Beef Wrap May 26

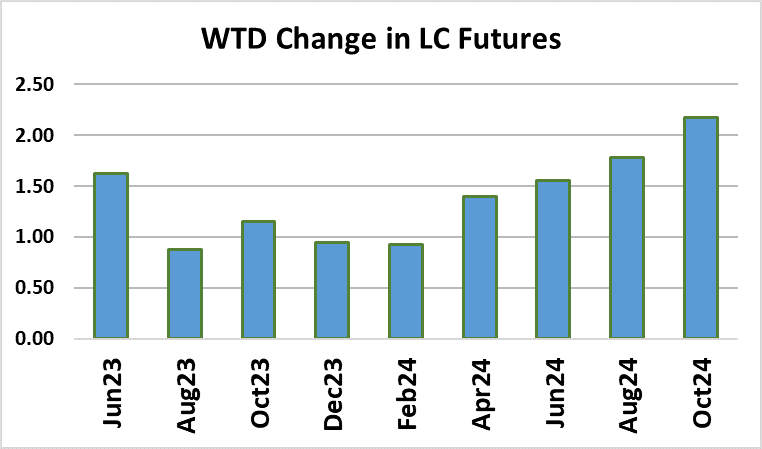

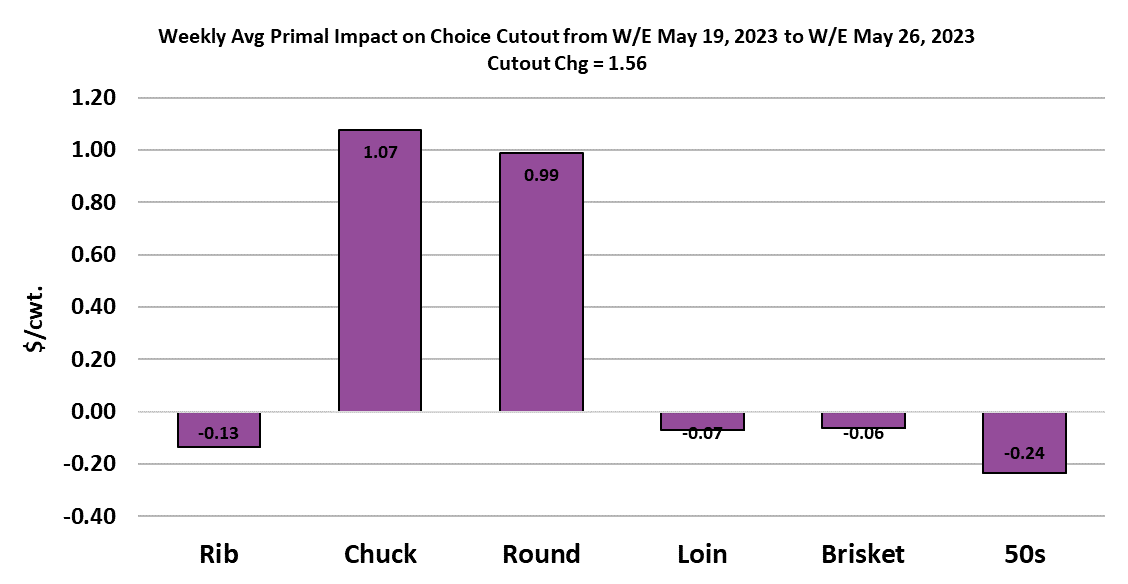

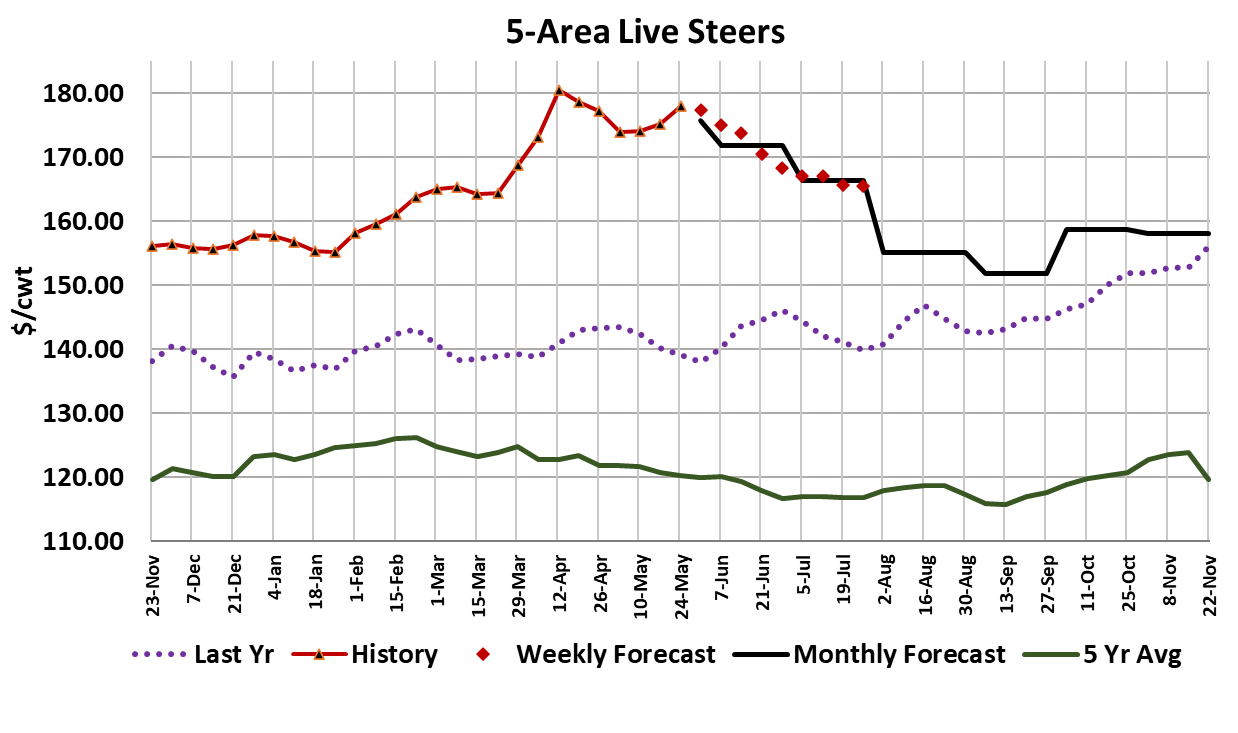

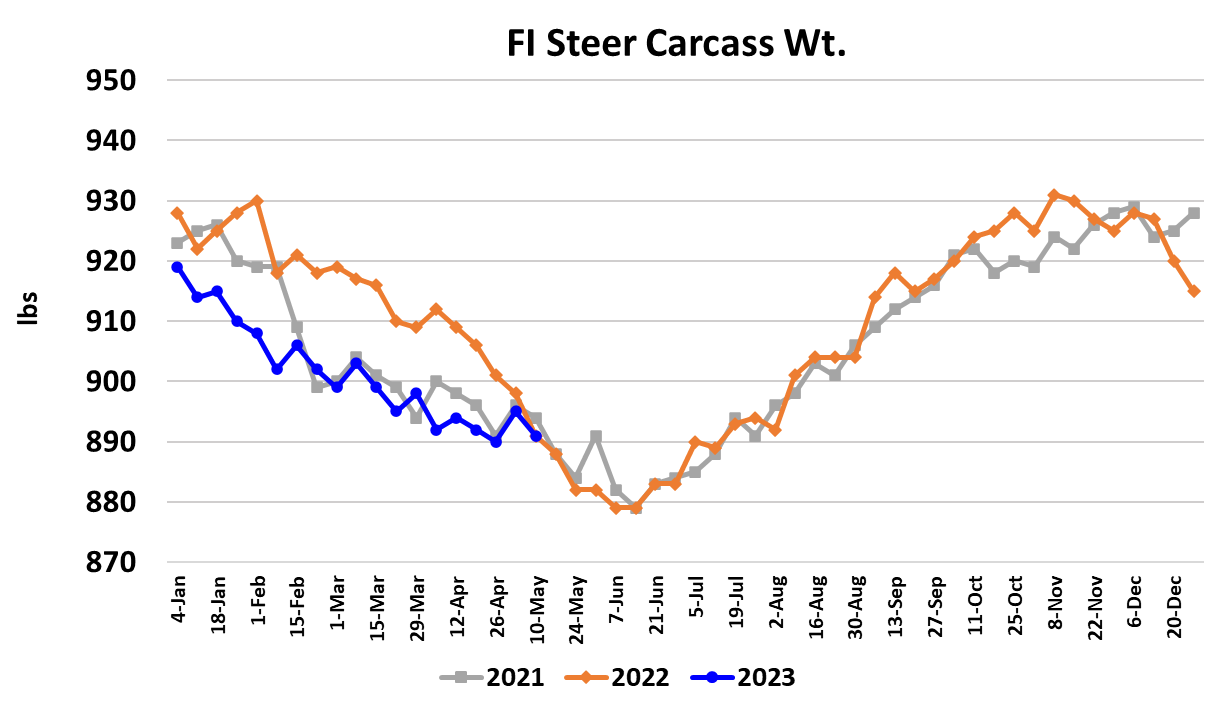

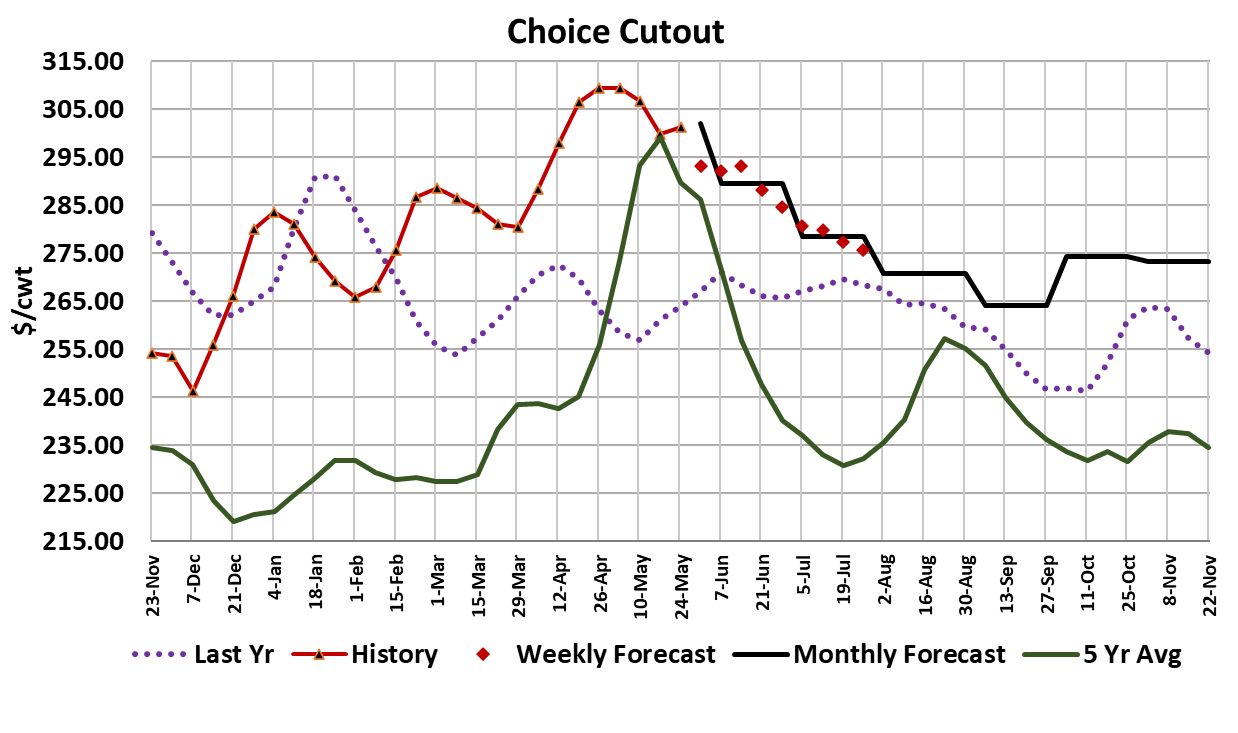

This was a week where there were plenty of reasons why the cash cattle market should have traded lower. Packers were buying for a short kill the following week and they were going to have access to their June contract cattle in just a few days. Instead, cattle feeders surprised everyone by digging in and demanding more money from packers. The average cash cattle price was close to $178/cwt., almost $3 higher than last week’s cash average. The biggest gains were in the North, up $3-4/cwt. and trade in the South was about $1 higher at $171. The flow model has been telling us that available cattle supplies were going to remain tight here in May and since packers have pushed the fed kill beyond what should be available in the last couple of weeks, it set up a situation where cattle feeders had improved leverage. Perhaps packers will be a little more cautious going forward about overkilling the available supply. This week, packers dialed back the kill on Friday and Saturday to give workers a little more time off on Memorial Day weekend. The fed kill registered 487k, down 17k from the week before. Next week, there will be no kill on Monday, but packers are likely to run a big Saturday to make up some ground. I have next week’s fed slaughter at 460k. That will help to tighten up beef availability, and could limit the near-term downside risk in the cutouts. There will probably be some last minute buying ahead of Father’s Day in early June that should be mildly supportive to the middle meats. The chuck and round primals saw the biggest price gains this week and that helped the Choice cutout to eek out a $1.56/cwt. gain on a weekly average basis. The Select cutout was down $0.30/cwt. The forecast has both cutouts moving lower in June as demand should start to moderate by the middle of the month and available cattle supplies should be increasing throughout the month. Today the Choice cutout is at $303/cwt., but I think it could easily be at $285/cwt. by the end of June. July will bring even better fed cattle availability and probably softer demand too, so that should keep the cutouts on a downward trajectory for the next couple of months. This week June LC futures gained $1.62 and finished on Friday at $167.35/cwt. That implies that traders are expecting cash prices in the Southern Plains to lose about $4/cwt. over the next five weeks. That seems reasonable to me, but it probably won’t be a dollar-a-week kind of move. Instead, look for some steady weeks and some where the price declines a couple of dollars. Steer carcass weights were reported down 4 pounds this week, so the seasonal downtrend in weights remains intact. However, weights should be getting close to a bottom and then will work higher into October. With fed cattle availability improving in June and July and carcass weights rising, overall domestic beef supplies should become more plentiful, pushing prices for most items lower. Domestic beef demand still remains quite good, in contrast to pork demand, which is near all-time lows. It seems reasonable to think that whatever has slammed pork demand this spring will eventually infect beef demand. Hopefully, the politicians in Washington can work out a compromise that keeps the US from defaulting on its debt and thus sending equity markets into a freefall. That is the most immediate danger to beef demand. If a deal isn’t struck quickly, the Treasury

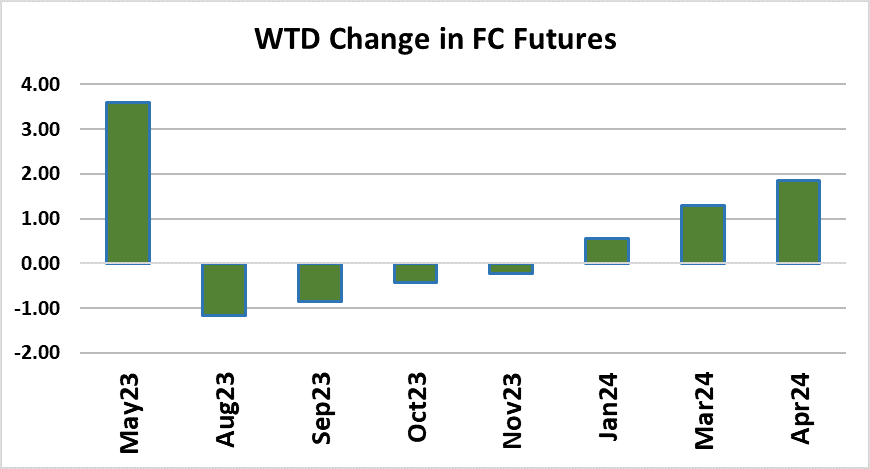

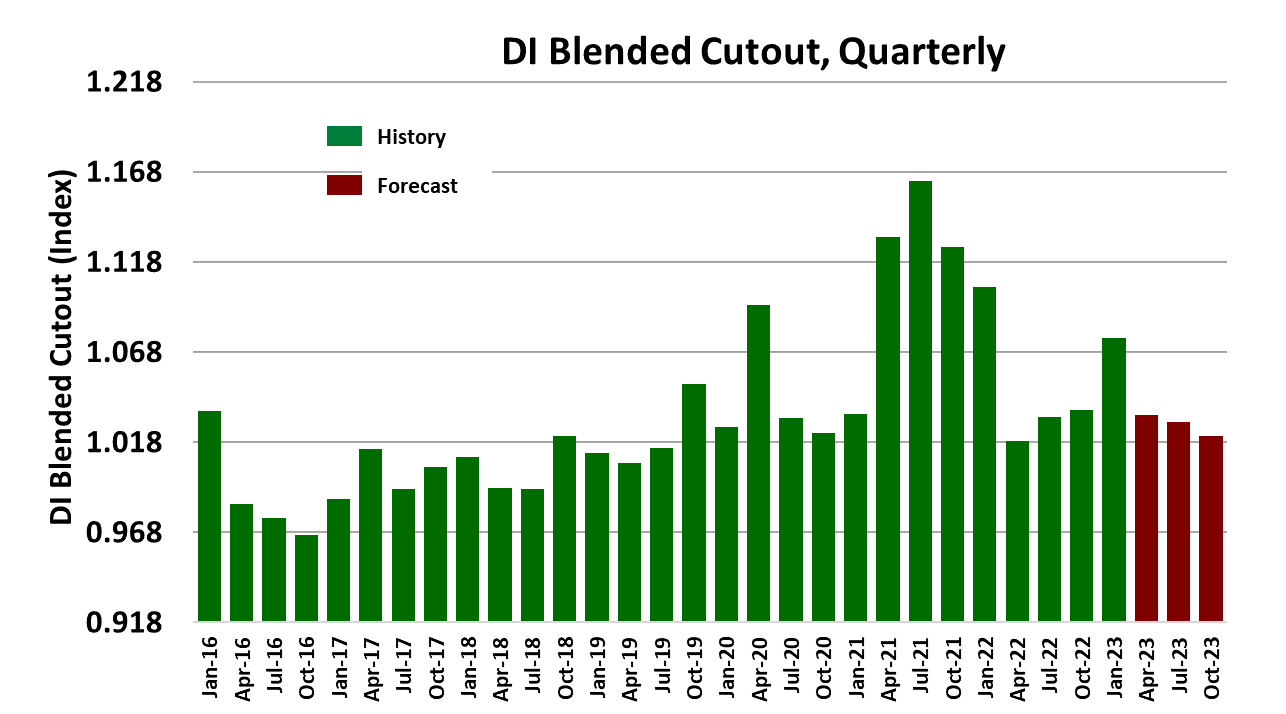

Department may end up having to delay some government benefits like Social Security or food stamps and that would have a direct impact on consumer’s purchasing power. I’m estimating the beef demand index to average about 1.055 for the first half of 2023, down from 1.062 in the first half of last year. I’ve got the demand index dialed back 1.035 in the second half of this year, mostly on the expectation that macroeconomic conditions will deteriorate as we move deeper into 2023. That is a big reason why the Aug, Oct, and Dec contracts are showing as over-priced currently. If we assume that demand in H2 is going to be the same as H1, then the futures may be justified in the value it is placing on the deferred contracts. Cattle supplies are going to continue to tighten and placements into feedyards are likely to remain well below last year’s level for the foreseeable future. Cattle feeders have been paying some relatively high prices for feeder cattle recently and that is going to translate into cattle later this year that need to sell for $170-180 just to breakeven. I’m not sure that the demand side of the beef market will be strong enough to support that type of cattle pricing later this year, but I could be wrong. As cattle supplies shrink, packers may continue to fight the market share battle and that could keep cattle prices higher that what I’m envisioning right now. Corn has taken a turn higher in recent days and that will just add to the breakevens on already-expensive cattle in feedyards. Next week, watch for some modest strength in the cutouts as less beef will be produced due to the holiday. I’d be surprised if cattle prices leg up again next week, but it is not outside of the realm of possibility.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}