Beef Wrap April 27

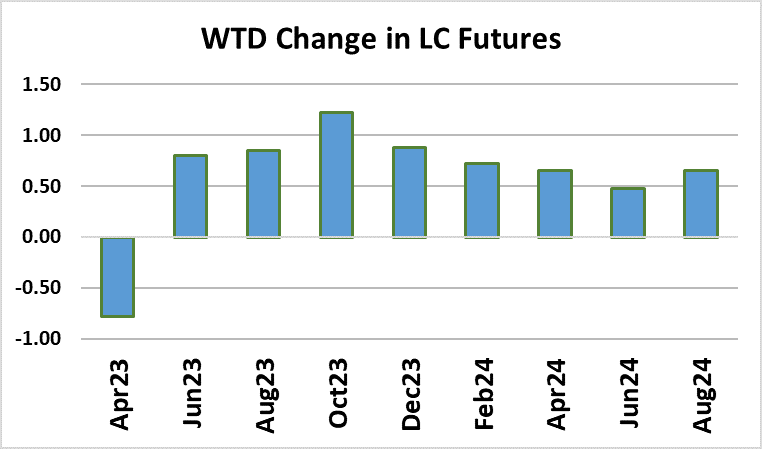

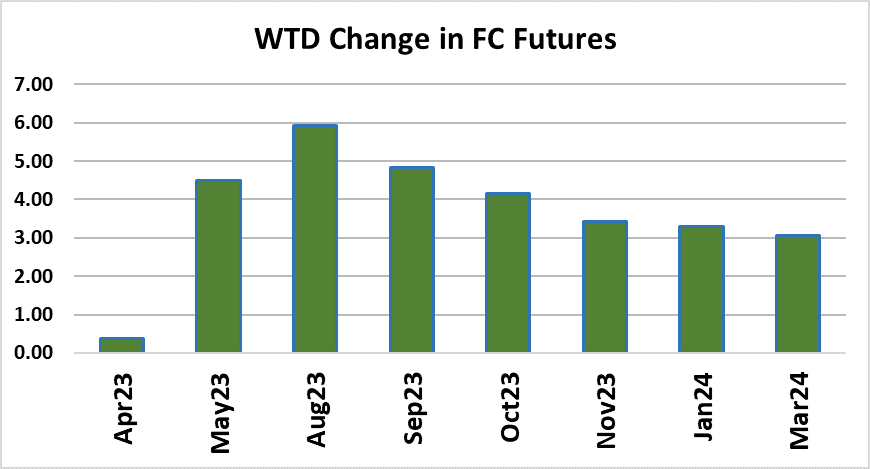

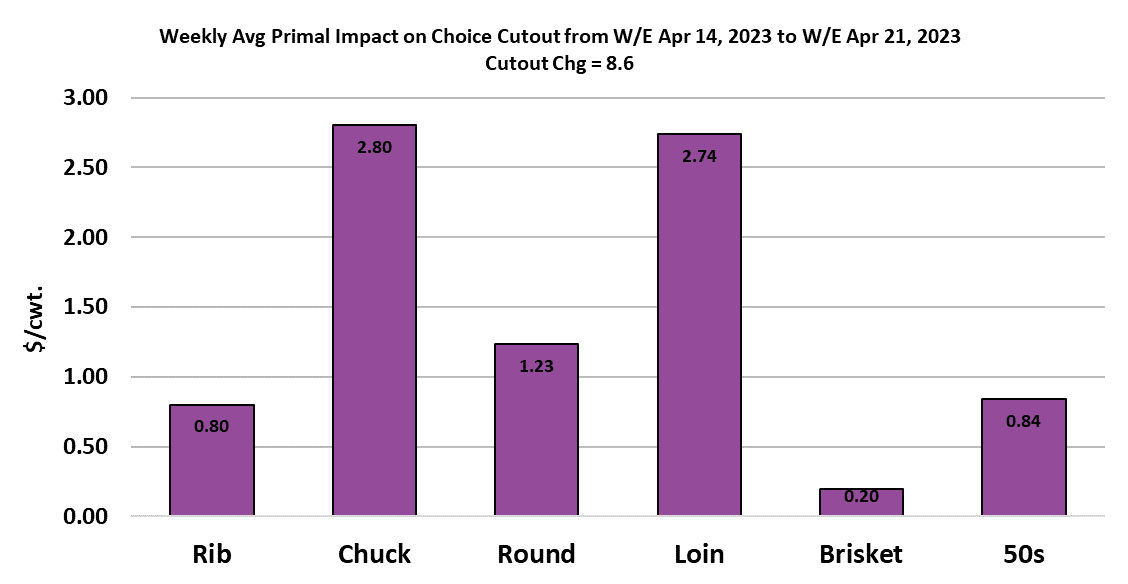

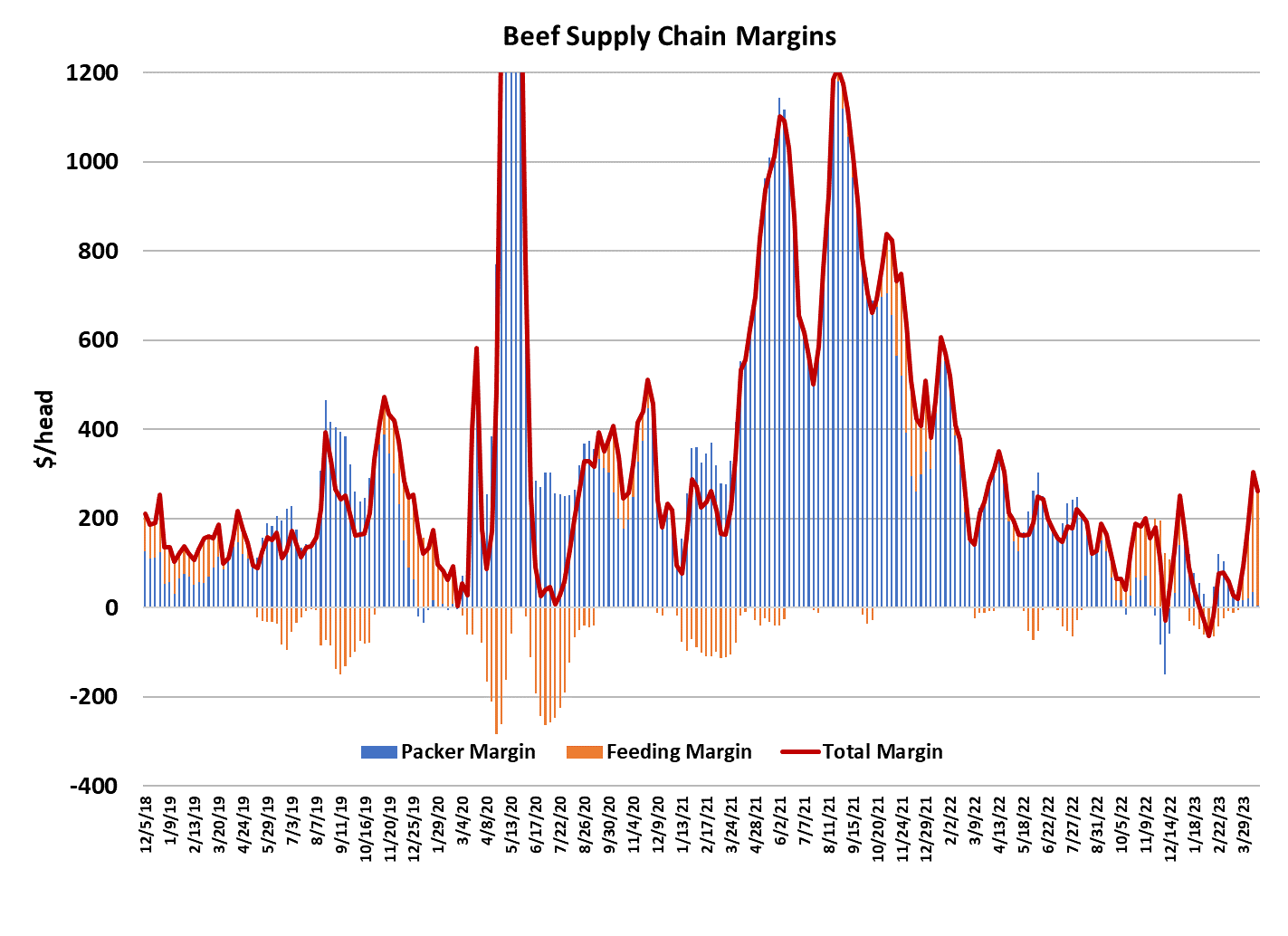

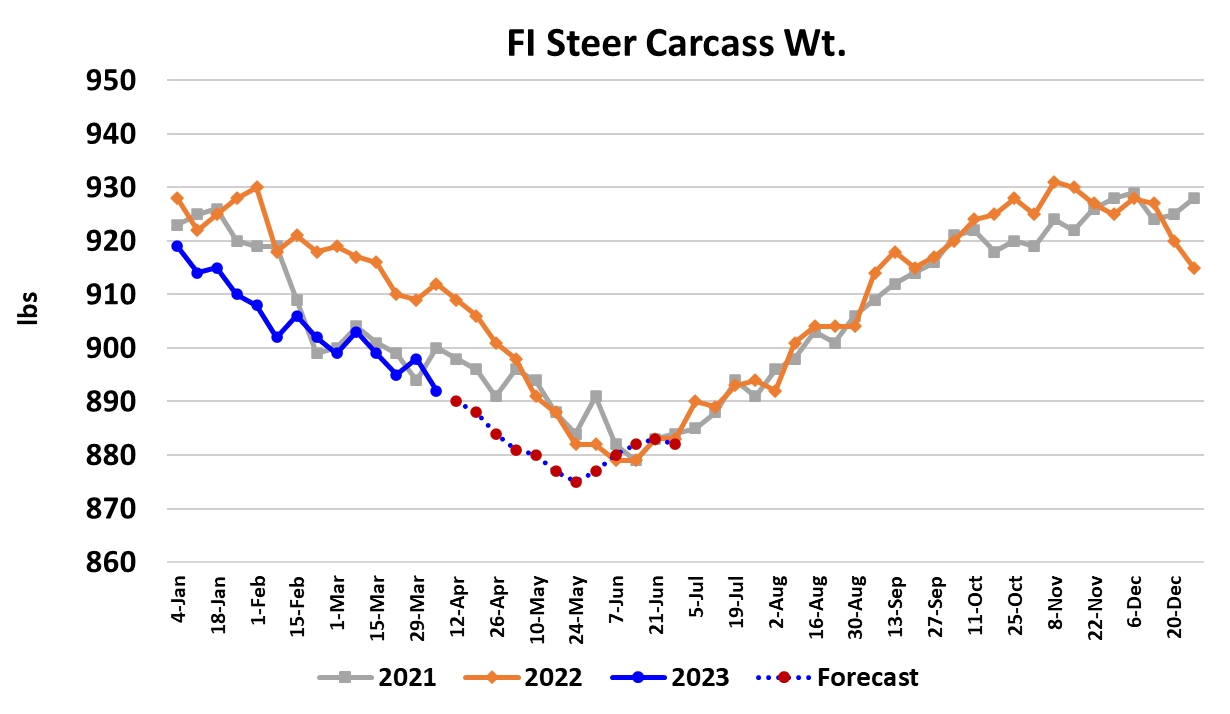

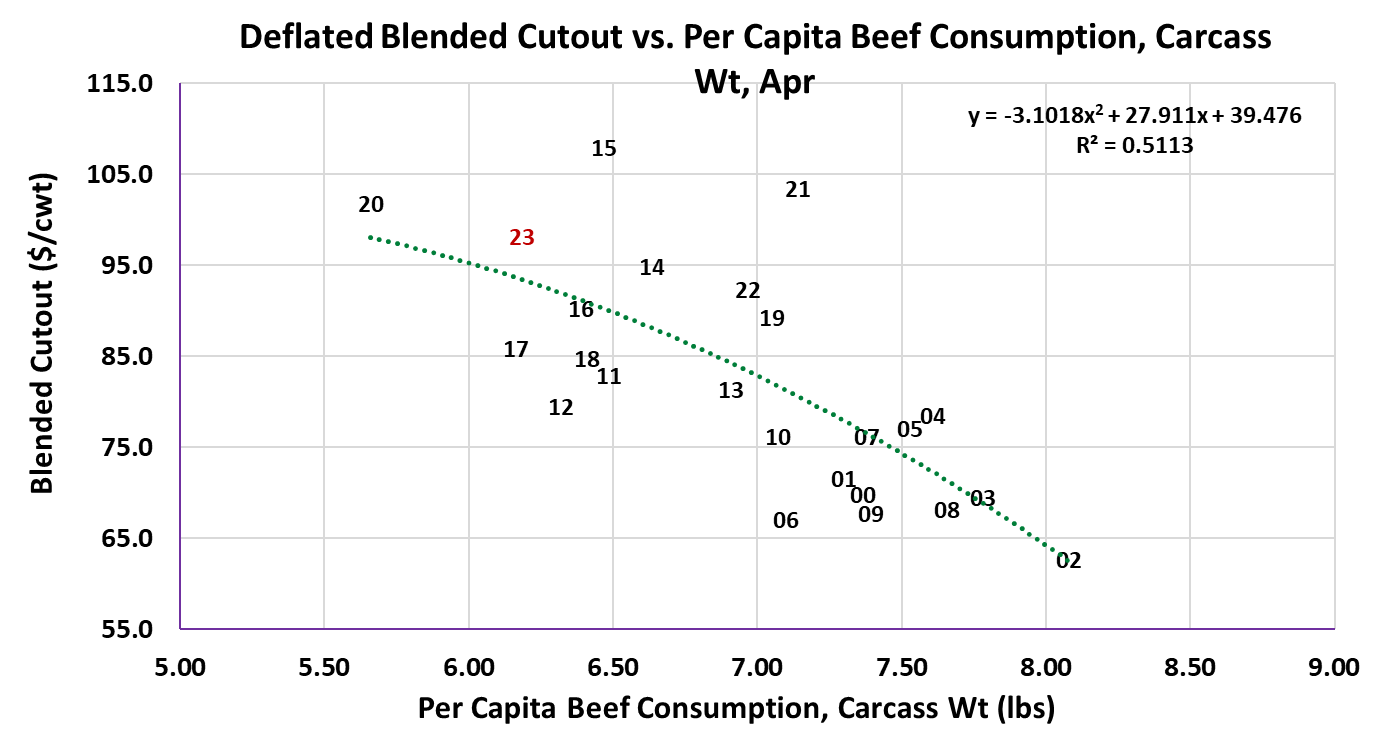

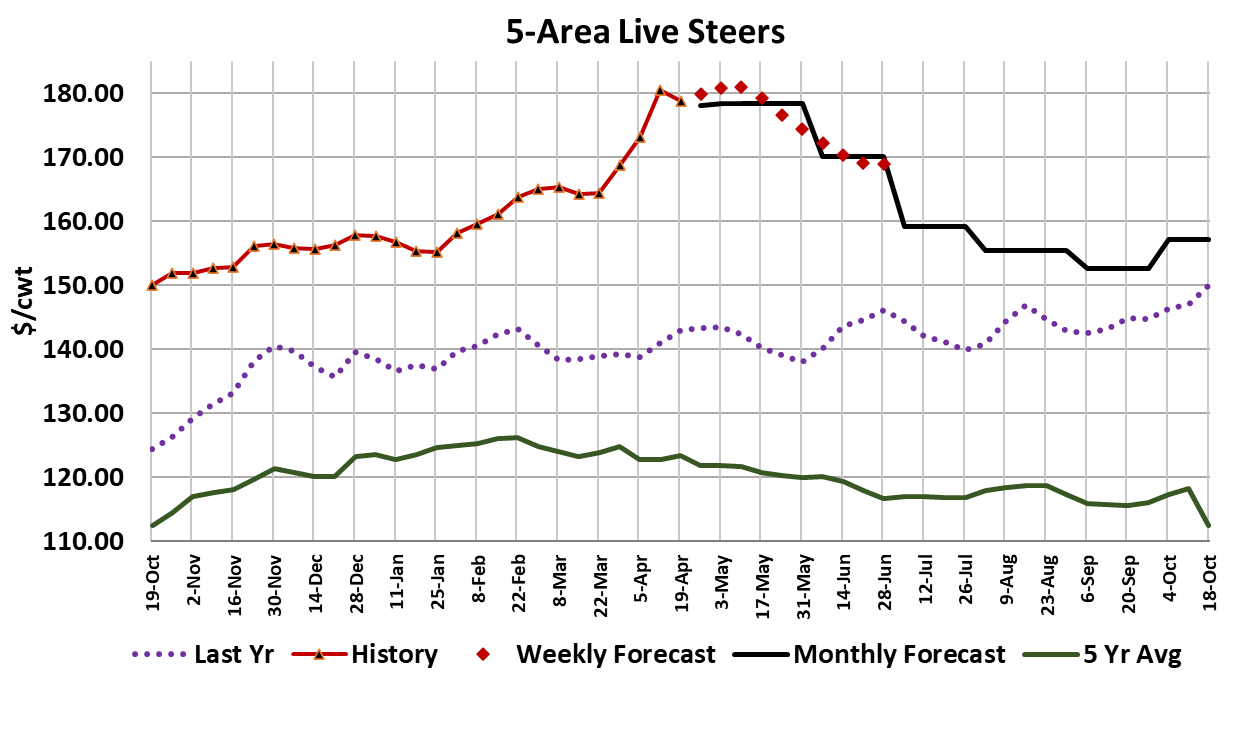

The cash cattle market eased about a dollar lower this week to average close to $177.50. Prices in the South fell mostly in the $173-174 range while in the North $177-179 was common. Trade volume was comparable to the week before and probably adequate relative to the current kill level. Packers will have access to their May formula cattle next week, so it is possible that they may manage to pressure the cash market downward a little more next week. The cutouts were mixed this week, with the Choice gaining $2.79/cwt. to average $309.30, while the Select lost $1.45/cwt. to $288.34. While it may look like the cutouts are losing steam, caution is still warranted because the next couple of weeks should see some of the best demand of the year and that could give the cutouts a second wind. The Apr LC futures expired today at $175.18, well above expectations just a few weeks back. Once again, the best gains in the futures came after the front month entered its delivery period. Now that Apr is off of the board, there is risk that the futures will chop and trade lower for a while until the Jun contract starts to approach its delivery. June is currently trading about $12/cwt. under the latest cash average and there is some question as to whether or not the cash cattle market will retreat fast enough to justify Jun’s large discount. I calculate this week’s packer margin at close to $50/head, which is their largest margin since the first week of March. Thus, there isn’t a huge incentive for them to pressure the cattle market in the near-term, especially since they will need all available cattle to meet the pre-Memorial Day demand. From a cattle feeder’s perspective, things are looking pretty good as they margins clocked in close to $225/head this week. As is typically the case, when cattle feeders have a lot of jingle in their pockets, they spend excessively on feeder cattle. They are now routinely paying over $200/head for 700 pound feeder animals and when those animals finish this fall, they are going to have to sell for $175/cwt. or better just to breakeven. Of course, they are counting on a great corn crop to push corn prices lower as the year progresses, but that is already factored into that $175/cwt. breakeven. One of the reasons that packers have been able to hold the cutouts at such a high level is that they are being very judicious with their slaughter plans. This week’s fed slaughter came in at 488k, which is right in the 480-490k range that the flow model suggested would be available during April and early May. They will probably be tempted to push the kill higher in the next couple of weeks, but as long as they don’t reach for a 500k kill, they should be able to keep the cash cattle market in a modest decline. When June arrives, the fed kill can probably comfortably expand to 500-510k per week and that likely means lower cattle prices and lower cutouts after Memorial Day. Of course, by June the sharp gains in the cutouts that we saw in the past few weeks will have had time to flow through into higher retail prices. That runs the risk of tempering consumption right at the point in the calendar when beef production is expanding. Beef buyers would probably do well not to ramp up coverage much beyond the end of May as a result. Carcass weights are starting to look a bit heavier and that could also help break the cattle market lower at some point in the next few weeks. FI steer weights ticked a little higher this week, but are still 12 pounds below last year. I’m not sure that last year is a great comparison however, because weights last spring were pretty heavy. There should still be a month or so of further declines before carcass weights make their seasonal turn higher. The DTDS weights are relatively heavy at the moment also, which we should take as a bit of a caution signal. Fed beef production this week is estimated at 420 million pounds, about 6% below both 2022 and 2021. It seems reasonable to expect that beef production will stay below last year right through summer, but the gap will be narrower in mid-to-late June than it is now. The demand side of the beef market seems to be holding up pretty well, at least from domestic consumers. The combined margin ticked a little higher after last week’s small decline, so it isn’t giving much guidance as to whether or not it is going to turn lower soon. My guess is that it won’t cool significantly until late May or early June. International demand for beef doesn’t look all that great right now, but that shouldn’t be too surprising given the level of US beef prices. The attached scatter diagram for May shows that I’m forecasting domestic beef demand to remain well above last year through next month. If I’m wrong about that I’m probably too high. I’m looking for the Choice cutout to average about $308/cwt. for the month of May, so not too much different from where it is right now. This week, it was the loins and 50s that provided the most support to the cutout and most of the other primals were close to steady. I am still waiting for the rib market to make its move higher, but recognize that maybe it will disappoint somewhat this spring. 50s averaged $190/cwt. this week, which is a bit odd since ground beef hasn’t been all that strong. The fat trim is probably nearing a top and once it turns, it holds a lot of downside risk. As the calendar now turns to May, it is all eyes on beef demand to see if it can live up to expectations. Beef supplies are likely to remain tight and that will be supportive so there is risk if consumer demand suddenly catches fire.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}