Beef Wrap May 6

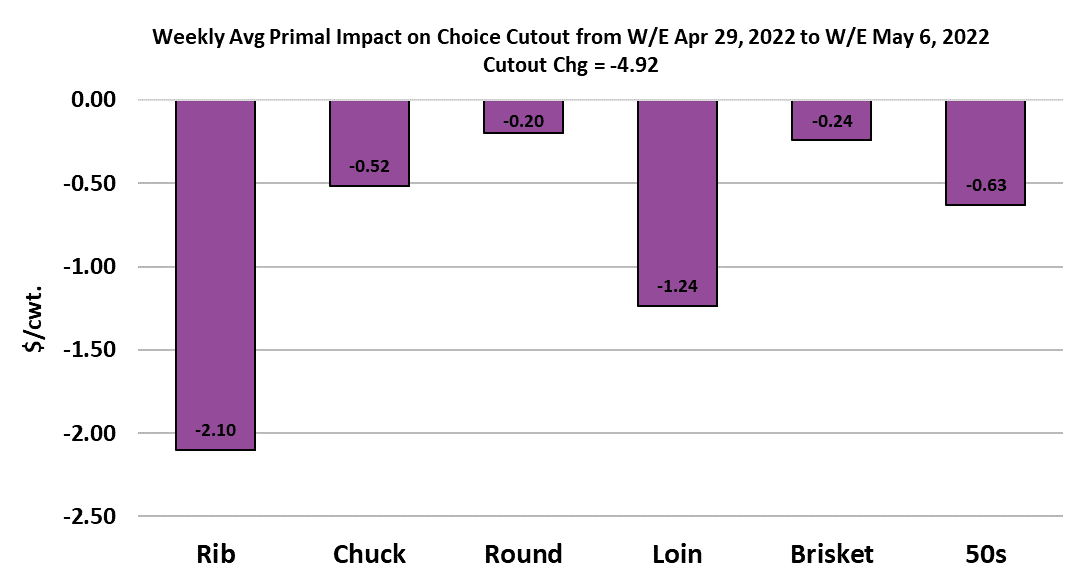

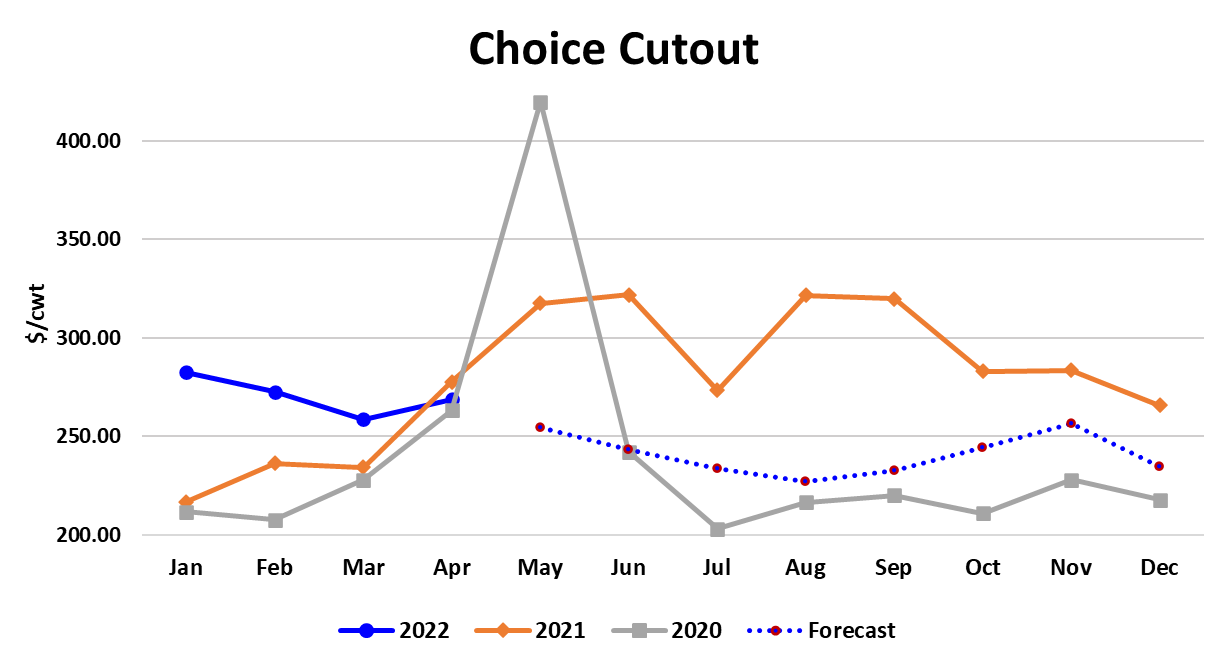

Things just keep getting worse in the beef world. The cutouts were down again

this week with the Choice losing $4.92/cwt on a weekly average basis and the

Select down $4.00/cwt. What’s worse is that the losses are being driven by

declines in middle meat pricing—a very unusual occurrence in early May. While

beef is losing value by the day, packers haven’t had any luck reducing their

cattle costs. This week’s cash cattle trade averaged $143.43, almost

unchanged from last week’s average. We still have a two-tiered market, with

cattle in the South trading for mostly $140 and cattle in the North bringing $146.

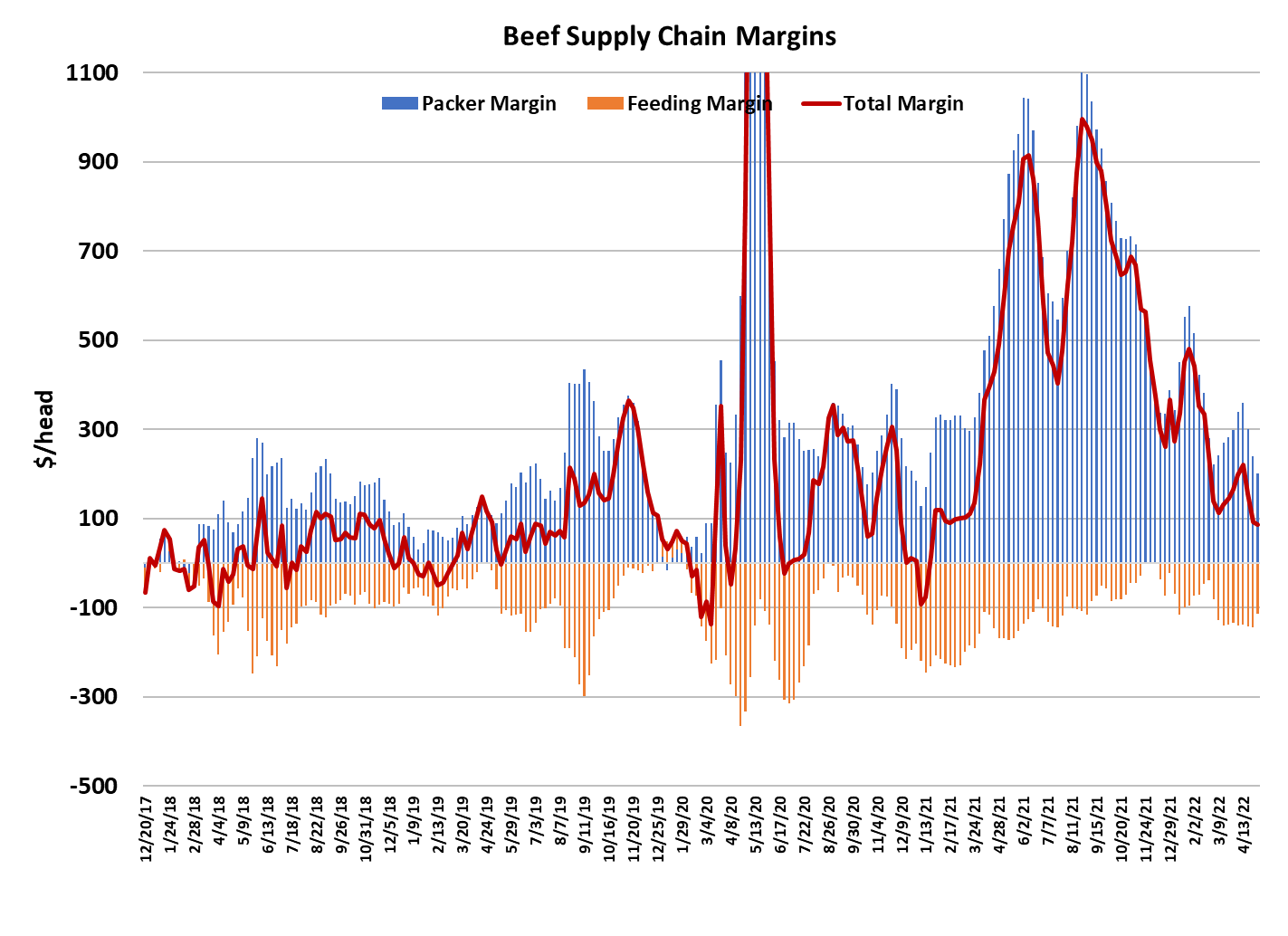

With cattle steady and beef pricing moving lower, packer margins fell again this

week and now average $193/head. The last time packer margins were below

$200/head was for a brief period in January, 2021. Keep in mind that in Jan/

Feb of this year, packer margins were running in the $400-500/head range.

January and February are normally the time of year when packer margins are

the worst and April/May is normally when they are at their best. What a strange

market situation. In most years, retailers are actively buying middle meats in

early May for the upcoming Memorial Day holiday, but not this year. The

attached chart shows that it was the ribs and loins that did the most damage to

the cutout this week.

My guess is that 2 things are going on simultaneously. First, retailers were

fearful of another high-priced spring market like they experienced in 2021 and

so they got busy earlier in the year and booked a lot of product in advance, thus

they don’t need to be in the spot market right now. Second, they are finding that

middle meats are not moving very well out of the meat case. It isn’t unusual for

retailers to cancel orders if the product isn’t moving for them. This highlights

one of the peculiar characteristics of the modern day meat buyer—they tend to

put undo emphasis on what happened last year and expect that it will repeat.

That turns out to be a huge mistake this year and it really should have been

pretty obvious that conditions were setting up for this year’s consumer demand

to fall well short of last spring. I won’t go through my well-worn list of reasons

why consumer demand is softer this year, because everyone has heard that

many times, but this week we can add one more negative to that list—a rapidly

declining stock market. Beef, more so that the other proteins, is sensitive to

macroeconomic conditions and this week we had the Fed raise interest rates by

a half-point and the stock market move sharply lower in response.

In 2019, the S&P 500 posted a 31.5% increase, in 2020 it was up 18.4% and in

2021 it was up nearly 31%. So, for the past three years consumers have grown

used to very strong gains in their equity accounts and that makes them feel

wealthier and spend more freely. The fact that it lasted for 3 years straight

probably had a lot of them thinking this was going to be the new normal. Now,

in 2022, the S&P 500 is down 14% so far and the outlook suggests that it could

fall 20% or more for the year. That is a cold slap in the face for consumers who

not that long ago were feeling like their wealth was going up forever. In this

environment, it won’t be hard for a consumer to pass on $15/lb ribeyes in the

meat case. Further, it will be much easier for them to pass on it in July/Aug

when the dog days of summer arrive than it is right now ahead of Memorial Day.

So, my guess is that the demand problem for beef will get a lot worse before it

gets better. You may remember a few months back I talked about the brisket

primal as a good indicator for stay-at-home smoker demand. The attached chart

shows how brisket pricing continues to fade. As expected, consumers are

spending their money on travel and experiences they missed out on during the

pandemic.

Concert ticket sales have been through the roof lately. Airports have been jam

packed. Staying home and smoking a brisket on their shiny new pellet grill is

not nearly as high of a priority as it was in 2020 and 2021. It might be a good

time to look for some very lightly-used smokers for sale. Now that we have

established that the demand side of the beef market is in trouble, lets consider

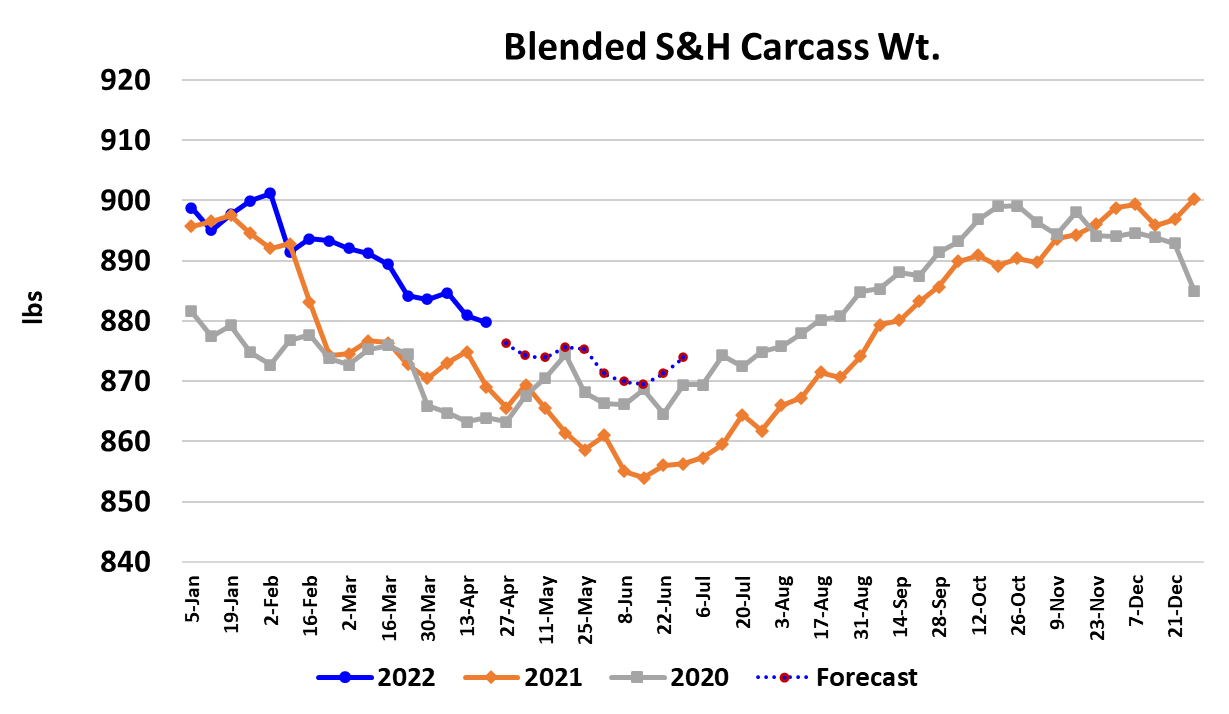

the supply side. This week’s fed kill came in at 510k, up 3k from last week and

just a little shy of what I calculate should be market-ready in May. I think we will

see at least one 520k kill before Memorial Day and once June rolls around kills

could routinely run 520-530k per week. Blended steer and heifer carcass

weights were reported 11 pounds over last year this week and we will soon

reach the point where carcass weights stop declining seasonally and start to

increase. That should be late May/early June. So, lots of cattle coming and

those cattle are pretty heavy. I’m sure that packers have been thinking hard on

how to move the cattle market lower in order to improve their margin situation.

The unusual tightness in the Northern market has limited packer’s ability to

pressure the cattle market so far.

It’s impossible to move packing plants in the North closer to where all of the

cattle are in the South, so the only alternative is to move cattle from the South to

the North. That is a much costlier proposition than used to be with fuel costs at

very high levels and truck drivers hard to find. As a result, I think that packers

have just had to bite the bullet and pay whatever it takes to source cattle in the

North. The supply imbalance should begin to resolve as we move into bigger

numbers in June and July and that will remove a major roadblock to lower cattle

prices. The Jun futures closed below $133 today, which is a full $10 lower than

the current cash market. Clearly futures traders think there is a big break

coming. I actually have fair value for June at $130, so I’m even more bearish

than the futures at this point, but I’m more concerned about what happens in late

summer and fall. I think traders have this mistaken belief that because inflation

is strong in the economy that means that cattle will need to sell for a lot more

than they have in the past. Not in the short run. Cattle prices have been held up

by very strong demand, but that is fading now. It is true that costs for inputs and

for labor have increased dramatically in recent months, but if consumers are

resistant to price increases (and it seems they definitely are now), then the only

margin relief comes from pushing down on input costs.

For packers, this means that they will need to pressure cattle lower and if

feedyards resist too much then packers will just cut the kill until feedyards are

forced to relent. In the longer run, high inflation will cause cattle prices to rise,

but that only happens after the herd has been reduced dramatically. The long

biological cycle in beef cattle means that it takes a long time to bring about that

kind of change. So cattle feeders that have had visions of $150-160 cash cattle

dancing in their heads are more likely to find the reality is a $115-125 cattle

market this fall. And, given what they’ve been paying for feeder cattle lately,

along with $8 corn, the losses in the feeding sector are likely to be huge. Once

that reality hits home, they will follow the same script and press down on the one

input cost they can control—feeder cattle prices. USDA released the trade data

this week and it showed March exports up 1.2% from last year, but March

imports were up almost 30%. That means that for the third month in a row, the

US has been a net beef importer. Next week, watch the middle meats for even

a modest rally because we will be in the sweet spot for Memorial Day buying.

Also watch for some softening in cash cattle prices, particularly in the South.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}