Beef Wrap April 29

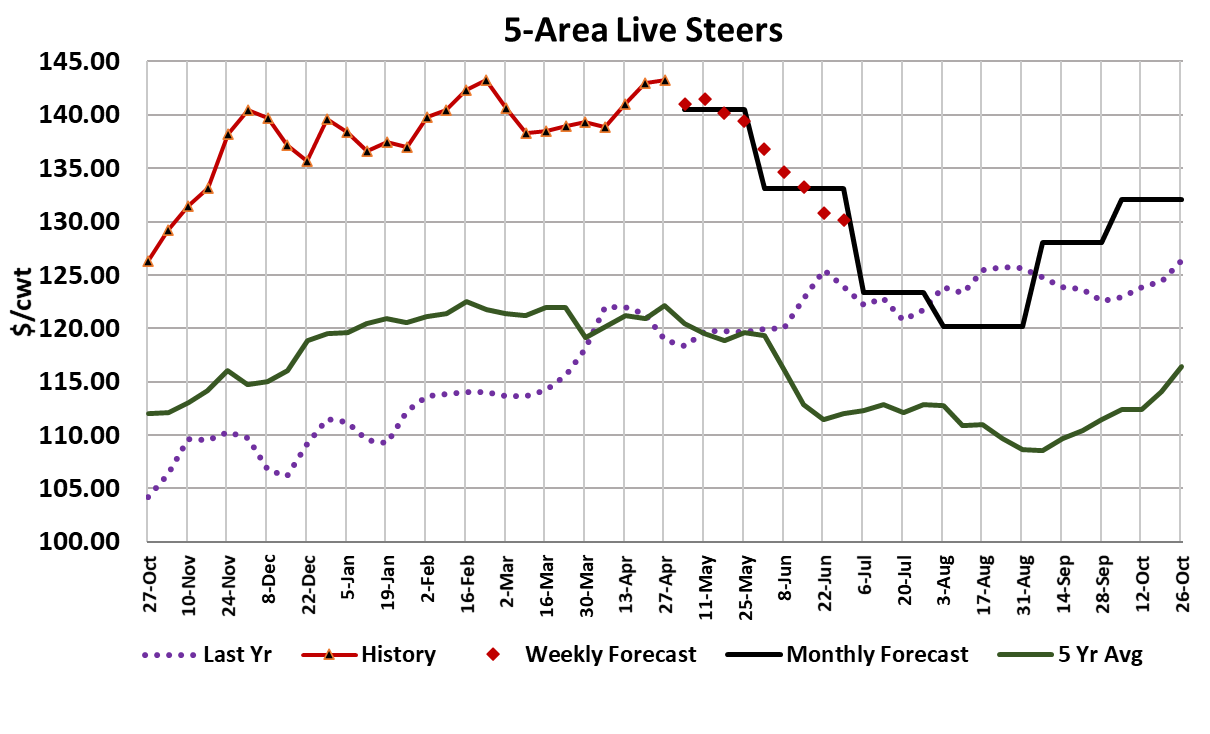

The cash cattle market managed to shake off last week’s bearish Cattle on

Feed report and held steady this week, thanks in large part to strong

bidding in the Northern states where prices were $5-6 higher than in the

South. The weekly average nationally was $143.31, almost even with the

week before. This is one of the widest regional price spreads that I’ve

ever seen. We saw a large number of deliveries tendered against the

futures contract again this week as cattle feeders in the South tried to take

advantage of a Apr LC price that was stronger than what they could get

from packers in their region. But aside from the steady cash trade and an

expiring Apr contract that was down only slightly, the rest of the cattle

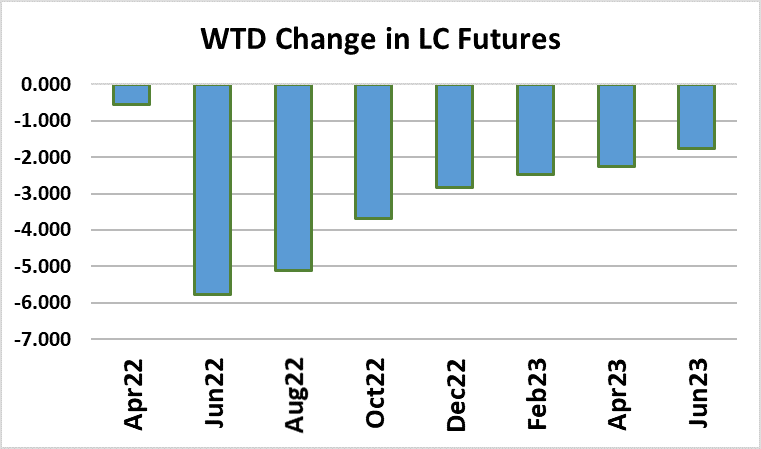

complex became extremely bearish this week. The Jun futures dropped

almost $6 and is pointing to cash cattle values in the low $130s two

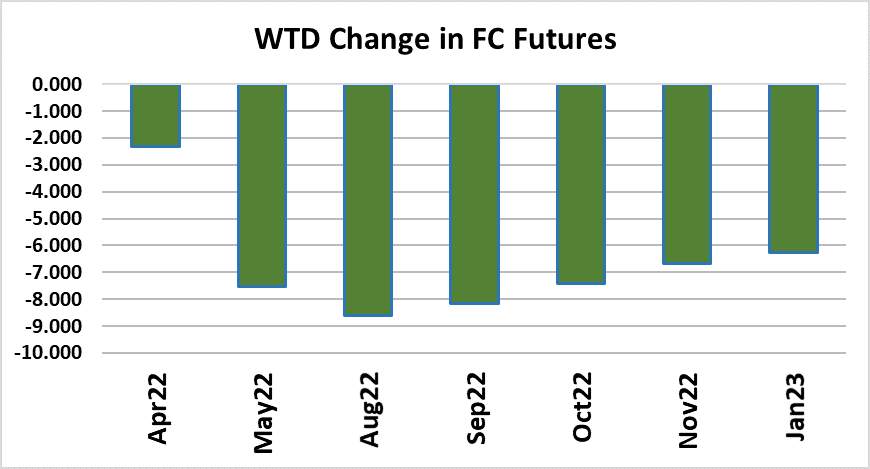

months from now. Feeder cattle futures sold off hard also. A big part of

what made traders so bearish was continuing softness in the beef market.

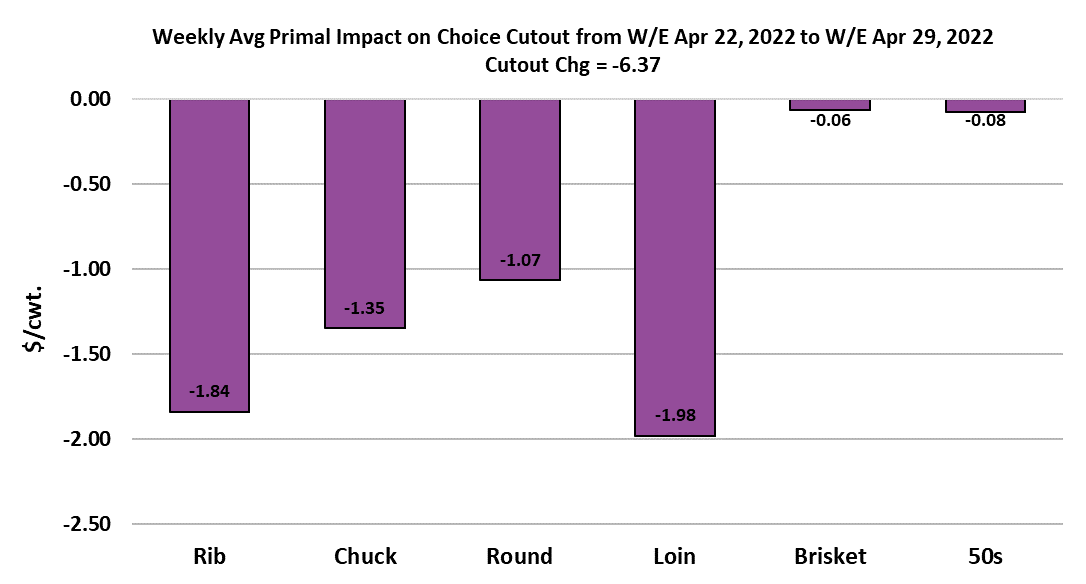

Both cutouts lost over $6 this week. That was a real shocker for traders

that are used to seeing the cutouts move rapidly higher after Easter.

The attached chart indicates that it was both middle meats and end meats

that suffered losses this week. Briskets and 50s were spared, but their

time in the barrel is probably not far off. What seems to have caught

traders off guard is how rapidly demand has deteriorated once the

pandemic ended. I have said for a long time that that meat demand is

likely to return to “normal” once the pandemic subsides, but even I didn’t

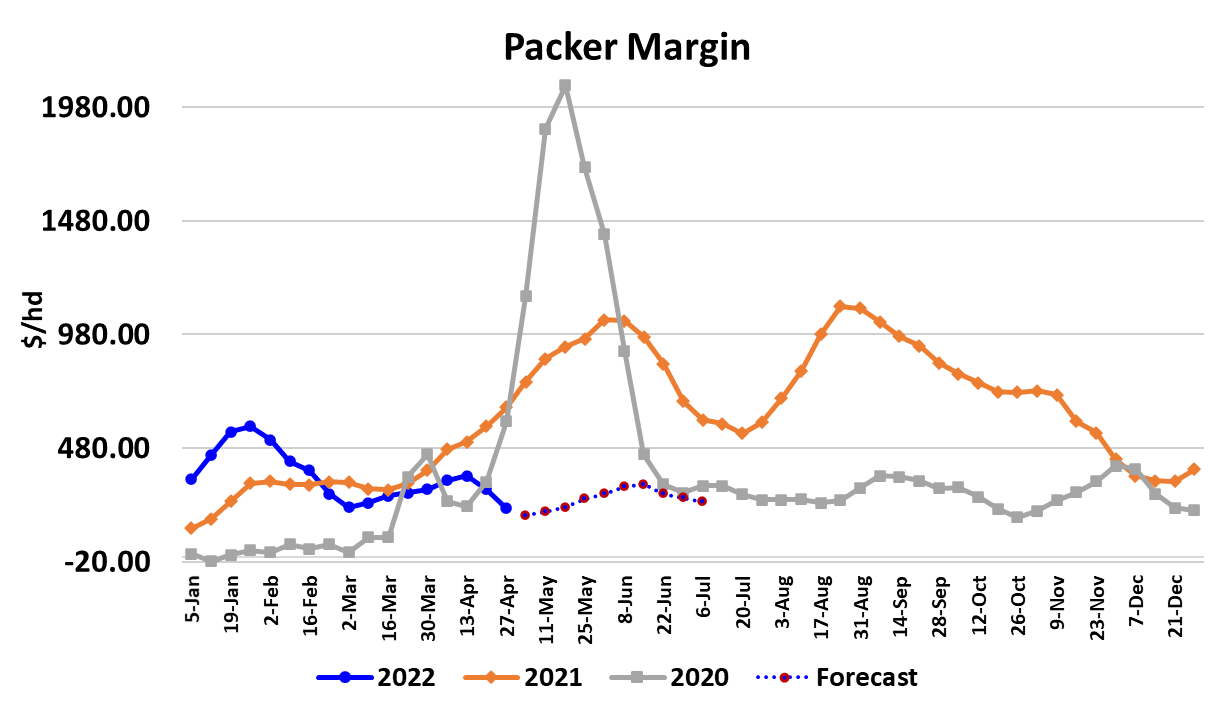

expect it to happen this fast. The combined margin chart is very

instructive in this regard. Note the very high levels of the margin from the

inception of the pandemic onward. 2021 was much stronger than 2020,

but that whole 2-year period was well above what was seen prior to the

pandemic. When I say demand is headed back to normal, I expect that,

over time, the combined margin will start to look a lot more like it did back

in 2018-19 than the pattern from 2020-22. The combined margin took a

big step down this week and looks to me like it is going to go negative very

soon. Too often traders focus on the supply side of the market and don’t

think enough about how demand will change in the future.

The tendency is to believe that if demand is good now it will be good in the

future and if demand is poor now it will be poor in the future. But the

combined margin clearly indicates that demand cycles from high to low

and back again. When the pandemic first started, it was difficult to know

how demand would be affected since no one had ever been through that

type of situation. So, I can excuse those (including myself) who didn’t see

the big pandemic demand surge coming. However, we have plenty of

experience with non-pandemic beef demand and it is inexcusable not to

have seen that beef demand would decline as the pandemic faded and life

got back to normal. The end of the pandemic is just one of the headwinds

for beef demand. We all know the others: inflation, no more stimulus,

high energy prices, war in Europe and now….a cratering stock market. Beef

demand, more so than pork or chicken demand, is very sensitive to the

health of the economy and that is looking shakier by the day. In order to

get inflation under control the Fed is likely going to have to send the

economy into a recession.

The stock market is picking up on this now and it will not be good for

beef demand. Packer margins are likely to be a lot narrower going

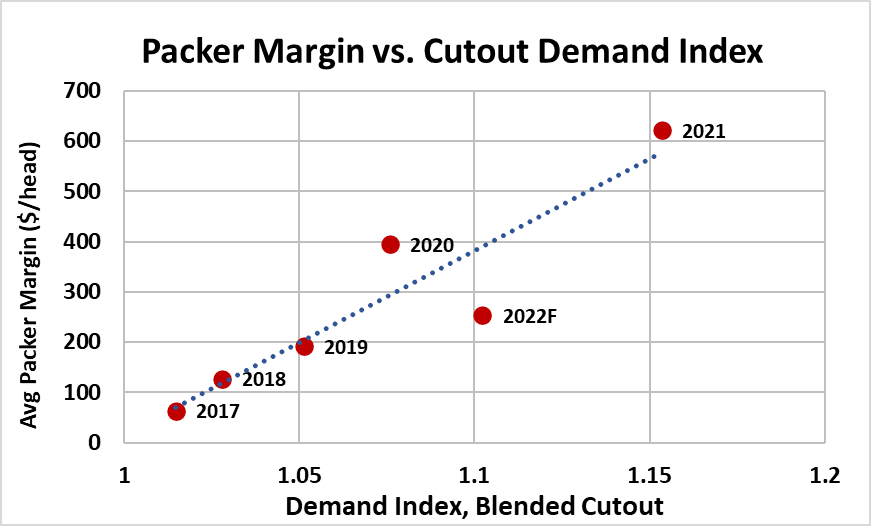

forward than they have been in the last couple of years. The attached

scatter diagram shows the annual relationship between the packer’s

margin and the level of beef demand. In strong demand years, packer

margins are strong, but in more-normal demand years (2017-19) packer

margins are much more subdued. The 2022F data point looks low on

this chart so maybe I have either the margin too low or demand too high

for 2022. Time will tell, but this week packer margins fell to $213/head

and I have them forecast to dip below $200/head next week. This

margin compression is coming at the time of year when packers

normally earn their best returns. The primary reason that my mispricing charts have shown such big over-pricing is that I have dialed

demand back down to more-normal levels as the year progresses and

into 2023. Apparently, futures traders are not yet ready to do the same.

Ok, that was a lot about demand, so what about supply?

This week’s fed slaughter came in at 509k, down 11k from the week

before. Packers seemed to dial back on the Saturday kill. However, the

first week in May is just around the corner and we know from past

placement patterns that market-ready supplies are going to grow

considerably in May, June and July. With the demand environment

seemingly getting weaker by the day, what will happen to beef prices

when much larger volumes start to get pushed through the system? It

could get ugly fast. I don’t think that we can count on export markets to

take a lot more than they are taking today, so that additional beef will

need to clear in the domestic market. I’m hoping that at least a

moderate amount of grilling season demand will emerge in the next few

weeks that allows the market to hold steady or even advance modestly

in the face of growing production, but that might just be wishful thinking.

For those that are expecting tighter supplies to lift cattle and beef prices,

I’m afraid they will have to wait until fall or early winter to realize that.

One other point is worth making here. Back in the pre-pandemic days,

cattle and beef prices tracked relatively closely. If beef prices struggled,

packers would soon find a way to push at least some of that financial

pain back on cattle feeders. During the pandemic, demand was so

strong and packer margins so wide, that beef and cattle prices were

often disconnected. As things get back to normal, I think that we can

expect packers to pay much more attention to what they pay for cattle

and that means that cattle prices are likely to come under more

pressure going forward. Next week, watch the cutouts for some

improvement in demand. The clock is ticking… spring demand normally

peaks near the end of May and then softens into summer. Keep an eye

on the equity markets. If the meltdown there intensifies it could spillover

in cattle futures and eventually the cash beef market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}