Beef Wrap June 2

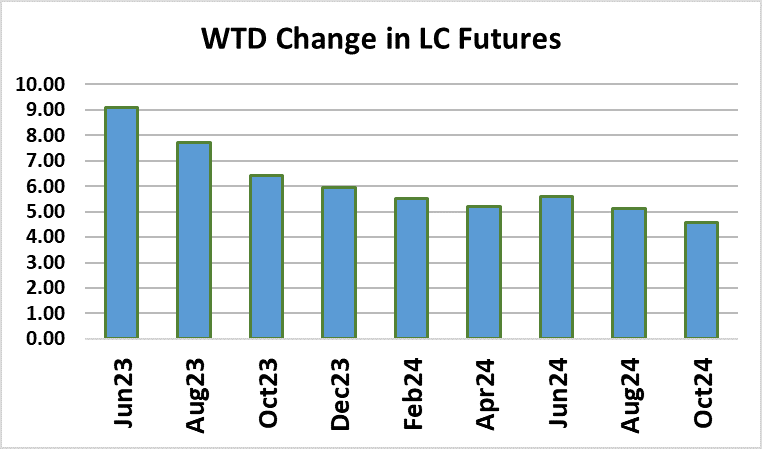

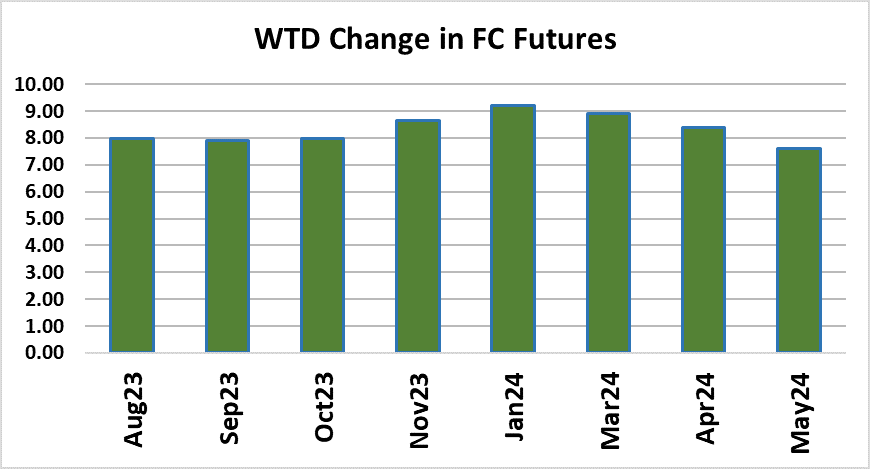

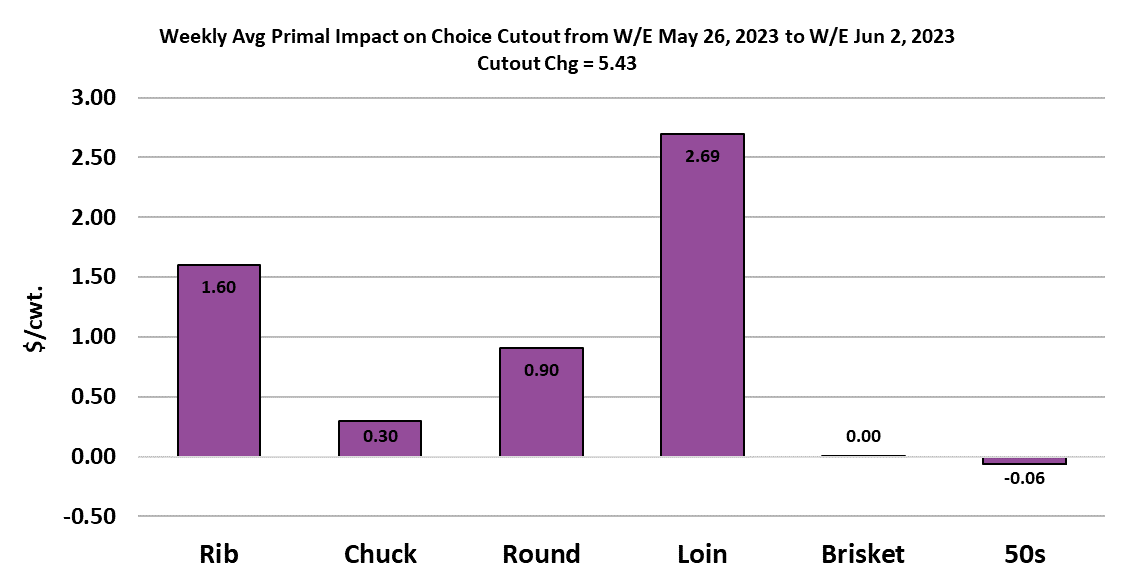

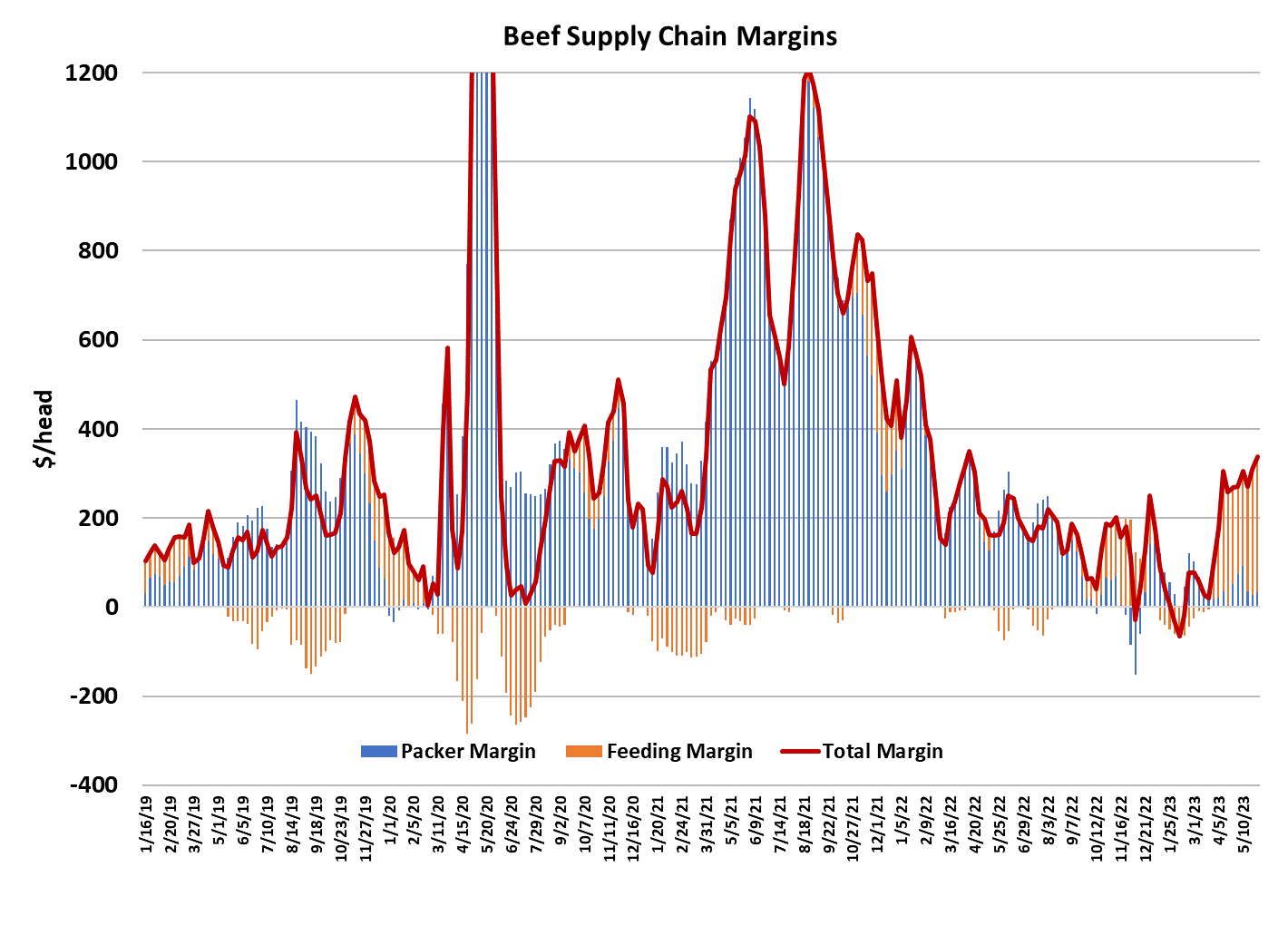

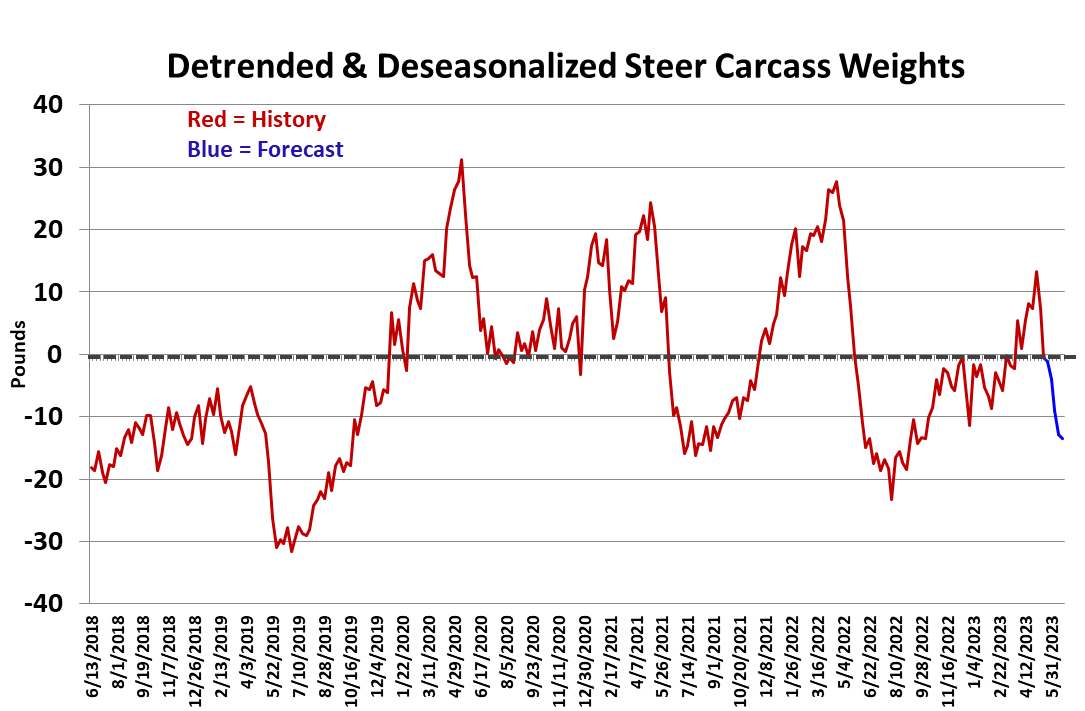

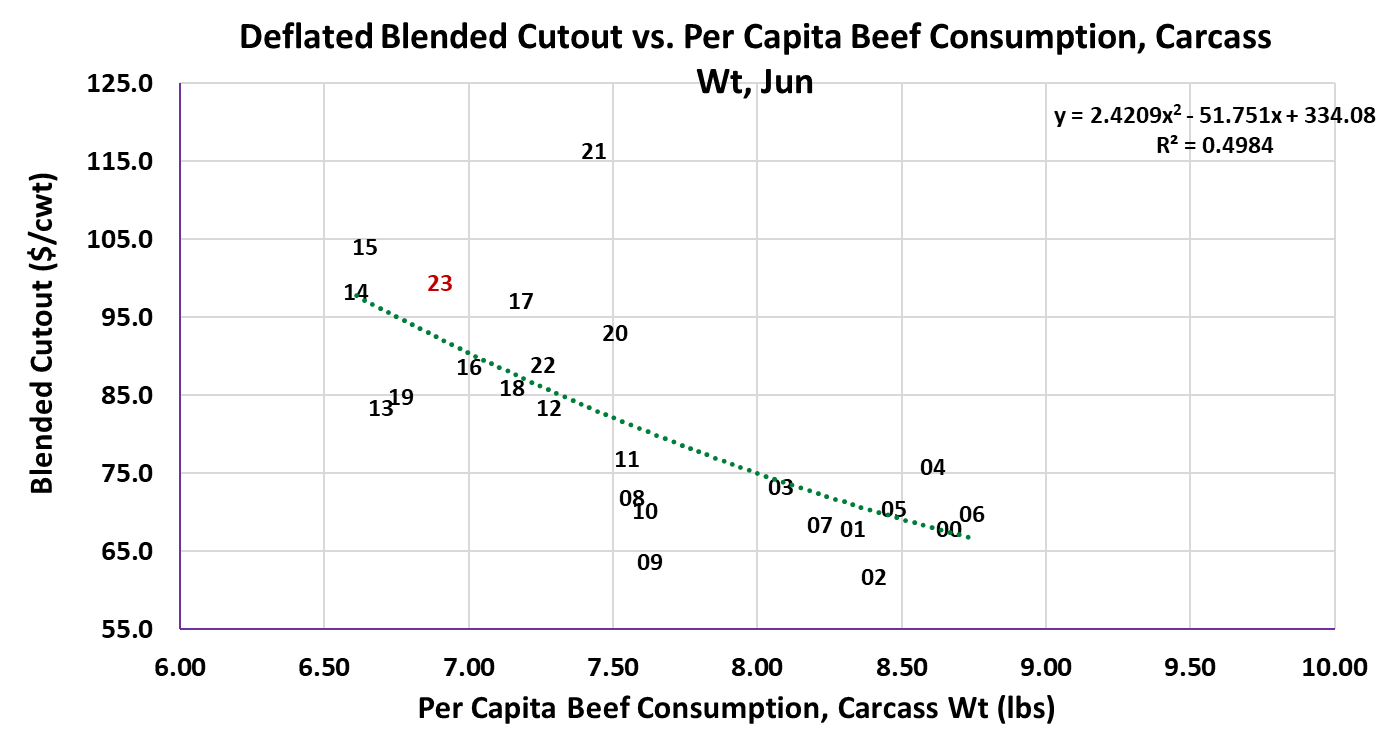

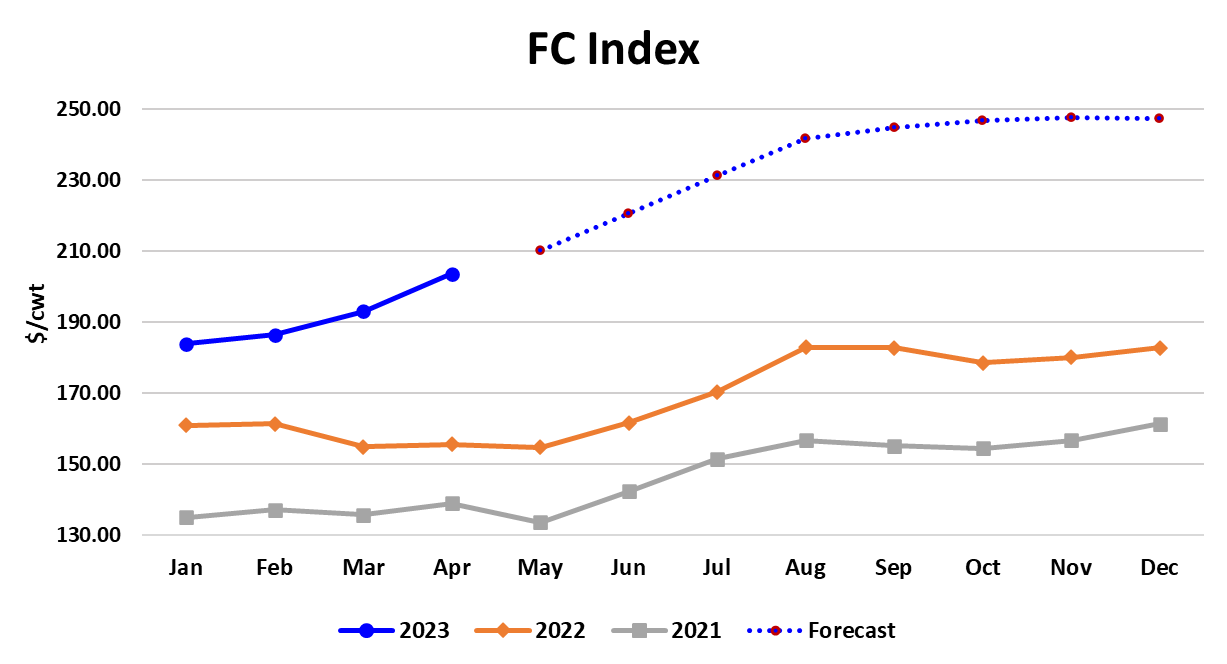

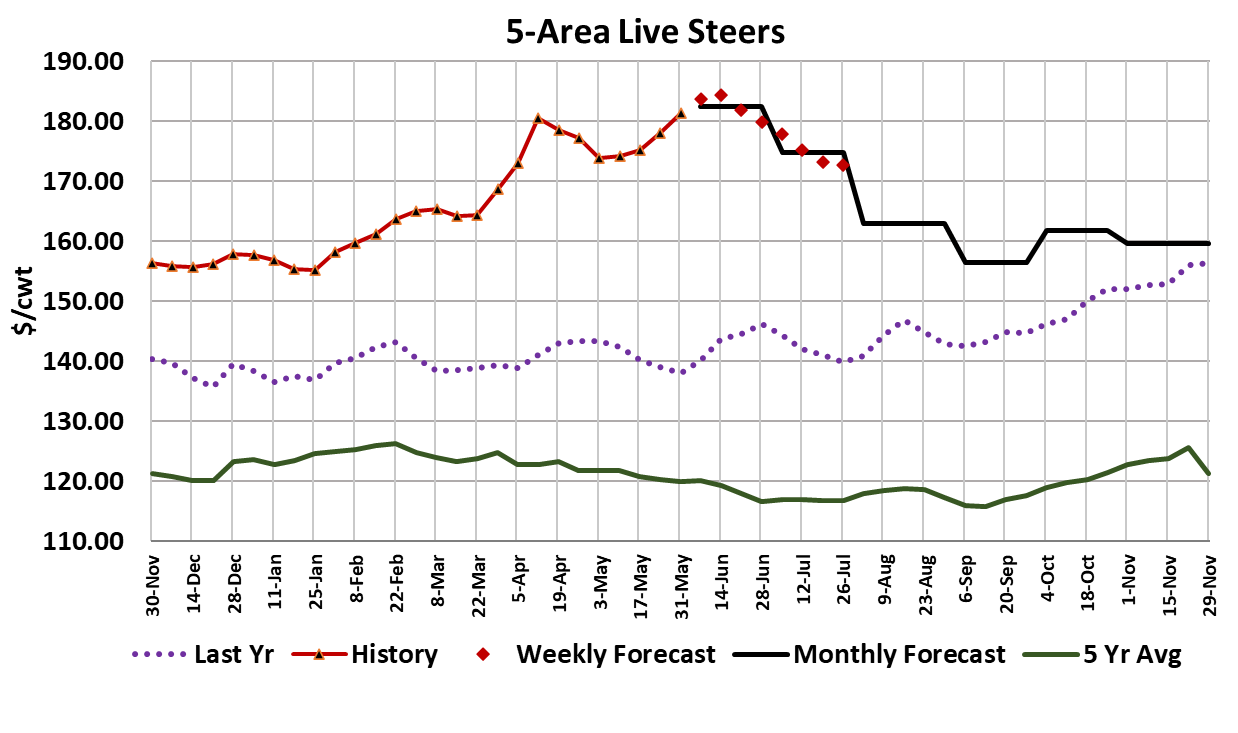

The cash cattle market caught fire again this week, with price levels in some instances surging $8-9/cwt. Trade in the North occurred in the $185-188/cwt range and in the South prices ranged from $175-180. Recall that last week’s southern trade averaged around $171. What caused packers to suddenly chase after cattle like there is no tomorrow? For several weeks now we have emphasized that cattle numbers were tighter than most people figured and apparently that coincided with packers strong need to replenish beef inventories following the holiday weekend. It isn’t just that numbers are tight, carcass weights are still coming down at a good clip. Feedyard currentness has improved a lot also. The attached chart gives the de-trended and de-seasonalized steer weights and you can see how abruptly they moved lower in recent weeks. That steep downtrend is expected to continue for at least a few more weeks. For packers, there is only one thing to do: get on the phone Monday morning and inform beef buyers that they will be paying a lot more for beef going forward. If this feels like deja vu, that’s because a similar thing happened back in early April when cattle prices suddenly jumped higher. In that instance, packers ran the Choice cutout up from $280/cwt. To $310/cwt by the end of April. Will buyers just throw in the towel and pay whatever the packers are asking? In the short run, yes, and it has already started, with the Choice cutout adding about $5 on Thursday and Friday alone. However, once buyers have had a chance to adjust, further increases might be difficult to come by. International buyers will almost certainly start to back away from the US market. Domestic buyers that have immediate needs ahead of Father’s Day and July 4, will have to pay up or go without. Even with some gains in the beef market, packer margins are likely to swing deep into the red next week when those pricey cattle show up for slaughter. I have this week’s margin near +$35/head, but next week it might easily be -$35/head. Cattle feeding margins, on the other hand, topped $300/head this week. As you might imagine, this surge in fat cattle prices has spilled over into the feeder cattle market and the Aug FC futures finished the week at almost $242/cwt. Keep in mind that the May FC contract just expired at $209/cwt., so traders are betting that in just three short months the cash feeder cattle market will add close to $33/head. That seems like an awful lot, but it is almost never a good idea to bet against a cattle feeder with a bunch of fresh money in his pocket. Of course, to get there corn prices will need to come down further by the end of summer, but that seems like a pretty good bet. This week, it was the ribs and loins that provided the most support to the cutout and that probably involved some last-minute orders ahead of Father’s Day. Fat trim prices have eased a bit, last quoted near $180/cwt., but with weights still coming down and feedyards very current, they may hold at these very high levels longer than most expect. In general, domestic beef demand has remained very good. The attached scatter for June indicates that my forecasts are projecting better demand this year than last. That is impressive. I bet the hog producers wish they had a scatter like that. The combined margin see-sawed sideways for a bit, but now looks like it will continue higher. It has been over a year since the combined margin was at these levels. Of course, all of these gains in cattle and beef prices are telling retailers that they need to continue pushing retail prices higher. That probably needs to happen in order to better align consumption with tightening beef supplies. This week’s fed kill registered 461k due to the holiday on Monday, but I expect packers to slaughter a little over 500k next week. The flow model has been suggesting that cattle availability would improve in June and July, but packers overkilled for a few weeks in April and May so maybe that growth in available supplies will be delayed a bit. That raises the possibility of perhaps another cattle price increase again next week. Once all of data is available, I expect this week’s cash cattle price to average close to $182, so $183 or $184 next week is certainly do-able. It is important to remember that because of the lag in retail price hikes, consumers are not yet seeing the full impact of recent wholesale price increases. As a result, they tend to consume more than they would if retail prices were more reflective of the increase in wholesale price. The debt ceiling fight in Washington was resolved this week without a default. Amazingly, the moderates and deal makers were able to deftly outflank the extremists in both parties an put forth a compromise to avert catastrophe. The stock market signaled its approval today with a 700-point gain in the Dow. The economy may still yet slip into a recession later this year and that would be detrimental to beef demand, but that is much preferable to the chaos that a default would have caused. Part of the compromise involves restarting payments on student loan debts in August and that stands out as a big risk for not only beef demand, aggregate demand across the economy. For now however, the mood is uplifting. Summer is here and its time to grill. Next week, watch the cutouts to see how much trouble packers have in passing along their increased cattle costs. Expect cattle feeders to come out of the gate looking for yet another price increase.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}