Beef Wrap November 26

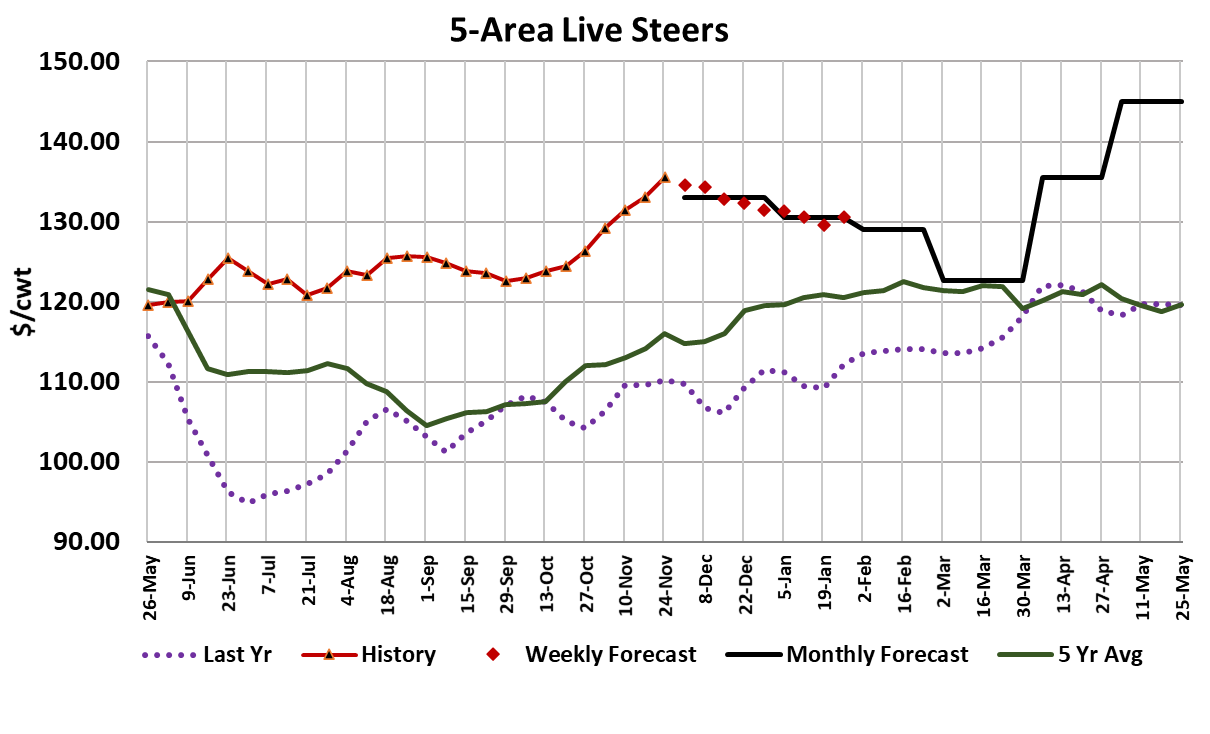

The cash cattle market continues to march higher while the beef

market slips lower. Last week’s average price for cash cattle was a

little over $133, up $2 from the week before and so far this week,

packers have come out bidding $135 to $137. Cattle feeders have

packers over a barrel and they know it. Over the past seven trading

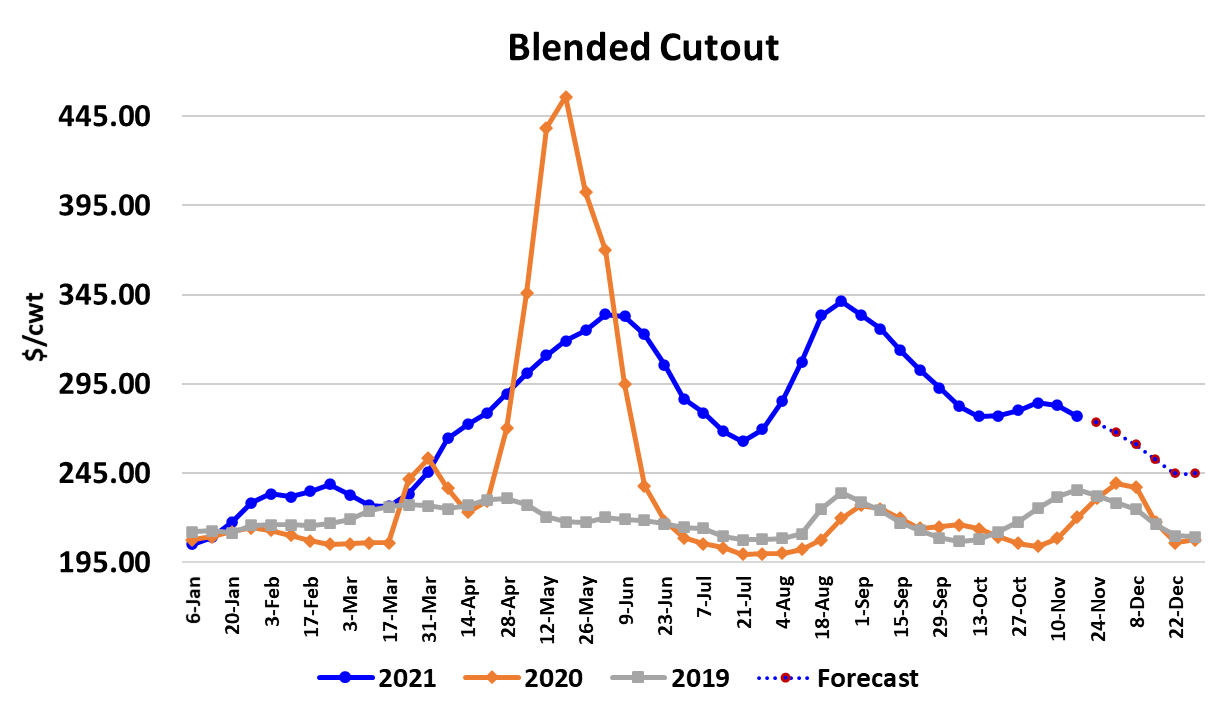

days, the Choice cutout has slipped $4.51 and the Select is down

$4.61. As beef pricing falls and cash cattle rockets higher, packer

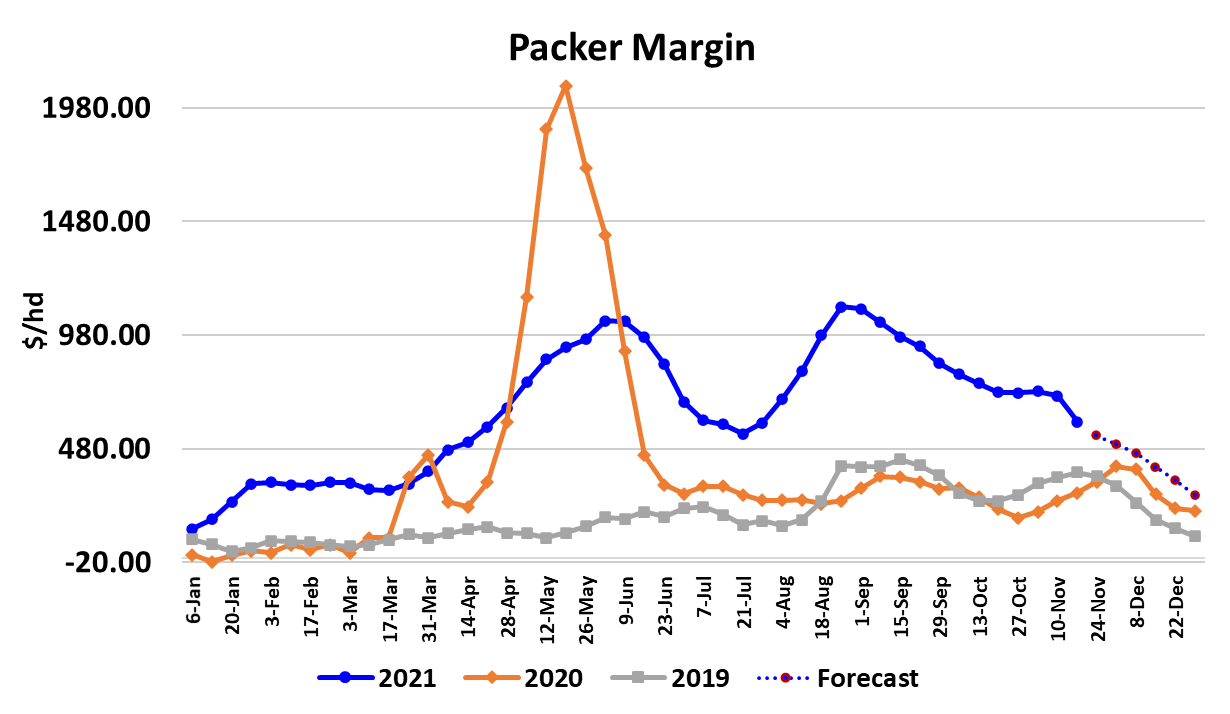

margins are compressing rapidly. Last week’s margin averaged just

under $600 per head and it looks like margins this week will be down

another $70 to $530/head. I fully expect packer margins to be below

$500/head next week when those $137 cattle start to show up for

slaughter. At the moment, packers are not really fighting back and

have just accepted that they need to pay up.

That is likely in their best interest because they have some highpriced orders that were booked back in Aug/Sep and it makes sense

that they not short those buyers. Soon however, those orders will be

in the rear view mirror and packers are more likely to resist higher

cattle pricing. Part of the problem in forecasting this market is no one

really knows what a “normal” packer margin is anymore. Prior to

2018, a normal November margin would have been in the $40-100/

head range, but in the last couple of years margins have averaged

around $335/head in November. If we were to use that as a guide,

then cash cattle could move into the mid $140s before margins fell to

$335/head. Is that where we are going? Cattle feeders seem to

think so, but futures traders are not yet ready to sign up for that. For

one thing, it is likely that future margin compression will come from

lower cutouts not just higher cattle prices. I’ve got the Choice cutout

working back toward $250 by the end of the year. If that comes true,

then cash cattle at $130 will generate a margin of only $275/head.

Further, once the holiday orders are filled, packers can scale back the

fed kill in order to cool off the cash cattle market.

The holidays will give them some cover to reduce the kill and I’m sure

that their workforce will greatly appreciate a less demanding schedule

in December. Kills have been large recently, with last week’s fed kill

registering 530k, which is well above what the flow model projects to

be available at this time of year. When packers want to over-kill the

cattle supply, they create a situation where cash cattle prices can rise

and feedyards get more current. With the Thanksgiving holiday right

upon us, this week’s fed kill may only be about 450k, so that will

provide some relief. After Thanksgiving, I expect packers to be less

aggressive and thus the fed kill could move back down into the

510-520k range. Carcass weights are near a seasonal top and will

soon start trending lower.

That will help tighten up the beef supply and thus provide some

support for the cutouts in January. The DTDS weights aren’t

signaling that feedyards are super-current, but they are well above

the lows that were made in late summer. Since feedyards aren’t

super-current and beef demand is easing, I believe that this rally in

the cattle will be short-lived and cash prices will be lower at the end of

the year than they are today. Time will tell. The chart below indicates

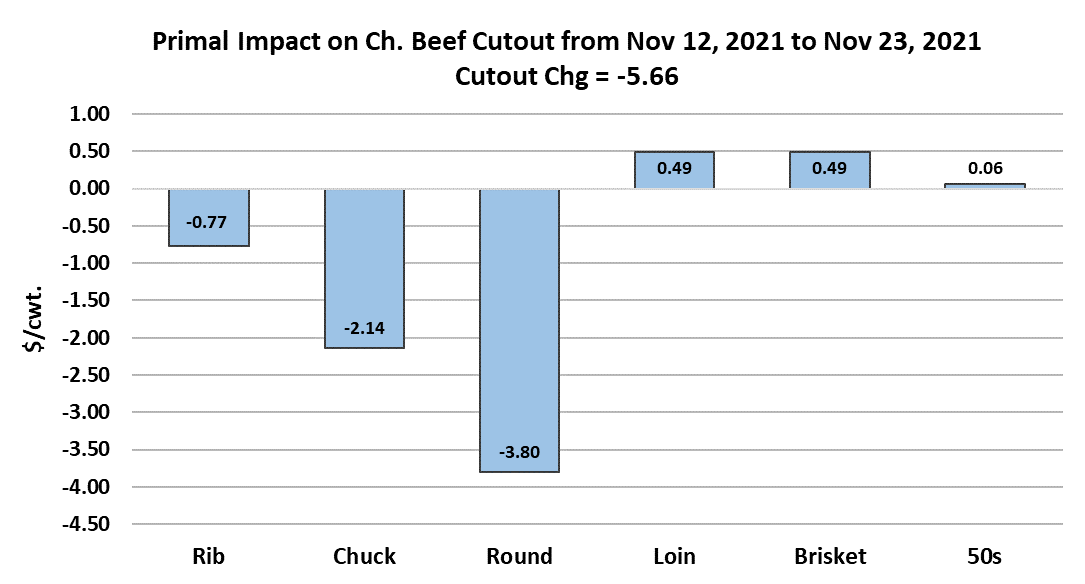

that the weakness in beef prices has been concentrated in the end

meats and the ribs to some degree. The ribs have failed to rally

ahead of the holidays and are now living on borrowed time.

By the second week of December, ribs are likely to be moving lower

in big chunks. It could happen sooner than that. End meats might

garner a bit of support between Thanksgiving and Christmas as

retailers look to offer consumers something different from the usual

holiday fare. Still, I don’t think that the ends will provide enough

support to keep the cutouts from moving lower once the ribs start to

break in earnest. The scatter diagram below gives the November

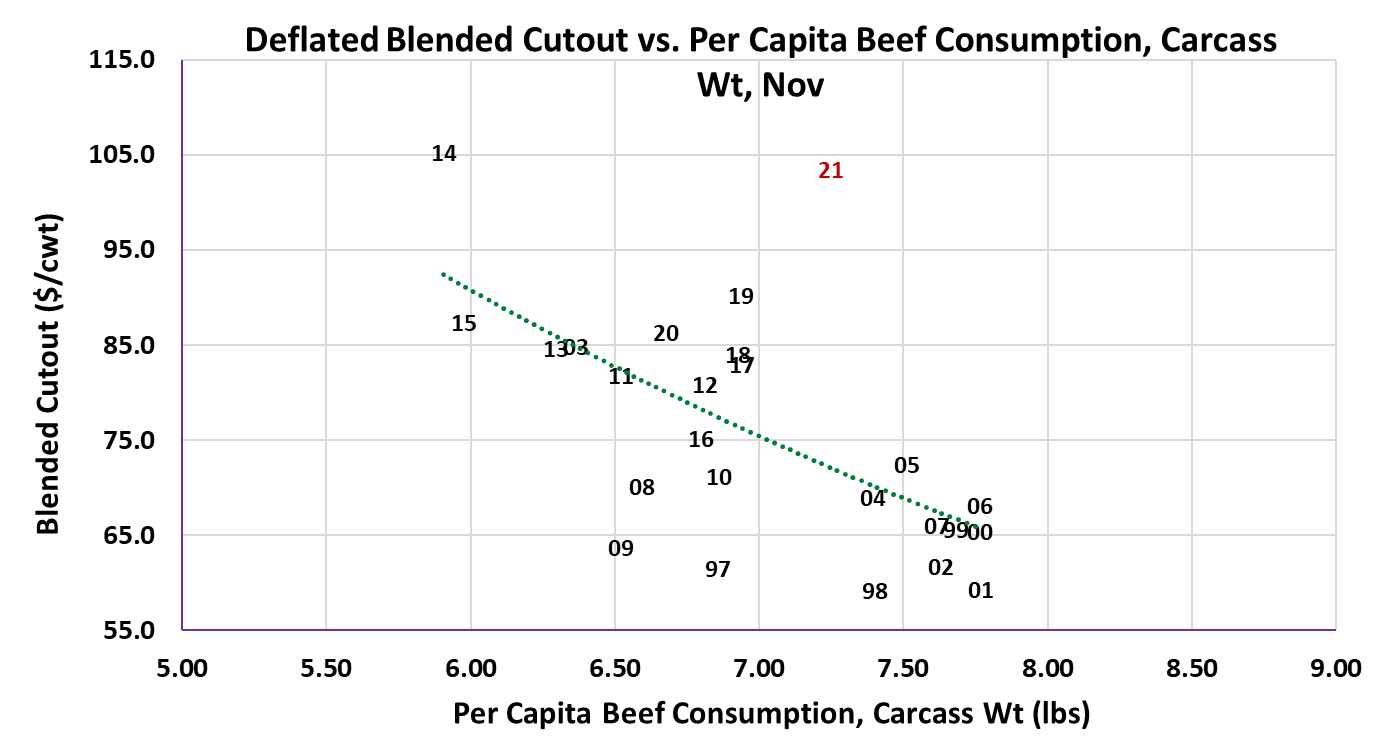

demand curve, with the cutout deflated using the CPI. As you can

see, the Nov21 data point is still exceptionally high, indicating very

strong domestic beef demand persists. The combined margin chart

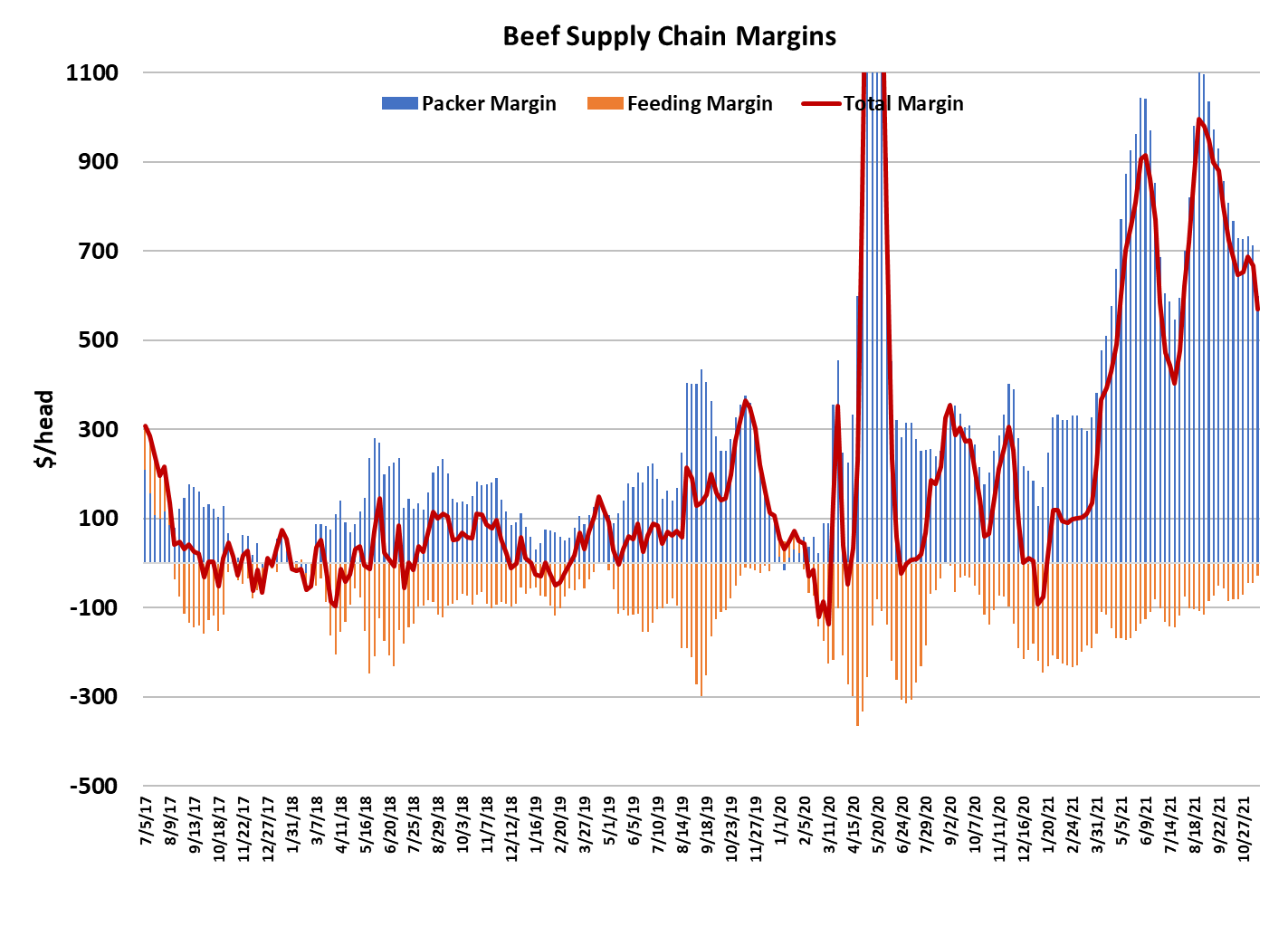

also suggests strong, but declining, demand. In the old days, it used

to be common for the combined margin to reach the zero line, but it

hasn’t been anywhere near zero since the arrival of the pandemic.

My guess is that it will continue to move lower, but won’t be near zero

any time soon. COVID infections in the US are starting to rise again

and with holiday gatherings just ahead, that trend is likely to continue.

We know from past experience that rising infections have been good

for beef demand, but with almost 2/3rds of the population fully

vaccinated and boosters widely available, rising infections won’t

generate the same stay-at-home mentality that it has in the past and

thus probably won’t boost beef demand to the same degree that it

has in the past. Last week’s Cattle on Feed report showed October

placements up 2.4% YOY and total on-feed inventories nearly equal

to last year, so there isn’t a shortage of cattle. Soon, the industry will

transition out of the near-term cattle supply tightness that was created

by small placements back in May/Jun/July and that will also help

keep cash cattle prices contained.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}