Beef Wrap May 27

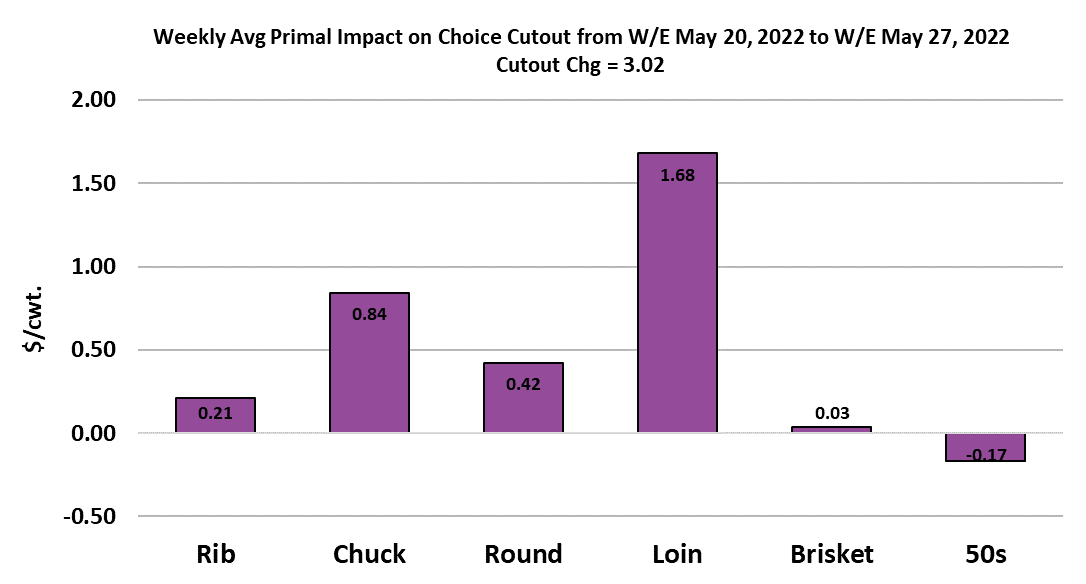

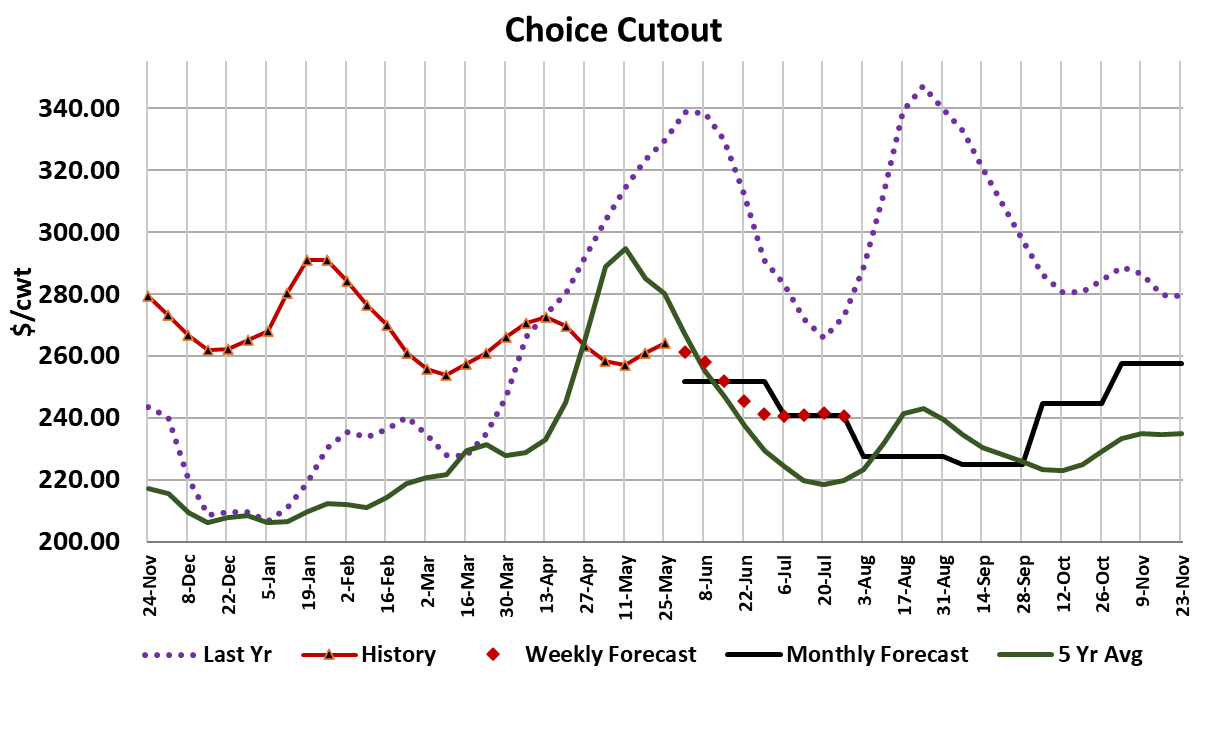

The cash cattle market continued its decline this week, losing about

$1.50 on its way to averaging $138.93. The Choice cutout gained

just over $3.00 on the week, but the Select cutout was down $0.88

cents. That makes two weeks in a row now that the Choice cutout

has printed higher for the week. Users were likely buying to

replenish in advance of the long holiday weekend and there could

have been some late purchases for Father’s Day, which is the next

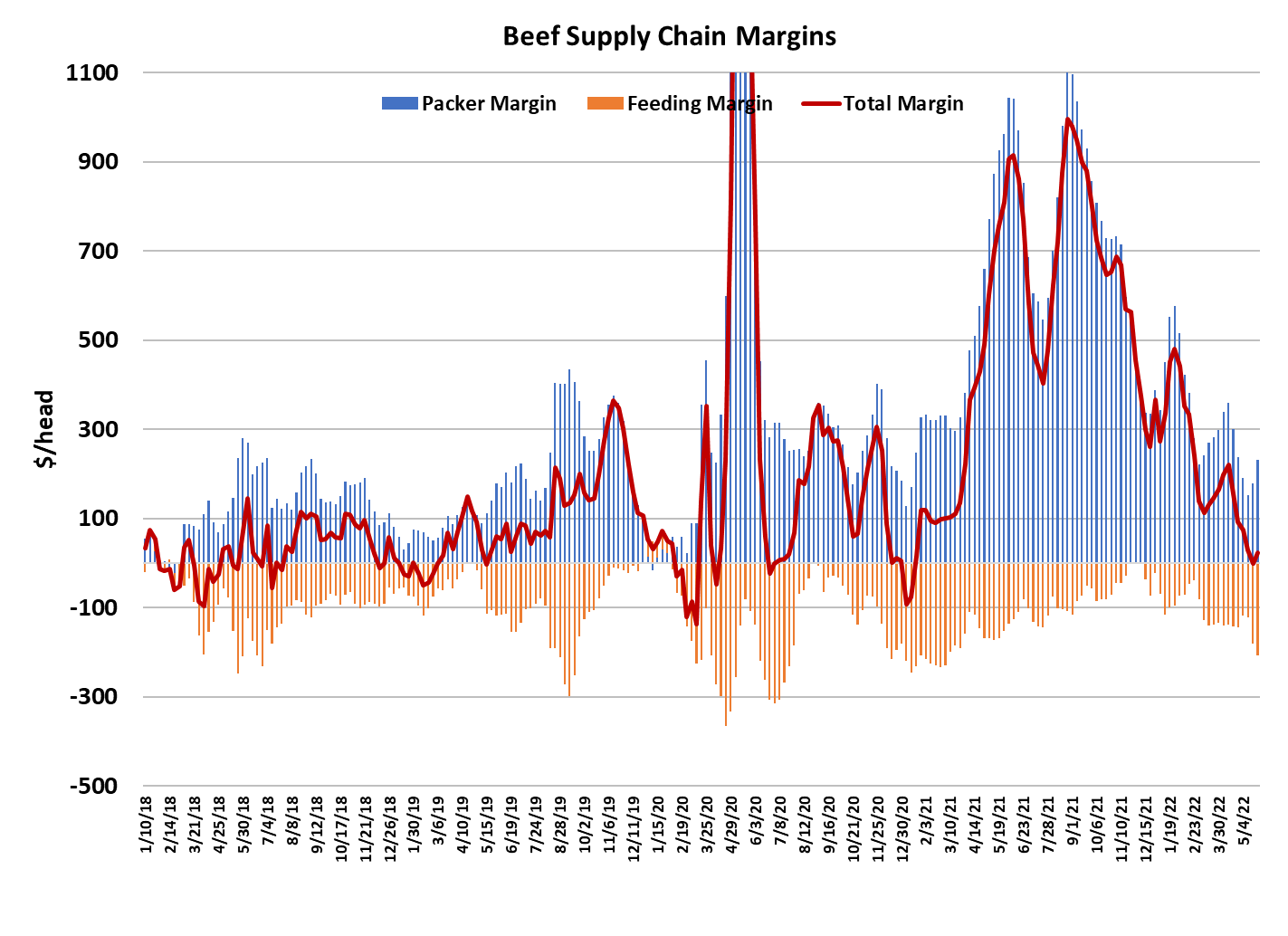

big beef holiday on the calendar. We saw the combined margin tick

a little higher this week, turning almost dead on the zero line. Next

week, the short kill could continue to support the cutouts, but I’m not

expecting a big move higher. Packers will likely schedule a very big

kill for next Saturday to partially make up for zero production on

Monday and most likely lighter-than-normal production on Tuesday.

The weather forecast across the US looks pretty favorable for the

Memorial Day weekend, thus we might expect the retail pull to be

pretty good.

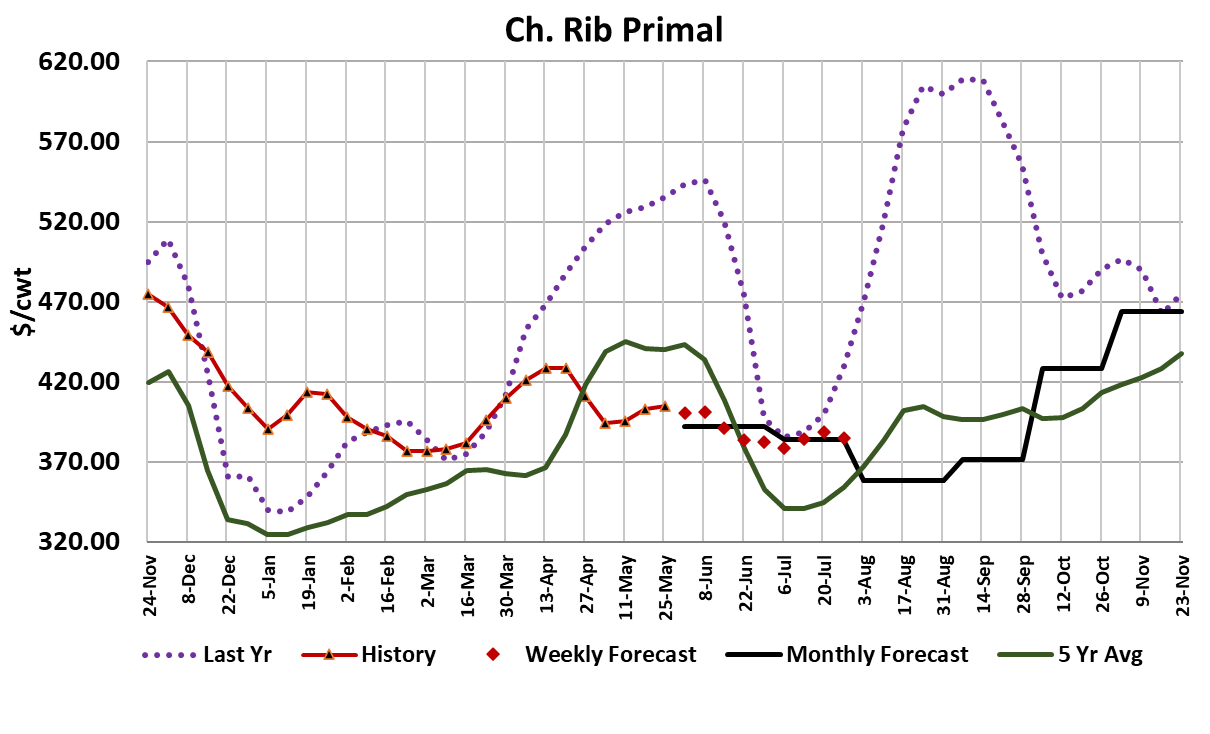

This week, it was the loins and chucks that lead the cutout higher.

Ribs seem to be dead in the water here and my concern is that after

next week, the ribs could resume their downtrend. Packers have a

relatively light kill scheduled for tomorrow as many will allow their

workers to take a long weekend. The steer and heifer kill came in at

500k, down from 534k the previous week. That makes me think that

last week’s big kill was an effort to offset some of what they were

going to lose at the tail end of this week. The cow kill was almost

unchanged from the week before at 145k. I’m projecting next

week’s fed kill at 436k and then expect packers to do about 530k in

the week following the holiday week. From there, we should see a

steady diet of kills in the 520-530k range in June and the top end of

that range could grow to 540k in July.

Right now the market seems to be able to handle fairly large

production without price concession, but that is because of seasonal

demand improvement around Memorial Day. When we get to the

middle of July, it is a pretty good bet that demand will be down

considerably and when we pair that with fed kills that could be

running 540k per week, you can see why I’m projecting the Choice

cutout to move down close to $240 in July. Demand in August is

likely to be even worse than July and thus I wouldn’t rule out a

Choice cutout at $230 or below in August. If we assume that

packers will maintain the upper hand in bargaining power this

summer (a pretty good bet given record numbers of cattle on feed

currently), then it is easy to see how cash cattle prices could be

forced below $130 or even $125 in August. If that happens it will be

a pretty dismal summer for cattle feeders.

I’m projecting cattle feeding margins in August that could be $500/

head in the red. August and September should be the low point for

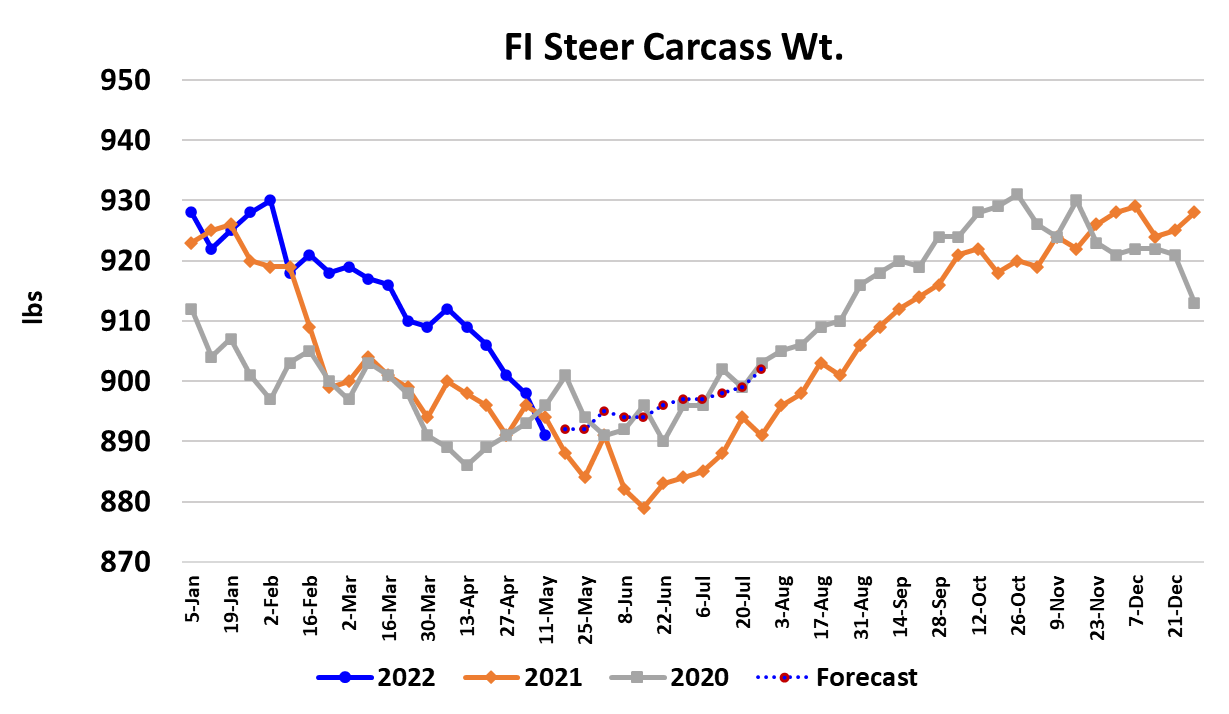

prices and demand this year, with both improving in Q4. Carcass

weights took a huge step down this week, with steer weights

reported 7 pounds lower than the previous week and heifer weights

down 10 pounds. It is not clear to me what caused the big drop in

weights because the fed kill was not particularly large in the week

that was being reported. Often when we see a big move in weights,

it will erase some of the move the following week. Perhaps that will

be the case this time. It may turn out that this week’s data

represents the bottom in carcass weights. Macroeconomic factors

are still pretty negative for beef demand, but at least the stock

market managed to have a positive week.

There will need to be several more of those in a row if it is going to

generate any meaningful improvement in consumer confidence and

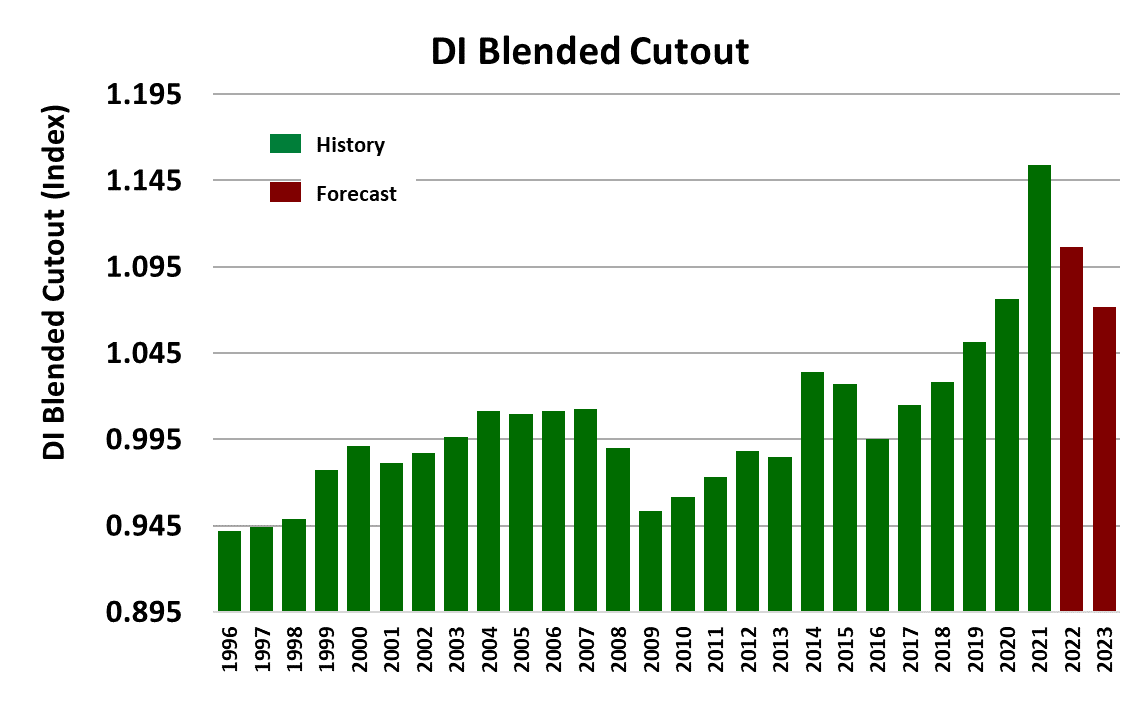

thus beef demand. As we approach the halfway point in the year, it

is pretty clear that demand in 2022 is going to be well below last

year. I’ve included a bar chart this week that illustrates just how

turbo-charged demand was last year. You can see from that chart

that I’m forecasting 2022 to be the second strongest demand on

record and even 2023 doesn’t get demand fully back down to prepandemic levels. This week’s export data was rather soft and the

most concerning feature was that beef exports to China fell below

the 3000 MT per week threshold. Just a few years back the amount

of US beef shipping into China was nearly zero and now China is a

very important trade partner for US beef.

With big production expected to flow from the beef pipeline in the

next couple of months, the last thing we need is for exports to

stumble. Packer margins improved to $230/head this week as beef

moved higher while cattle prices were lower. Margins might move a

bit higher yet, but they aren’t likely to get anywhere near last year’s

crazy-high levels. Next week, we could see some further modest

strengthening in the cutouts are retailers restock after the holiday

and packers have less product available due to the short kill. Cash

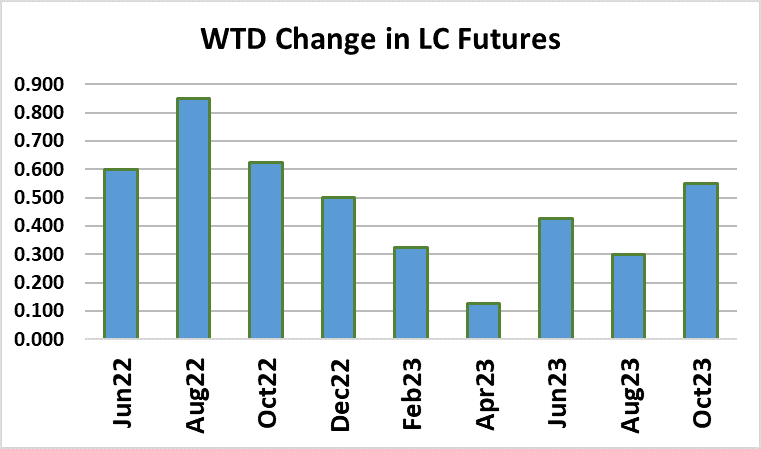

cattle are likely to remain on the defensive. The Jun futures at $132

seems achievable by the end of June, but I wouldn’t expect that it

can go a whole lot lower. That will be Aug’s job.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}