Beef Wrap November 17

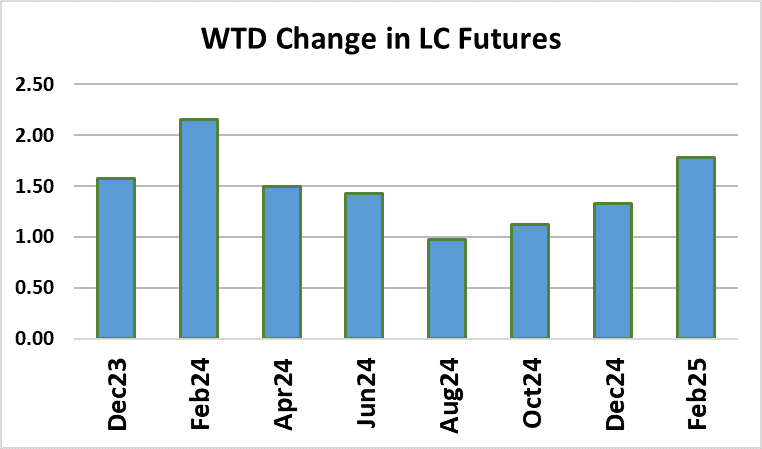

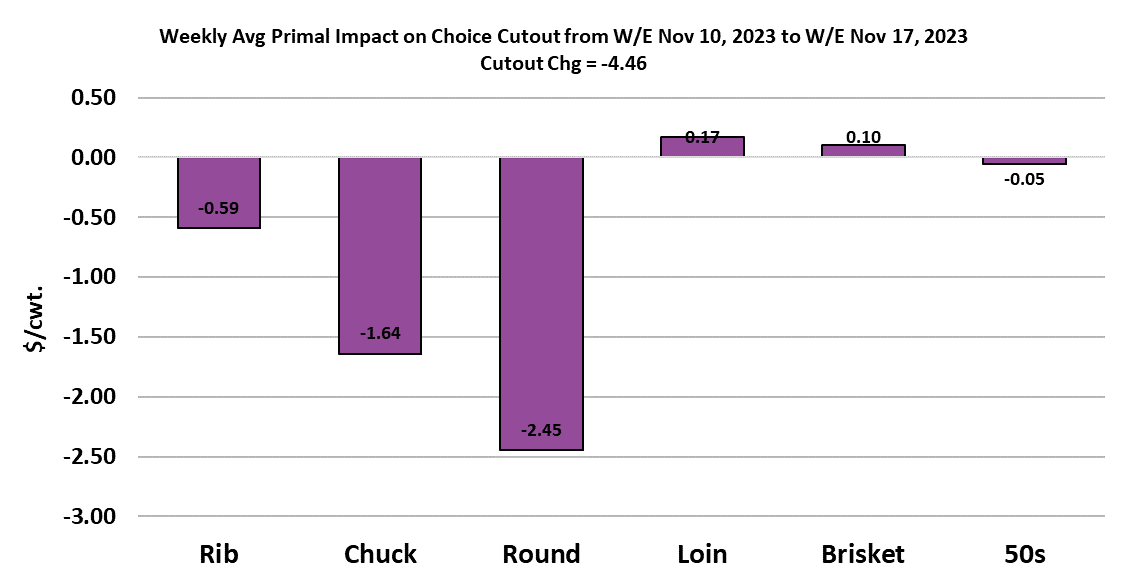

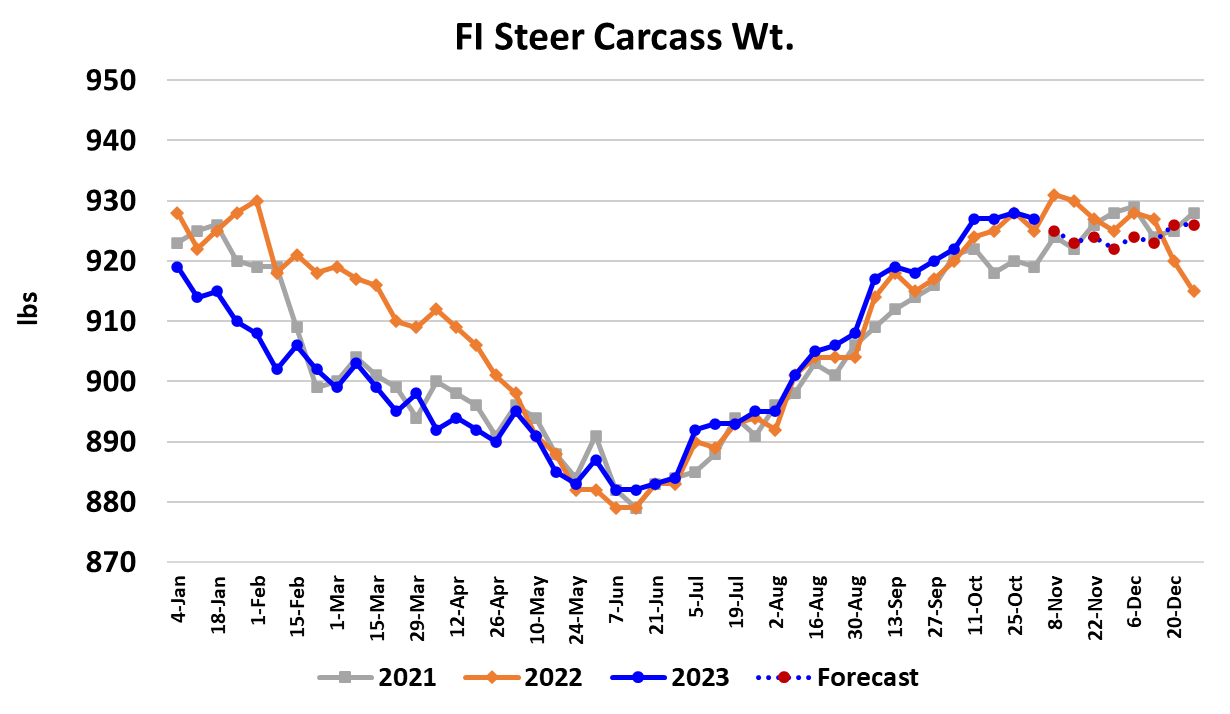

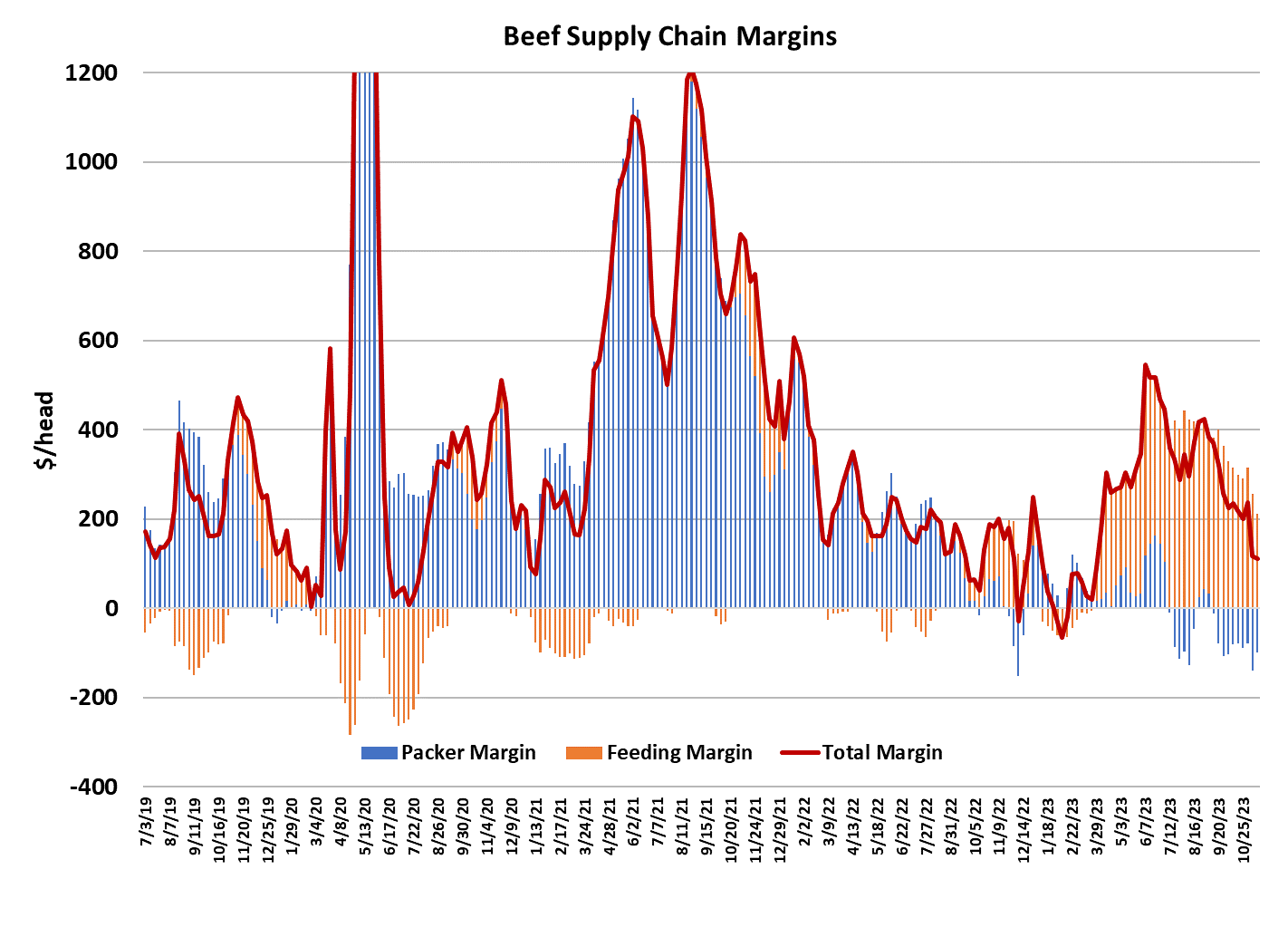

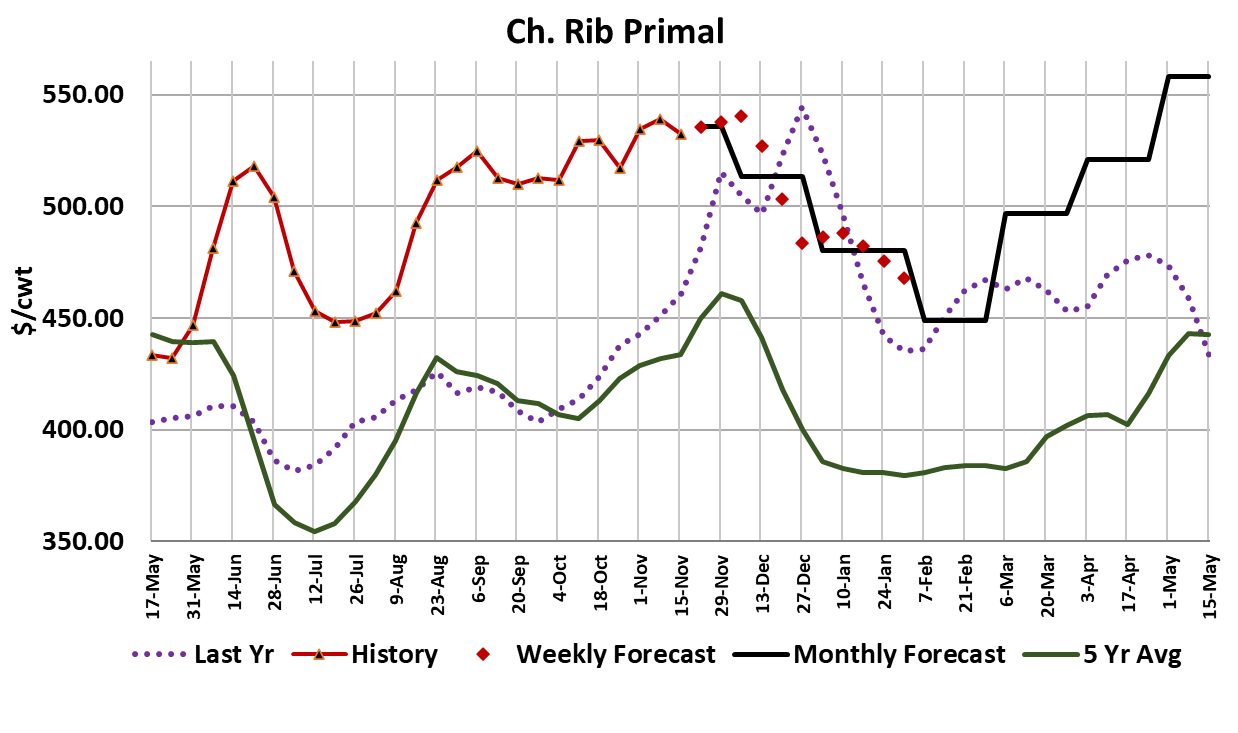

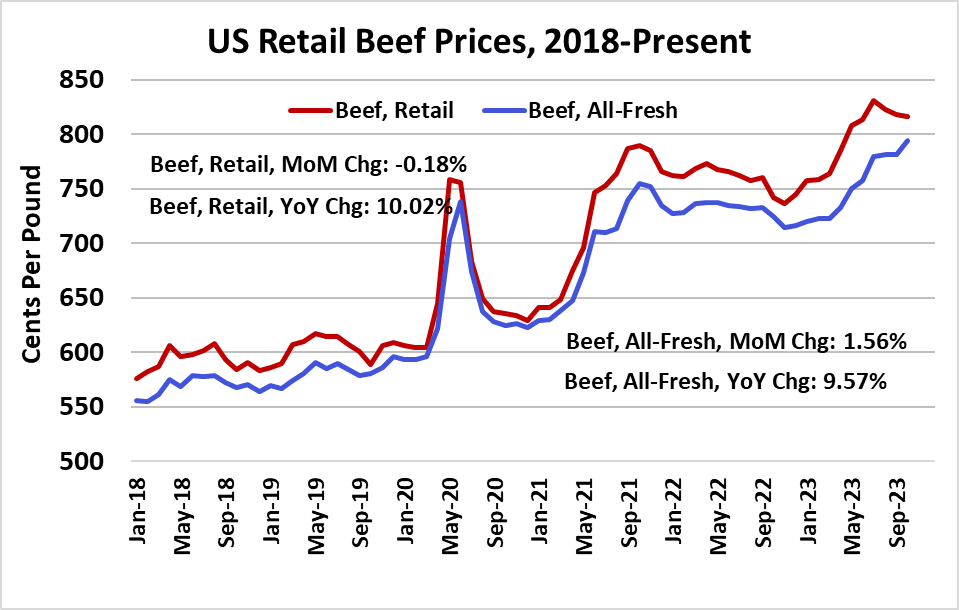

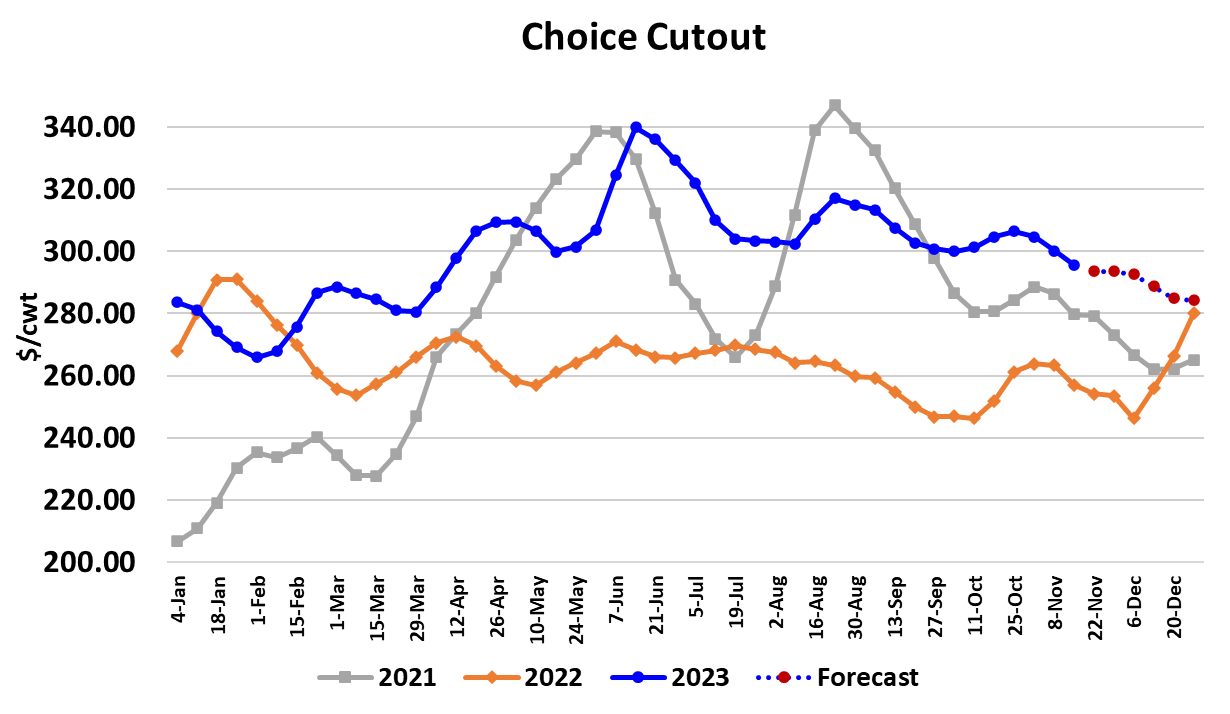

Live cattle futures settled down this week following the rout that took place last week. All contracts finished $1-2/cwt. higher than the week before. Whether or not that was justified remains to be seen because both the cutout and cash cattle moved lower. The Choice cutout dropped $4.46/cwt. to average $295.69 and the Select cutout was down $0.88/cwt. to $268.66. Once again, it was the end cuts that applied the most pressure. It was also notable that the ribs were lower again this week. In most years, rib prices are rising rapidly toward a peak in late November, but this year the ribs have only managed a small gain since the end of summer. Even though production has been relatively light in recent weeks, price levels for most beef items have moved lower and that points to some erosion in beef demand. In a historical context, beef demand is still quite strong, but in recent weeks it appears to be slipping. The combined margin eased a little lower this week and it appears that this downcycle still has a little bit more life left in it. Note, however, that the combined margin is still stronger than it was at this time last year. The futures moved higher for the first three days of the week, but a sharp sell-off on Thursday persuaded cattle feeders to take about $2 lower in the cash market. It looks like this week’s trade will average just a tad under $178/cwt. Both the North and South traded at that level, erasing any price differential between the two regions. The cash cattle market has lost $7 in the last two weeks and that is reduced cattle feeding margins down to about $200/head from the $300/level that was posted in late October. Still, packer margins are much bigger problem, registering close to $100/head in the red, even after getting cattle bought cheaper over the last two weeks. The cutouts are moving lower almost as fast as the cattle price and thus it has been difficult for packers to make much headway in improving their profitability. To be sure, the cutouts have come down faster than I expected, mostly because it was difficult for me to forecast declining beef demand in the middle of November, but that seems to be what is transpiring. Next week will be mostly about turkeys and hams for the retail sector, so beef movement will naturally be slow. However, following Thanksgiving week, retailers often like to give beef a strong presence in their ads because they realize that consumers are sick of turkey and ham and want a change. That might mean some help for the struggling end cuts just past Thanksgiving, but I don’t think it will be a huge gain. The fundamental forecast has the Choice cutout continuing to ease lower over the next few weeks and then dropping faster from mid-December onward as holiday middle meat demand dries up. A big part of the problem is that retail beef prices are still rising and that is limiting movement. This week, USDA reported that the all-fresh retail price in October was up over 1.5% from September. That price is now 9.5% higher than in October, 2022. So, price inflation is alive and well in the retail beef case. Maybe if the cutout continues to weaken, retailers will start to lower their prices, but that isn’t guaranteed. They have been burned several times over the past year and a half by spiking wholesale beef prices and thus may opt just to keep their retails steady. Over the next couple of months, cattle feeders will need some help from better retail off-take in order to move the number of cattle that will be ready for market. It looks to me like that could all come to a head in January, when fed kills in the 505-510k range will be necessary in order to keep feedyards current. If the consumer off-take only supports 485k, then there will be problems and cash cattle prices could move rapidly lower. Retailers can see that the cutouts are now drifting lower, but the lag time for that to show up in retail prices is long and come January retail prices might still be near today’s levels. That is a concern. This week’s fed slaughter registered 492k, which was up almost 20k from the week before, but some of that can probably attributed to packers trying to get a little extra product around them heading into next week’s short kill. I’d look for a fed kill next week a little below 450k. The flow model is pointing December fed kills around 490k in the non-holiday weeks. That should be manageable, but they will need to kill a lot more in January. Steer weights were reported down one pound this week and that was a bit of a surprise since I had a few more increases built into the forecast. As a result, I lowered the near-term weight forecasts and then realized that the top in carcass weights may have already happened in the last week of October. That wouldn’t be particularly unusual from a timing perspective. If that turns out to be the case, it means a bit less production from now to the end of the year than I originally envisioned. Every little bit helps. Today’s Cattle on Feed report showed October placements up 3.8% YOY. That was less than the 6% increase that analysts were expecting. The futures market might get a little boost from that on Monday, but it’s not a major game-changer. The total number of cattle on feed as of Nov 1 is 1.7% larger than last year, so concerns about large cattle supplies on the horizon won’t go away. The weekly export data continues to look soft, so no change there. Next week, beef will be on the back burner as the population celebrates Thanksgiving. That probably means further erosion in the cutouts and possibly additional softening in the cash cattle market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}