Beef Wrap May 12

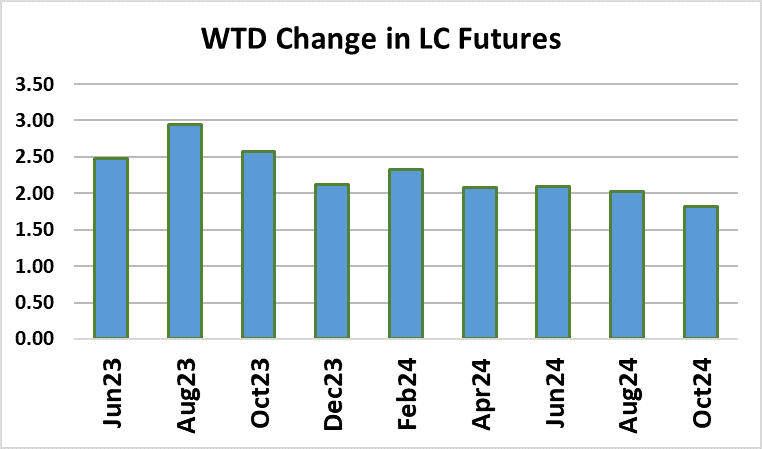

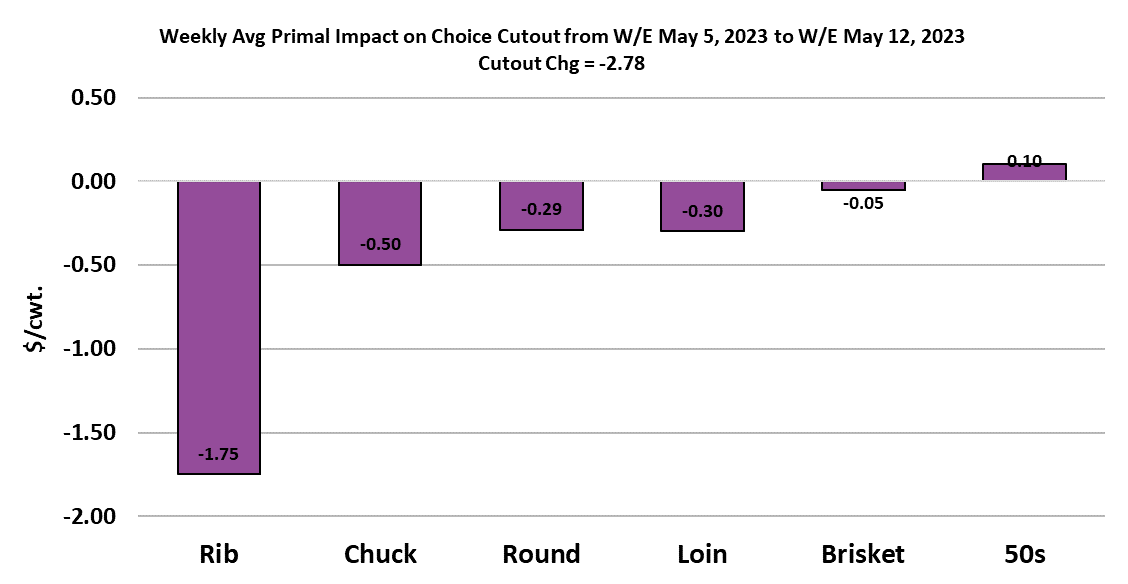

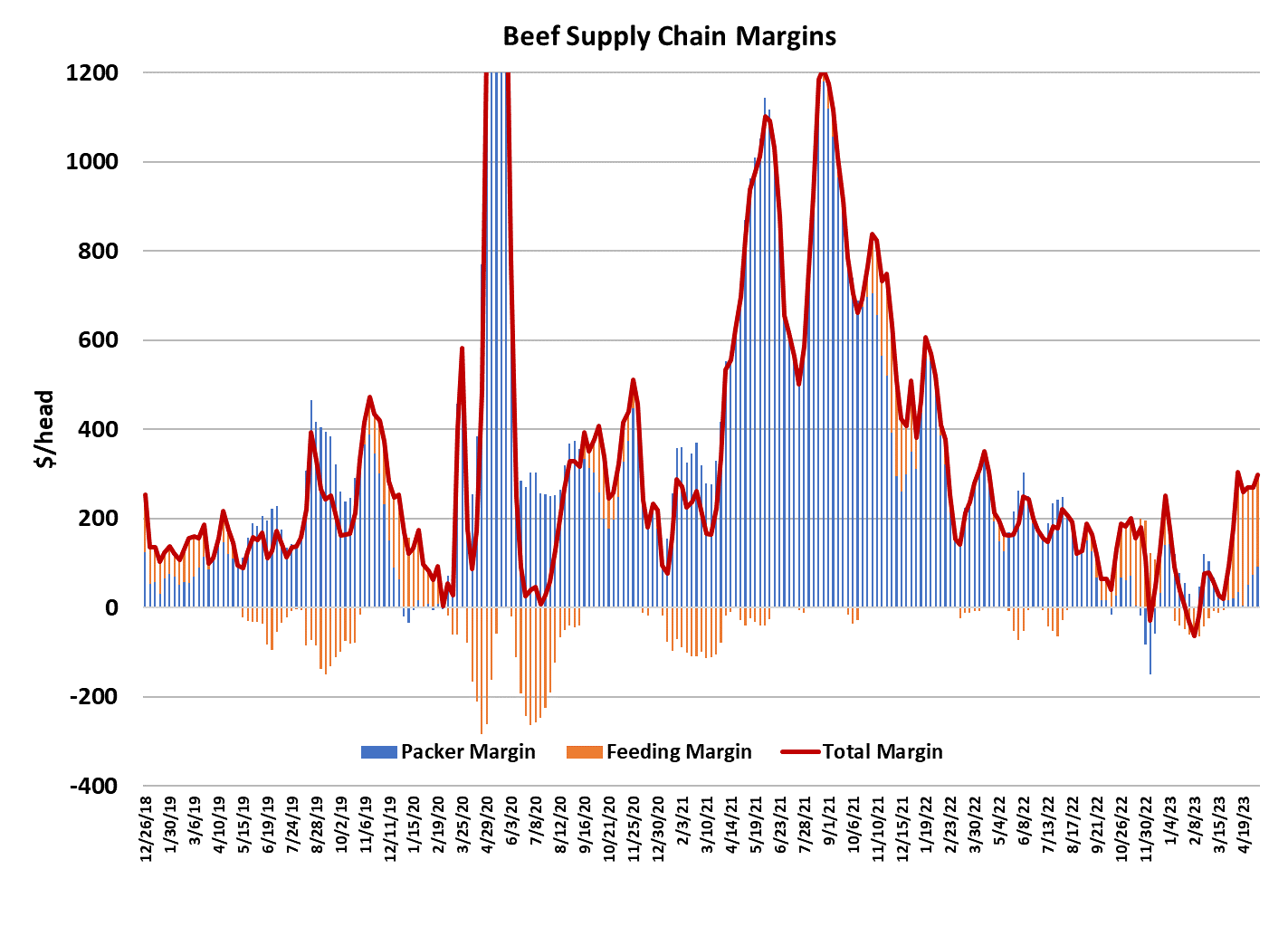

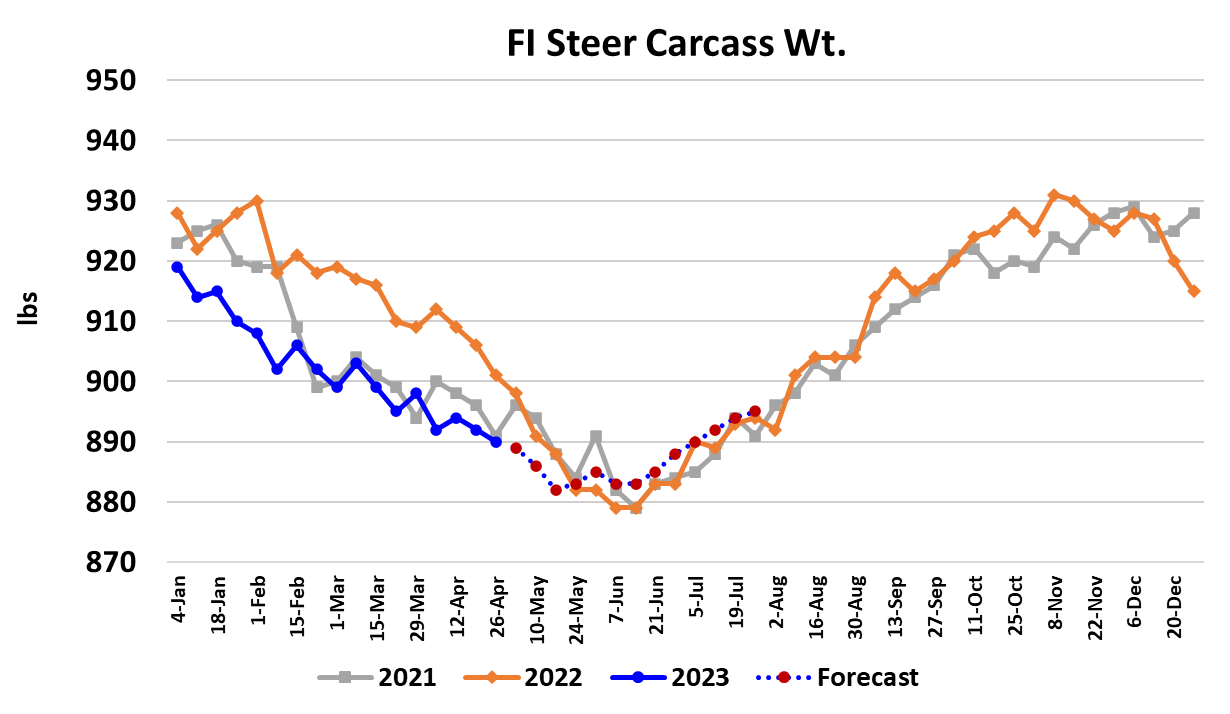

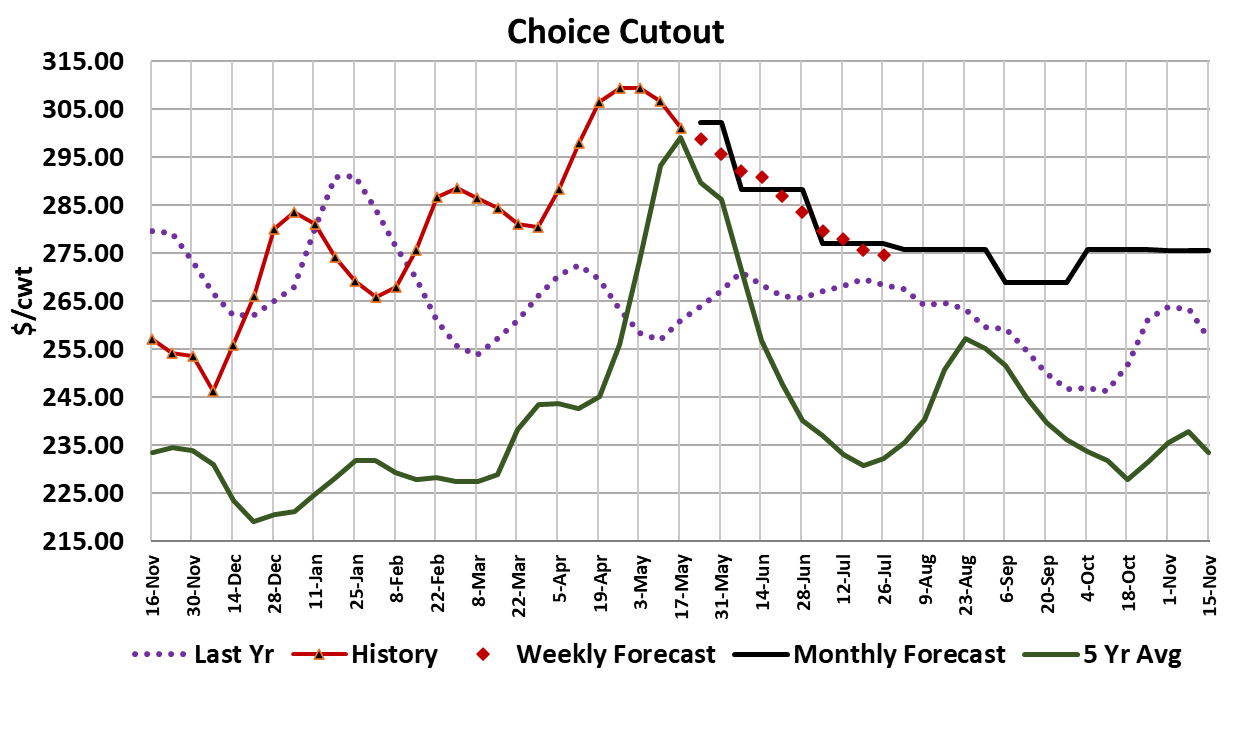

Beef packers pushed the kill harder than they should have this week, with the fed kill coming in at 503k. That is 13k over the top end of the range that our model says should be available during May and it very well could paint packers into a corner just like the large fed kill at the end of March preceded a sharp shift in leverage toward cattle feeders in April. I don’t think that this misstep will facilitate a $15/cwt. rally in the cash cattle market like we saw in April, but it could stall the downward momentum in the cash cattle market and might even cause it to tick a little higher. If that happens, there is a very good chance that Jun and Aug futures will extend their current rally. Speaking of stalling the cash market, this week’s average cash cattle price looks like it will come in around $173.90/cwt., which is almost dead on with the prior week. Transactions in the South were largely in the $170-171 range (down $1-2), but in the North cash traded $176-177/cwt., which was mostly steady with the week before. Futures traders are starting to take notice and the Board went bright green on Friday. Any steady cash trade is bullish in this environment where the Jun contract has been carrying a steep discount to cash. Last time that packers found themselves facing a stronger-than-expected cattle market, they wiggled out of it by pushing the cutouts sharply higher. The calendar was their friend back in early April, but here just two weeks ahead of Memorial Day, it is unlikely that they are going to be able to generate much additional upside in beef prices. In fact, the beef market is starting to sag, with the Choice cutout losing $2.78/cwt. on a weekly average basis and the Select cutout was down $3.72/cwt. The biggest loser in the beef complex this week was the rib primal, which dropped over $15/cwt. this week. When the ribs turn south ahead of Memorial Day, that is a pretty good indication that buying for the holiday is running out of gas. End meats have held up better than expected, even though both the chuck and round primals traded a little lower this week. I’m more than a little concerned that this week’s big kill was primarily driven by the need to fill Choice middle meat holiday orders and the extra quantity of end cuts produced will put more pressure on that segment of the market than it can bear. It looks to me like the spring top in the cutout is in and it is likely to track lower through most of the summer. Last minute Father’s Day buying could slow the decline a bit in June, but in general I think that the Choice cutout will continue to erode and will likely reach the $275/cwt. mark in July. Packer margins this week were a little over $90/head—the best margin since the first week of March. However, if the cutout continues to work lower next week as expected, then that margin could easily be cut in half on the next weekly print. I currently calculate cattle feeding margins at about $209/head, so merging that with the strong packer margin helped keep the combined margin moving higher this week, but I sense that the combined margin is very near a top and will likely move back into a downcycle within a week or two. This week USDA released its retail price data for April and it showed beef prices up 2.8% from the previous month and 1.5% stronger than last year. That data probably only caught just a small portion of the increase that is coming after the sharp rally in beef prices back in April. I’d look for next month’s month-on-month price gain to be even stronger and that probably will apply to June as well. Thus, by the time we get to the middle of June, beef production will be up from current levels and the retail price that consumers see will also be higher. That may create a market where consumer off-take is poor relative to production and thus we might see wholesale beef prices correct even lower than what I’ve already built in. Carcass weights are still coming down, with steer weights dropping 2 pounds in this week’s FI data. The seasonal bottom in carcass weights is probably still a few weeks away, but when that occurs it may be at the point where carcass weights move over last year. Right now they are still 8 pounds lighter than last year. Cattle in the north appear to be well on their way to recovering from the sloppy winter and once that process is complete, odds are that the weight gap will flip so that we will be looking at small YOY gains in carcass weights during the second half of 2023. The flow model suggests that weekly fed cattle availability should be in the 480-490k range during May and that will expand to the 500-510k range in June. By July, fed kills in excess of 520k per week could be the norm outside of holiday weeks. That is when retailers are likely to reclaim a big chunk of the margin that they lost back in April when the cutouts rallied hard. USDA will provide another COF report this Friday and it will likely show yet another YOY decline in placements during April. Beef availability is set to run 4-5% below last year during the second half of the year and that should keep the cutouts solidly over last year, but demand is likely to erode from what we have seen so far this year and that will help to contain the price increases. Beef buyers should start thinking about moving to a hand-to-mouth stance post-Memorial Day and perhaps even sooner. Next week, watch for signs that cattle feeders have gained some leverage in the cash market. If they can manage another week of mostly steady pricing on cattle, it should be considered a victory for them.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}