Beef Wrap May 24

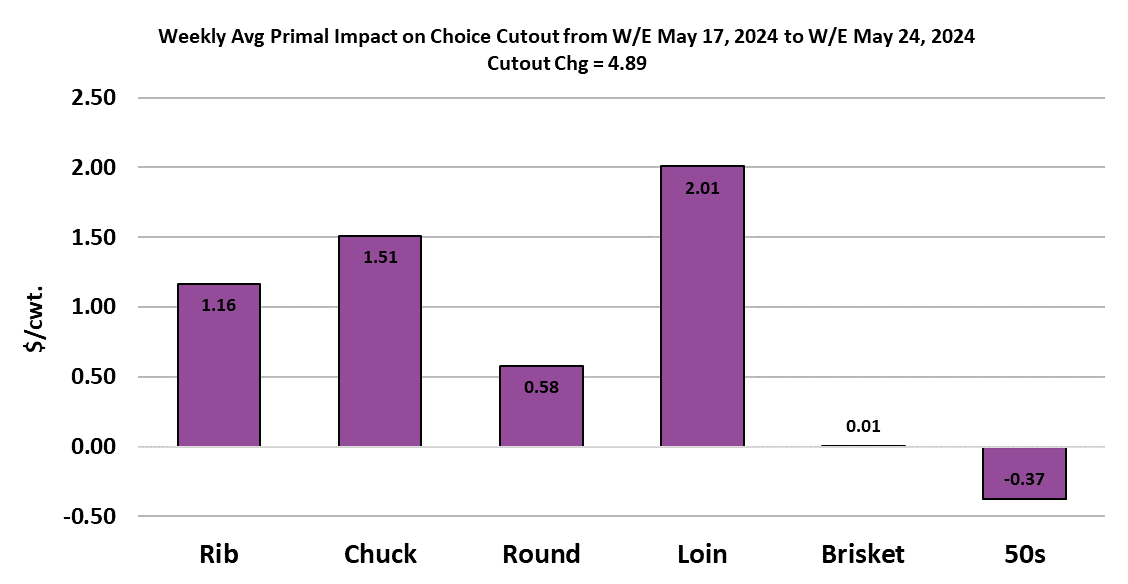

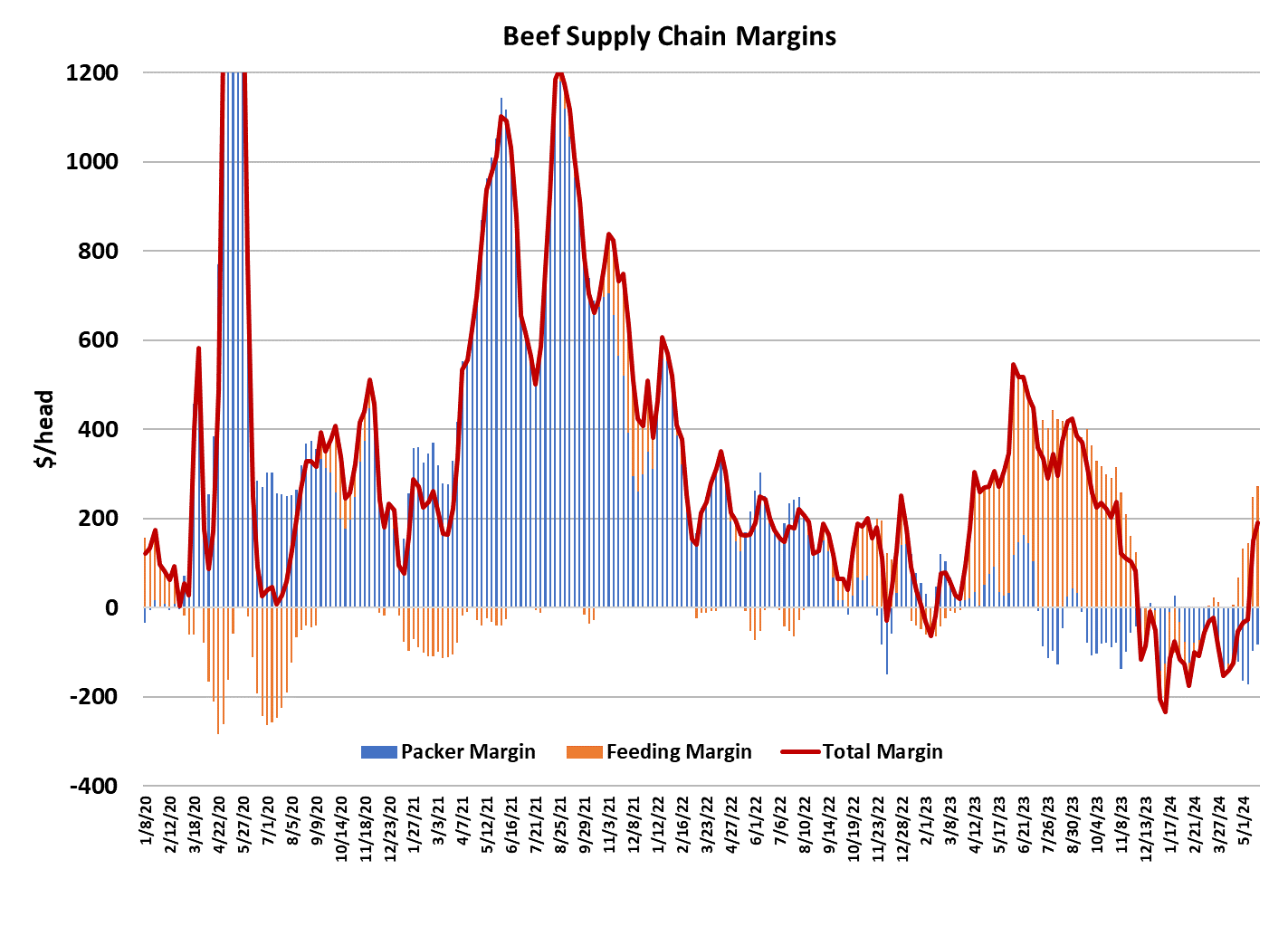

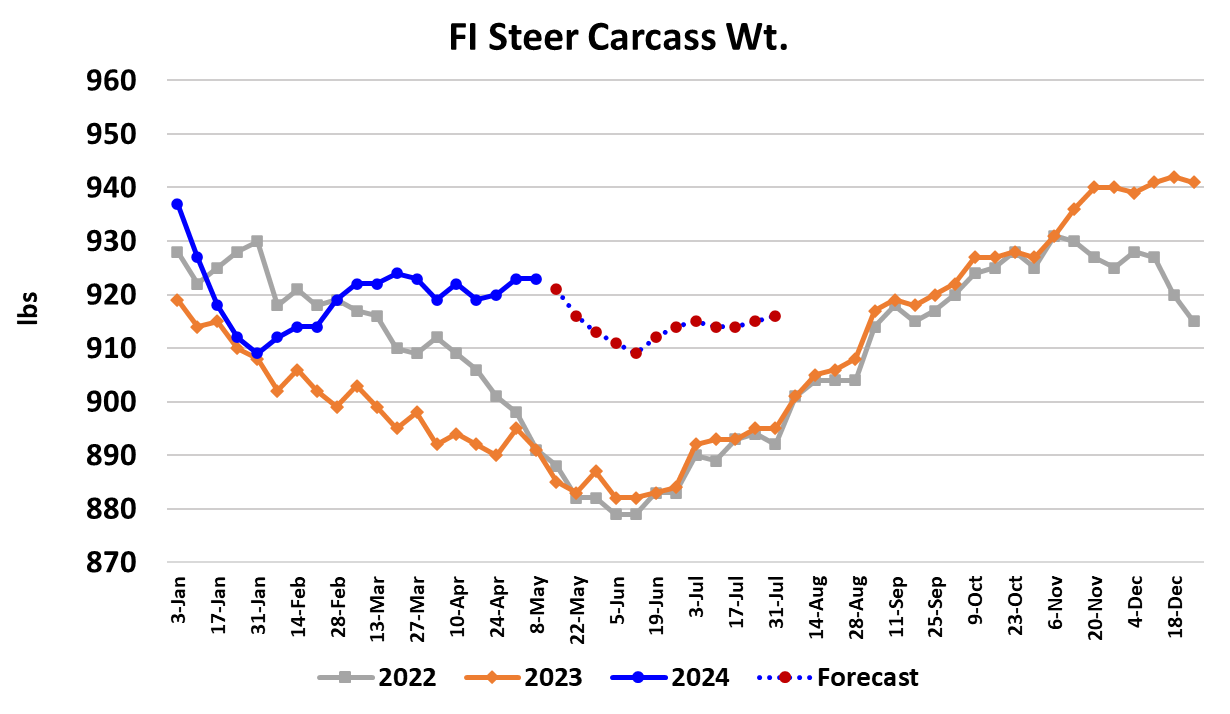

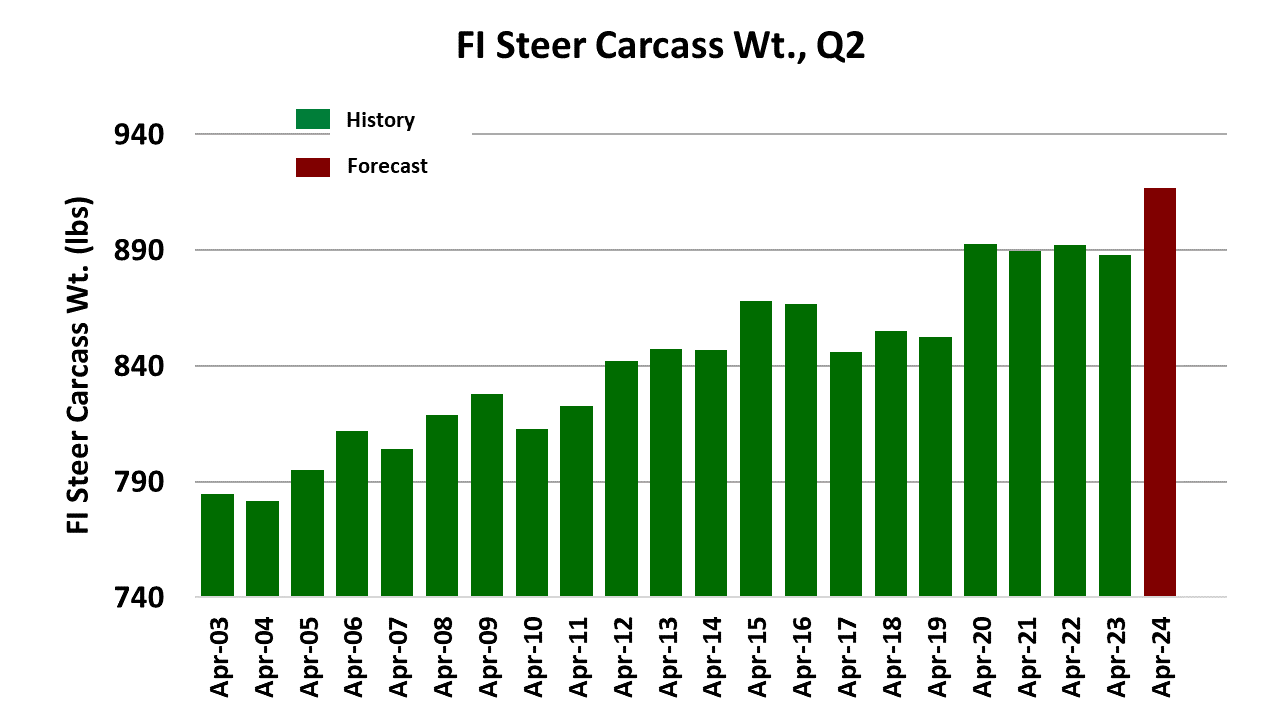

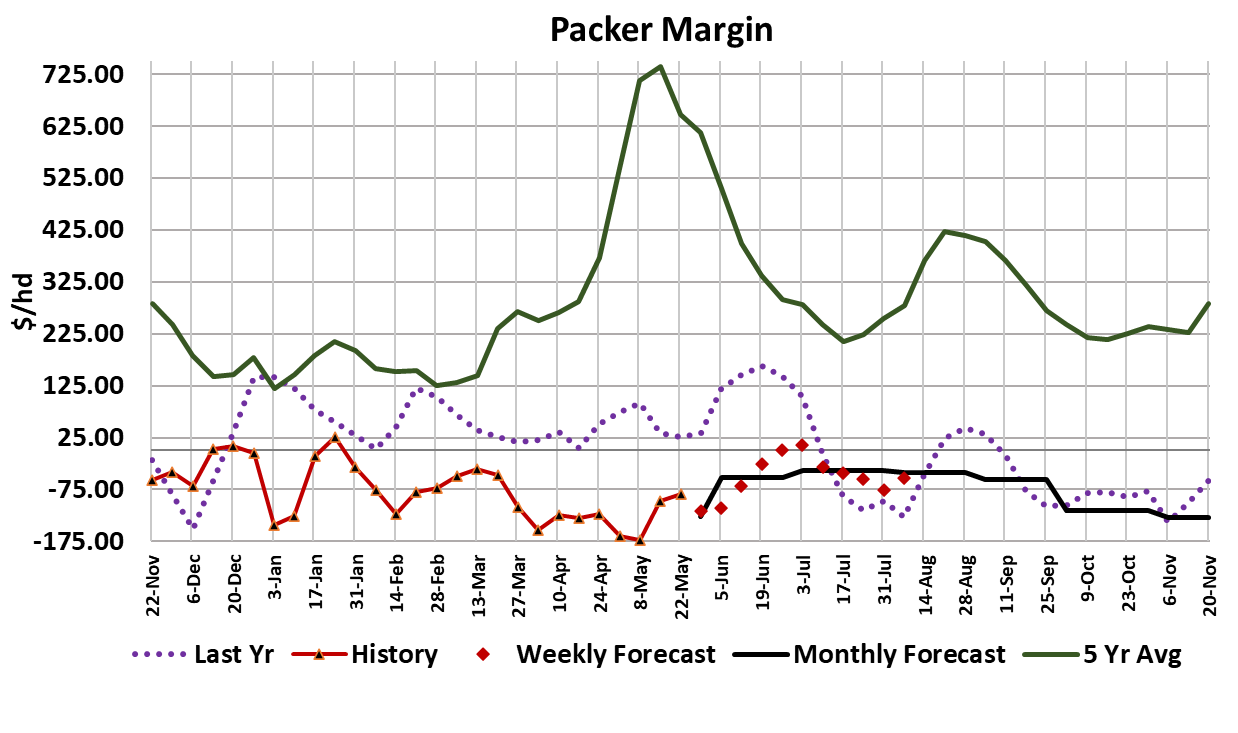

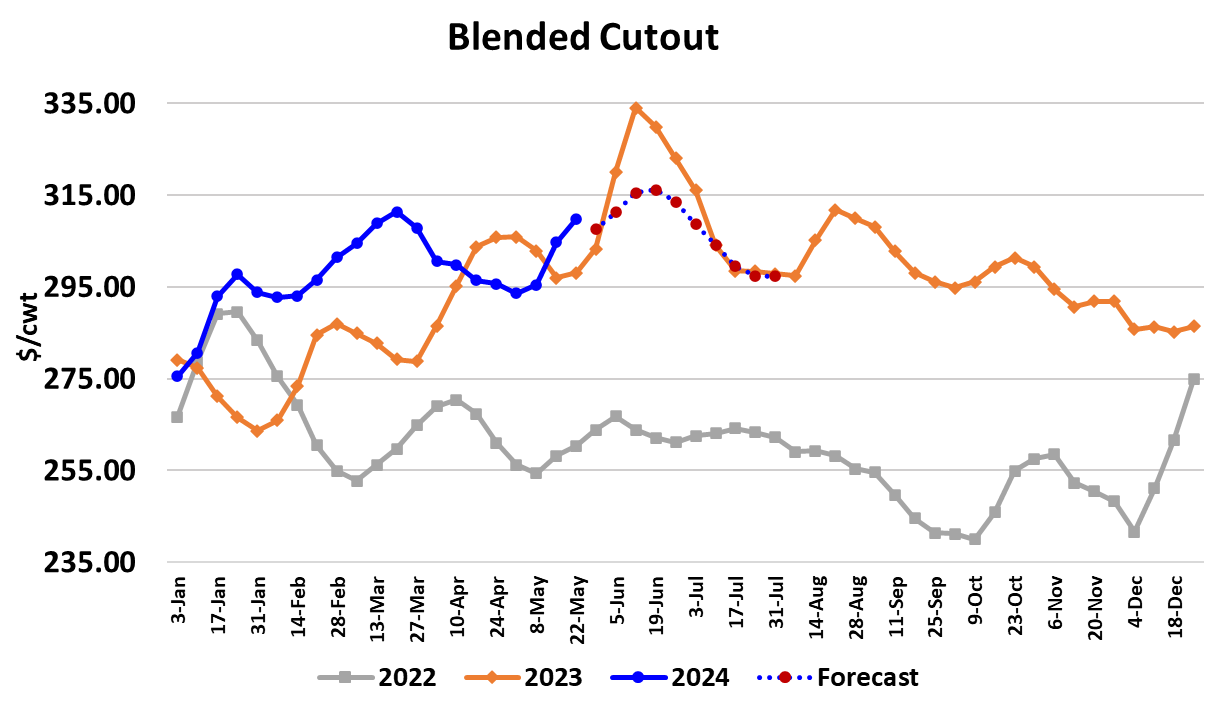

The beef market managed to stay on its upward trajectory for the second week in a row, with the Choice cutout gaining $4.89/cwt. on a weekly average basis and the Select cutout adding $6.48/cwt. The cattle market also posted gains as trade in the South was mostly $1 higher at $187 while the Northern trade was closer to $2 higher at $192. When the five-area average is released on Tuesday, I expect it will be very close to $190, up about $1.50 on the week and a new all-time record high. The fact that cattle prices are higher than they have ever been must come as a huge head-scratcher to the bears who thought that counter-seasonally increasing carcass weights and large on-feed inventories were sure to spell doom for cattle pricing this spring. It seems to me that the counter-seasonal increase in carcass weights had the opposite effect because it meant that cattle feeders were intentionally adding days on feed, thus allowing them to slow down marketings, making it harder for packers to fill out their kill schedules each week and that gave cattle feeders the upper hand in weekly price negotiations. At some point however, the desired days on feed will be achieved and that should cause some slippage in cattle feeders’ leverage because the cattle supply chain will need to operate normally once again in order to prevent an unwanted backup. We will know that point has been reached when cattle feeders start to exhibit a sense of urgency to move cattle and that is usually characterized by cash trade that happens earlier in the week and often at lower money. As long as cattle feeders are holding out until late on Friday to trade cattle, there is no sense of urgency to market. This week, the cash trade was largely complete by Thursday afternoon, but that might be more a function of wanting to get the cattle trade done early so that participants could take a long holiday weekend. Further, packers signaled that they were willing to pay at least steady money on Wednesday’s Fed Cattle Exchange, which cattle feeders correctly read as “they need the cattle”, thus moving the leverage meter in the cattle feeder’s favor. As one might expect, all-time record high prices come with some pretty good cattle feeding margins. I calculate this week’s feeding margin near $270/head. It has escalated rapidly over the past month or so. Packers too saw margin improvement this week, with the packing margin now only $82/head in the red. The combined margin has moved sharply higher over the past couple of weeks as buyer interest in beef finally ignited after weeks of indifference earlier in the spring. The important question now is whether or not that improved demand from beef buyers will persist into June or if it will peter out now that all Memorial Day needs are met. The cutouts did appear to waffle near the end of the week, but I want to see how the cutouts perform next week post-holiday. The weather forecast for Memorial Day itself looks great for the Western and Central sections of the US, but not so great for the population centers along the East Coast. If movement at retail is strong over the weekend, we could see a bump in the cutouts early next week on fill-in buying. Next up is Father’s Day, which is also a pretty big beef holiday. It is pretty safe to assume that dad prefers a steak over hamburgers on his special day. The fundamental forecast has the cutouts continuing to work a little higher over the next few weeks toward a peak in late June, but I recognize that beef demand could let up after Memorial Day and so there is more downside risk to the forecast than risk that it will over-perform. The fed kill clocked in at 496k this week, up 6k from the week before. Next week, packers will likely run a big Saturday kill to help make up the ground lost on Monday’s holiday, but the weekly fed total may still only be about 445k. As we move into June, I’m expecting weekly fed kills to run in the 495-505k range. Steer carcass weights declined one pound in this week’s data release, but that is little consolation given that carcass weights are running 32 pounds heavier than last year at this time. Fed beef production was up about 5% YOY this week and has been running 4-5% higher since early April. The lion’s share of that increase is coming from carcass weights. In spite of all that extra production, the blended cutout was up 4% YOY this week, so it is clear that demand is pretty strong at present. Whether or not demand will remain at this level is still an open question, but several macro indicators seem to point to consumers coming under increasing financial stress. Beef is not usually the first thing that consumers give up when their financial picture darkens, but it is definitely on the list of possibilities. USDA provided the results of their most recent Cattle on Feed survey today and it showed April placements down 5.8% YOY and total on-feed inventories now about 1% below last year. That was mostly in-line with analysts’ expectations, so there shouldn’t be a strong reaction when the futures open on Tuesday. Speaking of futures, the Jun live cattle contract has been on a tear lately, moving higher in 8 of the last 9 trading days. Just two weeks ago traders were thinking that $176 was a fair value for cash cattle at the end of June, but that has now been revised upward to $184. Next week, it will be important to watch the cutout values coming out of the holiday. If they can hold steady or advance, that is a positive sign that may signal a seasonal boost in demand and perhaps higher cutouts in the near future. If they struggle however, it could mean a return to the lethargic environment that was in place back in late April/early May.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}