Beef Wrap May 5

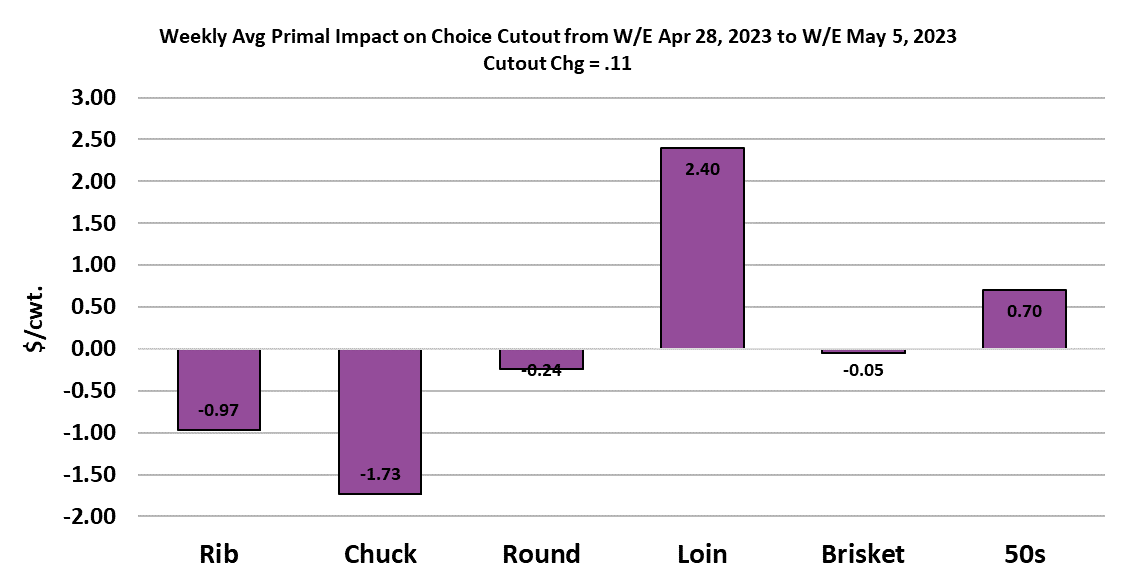

The beef market stalled this

week with the Choice cutout adding a mere $0.11/cwt. and the Select cutout up

$0.15/cwt. Beef buyers aren’t happy about a Choice cutout over $309 and a

Select cutout over $288, but their ability to resist strong beef prices is

limited by continued small fed kills and low weekly production. The

cash cattle market continued to retreat from the record high that it set three

weeks ago, averaging about $174.15, down a little over $3 from the week before.

The demand side of the beef market continues to look pretty strong and will

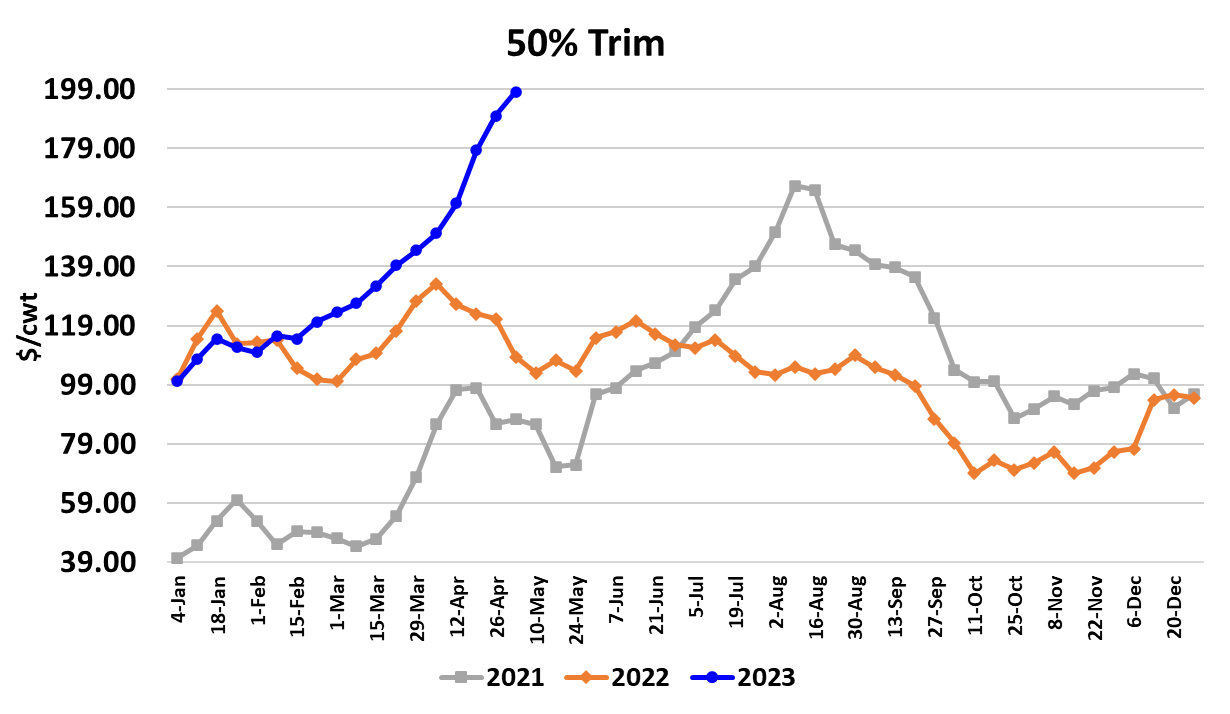

probably remain that way through Memorial Day. The 50s market is still

hovering close to $200/cwt., and 50s, along with loins, were the only items to

provide support to the Choice cutout this week. Everything else was a

little softer. I think that we are pretty close to the spring top in the

cutouts now, but I don’t expect them to move rapidly lower either. The

forecast has the Choice cutout working back to about $300/cwt. area by the end

of May and by the end of June it could be back down around $285/cwt.

Retailers will be busy raising retail prices during May and by the time we get

to June, that should start to curtail consumption somewhat. This week the

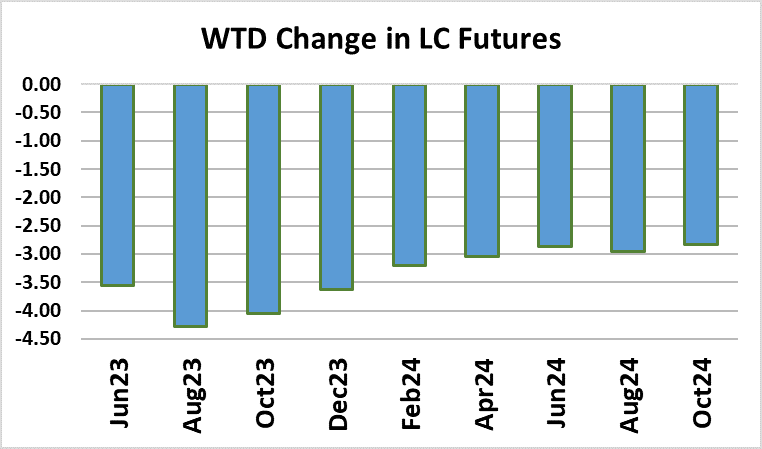

Jun LC futures lost over $3.50/cwt., and so far the cash has been coming down

alongside the futures. However, the Jun contract is about $10/cwt.

discount to this week’s trade in the Southern Plains, which was close to

$172/cwt., and that may limit the downside potential for June in the near

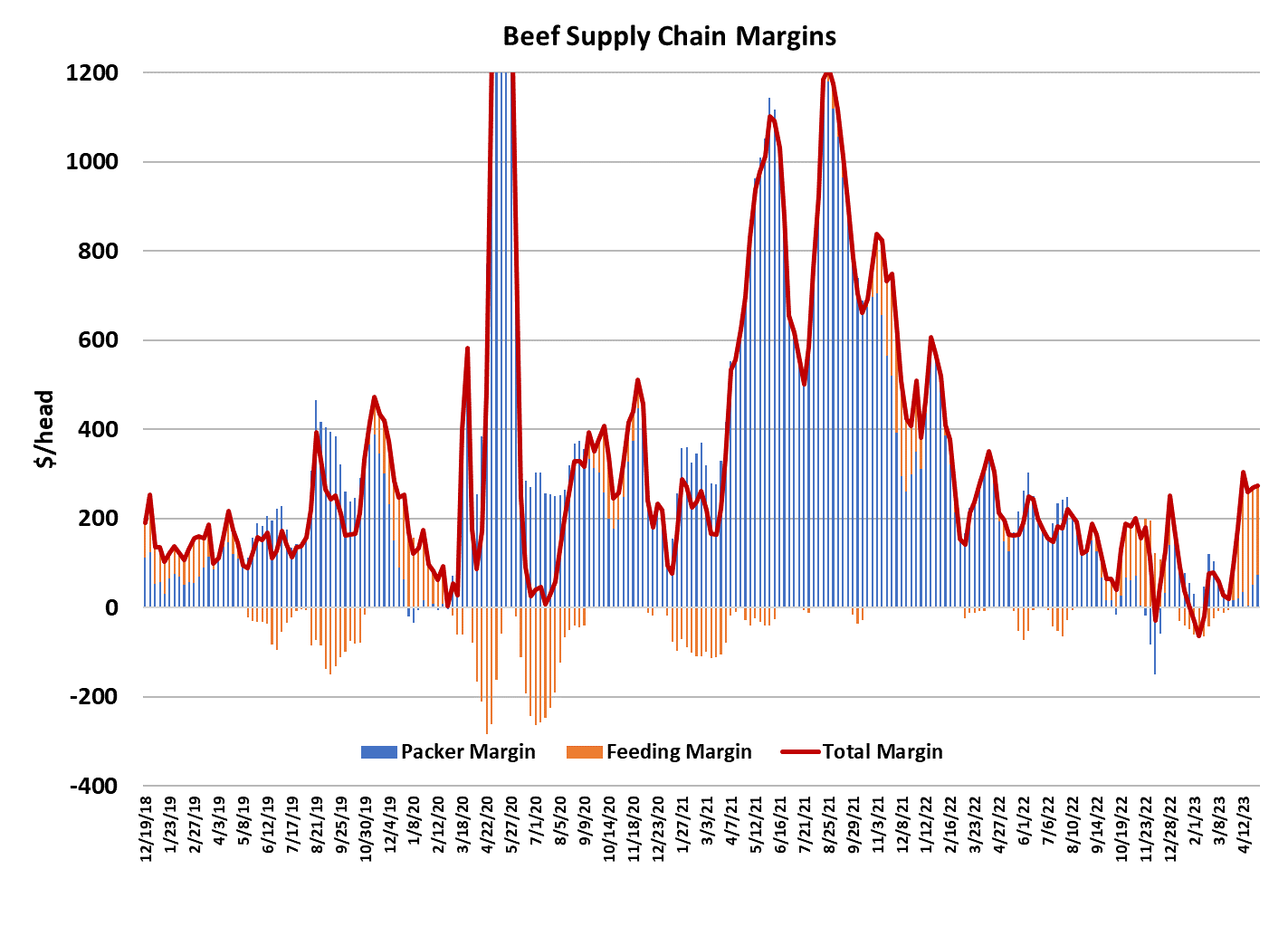

term. Packers have done quite well at navigating this period of tight

supplies without trashing their margins. I calculate this week’s packer

margin at about $73/head and expect that to expand a little in the next couple

of weeks. Of course, the declining cash cattle market is tempering cattle

feeding margins which are now just a hair below $200/head. But, at least

we have both segments of the supply chain making money at the same time and

that usually only happens when demand is pretty good. Another piece

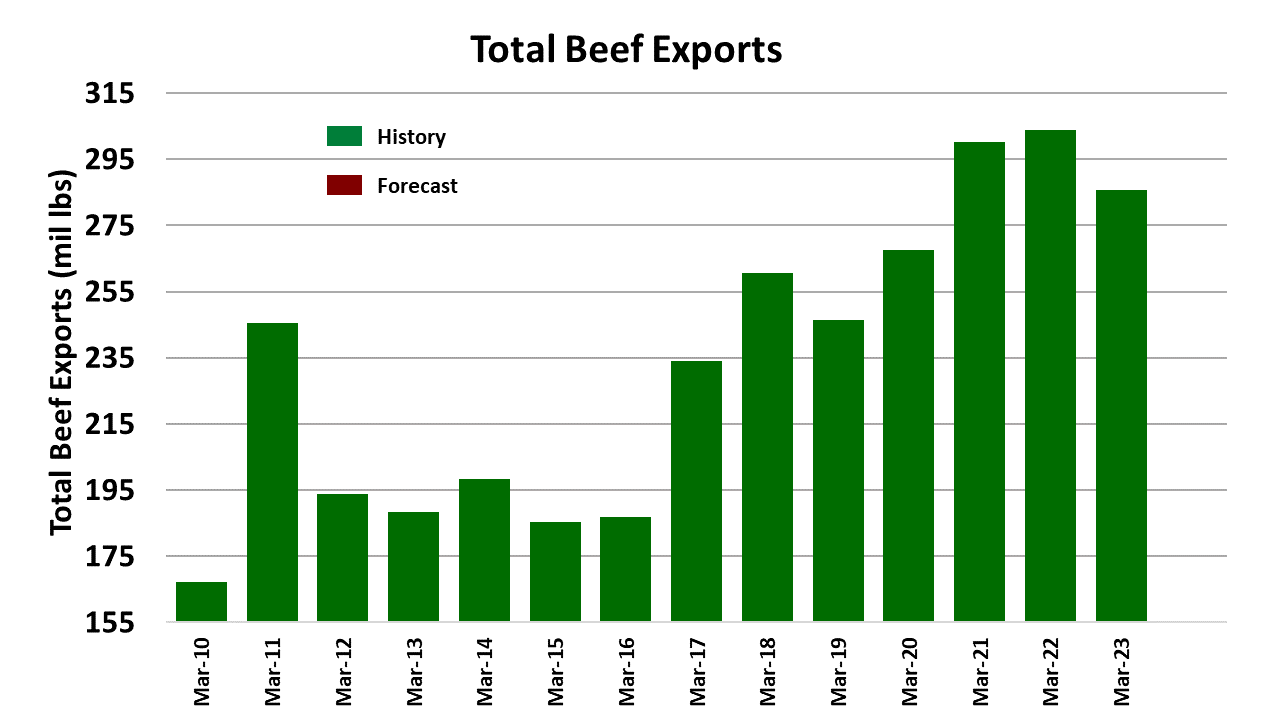

of good news came from the FAS weekly export data on Thursday, which showed

beef exports looking better than they have in recent weeks. We also got

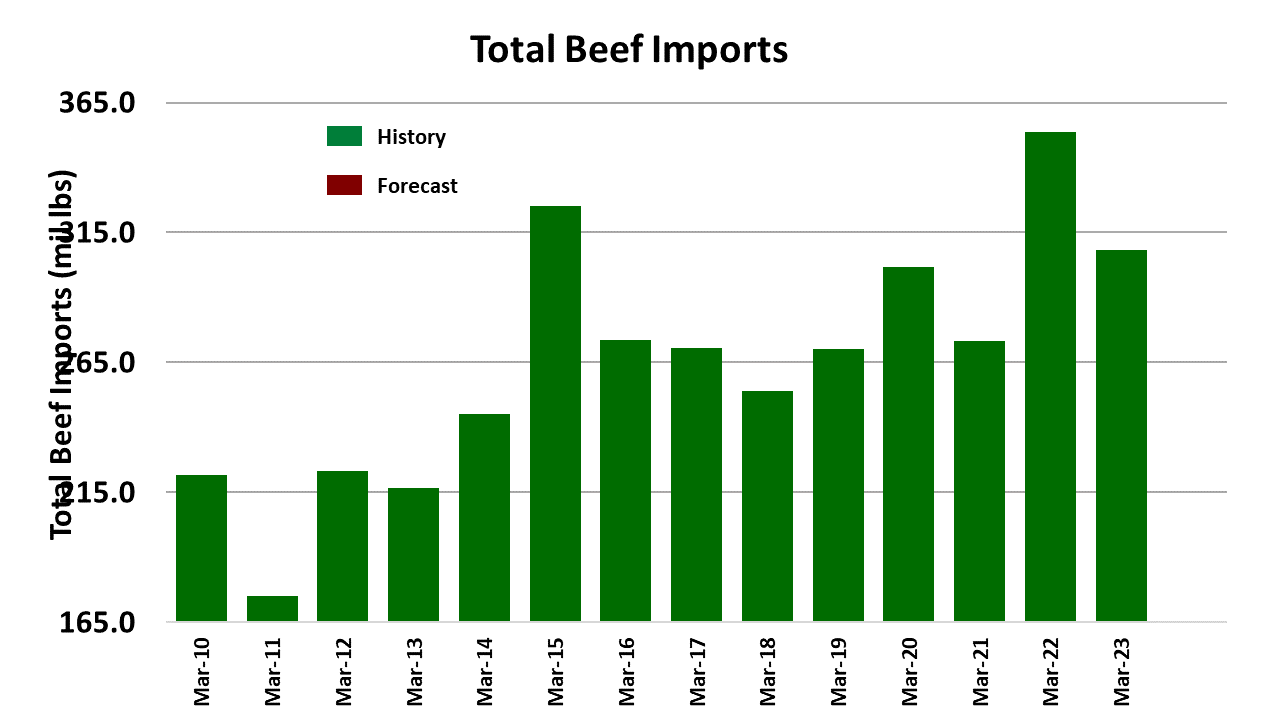

the official ERS trade data for March this week and it pegged beef exports at 285.7

million pounds, down 5.9% from last year. Those YOY gaps are likely to

grow during the summer months, simply because exports were really strong last

summer. It is encouraging to see exports perking up in a time period when

beef is priced pretty high. This week’s fed kill registered 484k, right

in line with what the flow model predicted for this time of year. I think

that as Memorial Day draws nearer, packers will try to cheat-up the kill into

the 490-500k per week range and that is probably when the declines in the cash

cattle market will slow or perhaps stop all together. After June arrives,

our model suggests that cattle supplies should be sufficient to fuel kills a

little over 500k per week. That’s not a very big increase from where we

are today, but it should provide some pricing relief for beef buyers.

Demand also usually drops off after Memorial Day, except for last minute

Father’s Day buying. That should also help lower wholesale beef

prices. I think retailers will be more open to featuring pork after

Memorial Day also. Apparently, JBS’s plant in Fort Morgan, Colorado

is still hampered by mechanical issues it suffered a couple of weeks ago and is

not processing at its normal rate. If that continues, it won’t help the cash

cattle market any. Cattle carcass weights are starting to look a little

heavy, and the FI data seem to be suggesting that perhaps weights will bottom

earlier this year than in the past couple of years. Cattle in the

northern feeding areas are now starting to get caught up after the rough winter

and that has caused the gap between in carcass weights between this year and

last to narrow. The DTDS weights are also well above zero now, so

that is something to keep an eye on. The corn market has been rather

jittery of late, but that is normal at this time of year, when farmers are

working to get the crop in the ground. All indications are that this

summer’s weather will be a vast improvement over the last two years and that

should help grain stocks to build and corn futures prices to retreat.

Cash corn basis in the Southern Plains remains stubbornly high however,

and that could continue even after the new crop is harvested, so cattle feeders

might not see as much of a decline in their corn costs as the futures board is implying.

Feeder cattle prices have come tumbling down, following the live cattle futures

as they corrected from their highs. The front of the feeder cattle curve

lost $8-9/cwt. this week, but declining corn prices will eventually provide support

to the feeder cattle market. That should turn feeder cattle prices

higher again once the near-term correction in live cattle has run its

course. All in all, the cattle and beef complex seems to be coming back

into better balance after a wild ride in April when prices spiked. Next

week, watch the weight data for signs that that season bottom in weights may be

near and watch the weekly export numbers for potential further improvement.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}