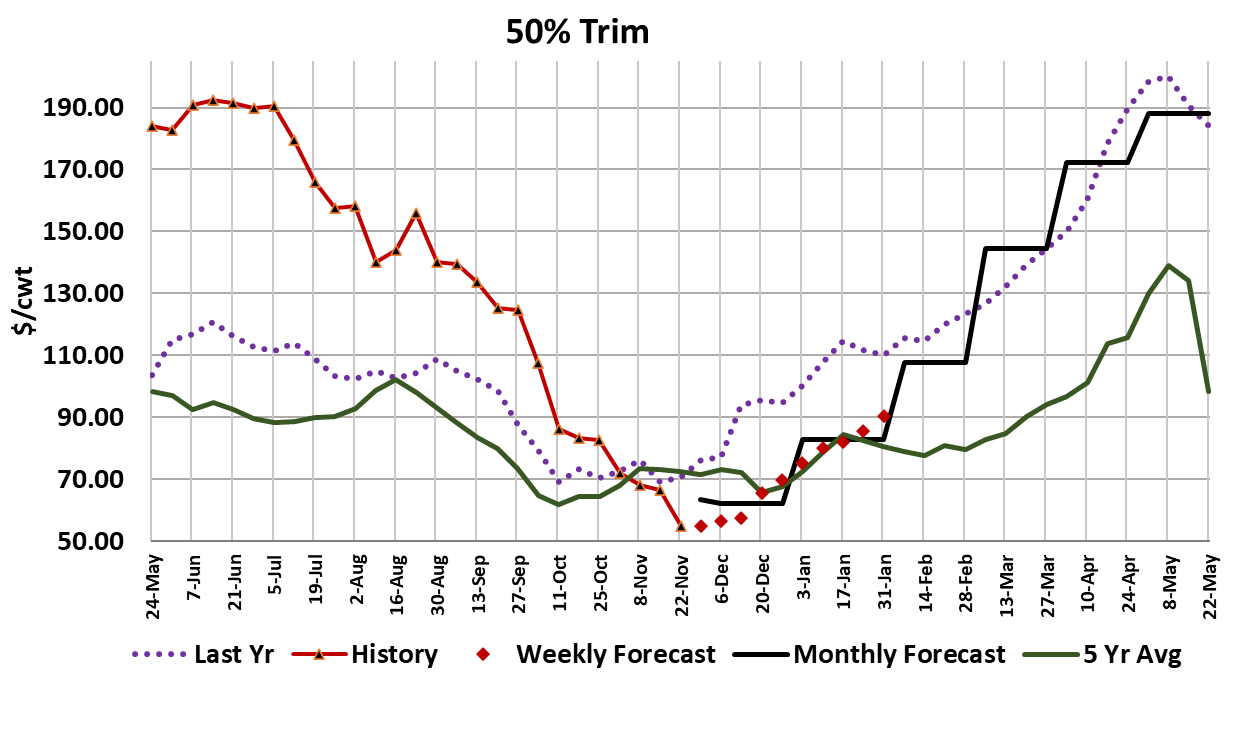

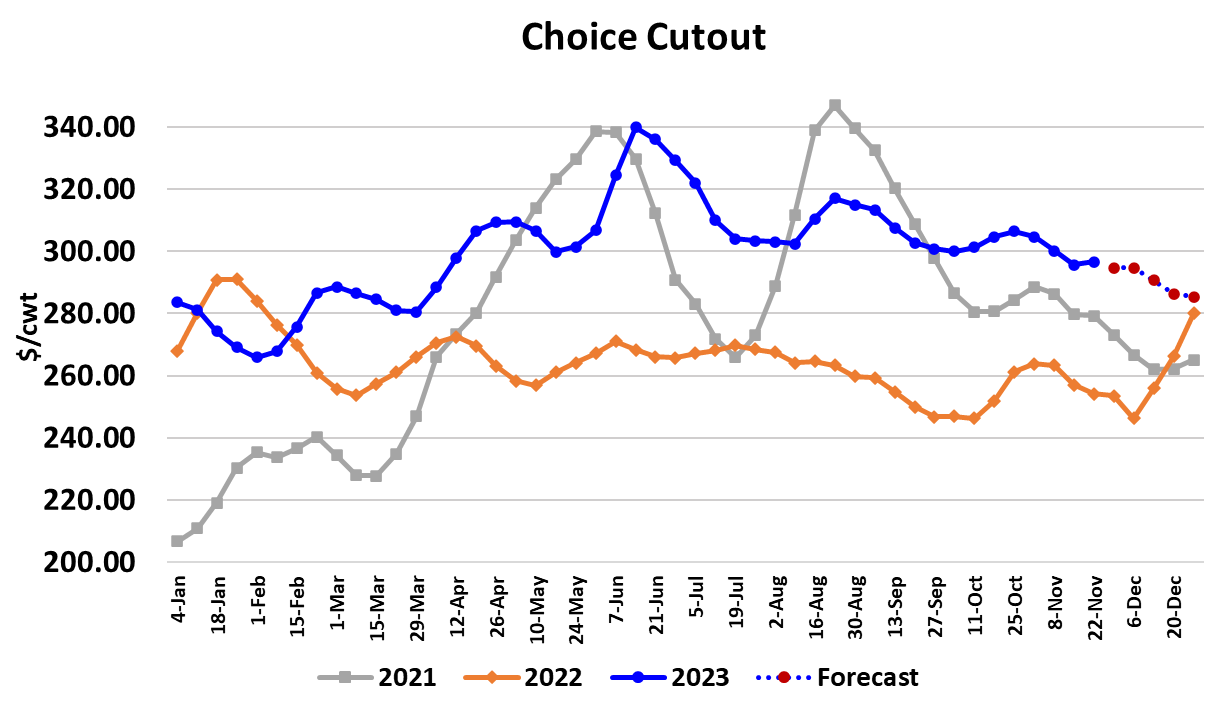

It should have been a quiet holiday week in the cattle and beef markets. The cutouts were up a little, the cattle market was down a little, but the futures market threw a hissy fit again and some of the front contracts lost almost $6 over the course of the four-day week. It makes one wonder if human futures traders are paying attention to what is going on in the cash markets or if we simply have a bunch of computers trading with each other and taking the market wherever the program sends it. This week saw some gains in the rib primal that were strong enough to offset further declines in the end cuts and thus the Choice cutout added $0.96/cwt. to average $296.65/cwt. The Select cutout was up $0.31 to $269.03 on a weekly average basis. Cash cattle trading got started on Wednesday and prices there were mostly $177/cwt., down about a dollar from the week before. On Friday, as the futures market was melting down, packers swooped in and found some cattle feeders in the northern region that were willing to take $275 dressed. That was down $5 from the previous week. The most important question that we can explore at the moment is “What is causing all of the fear in the futures market?” I think that traders are fearful that cattle are going to get backed up in the supply chain and thus cause prices in the cash market to crater. Some of what happened this week might be related to the carcass weight data that USDA published in its comprehensive cattle report. That report showed carcass weights jumping 10 pounds in one week and everyone knows that escalating carcass weights typically precede a backlog of market-ready cattle. However, I think that 10-pound increase is suspect because the previous week that report showed a solid drop in carcass weights that failed to materialize in the weekly FI carcass weights. So, at least half this week’s 10-pound increase was probably just a correction from the previous week’s error. That said however, there very well could be a carcass weight problem brewing longer term. The de-trended and de-seasonalized weights have been steadily rising and if my forecast is close to correct, they will reach zero near the end of December. So that suggests that feedyards will be less current at the end of the year than they are now and we know there will be two holiday-shortened kills associated with the Christmas and New Year’s holidays. Packer margins are still in poor shape (-$60/head this week) and their forward book is really light for this time of year. Therefore packers won’t have a lot of incentive to slaughter aggressively and thus help feedyards remain current. In addition, placements have been strong for the last couple of months and feedyard inventories as of Nov 1 were 1.7% larger than last year. When we put all of those things together, it does start to paint a ominous picture for feedyards and perhaps that is what futures traders are reacting to. Another thing to think about is that prices for many commodities are now well off of their pandemic highs and perhaps it’s just cattle’s turn to reset price levels. Beef demand, even though it is historically strong, is starting fade a bit and when the holiday business dries up in a couple of weeks, that weakness in demand could accelerate. So that is another concern. However, we must not forget that the liquidation phase of the cattle cycle is ongoing and animal numbers are shrinking. That is a powerful force that will be supportive to cattle and beef prices over the next couple of years. While the near-term pessimism might be justified, it probably doesn’t alter the longer-term price potential and the selling in the futures has dragged down the prices of the 2024 and 2025 contracts to very attractive levels given the cyclical supply contraction that lies ahead. It is worth a close look at the combined margin chart this week. Note that it is still working lower and is now moving back into the lower end of the historical range (below $100/head). It hasn’t been this low since early spring, so this has been a very strong run where there was plenty of margin in the system to support prices. Going forward, there is likely to be less overall margin available and so the competition between the various segments of the supply chain should intensify. Another leading indicator that I like to keep an eye on is the price of fat trim. There are a lot of factors that affect pricing in that market, but often it can give a clue about the near-term supply of fed cattle. This week the 50s averaged close to $55/cwt. and the attached chart shows how far that is from the highs posted last spring. Hopefully, it is pretty near its annual bottom, but it looks pretty bearish at the moment. We knew that the kill would be small this week due to the holiday, but packers slashed it even further than I imagined, with the fed kill estimated at only 417k. They made almost no attempt to make up ground on Saturday. That is a bit concerning as well when we think about feedyard currentness. Next week, that tiny production could collide with short-bought beef buyers looking for holiday middles and thus I expect that the cutouts will see some modest gains. In the cattle market, cattle feeders will do well to hold the market steady, but the odds are greater that it declines again.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}