Beef Wrap May 19

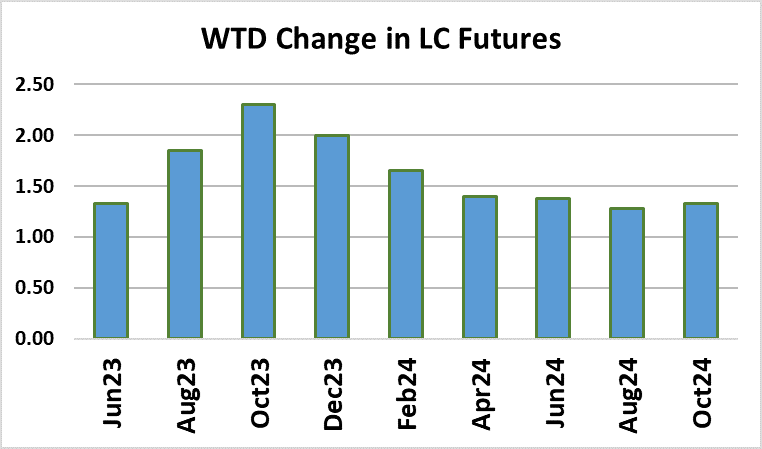

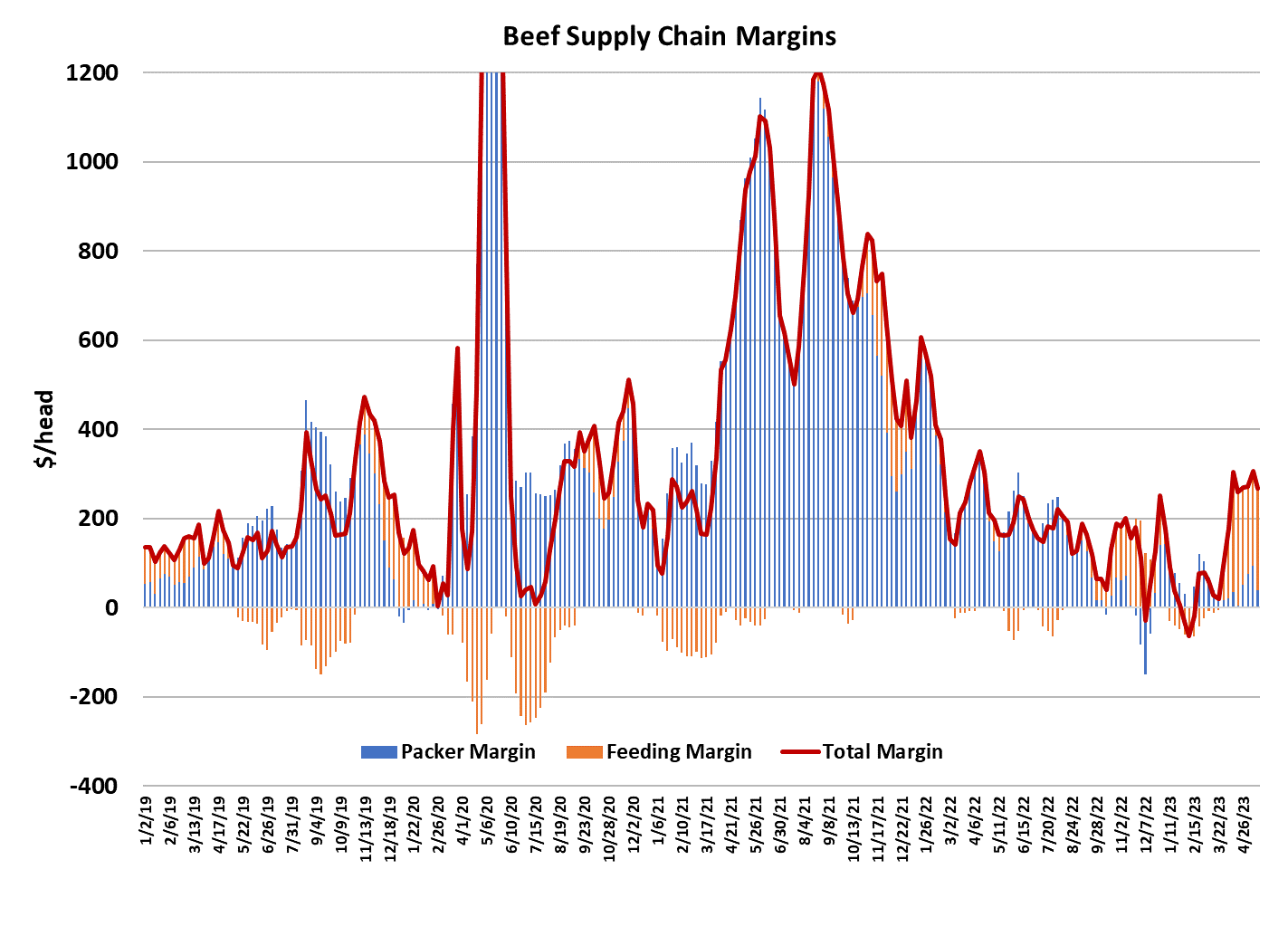

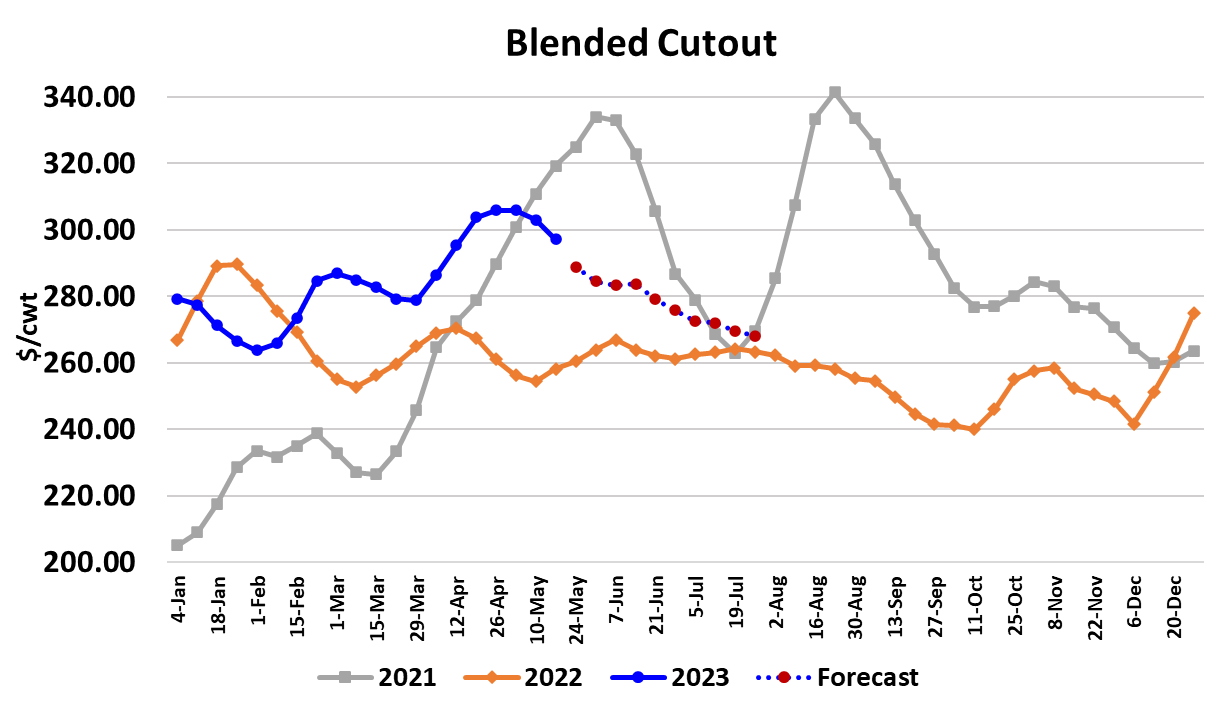

Cattle feeders managed to squeeze a little more out of the packers this week as cash cattle averaged close to $174.85, up about $0.50/cwt. from last week’s average. That is the second week in a row that packers have been unable to pressure cattle prices even though cutout values have been falling. Jun LC futures found it necessary to move higher and narrow the gap between cash and futures for the second week in a row. The Choice cutout averaged 299.80/cwt. this week, the first sub-$300 print in five weeks and down $6.83/cwt. from the week before. The Select cutout fared much better, losing only $0.86/cwt. on the week. Packer margins dropped from around $93/head last week to about $37/head this week. Next week, packers will need to purchase fewer cattle because of the Memorial Day holiday the following week, so perhaps they will have better luck in stepping cattle pricing downward. However, they are still pulling pretty hard on the available cattle supply as this week’s fed kill came in at 504k, which is at least 15k more than what the flow model suggests should be ready to harvest in May. It is hard to believe that many cattle are finishing ahead of schedule, particularly in the North where late winter weather muddied feedyards and slowed gains. No doubt that packers had a Memorial Day orders to fill and that probably factored into the decision to slaughter so many cattle this week, but it could put them at a disadvantage when it comes to sourcing cattle in early June. Cattle availability should be improving as we move deeper into summer and that is likely to get cattle prices back on a downtrend. Jun LC futures looks fairly priced here at around $166/cwt., but there should be bigger beef production and quite possibly softer demand when the Aug LC expiration arrives at the end of summer, so that contract looks about $8-9/cwt. too rich at the moment. It is pretty clear that demand for Choice product is fading now that all of the Memorial Day business is wrapped up. All of the primals moved lower this week, with the rib primal suffering the biggest decline. The next thing on the demand agenda will be to see how well the beef clears out of the retail counter over Memorial Day weekend. If movement is good, then that could lead to some refilling in anticipation of Father’s Day and might slow down the retreat in Choice prices somewhat. If Memorial Day movement disappoints, then the cutouts probably continue to track lower at a steady clip, sending packer margins into the red. However, after Memorial Day the impetus to overkill will be gone and packers can simply cut the kill if demand doesn’t warrant it. That would shift the hot potato into the cattle feeder’s hands as he sees more cattle becoming market-ready, but less interest on the packer’s behalf to process them. The 50s market has finally started to cool some, with this week’s average price close to $190/cwt., down about $10 from the week before. The previous week’s larger kill probably played a role in that as did the fact that carcass weights seem to be heavier than expected. This week’s FI data showed a surprising five-pound jump in steer weights. In the attached chart, that unusual jump in carcass weights makes it look like they are making their seasonal bottom about a month earlier than normal. My guess is that they will work a little lower in the next couple of prints, but then probably start to track above last year by the time June arrives. So the weight data is looking bearish, while cattle availability appears somewhat bullish in the short run. That makes the steady cattle pricing seem appropriate for the moment. Speaking of cattle availability, USDA released a Cattle on Feed report this afternoon that showed feedyard placements during April down 4.2% YOY. That was pretty close to the consensus, so it probably won’t impact the market much, but it does represent the eighth month in a row where placements have been below last year. We are in that phase of the cattle cycle where YOY placement declines are likely to continue for another couple of years. The weekly export data bounced higher this week, but that was probably more of a data anomaly rather than a strong indicator of better export demand. I read international demand for US beef as lukewarm at best right now. Maybe as beef prices work lower in early summer, international interest will pick up, but it is a pretty good bet that 2023 beef exports are going to come in below last year. I have them down 7% and that might not be enough. Another thing that should be on everyone’s radar screen is the fight over the debt ceiling that is going on in Washington. Every so often, our elected officials feel the need to bring the US to the brink of default and this time it seems more serious than normal. If the US does go into default (and that could happen in less than 2 weeks), the financial markets will likely react by devaluing all risky assets and that won’t be good for consumer’s retirement accounts. We could go from feeling fine to everyone feeling a lot poorer in just a matter of days and that wouldn’t be good for beef demand this summer. Both sides in the fight have been saying that a deal will get done eventually, but the make-up of Congress is different this time with more fringe elements who would like nothing more than to blow the system up. That is what makes this event more serious than previous ones. The government may have to shutter some functions due to lack of cash if a deal doesn’t get done and that will affect some of the data flows out of USDA that we depend on for analysis. The major reports like cutouts and cattle prices are likely to still get released, but some of the more infrequent reports might not. Keep your fingers crossed that cooler heads will prevail in Washington. Next week, watch the futures early in the week. If they go red on Monday and Tuesday, that likely will set the tone for a lower cash cattle trade. If they refuse to back down, the cattle feeders might do the same and we could end up with another week of steady trade. I think the mostly likely scenario is a $1 decline.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}