Beef Wrap June 3

The cash cattle market continued lower again this week, averaging

$137.84, which was down about $1.25 from last week’s average.

The holiday on Monday reduced beef production for the week and

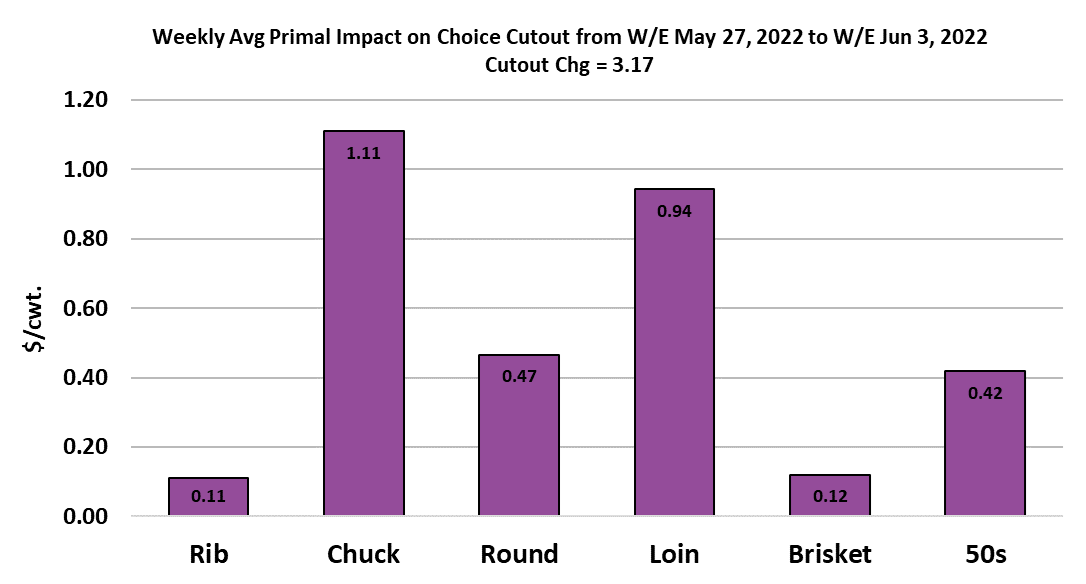

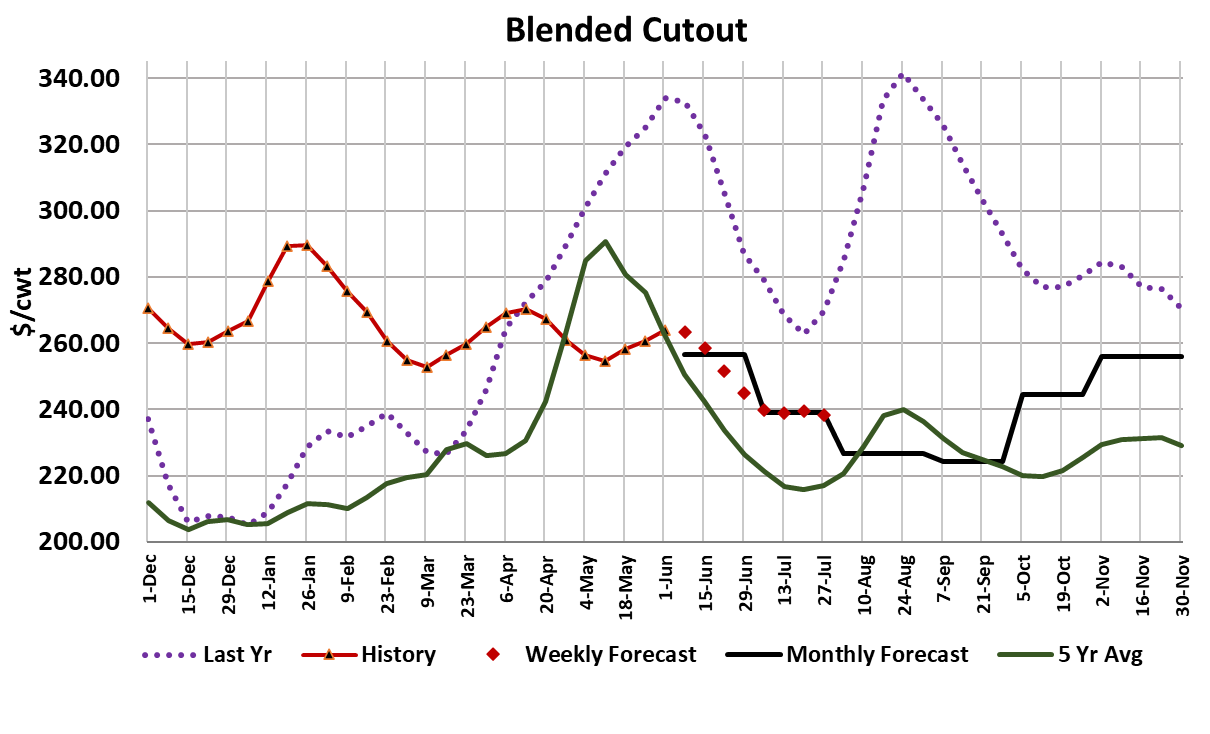

helped to support the cutouts. The Choice cutout added $3.17/cwt on

a weekly average basis and the Select was up $4.39/cwt. Futures

traders were excited to see the cutout continue on its upward

trajectory, and they added about $1.50 to the Jun and Aug contracts.

The gains were even bigger in the deferreds, which was a bit of a

reversal from earlier weeks where traders seemed to want to extract

some of the premium that had been built up in the late 2022 and early

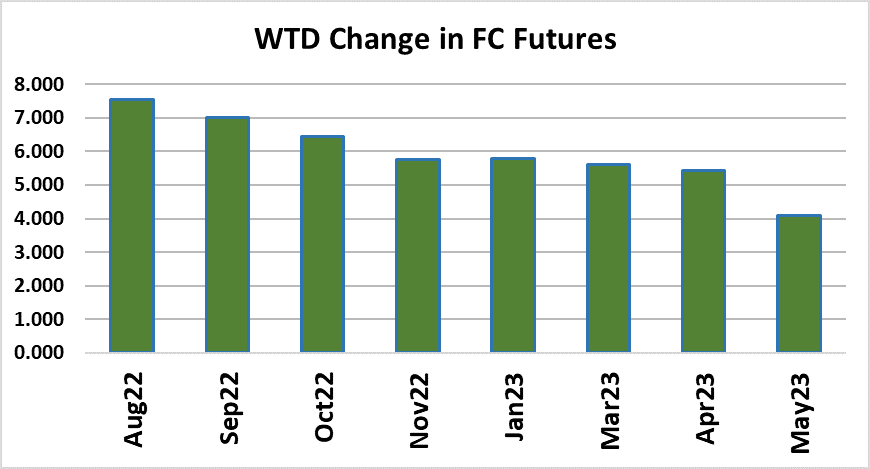

2023 contracts. Traders were also very enthusiastic to buy feeder

cattle futures, with the Aug and Sep contracts up over $7 on the

week. I’m not really sure all of that enthusiasm is warranted, but after

dismal showing of the beef market leading up to Memorial Day, it isn’t

surprising to see a bit of over reaction to a little good news.

Keeping that good vibe going will be the challenge for next week,

when packers will have a lot more production to move through the

system. Packers are planning on a huge kill tomorrow at 96,000

head, with probably more than 75,000 of that being steers and

heifers. Further, the daily kills this week were very strong and we saw

one day where the estimated fed kill was 101,000 head. I think they

are likely to keep the daily kills close to that level again next week, but

next Saturday will likely be closer to 50k. I’m forecasting next week’s

fed kill at 528,000 head, which would be 50,000 more than what they

did in the current holiday-shortened week. If that forecast comes true,

it would be the largest steer and heifer slaughter week so far in 2022.

Will demand be strong enough to handle that without any price

concession? I don’t think so.

Demand has probably improved a little bit in recent weeks, but at

least part of the recent price gain must be attributed to the reduced

kill. The combined margin is climbing higher, which indicates that

beef demand is on the rise, but we need to keep in mind that the last

2 upcycles in the combined margin were relatively short. My guess is

that this one will be also. There may be some last-minute Father’s

Day buying to get done early next week and if there is, it will likely be

focused on the middle meats. This week’s buying was all about

replenishing following the long Memorial Day weekend. Now

summer is on in full force and that means that consumers will be

hitting the road and taking vacations. That type of activity tends to

boost demand at QSRs and thus ground beef should do well. With

what consumers are having to pay for gas, they will be more likely to

skip the full-service restaurant and go to the QSR instead.

The gains in the cutout were spread across the carcass, which is

another sign that at least some of the price lift came from smaller

production. There is always a lot of enthusiasm around the beef

complex at the beginning of summer. Maintaining that into July and

August is often a challenge, however. Another feature of the supply

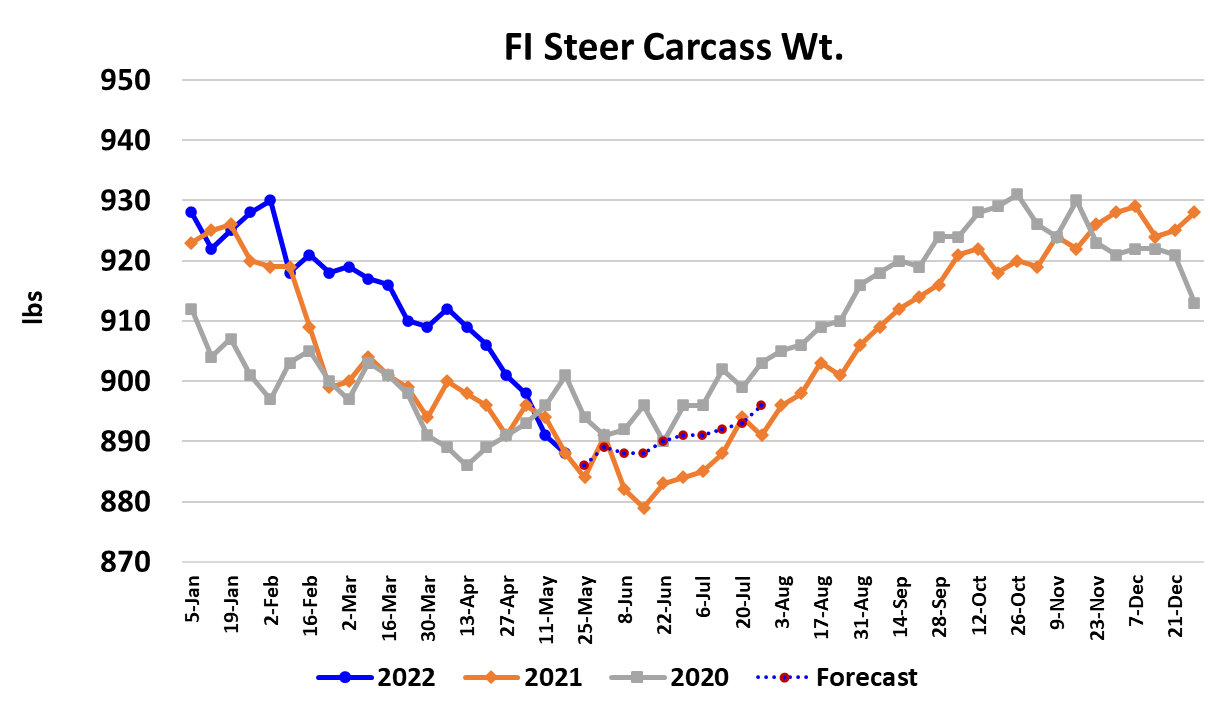

side in the last few weeks has been the rapid decline in carcass

weights. The last two weeks have seen 10 pounds come off of steer

weights and that is a bit unusual since weights are normally

bottoming and turning higher in May/June. It is a very welcome

development since the DTDS weights had been very high earlier this

spring and that had me thinking that producer leverage was going to

be non-existent this summer. The leverage meter is still likely to

point in the packer’s favor for most of the summer, but it won’t point

as strongly as it would have had weights not dropped so hard in May.

The passing of Memorial Day has done very little to help the

macroeconomic picture in the US. The stock market continues to be

volatile and on a mostly downward trajectory. Price inflation is still

strong and now gas is routinely over $5/gallon in many parts of the

country. That alone is enough to make consumers feel miserable,

but we have also had to deal with repeated incidents of gun violence

against innocents and that is also casting a bit of a pall over the

normal celebratory mood that comes with the start of summer. So, I

can think of a lot of reasons why beef demand might be tempered.

Packer margins this week were $265/head, up about $50 from the

week before, thanks to rising beef prices and falling cattle prices.

Packers should find it relatively easy to maintain a $200-400/head

margin on the cattle they buy this summer given that feedyards are

full to the brim. Producer margins, on the other hand, are likely to

slip deeper into the red as the summer wears on.

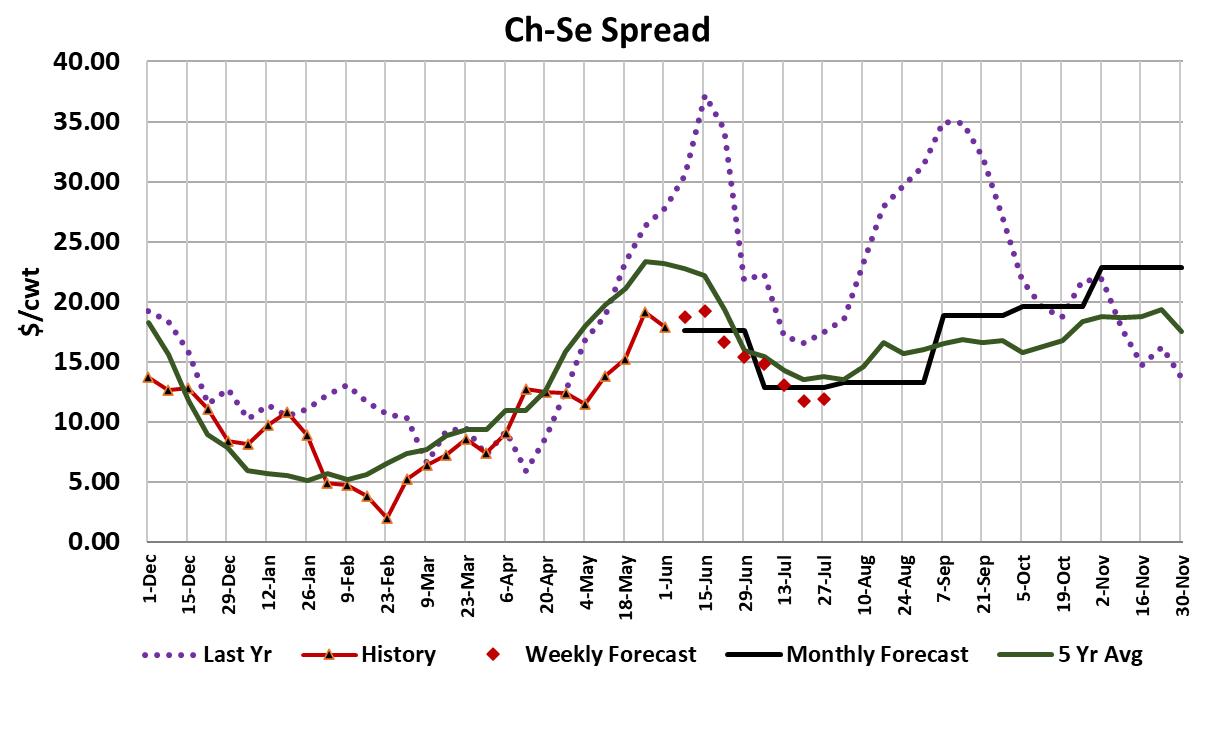

One interesting feature of the spring market this year has been that

the Choice-Select spread has held well below historical norms for this

time of year. The spread normally peaks around Memorial Day and

then works lower into August and that is likely to be the case this year

too. In all, it looks like the cattle and beef complex is in pretty good

balance right now but the overarching theme of eroding demand in

the post-pandemic era remains in place, even though we are seeing

a small upcycle in demand currently. By the time we get to August,

I’m looking for the cutouts to be around $25/cwt lower than today’s

levels and cash cattle to be trading into the mid $120s. Next week,

watch the cutouts for signs that they are struggling under the

production rebound and watch the trims and grinds for signs that

demand through QSR channels is picking up.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}