Beef Wrap December 01

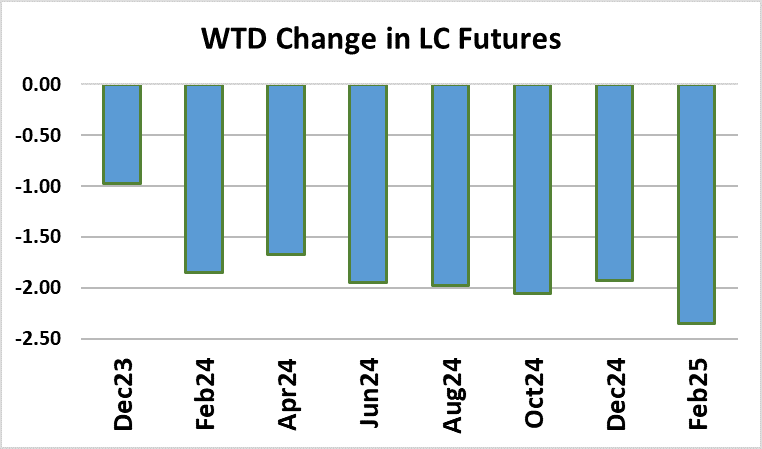

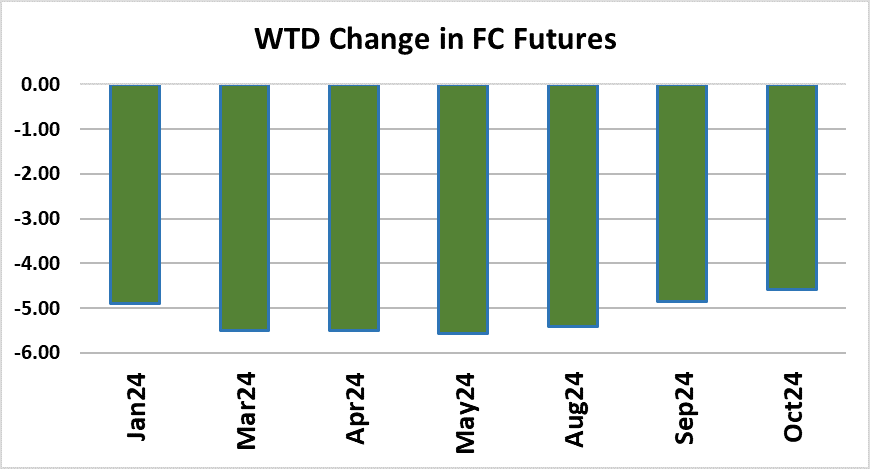

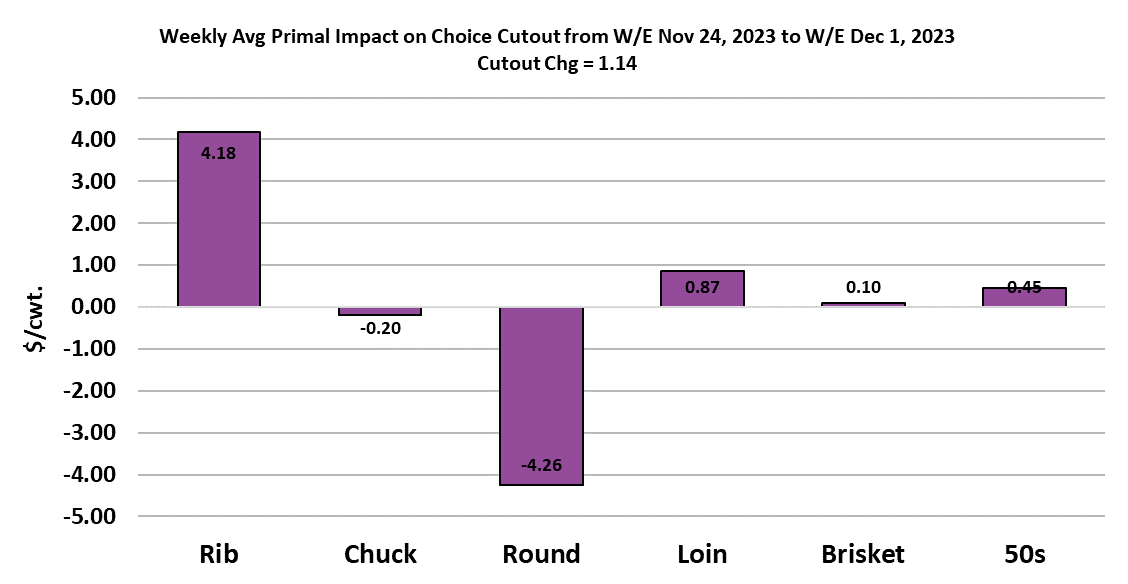

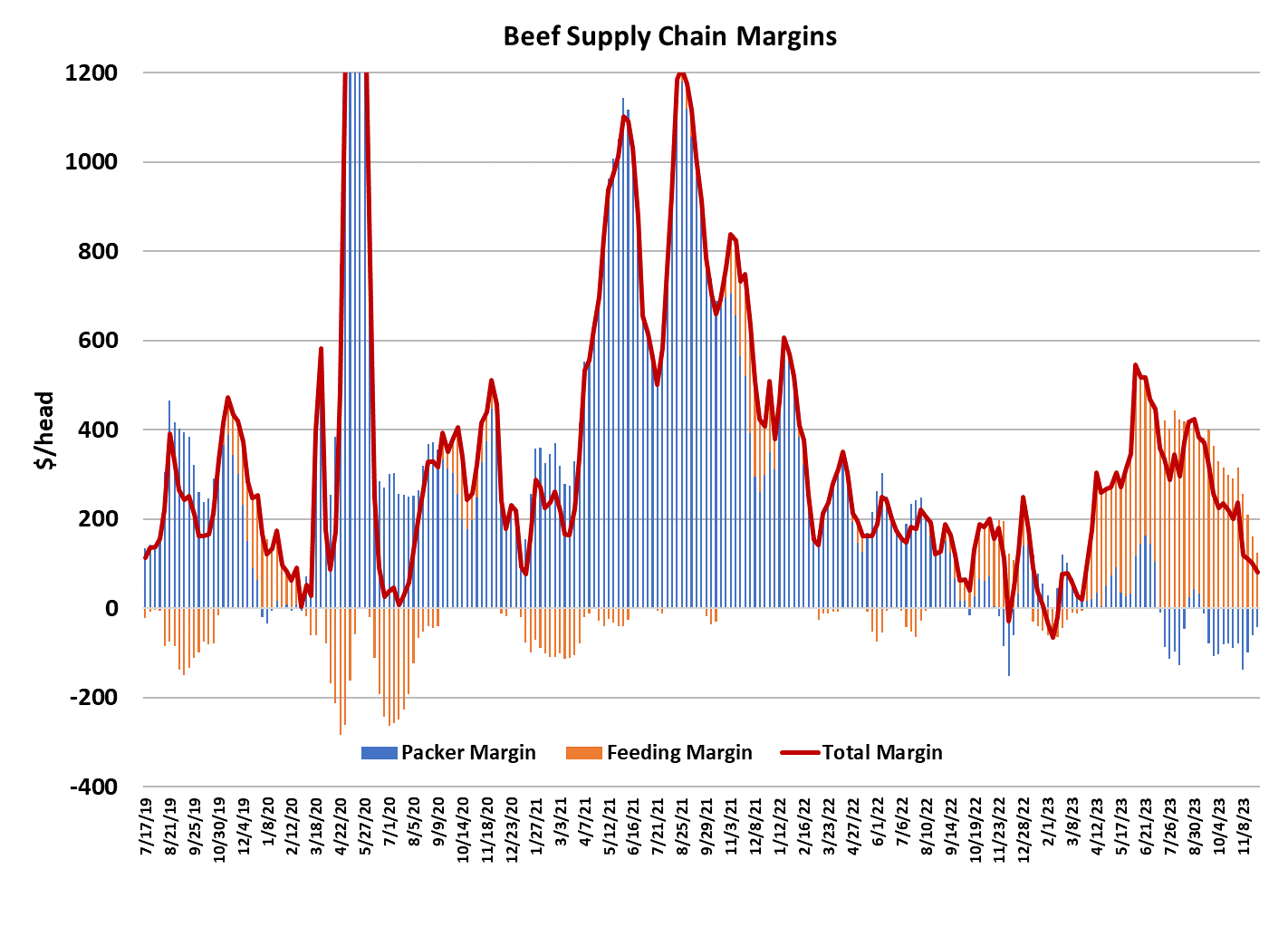

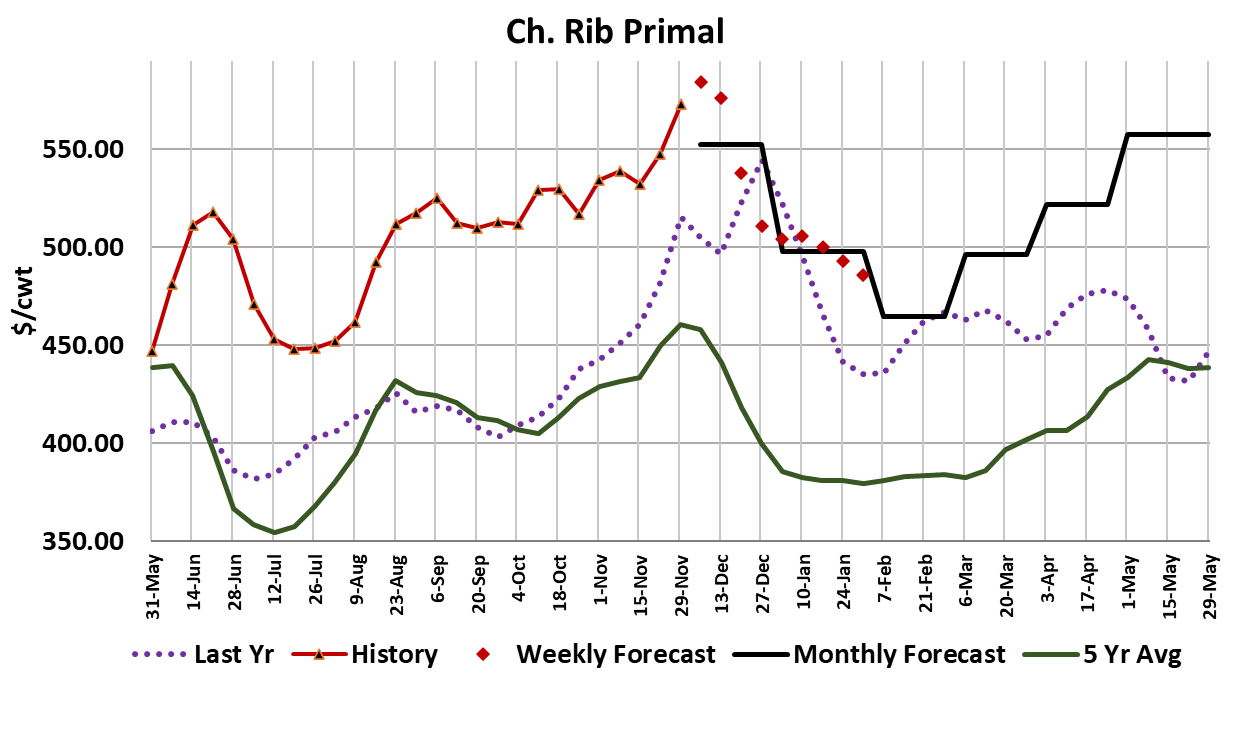

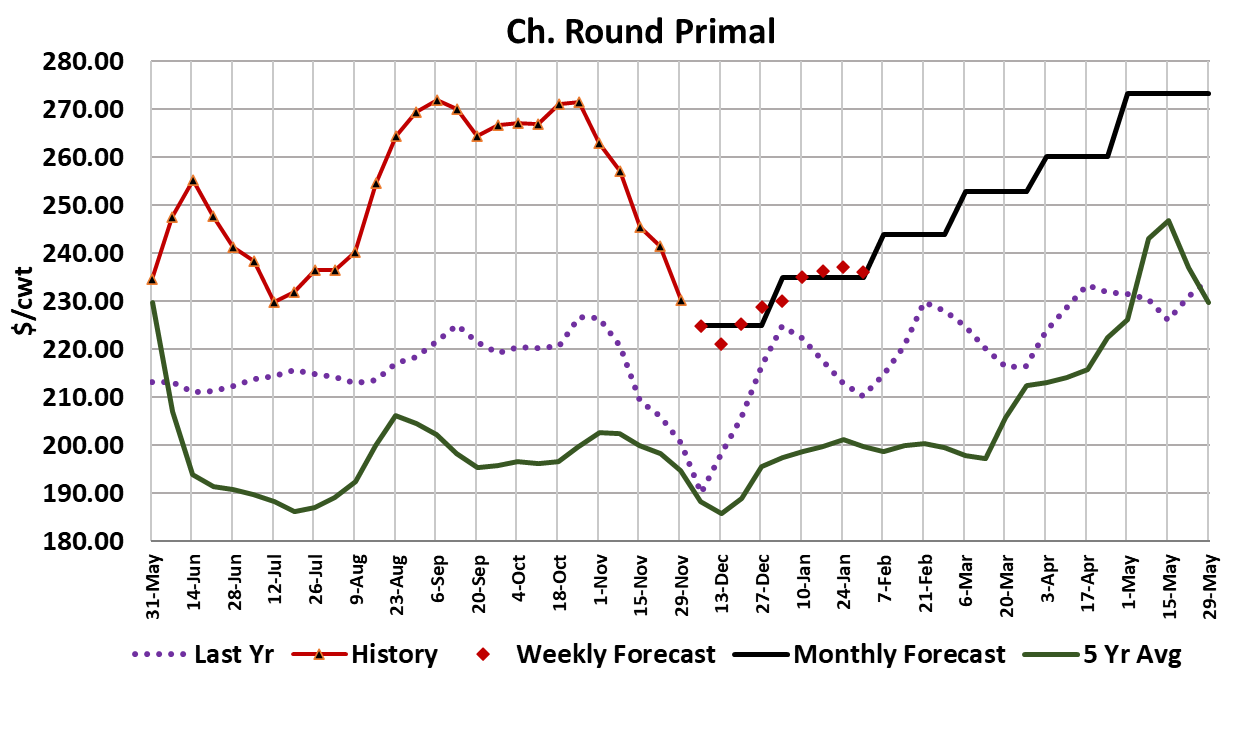

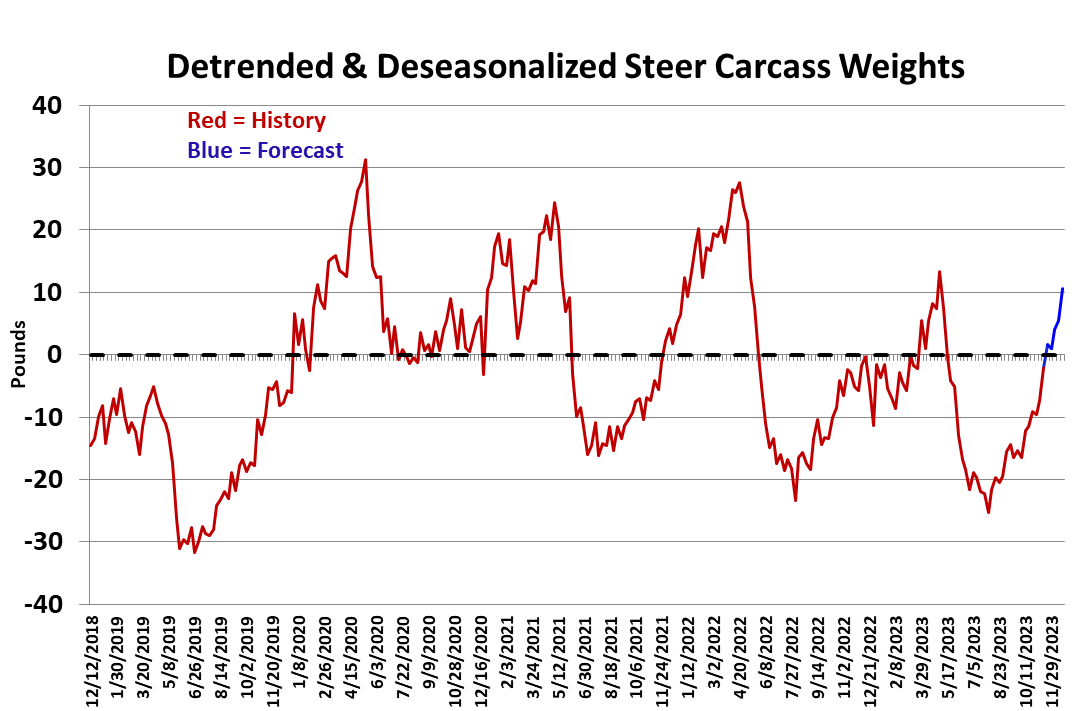

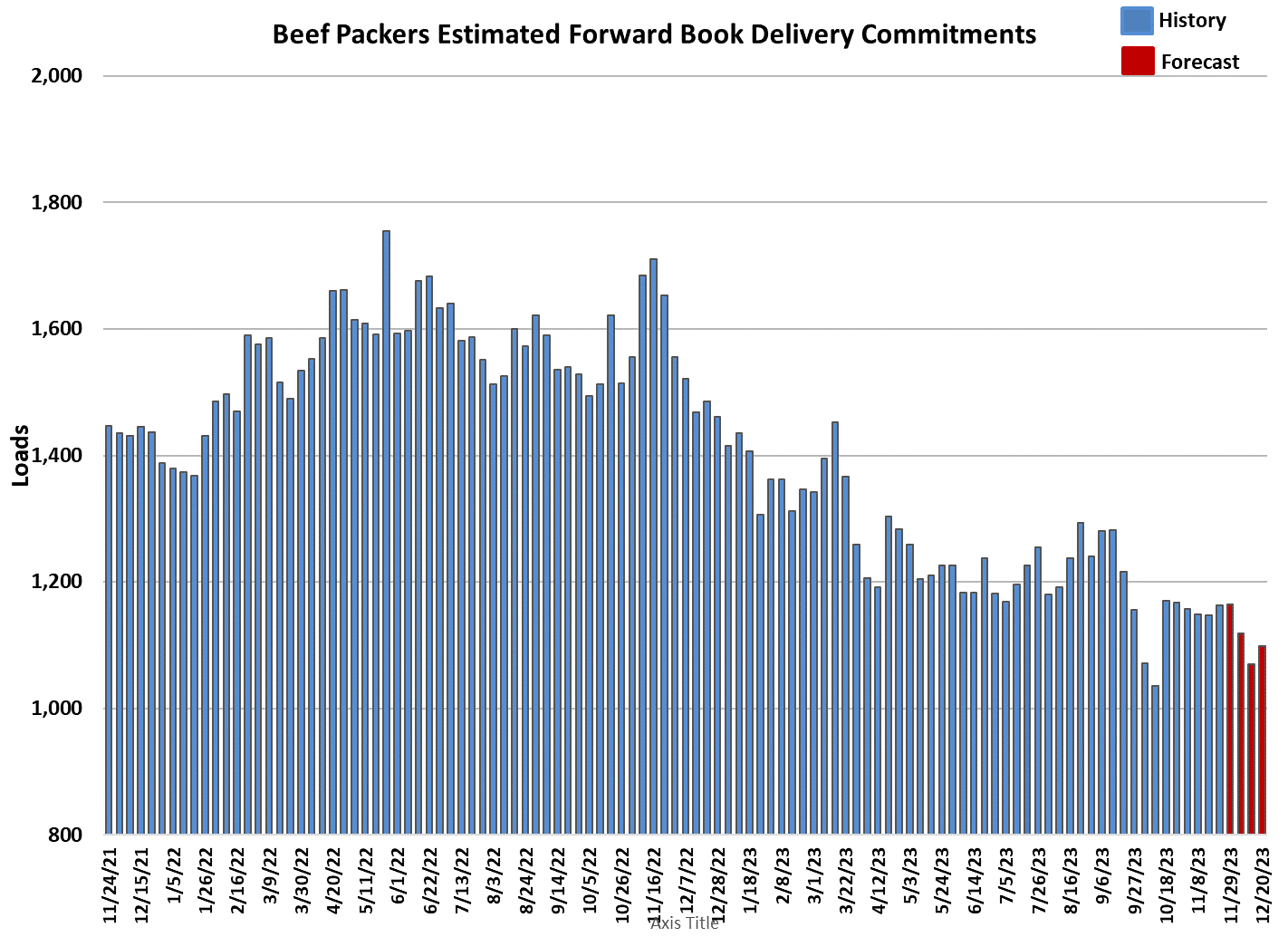

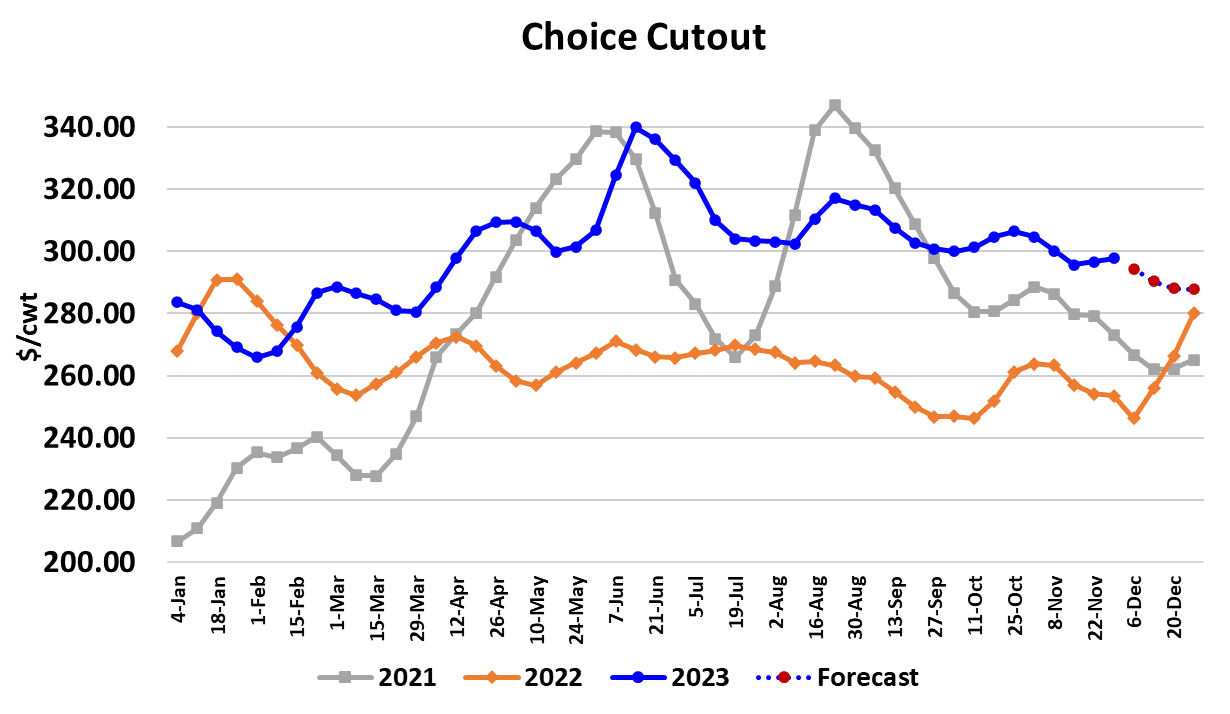

The rib primal finally came to life this week, jumping a little over $25/cwt. to average $573.27. That isn’t too far off of the all-time record high at $609/cwt. set back in September of 2021. This is a result of last-minute holiday buying and is carefully orchestrated by packers because they will be delivering formula-priced ribs in the next couple of weeks that depend on the spot rib price. Once that business is done, usually near the middle of December, we can expect rib prices to fall like a rock. That will create a problem, because nothing else is holding the cutout up. End cut prices are really struggling of late as evidenced by the attached chart depicting price for the round primal. The pattern for the chuck is very similar. Even with the big gains in the ribs this week, the Choice cutout was only able to average $297.79, up $1.14 from last week’s average. The Select cutout dropped $3.30 to average $265.70. Packer margins improved to about -$43/head from -$60/head last week, mostly due to declining cattle costs. Once the support from the ribs has run its course, the Choice cutout could fall below $290 in short order. The cash cattle trade got started on Monday at $175/cwt. when cattle feeders were thrown into a panic by another sharp decline in the futures. The futures rebounded on Tuesday, but couldn’t hold those gains later in the week. There were some cattle that changed hands at $174 and it looks to me like the average for the week is going to come in close to $174.40. The fat margins that cattle feeders have been enjoying since the spring are rapidly dissipating. In fact, if the packers can push cattle prices just $1 lower next week, that will be all it takes to put cattle feeding margins into negative territory. The combined margin chart is still trending lower and may make a run at the zero line before the end of the year. That suggests that overall beef demand is softening despite how strong the rib market seems right now. It feels as though demand for the lower-priced beef items like end cuts and fat trim is struggling a lot more than demand for expensive, high quality middle meats. That makes the demand outlook for January and February somewhat scary because normal seasonal patterns point to sharply lower middle meat demand after the holidays. Another thing that makes January and February scary is the number of cattle that will become market ready during that time period. The flow model suggests that fed kills will need to run close to 500k per week in Jan/Feb in order to keep cattle from backing up. Kills are below that level now, when demand is much better than it will be early next year. So, I can envision a scenario where Jan/Feb demand is only strong enough to support fed kills in the 470-480k range and when packers throttle back to that level, it could cause cattle to back up in feedyards pretty quickly. There is already ample evidence that feedyard currentness is slipping with steer carcass weights being reported higher again this week and the de-trended and de-seasonalized carcass weights rising rapidly. The forecast for the DTDS weights would have them at +10 pounds by the end of the year. That is a screaming sign that marketing rates are too slow for the amount of cattle coming down the pipeline and when beef demand downshifts in January, we could be looking at a train wreck in the cattle market. In the near-term, packers are only going to kill enough cattle to cover their holiday middle meat orders because they are struggling to move all of the end cuts that are produced in the process. The attached chart gives an estimate of the forward booked deals that need to be delivered on between now and Christmas (derived from the weekly Comprehensive Beef report). It isn’t a big number. Another thing that the chart makes pretty clear is that forward booked business has been in steady decline since fall of last year. Beef buyers have been less and less enthusiastic about booking forward in this high-price environment. All of this paints a pretty dismal picture for Q1 of next year, both in the beef market and in the cattle market. Futures traders have been sniffing this out and that is why the bears have been the big winners in the market lately. Most of the deferred live cattle contracts lost close to $2 this week, but the feeder cattle futures were hit even harder, with losses in the $5 area. This is not a very good environment for bottom picking because the bottom may still be a long way off. Of course, this is a short-term bearish situation in a longer-term bullish environment due to the ongoing liquidation of the cattle herd. As the front end of the futures curve comes down to deal with the near-term bearish fundamentals, it will likely drag the deferred contracts way too low and once this short-term problem clears in a few months, it may lead to a strong upward re-pricing for contracts settling in the second half of next year. Time will tell. One thing is certain however, this downdraft in live and feeder cattle prices is not going to encourage much herd rebuilding. In fact, it may accelerate the liquidation to a modest degree. I continue to think that the liquidation phase of this cattle cycle will last longer than normal and we might not see herd rebuilding until 2025 or 2026. For the next couple of weeks, it will be all eyes on the ribs looking for signs that the holiday business is coming to an end. The cutouts probably drift a little lower in the near term and cash cattle prices will remain vulnerable.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}