Beef Wrap May 13

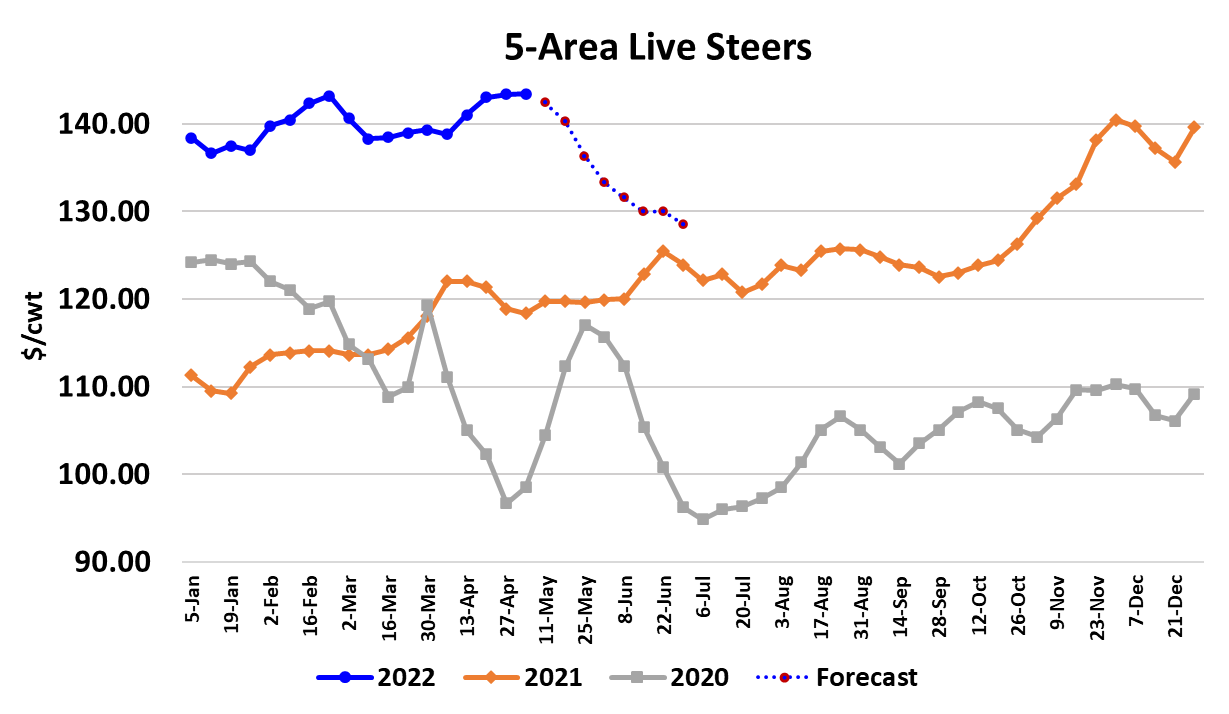

The cash cattle market started to work lower this week, with live trade

averaging $142.39/cwt, about $1 below last week and the dressed

market averaging $229/cwt, about $1.50 below last week. The

cutouts were lower again this week, but the declines slowed somewhat

as the Choice lost $1.34/cwt and the Select lost $3.64/cwt. Packer

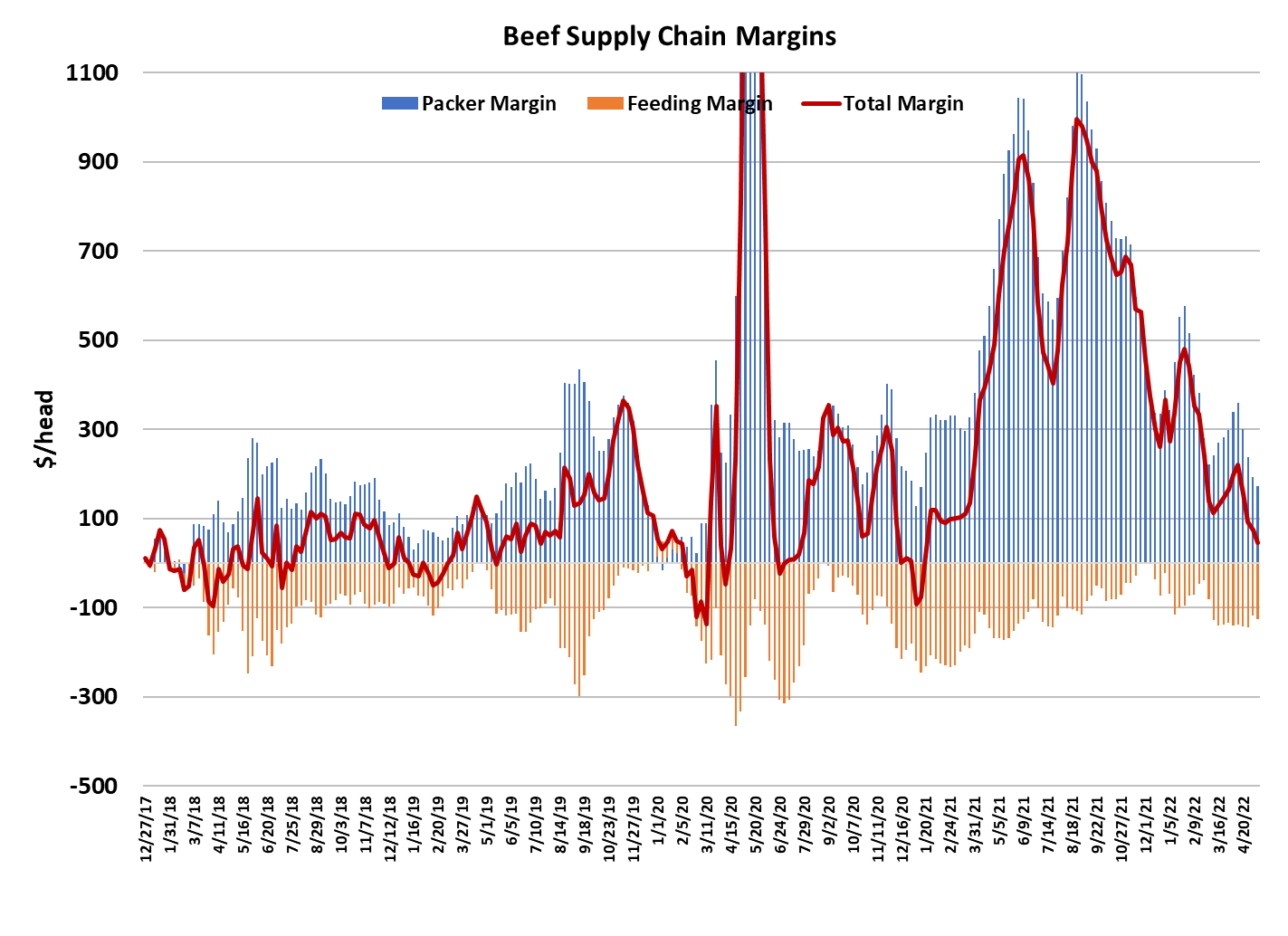

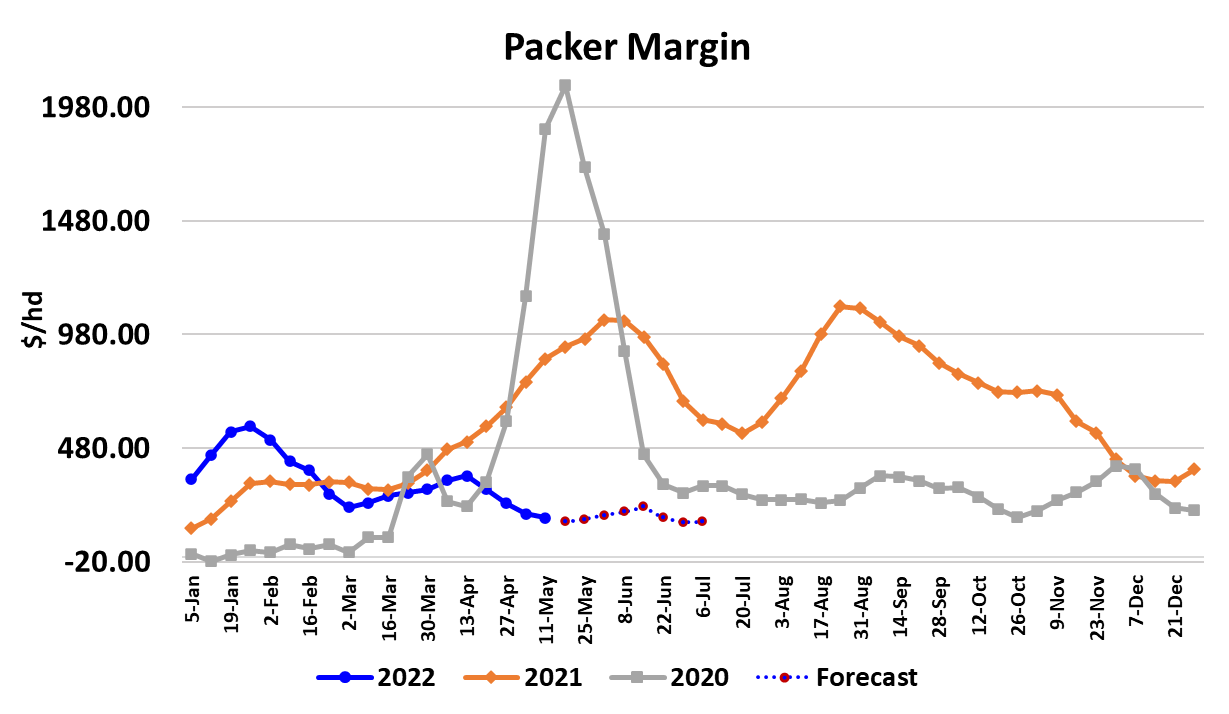

margins continued to compress and are now only $175/head. Last

year at this time packer margins were close to $900/head. That

dramatic difference in packer margins reflects a much different

demand environment this May compared to last year. We can see

further evidence of that in the attached combined margin chart. It is

clear that demand is still in a downcycle and is now lower that it was

back in the beginning of 2021 when the great demand bubble began to

emerge. It has been my contention that demand is heading back to

more normal levels. If you want to know what “more normal” demand

looks like, check out the combined margin chart between early 2018

and the middle of 2019.

There was a mini-demand bubble at the end of 2019 caused by the

Finney County plant fire that suddenly shorted the beef market and

sent buyers scrambling to find other sources of beef. While the trigger

was an abrupt loss of supply (a big plant went down), the ensuing

buyer panic shows up as stronger-than-normal demand and indeed it

is. If you look at the 2018 to mid-2019 period, you will notice that for

the most part the combined margin traded between +$100 and -$100/

head. Unless another black swan event rears its head, that range is

likely what we are headed back toward. That means way softer

demand going forward than what we came through in 2021. This

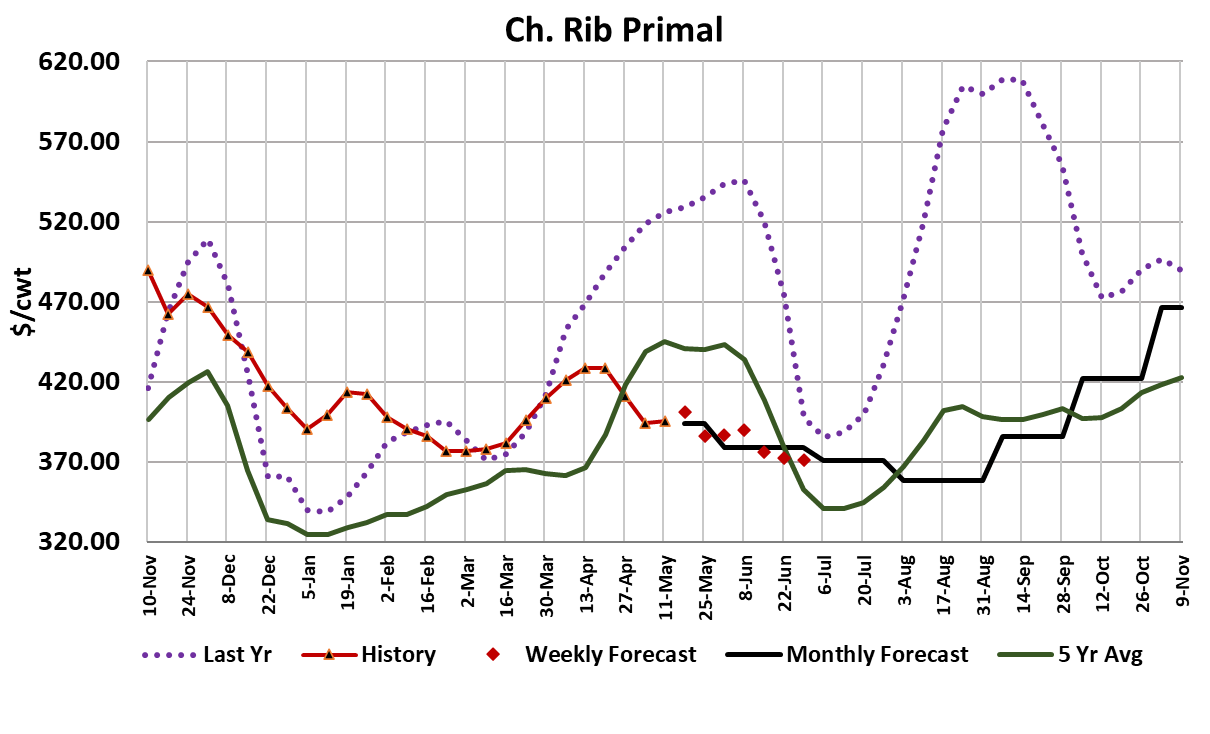

week it was the round and loin cuts that put the most pressure on the

cutout. Ribs managed to contribute a small positive to the cutout, but

the gain was pretty paltry for this time of year. In the next few days,

buyers should be wrapping up any last minute needs they have for

Memorial Day features. It wouldn’t surprise me to see the cutouts

actually post a modest gain next week as that business gets done.

After that however, the cutouts are likely to go back on the defensive

again. There will likely be some Father’s Day buying to complete in

late May/early June, but given the current trajectory of demand, I’d be

surprised if it can turn the cutout measurably higher. After next week,

the forecast has the cutouts working steadily lower and we could see

the Choice cutout in the $235-240 range before the end of June. If I’m

right about the trajectory of the cutouts over the next couple of months,

packers will need to put some serious pressure on cash cattle prices in

order to keep their margins intact. Fortunately for them, conditions

should swing the leverage meter in their favor and thus help in that

regard. Past placement patterns tell us that the number of market

ready cattle is going to grow from now through at least July, and

maybe beyond.

Carcass weights still look pretty heavy. Steer weights were reported

five pounds lower this week, but blended carcass weights are still 10

pounds over last year. Further, we are now at the point in the

calendar when carcass weights start to increase seasonally, so we

could see even greater supply contribution from carcass weights over

the next couple of months. Next Friday, we will get a fresh Cattle on

Feed report from USDA and I’m expecting it to show April placements

down 4.8% from last year. That sounds like some supply reduction,

but even that would still be 4.2% greater than 10-year average

placements for April. Those cattle won’t be ready for slaughter until

well into the fall, so it won’t do anything to relieve the near-term supply

bulge that is coming. If I’m close on placements, the May 1 feedyard

inventories will be 1.3% greater than last year. Bigger cattle supplies

than last year combined with way softer demand than last year is the

recipe for much lower beef pricing this summer.

The export market might help to take some of that product off of the

domestic market if price levels get low enough, but the USD is likely to

remain very strong and that could work to temper some of that export

demand. And, as I’ve pointed out before, there has been a big

increase in imported beef flowing into the US. That isn’t likely to

change dramatically and could easily offset any gains in exports this

summer. This week, USDA reported that retail beef prices increased

five cents per pound in April and are now almost 15% stronger than

last year. At the wholesale level, the blended cutout was 3.4% lower

in April than it was a year ago. Clearly, retail margins on beef are very

good right now, but I would look for retailers to start cranking down

retail prices and offering hotter features once we move beyond

Memorial Day. That will be needed in order to improve product flow

through the system because cattle slaughter and beef production are

both likely to increase from this point forward. Compared to the past

couple of grilling seasons, this one has been much more sedate and

prices have been better behaved.

Given the troubles in the macroeconomy (inflation, falling equity

markets, poor consumer confidence), I don’t think we are at risk to see

any substantial demand surges this summer. Demand will still cycle

and produce some ups and downs in price levels, but the amplitude of

those changes should be much smaller than in the past couple of

years. My fundamental analysis suggests that the bias throughout the

summer should be toward lower price levels, so buyers should

probably be cautious about extending coverage too far forward for the

next few months. Next week, watch for some modest increases in the

middle meats as the last-minute Memorial Day business gets done

and look for further softness in the cash cattle market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}