Beef Wrap November 12

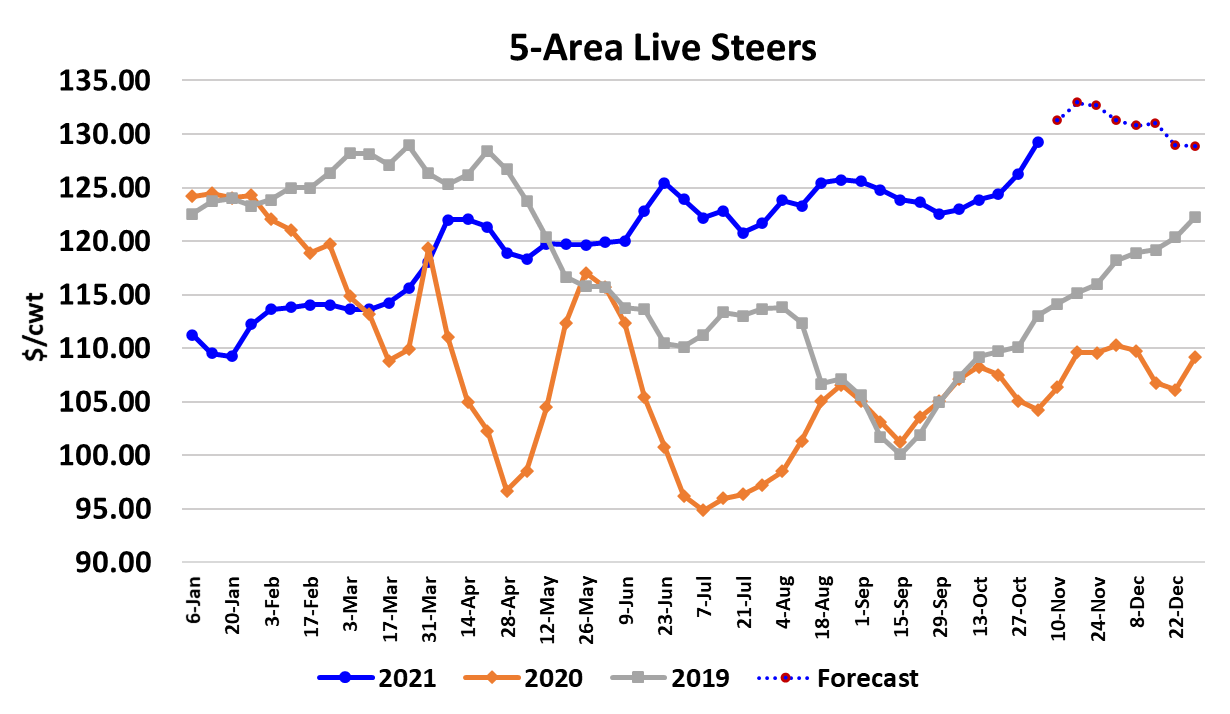

This week the cash cattle market moved up $1-2 over last week and

movement was pretty brisk. It looks like the weekly average is going

to finish somewhere around $131.50. While cattle prices were busy

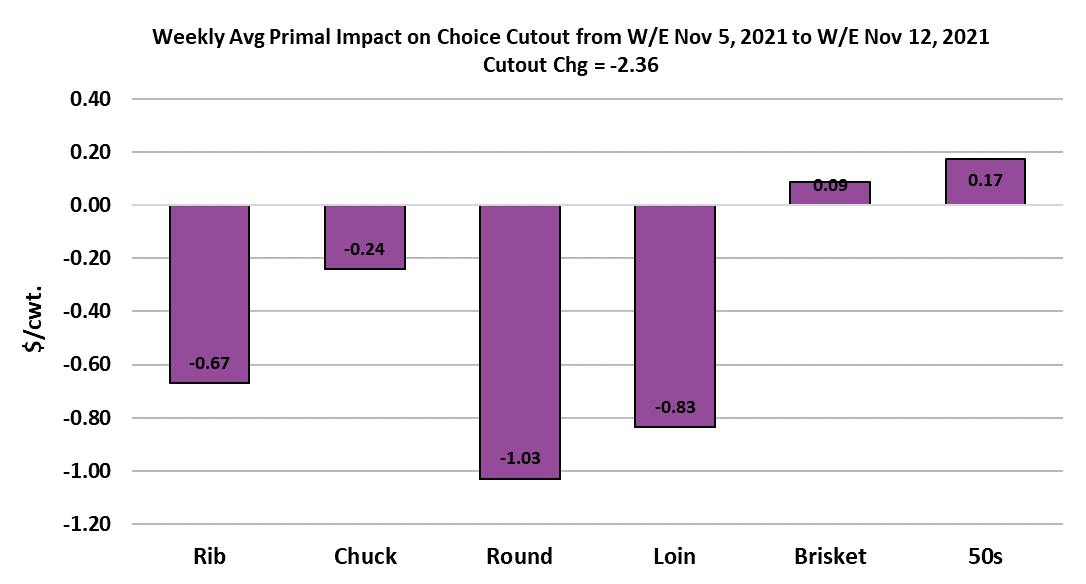

advancing, beef prices were slipping. The Choice cutout dropped

$2.36 on a weekly average basis and the Select was up $1.74.

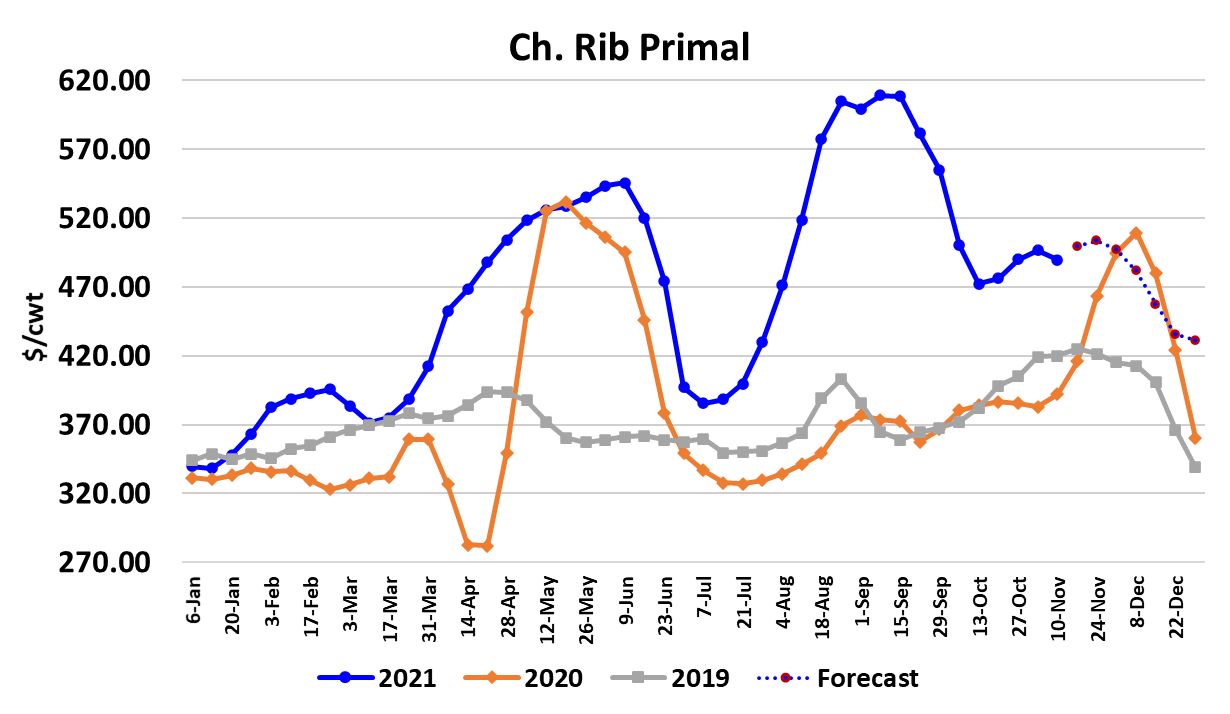

Perhaps the most important news there was that the rib primal failed

to advance this week. The rib primal finished the week down almost

$7. Over the past 20 years, there have only been three instances

where the rib price declined between the first and second week of

November and in two of those cases the drop was less than $1. The

average week-to-week increase was over $5.

In all three years where rib prices declined in early November, they

eventually moved higher into December. In fact, the average price

increase from the second week of November to the second week of

December over the past 20 years has been $25 (and I’m excluding

last year’s $117 increase). So, the evidence seems to suggest that

rib prices will advance from here over the next few weeks. I am still

keeping a small increase in the forecast, but must admit that it doesn’t

seem like a sure thing in this environment. However, the rib wasn’t

the only primal to blame for this week’s setback in the cutout.

Chucks, rounds and loins were also softer. Perhaps consumers are

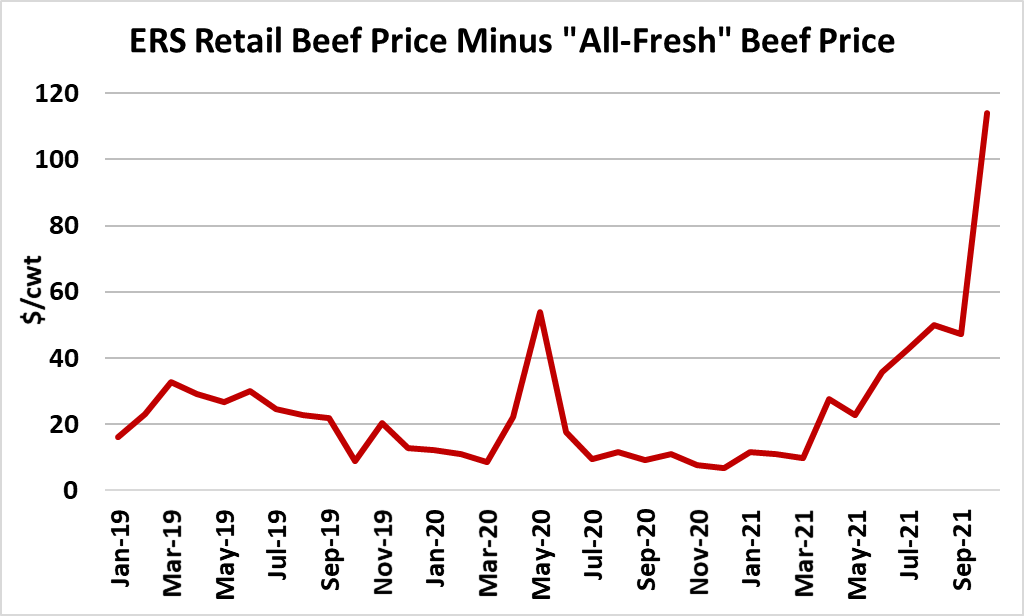

starting to balk at high retail prices. USDA released its retail price

data for October this week and the traditional retail beef price was up

about 0.4% (a new all-time record). However, the “all fresh beef”

price was down 8.6%. The difference between these series is that

the all-fresh beef data takes into account feature pricing and thus

better reflects the mix of items that consumers are actually buying.

The regular retail beef price is simply the price of the same set of cuts

month after month and it is the data used in the CPI calculation.

This recent data seems to be telling us that retailers are keeping their

everyday beef pricing elevated and consumers are buying more

lower-priced items on feature than they did this summer. That seems

to fit with the idea of eroding beef demand at the consumer level.

The chart below shows how exceedingly wide this spread was in

October. Also note the spike back in May, 2020 as the pandemic was

unfolding and unemployment was soaring. That spike was an alltime record before the October data was released. It seems to me

that the evidence keeps mounting that beef demand is slowly pulling

back. On the supply side, this week’s fed kill came in at 511k, up 6k

from last week. It seems as though packers are only willing to push

the kill as far as needed to cover existing orders because over-killing

at this point is only going to push cattle prices up and beef prices

down. I calculate this week’s packer margin at about $680/head,

down about $50 from last week.

In the near-term, I don’t see packers getting cattle bought cheaper

and the cutouts probably don’t have much upside potential, so it is

logical to expect margins to continue lower. If beef demand really is

slipping lower as I suspect, then packer’s first response to that should

be to limit the kill so that it doesn’t do too much damage to the

cutouts. The problem is that they probably can’t cut the kill much

beyond current levels and without risking shorting someone on their

holiday middle meat orders. However, many users put ribs into

suspended fresh programs back in late summer and there is a very

good chance that those ribs will end up costing them more than if

they were buying them in the spot market today. Oops.

Product booked in advance for holiday delivery was probably sold at

prices well above today’s level, so they will want to make sure those

orders get delivered. At this point, packers must feel a bit trapped

(and they are), but as soon as they feel like they can cut the kill, they

probably will in order to slow their margin erosion. They can always

use the “tight labor” excuse to reduce the kill. Steer carcass weights

were reported up 2 pounds this week, but it may be that the top in

weights has already occurred. There are no signs of inclement

weather for cattle country in the near future. Post-Thanksgiving, look

for weights to slowly work lower but if packers slow down the kill then

that could keep weights elevated a bit longer than expected. Next

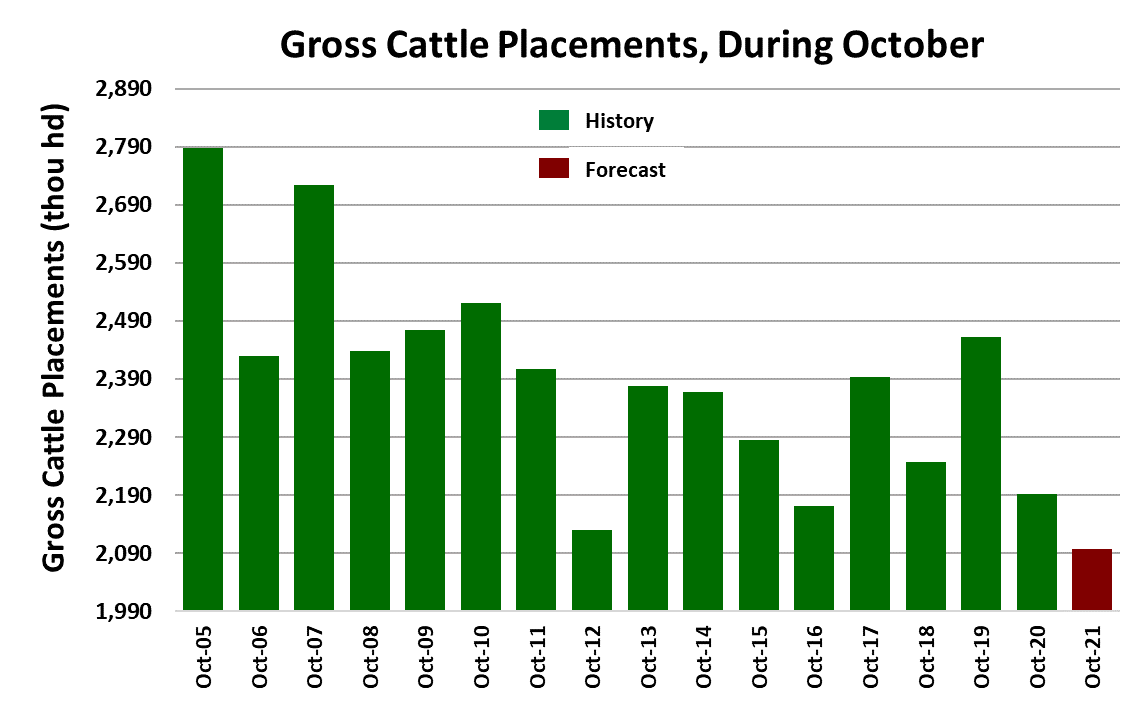

week, USDA will issue a Cattle on Feed report and I’m expecting it to

show October placements down 4.3% YOY. October is normally the

largest placement month of the year, so a 4-5% decline amounts to a

relatively large number of cattle that might go un-placed. I expect that

I will be near the low end of analysts’ estimates for placements, but

cattle feeders really do need to scale back placements if they want to

capture more margin from packers. That is especially true if beef

demand is in a long term trend lower.

Futures traders seemed to shrug off the higher cash trade this week

as the Dec contract was up only marginally on the week. I think

traders are seeing this current cash market strength as just a shortterm bump higher supported by a transitory tightness in the cattle

supply coming at just the right time when packers have orders to fill.

With 3 major holidays on the horizon, there will be plenty of

opportunities for packers to slow the kill in order to keep a lid on cattle

prices. Plus, with the Dec futures price nearly even with current cash,

there is no incentive for cattle feeders to hold back cattle. Next week,

look for the cutouts to be about steady with the middle meats perhaps

a bit higher and the end cuts a bit lower. Buyers won’t be aggressive

because we are leading into Thanksgiving week when hams and

turkeys will be dominant.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}