Beef Wrap May 17

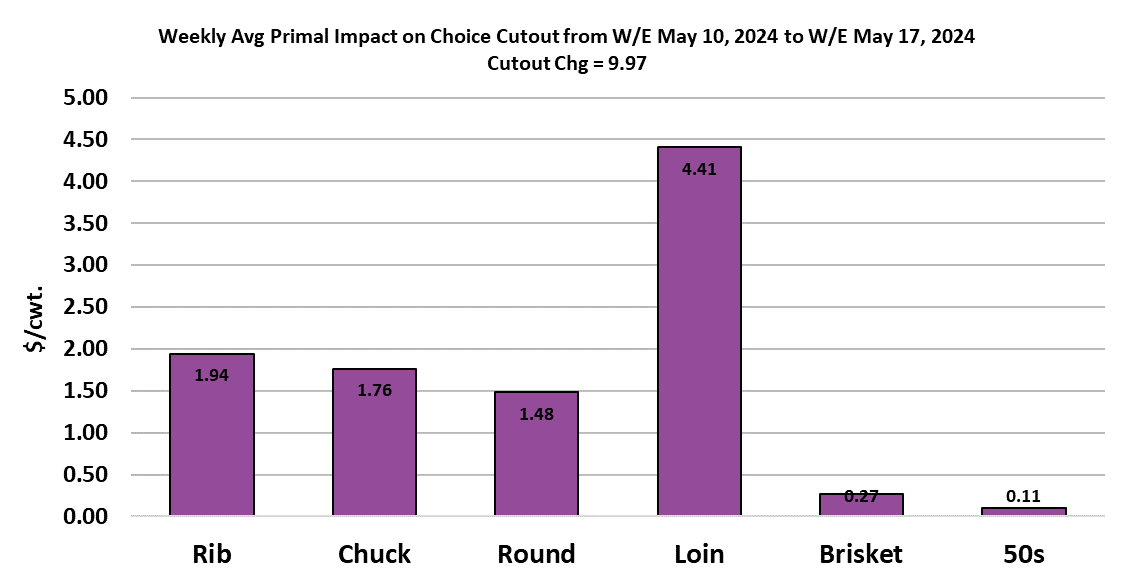

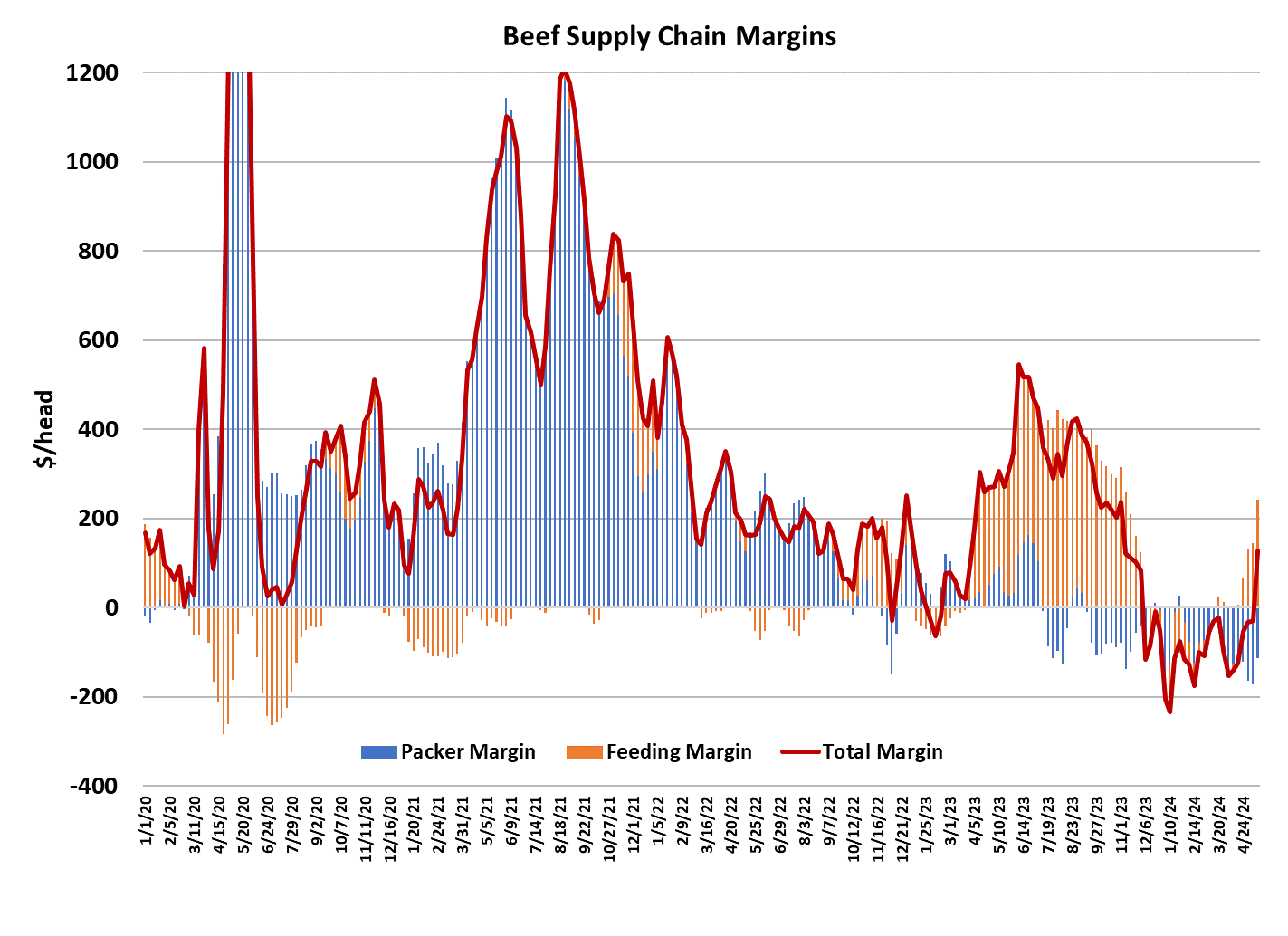

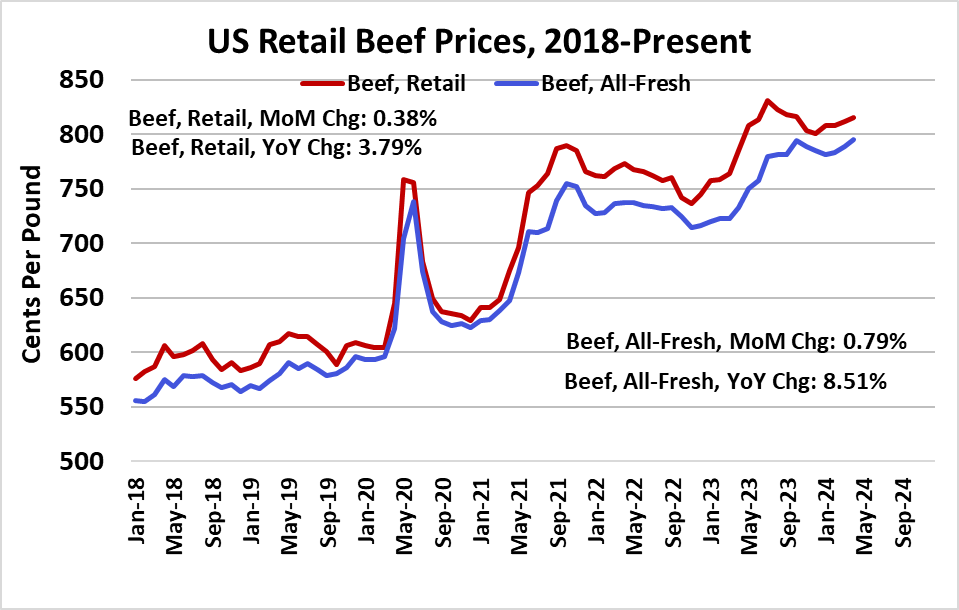

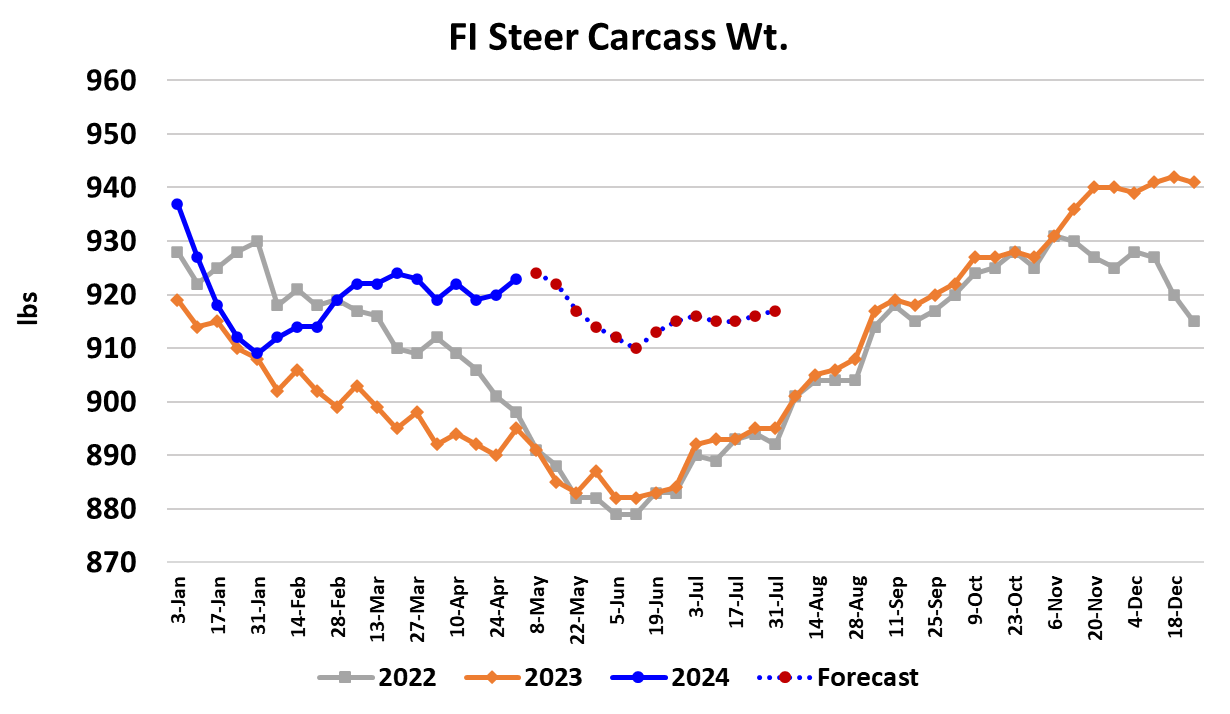

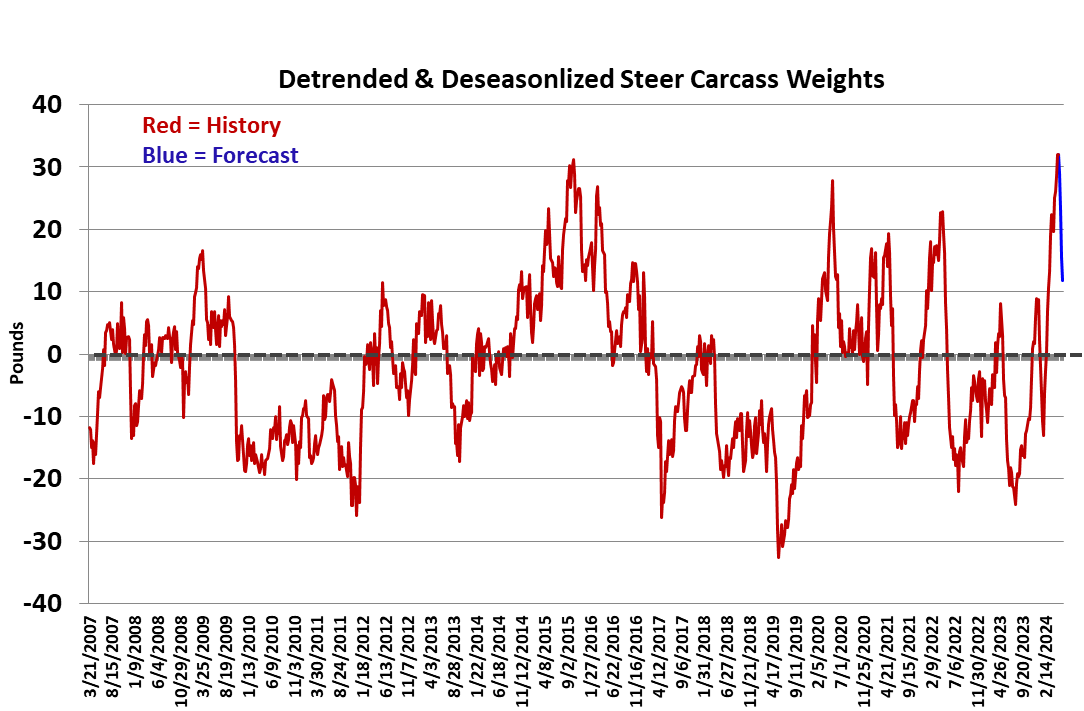

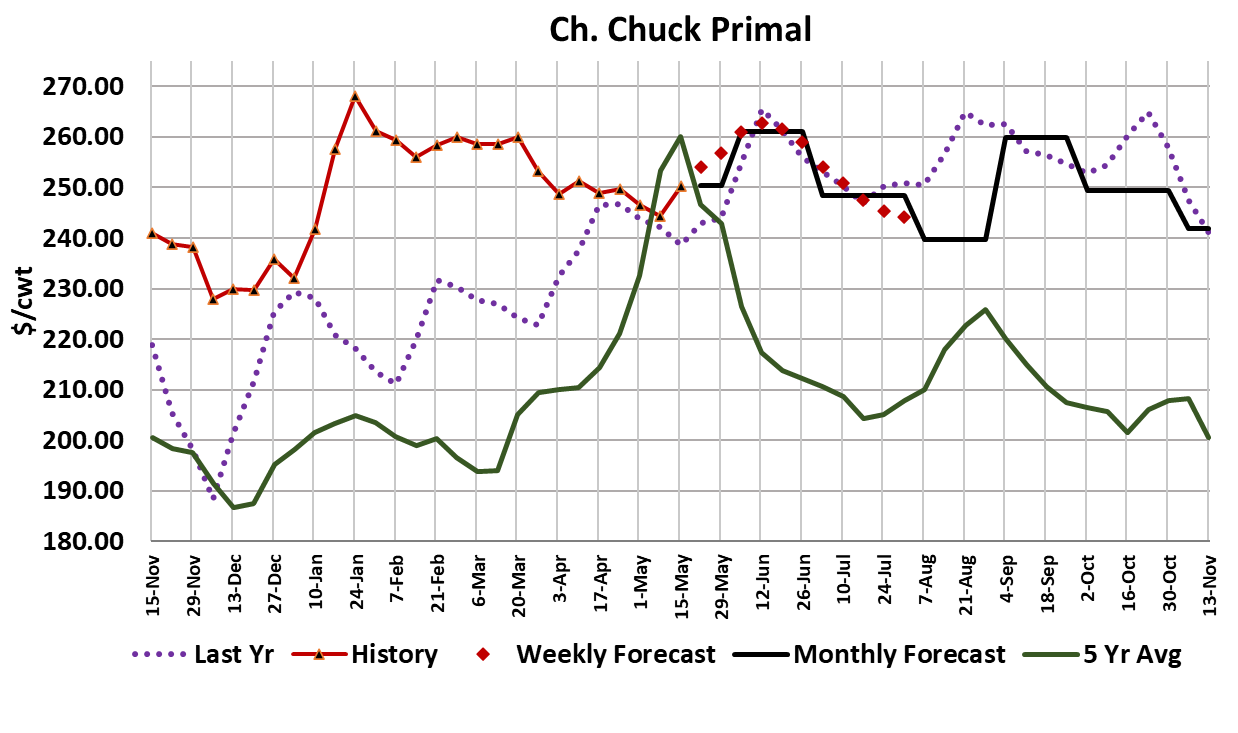

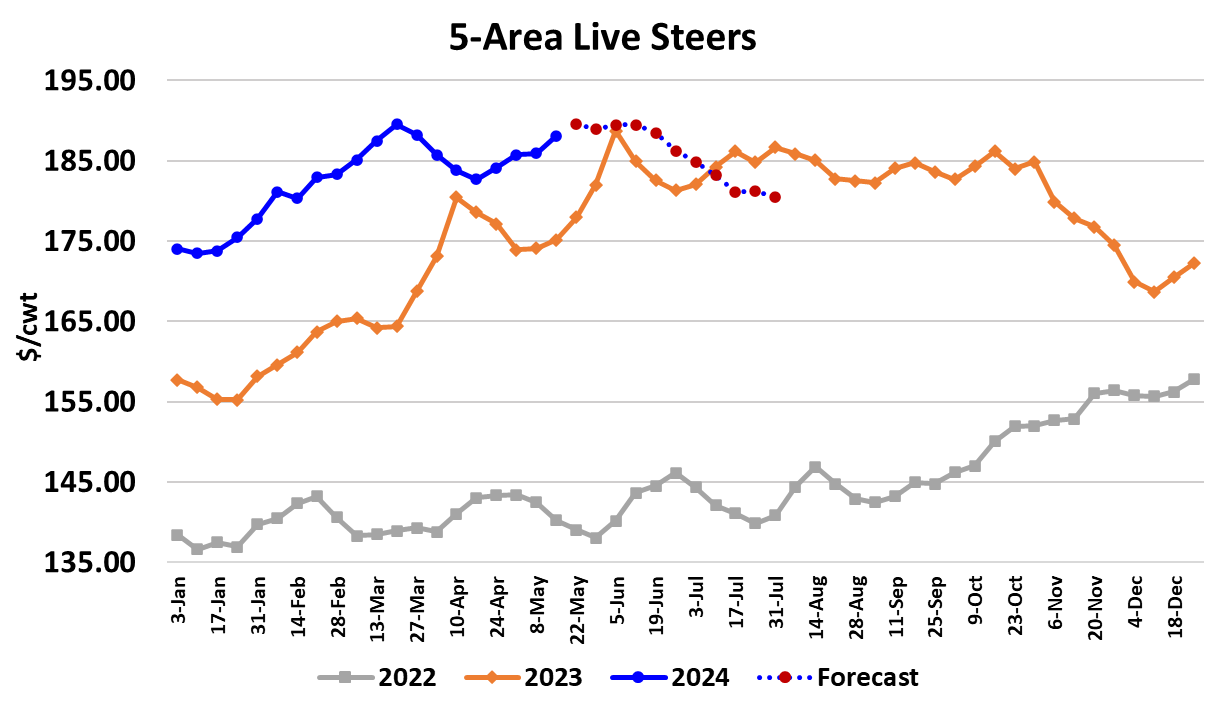

This week’s theme in the cattle and beef complex was “better late than never”, as the cutouts rocketed higher just two weeks before the Memorial Day holiday. There was speculation that the buying was driven by packers’ announcing their intention to limit this week’s kill and that caused beef buyers to quickly jump off of the sidelines. The strength of the rally was impressive, with the Choice cutout adding $9.97/cwt. to average $306.74 and the Select gaining $5.79/cwt. on a weekly average basis on its way to $293.84. Of course, as cattle feeders watched beef prices soar, they wanted their share of the proceeds and refused to trade cattle until packers ponied up another $2 in the live market. Cash prices in the Southern Plains should average close to $186 when all of the data is tallied, and in the North the average should be close to $190. That should put this week’s 5-area live price very near $188. Packer margins improved, now only about $100/head in the red, up from -$175/head the prior week. Still, packers can’t be very happy about negative margins at this point in the calendar. They did pull back on the kill some, as fed slaughter totaled 482k, down 22k from the week before. Next week’s harvest is likely to be limited by light kills on Friday and Saturday as packers allow workers to enjoy a long holiday weekend. The weekly kill could still come in close to 500k, if packers run hard at the beginning of the week, but my guess is that it will be somewhere in the 480-490k range. One thing a packer doesn’t want to do is run out of product when prices are surging. If the weather is good over the holiday weekend, then there will likely be significant fill-in buying early in the first week of June. The interesting thing about this week’s rally is that it was spread across most of the carcass, rather than concentrated in the middle meats. True, loins and ribs were the biggest gainers, but there were also strong improvements in the chuck and round primals. That tells me that it wasn’t just the steak buyers that were sitting on the sidelines earlier this month. Of course, the question that comes to the forefront now is whether or not this rally will quickly reverse once the buying surrounding the holiday is done. Just judging by the progression of daily prices this week, it looks like it might have some staying power. There are two more big beef holidays that follow Memorial Day and this rally might spur buyers cover their needs a little further in advance for those holidays. When consumers head to the store to get their grilling items for next weekend, they will probably be looking at near record high pricing. This week USDA reported that retail beef prices in April rose 0.8% from March and now sit 8.5% higher than at this time last year (for the all-fresh series). That all-fresh price series takes into account beef sold on feature, so the relative dearth of beef features this spring could be what is driving the average price up so much. We have heard executives at companies such as Walmart and McDonald’s comment lately about how the lower-income consumer is under pressure and is scaling back on their food spending, so the upcoming holiday weekend will be a good test of that theory for the beef complex. This week’s carcass weight data showed another counter-seasonal increase in steer weights, up three pounds and now 28 pounds heavier than last year. The de-trended and de-seasonalized carcass weights notched an all-time high this week and that would normally be very bearish for cattle prices since it suggests that feedyards have fallen way behind on their marketings. Given that cattle prices advanced for the fourth week in a row and are now pressing against the all-time high, about the only conclusion that makes sense is that carcass weights don’t matter at this point in the cattle cycle where animal numbers are shrinking and thus producers are compensating for fewer animals by making each one a lot heavier. We saw the same phenomenon back in 2014-15, the last time that numbers were cyclically tight. Once we get beyond Memorial Day, front-end cattle supplies should be sufficient to fuel fed kills in the 500-510k range, but packers may only go there if they get some degree of margin relief. Next week USDA will provide another Cattle on Feed report and while the consensus average for April placements isn’t available yet, it is expected to somewhere in the area of 6% lower than last year. I’m expecting a little bigger drop, perhaps 8% lower, YOY. That would leave total on-feed inventories as of May 1 down 1.2% from last year. My guess is that placements will continue to run below last year for much of the balance of 2024. That means that cattle availability will get significantly tighter late in the year and into 2025. As long as demand doesn’t fall apart between now and then, then there is a good chance that beef prices will track above last year in the final months of the year. This week’s sharp price gains won’t do much for international interest in US beef and exports are expected to remain tepid. Next week, everyone will be watching to see if the cutouts can add to their recent gains. If they do, that bodes well for pricing in early June.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}