Beef Wrap May 20

The cash cattle market started to eased further this week, dropping a

little over $2 to average $140.26. The beef cutouts were higher, with the

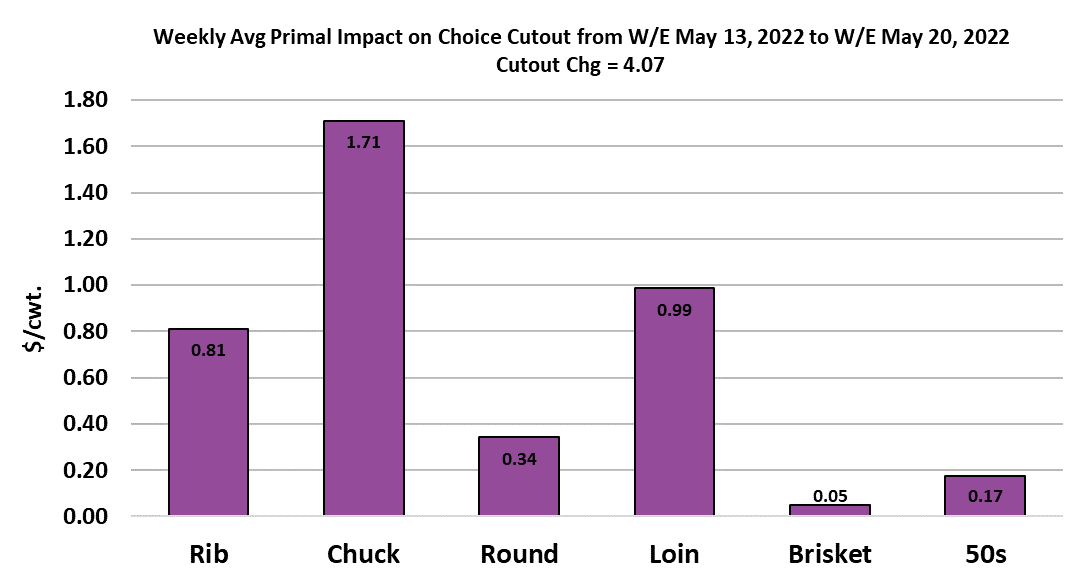

Choice gaining $4.07/cwt and the Select up $2.61. Given that this week

was the sweet spot for last-minute buying ahead of Memorial Day, it was

somewhat surprising to see the chuck primal leading the Choice cutout

higher. Ribs and loins did post some modest gains, but not nearly to the

degree that is normally expected right ahead of the start to summer. It

does make me wonder what will happen as we move deeper into

summer and the end cuts are more likely to become a drag on the cutout

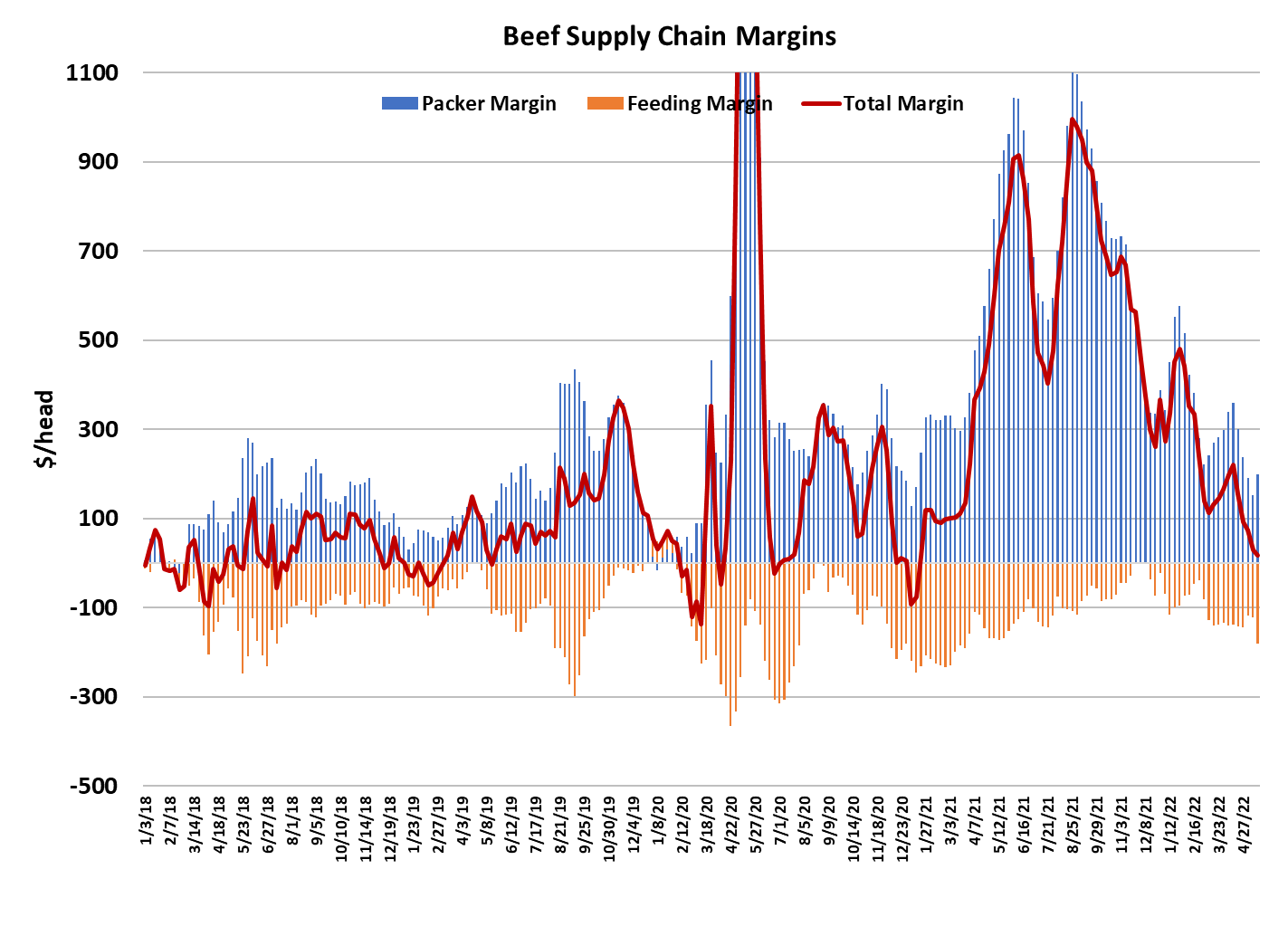

rather than a supporting factor like they were this week. The combined

margin chart tells us that beef demand is still in a downcycle and it is

approaching the zero line for the first time since January, 2020. I would

like to think that the zero line will be the point where it makes a bottom

and turns higher, but my fundamental forecasts have it continuing lower

toward a bottom around -$170 near the end of June.

With the cash cattle market now in decline, the feedyard margins should

only get worse from here and as far as the packer margin goes, this weak

showing heading into Memorial Day leads me to forecast the cutouts

lower in June and July and that will probably limit the upside potential for

packer margins. When consumer demand fades, there is simply less

margin to be shared among the supply chain participants. That

softening in consumer demand is being helped along by a sharply lower

stock market, which will make consumers feel poorer pretty quickly.

Over the past few years, a greater percentage of the population has

become involved with equity markets. That was great while equity prices

were going up, but now that they are coming down it means that a larger

swath of the population will feel the pain. Combine that with rampant

price inflation in the economy and it is easy to see why consumers might

pass by the $15/lb ribeye in the supermarket. So, even though the

cutouts ticked up a bit this week, I remain a demand bear.

On the supply side, packers put together a huge kill this week, with fed

slaughter coming in at 533k. That was 22k larger than last week. Some

of that additional meat could be meant to fill orders already on the books

for next week, but I suspect that pushing that big of an increase through

the system will likely result in softer cutouts. Of course, we will have a

short kill for Memorial Day week, so that could help to limit the supply

pressure briefly in early June. However, after Memorial Day the flow

model is telling me that weekly steer and heifer slaughter should be

above 520k per week and might even exceed 530k. By then, carcass

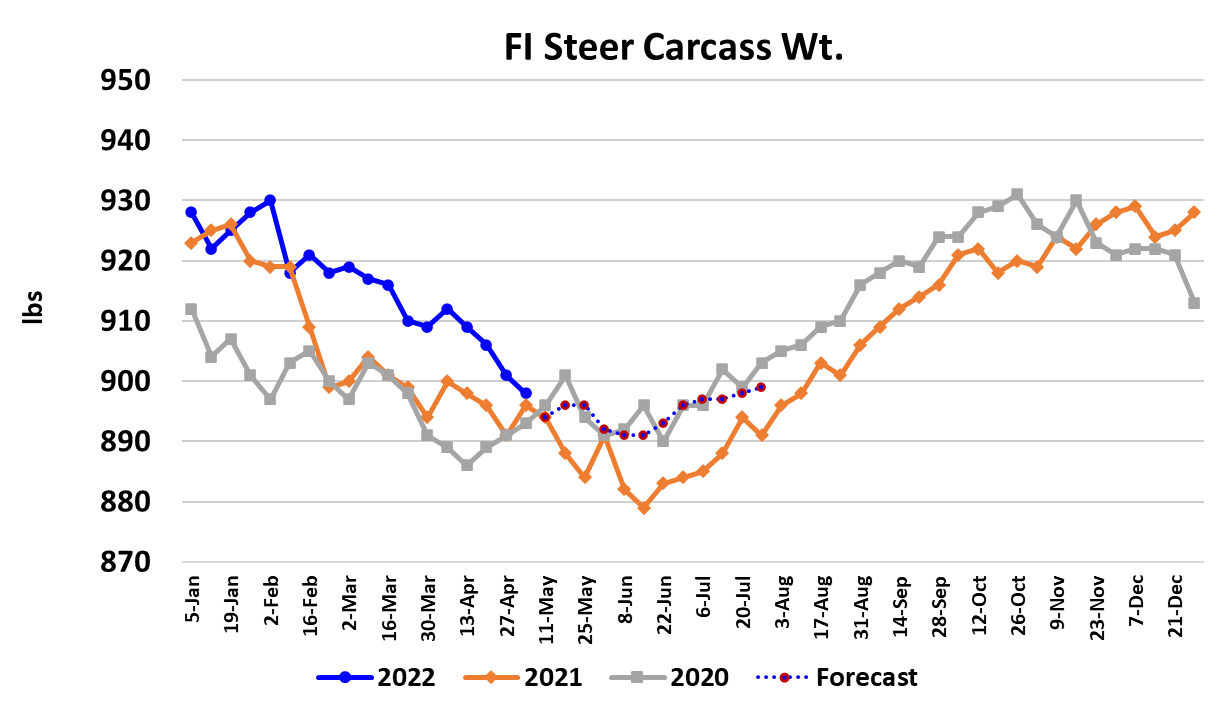

weights should be on the rise also. This week USDA reported steer

weights down 3 pounds for the first week in May, but weights normally

bottom around mid-May, so the supply side won’t be getting help from

declining weights much longer. The big kill should help to improve

feedyard currentness, but it is important to remember that packers

bought a lot of cattle with time a few weeks back and they will likely be

working through those in the near future, taking some demand out of the

spot cattle market.

And of course, we can’t talk about the supply side without discussing this

afternoon’s Cattle on Feed report, which showed April placements down

only 0.9% when analysts had been looking for a 4.3% decline. This is

the second month in a row where placements came in well above

expectations. When this happened last month, the futures dropped $3/

cwt the following Monday. A similar result is likely this time, but maybe to

a lesser degree since the futures have been beaten down pretty hard

already. All of the contracts lost ground this week, but it was the very

deferred issues that lost the most. Those are the ones that have been

showing up as way over-priced on the weekly mis-pricing charts and it

does seem that traders are now starting to adjust their price expectations

for late 2022 and early 2023 downward. Today’s COF report showed

May 1 feedyard inventories up 2% and the largest for this time of year

since the series began in 1996. That is pretty bearish in itself, but when

we also consider that it is happening at a time when demand appears to

be softening and carcass weights will soon be increasing, then it

becomes an even bigger stumbling block for prices this summer.

Fed slaughter in May has lined up very well with what the flow model

suggested and gives me a higher degree of confidence that June and

July kills will also come in close to the projection. If there is a miss, I

think it will miss to the downside because I could envision a situation

where packer margins deteriorate more than expected and packers

throttle back on the kill. If that happens, then it just pushes the supply

problem further into the future and probably adds to carcass weights

also. For much of this year, it seems that all the market pundits wanted

to talk about was how cattle supplies were going to get seriously tight

because cow kills have been elevated and we have been liquidating the

beef herd. Well, here we are almost to June and we have record

numbers of cattle on feed in a declining demand environment.

There will come a time when cattle supplies get tight and drive prices

higher, but that moment is a long way off from the present. Right now,

the industry needs to be focused on surviving the next few months of big

supplies and softer demand. It would really help if retailers would

aggressively lower price levels, but they are typically slow to do that and

not inclined to do it in May/June when historically consumer demand has

been the best. I’d look for bigger retail price reductions in July and

August. Next week, we will be watching closely to see how the market

handles this week’s big production. I’m forecasting the cutouts a little

lower and the cash cattle market to pull back another couple of dollars.

Monday’s futures market reaction to the COF report should help get the

ball rolling in that direction.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}