Beef Wrap November 18

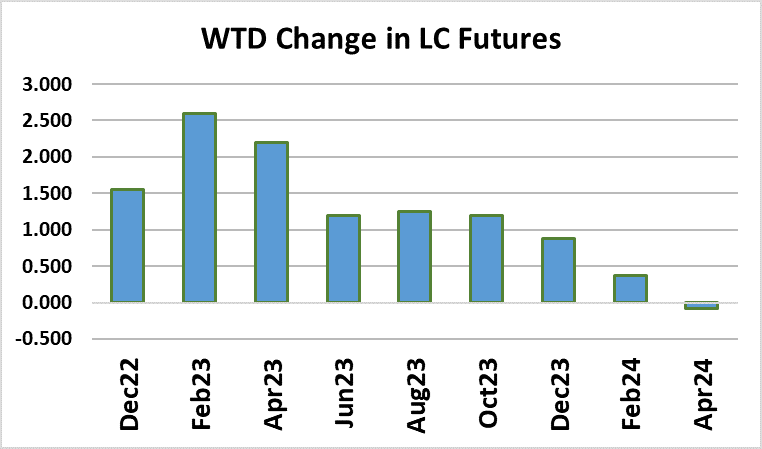

If one was to only look at the LC futures board this week, they might come to the conclusion that this was a good week for the cattle and beef complex. The reality is not so much. While the Feb futures was busy adding $2.50/cwt, the Choice cutout lost $6.20/cwt. and the Select cutout was down $3.68/cwt. The cash cattle market averaged $152.68, almost identical with last week’s average. So why did the futures get so excited? Futures actually moved lower early in the week and the bulk of the rally occurred in the last three days. I think most traders expected that, because packers would need to buy less cattle than usual because of the upcoming Thanksgiving holiday, that cattle prices might soften. When it became clear that cattle feeders weren’t going to take less money in a week before a major holiday, that was read as a bullish sign by traders. But, as you might guess, paying steady money for cattle when the cutouts are dropping like a rock doesn’t bode well for packer profitability. They were already operating on a small margin, but I think this is going to be enough to push their margins into the red next week.

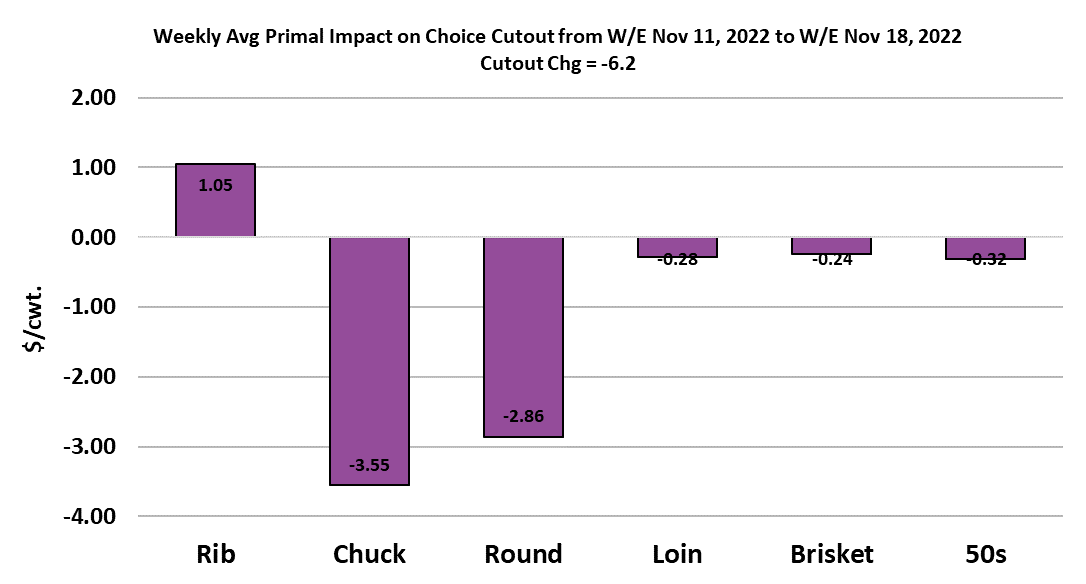

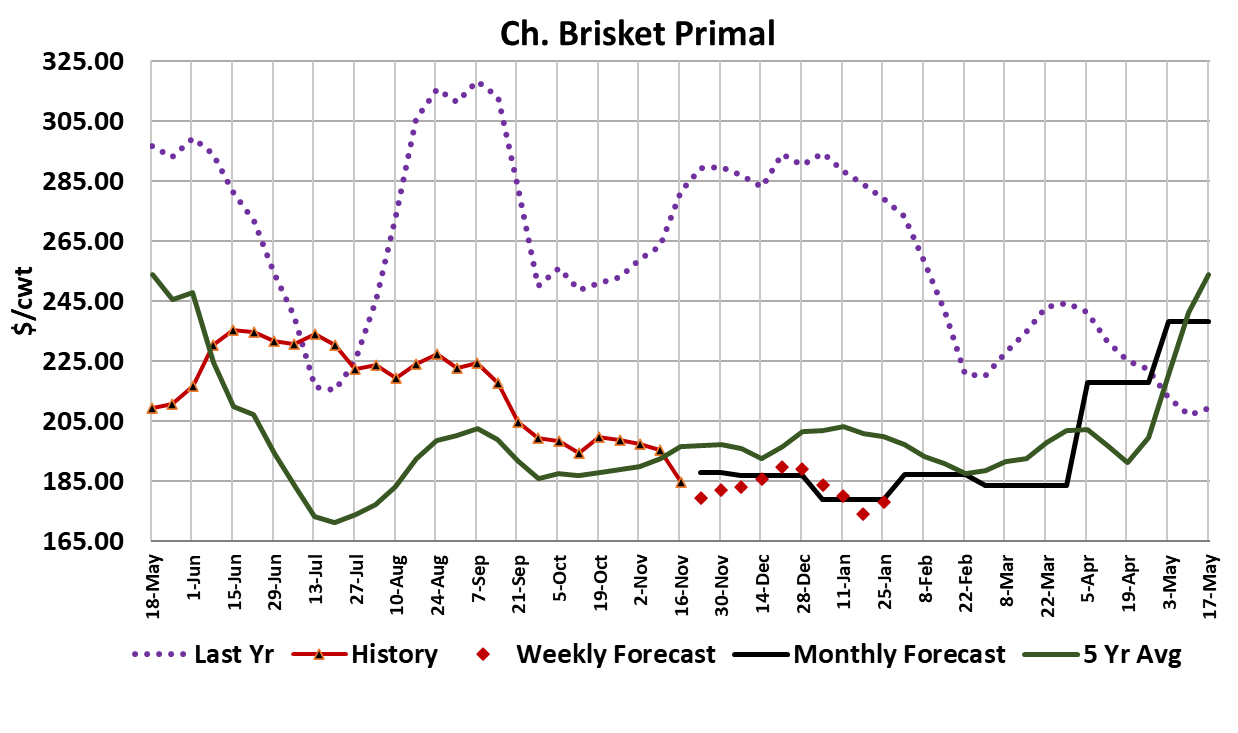

It is a really strange situation for this time of year. Normally in the week before Thanksgiving, the cutouts are moving quickly higher spurred on by strong middle meat interest, and packer margins are improving. And indeed, the middle meats, or at least the ribs, are moving higher in normal seasonal fashion. The problem is that prices for the rest of the carcass are heading south fast. The round primal lost $11/cwt this week and the chuck primal lost $12/cwt. Briskets lost $10/cwt. These are big chunks of meat and make up a large proportion of the cutout. Even the 50s averaged $6/cwt. lower this week. Literally, the only thing going up is rib prices. That isn’t enough to support the cutouts and interest in the ribs is going to fade quickly after another couple of weeks. Worse yet, the Choice-Select spread is moving lower, averaging just under $25/cwt. this week and that has a negative impact on packer margins because way more Choice beef is produced than Select.

Of course, it could be possible that this week’s awful showing by the end meats is simply due to retailers (and their customers) focusing on the Thanksgiving week ahead and realizing that almost no one is going to be looking for a chuck roast in a week when ham and turkey dominate. Once the hams and turkeys have been cleared, then perhaps retailers will develop a stronger appetite for end cuts. Time will tell on that one, but packers can’t be feeling very good about the way things are shaping up so far.

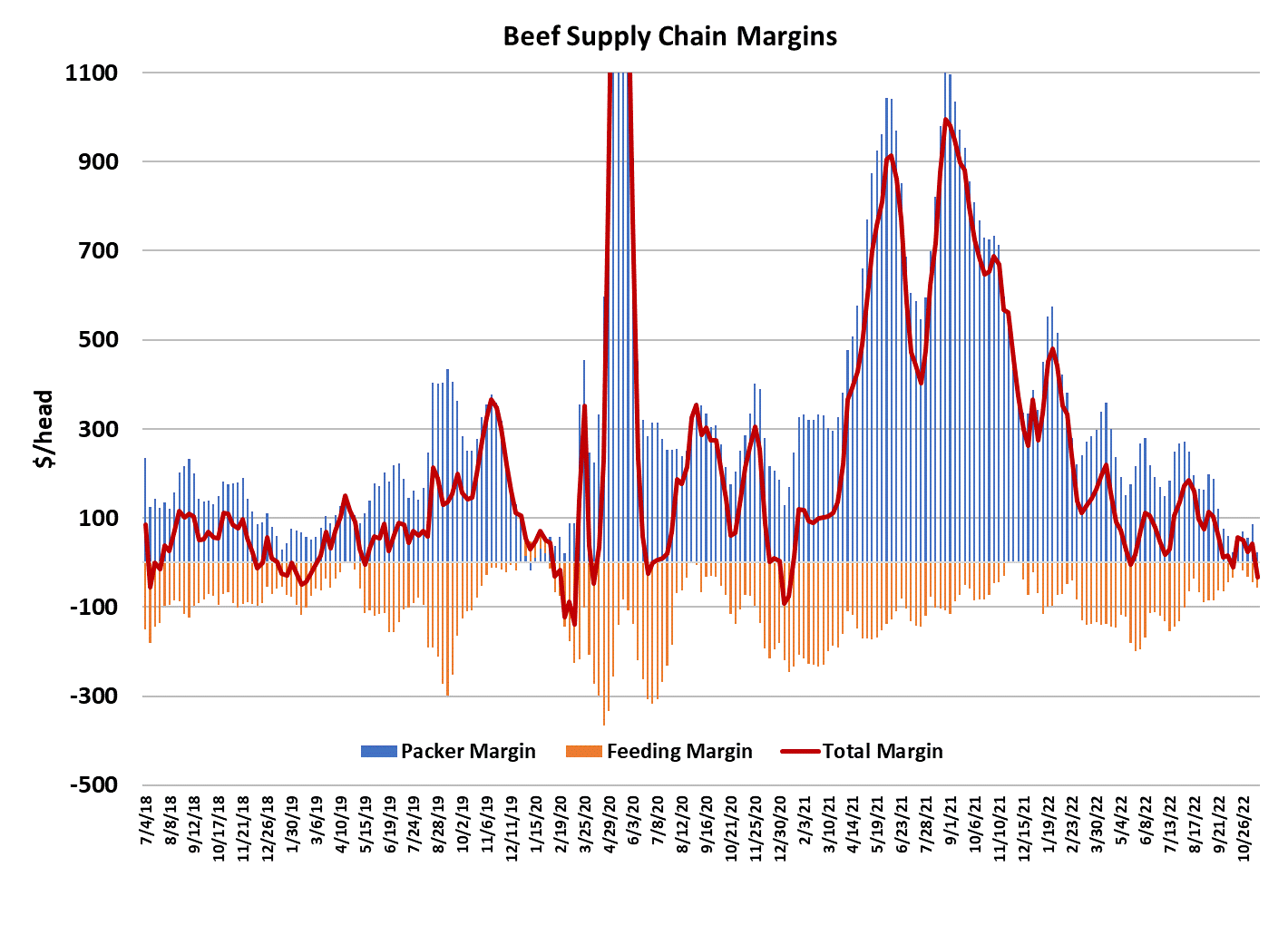

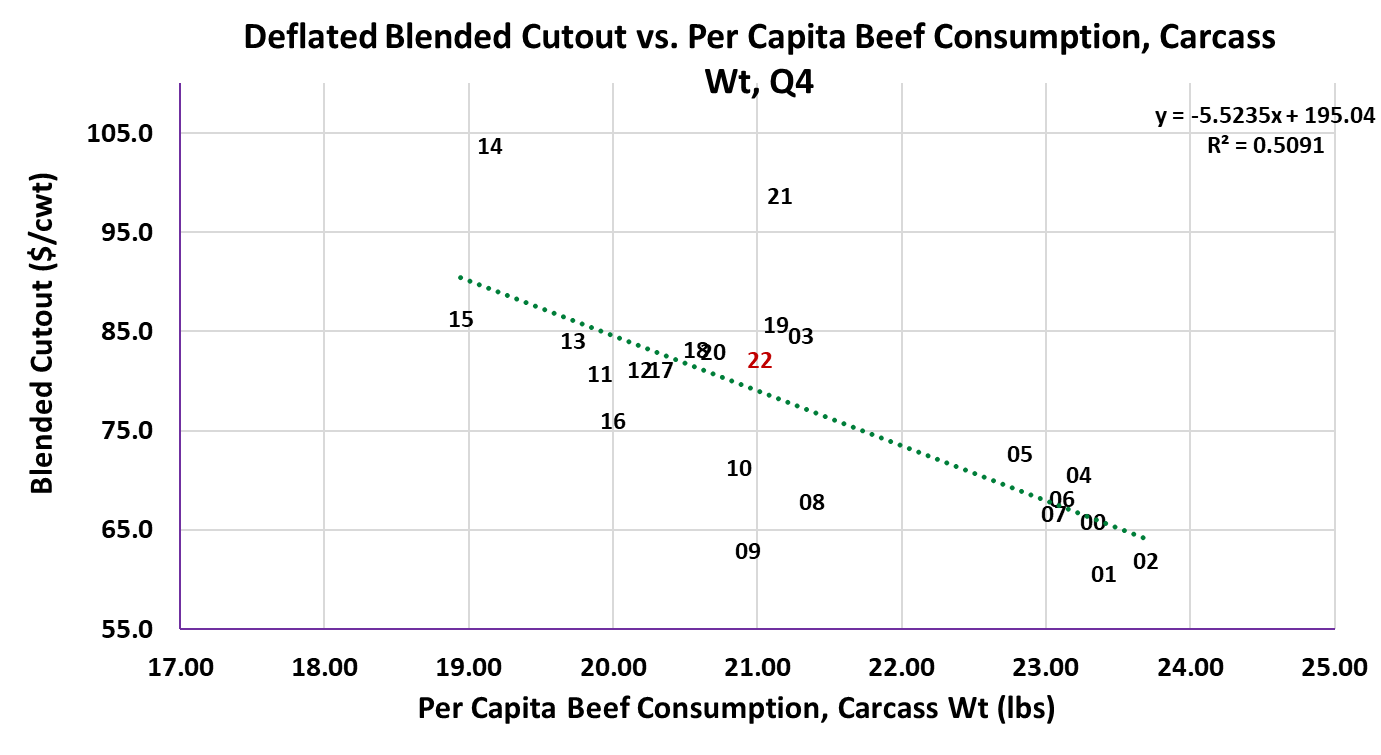

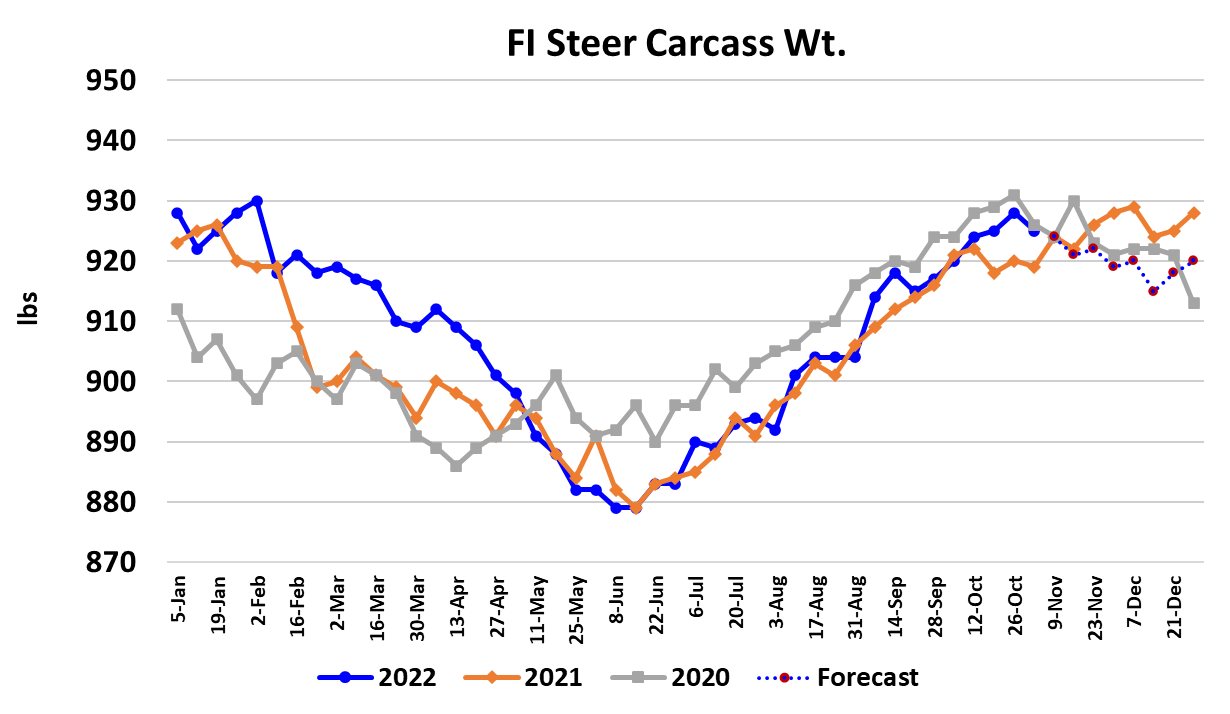

I calculate this week’s margin at $23/head and expect that next week it will be below zero, unless the cutouts take an unexpected turn higher. It is quite possible that the fall top in the cutout has been made and it will work lower through the balance of 2022. Notice that the combined margin took a sharp turn lower this week. The last three “cycles” in the combined margin have been very weak on the up-move and very strong on the downswing. That doesn’t inspire a lot of confidence in beef demand moving forward. Note also the demand scatter for Q4, which shows 2021 and 2022 at nearly the same per capita consumption, but 2022 much closer to the regression line. That scatter is calculated using deflated prices, so it accounts for the impact of inflation. This week’s fed slaughter came in at 515k, about the same level as the prior two weeks. Next week should see the fed kill dip down to 440k as all packers will be dark on Thursday. However, they will likely come back the following week with a 520-530k kill to help make up for lost production. Packers are probably making delivery this week on the biggest portion of their forward book and the amount of product committed in the weeks to follow should decline. That would make it easier for them to cut the kill, which is really the only way that they are going to get their margin problem solved. FI carcass weights were reported three pounds lower this week and it looks as though the seasonal top in carcass weights has been made. Look for weights to trend lower from now until mid-April.

Feedyards seem to still be rather current although the DTDS weights have moved up over the past couple of months. So far, the weather has been very conducive to good gains in feedyards but we are now at the point in the calendar where winter weather becomes a major risk. This afternoon USDA reported October placements down 6.1% from last year and that was about 2.5% lower than what analysts were expecting. That left feedyard inventories as of Nov 1 down 2% from last year. That isn’t a huge decline, but there is a good chance that placements will continue to be lighter than last year and by the time we get to the end of Q1, feedyard inventories could easily be 5-6% below last year. It is that possibility that has kept support under the deferred LC futures. The longer-term supply picture is bullish indeed, but we need to remember that supply is only part of the price picture and demand will have something to say about price levels too. Right now, the demand picture isn’t all that encouraging. Next week, watch those end meat prices because they will likely determine the direction of the cutout. As always at this time of year, keep a close eye on the weather in the Plains states.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}