Beef Wrap May 31

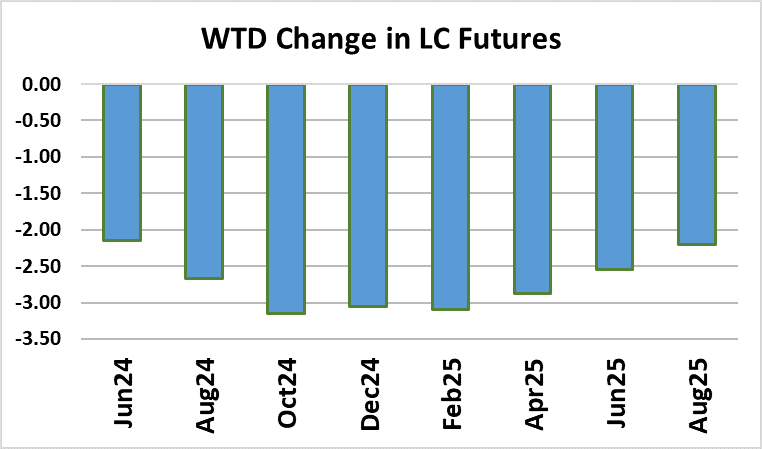

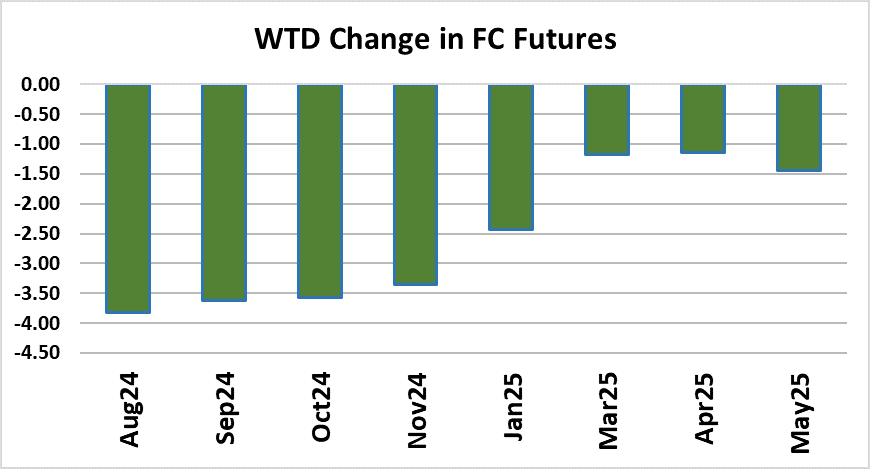

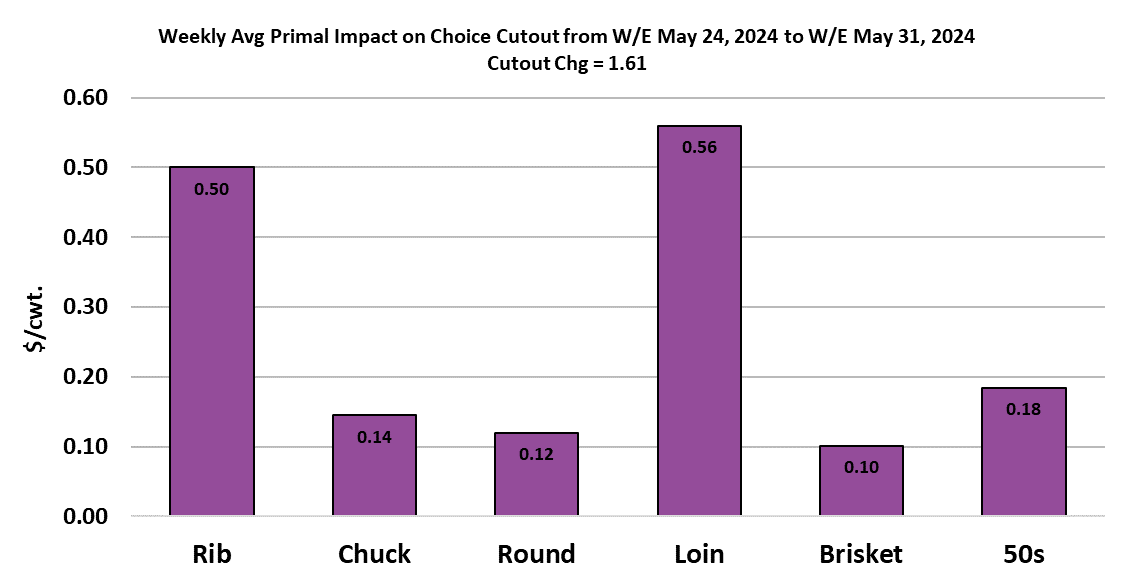

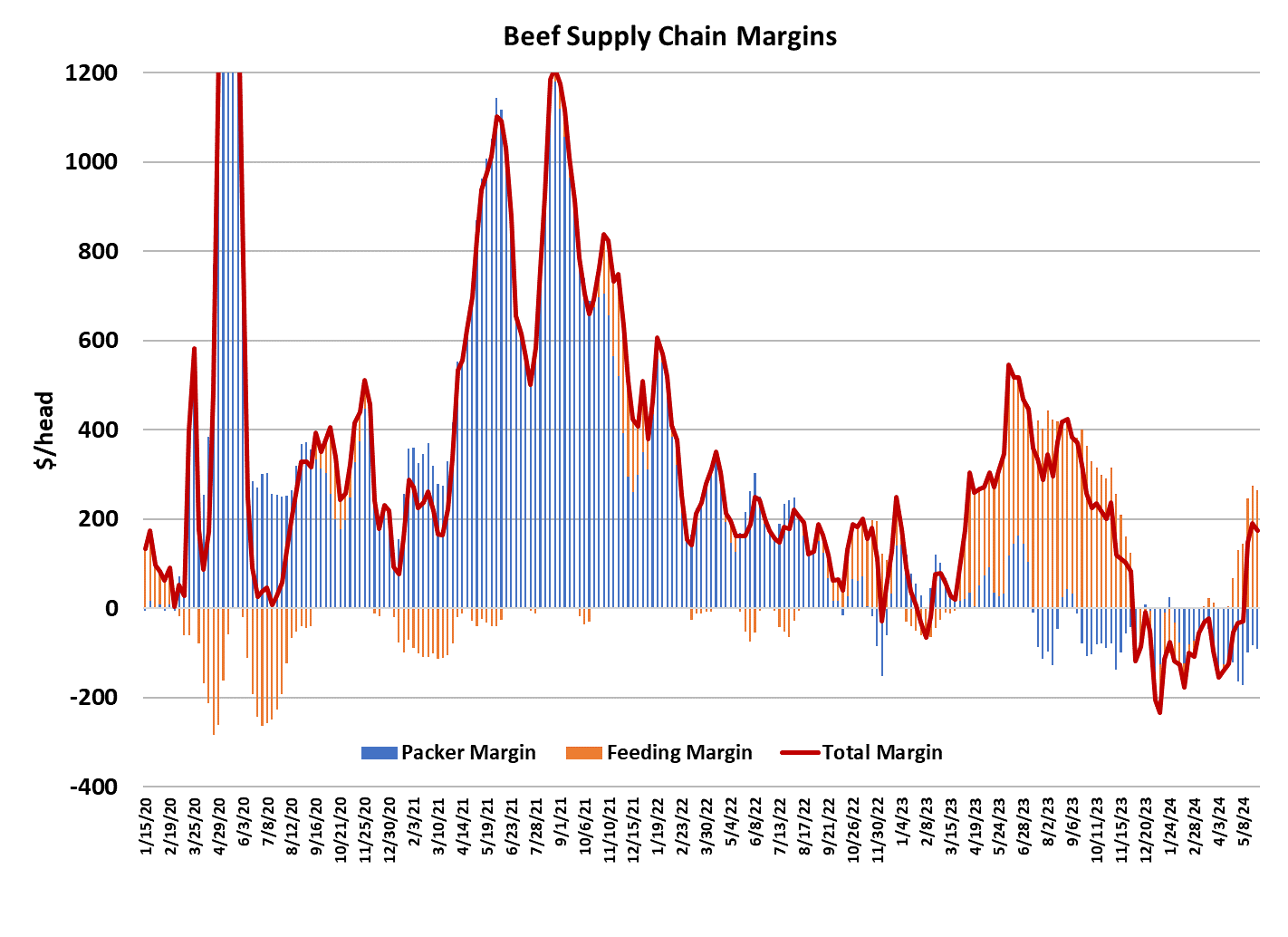

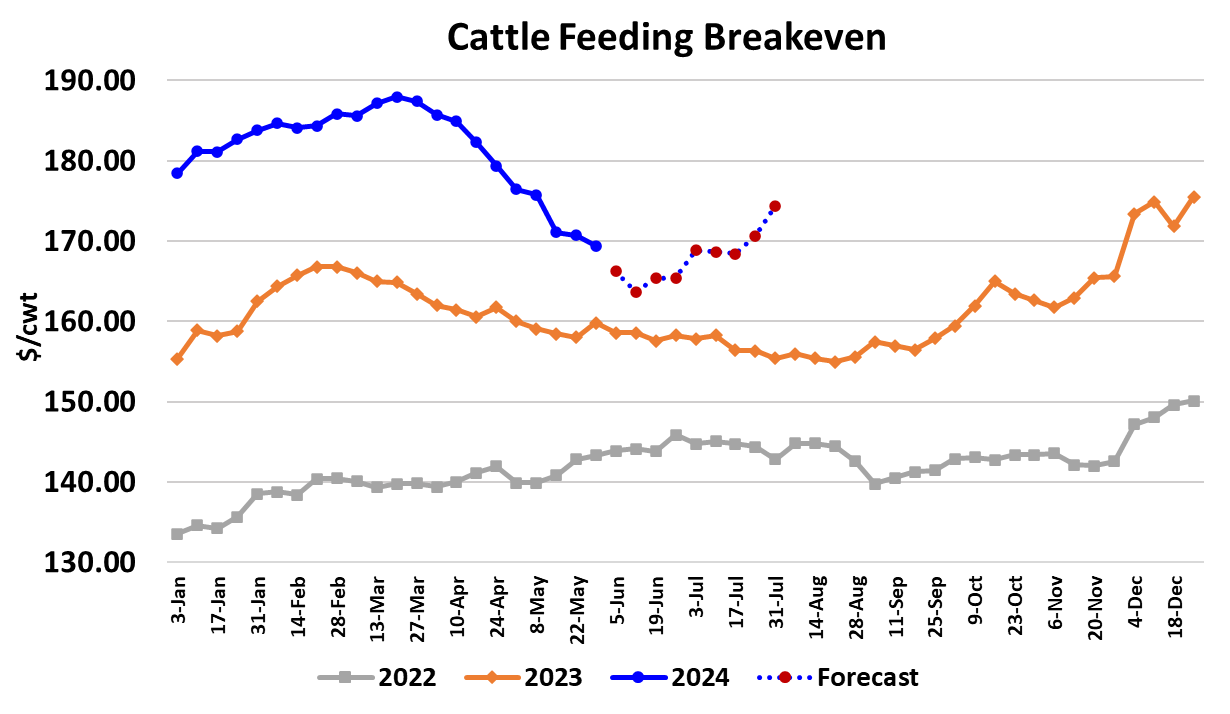

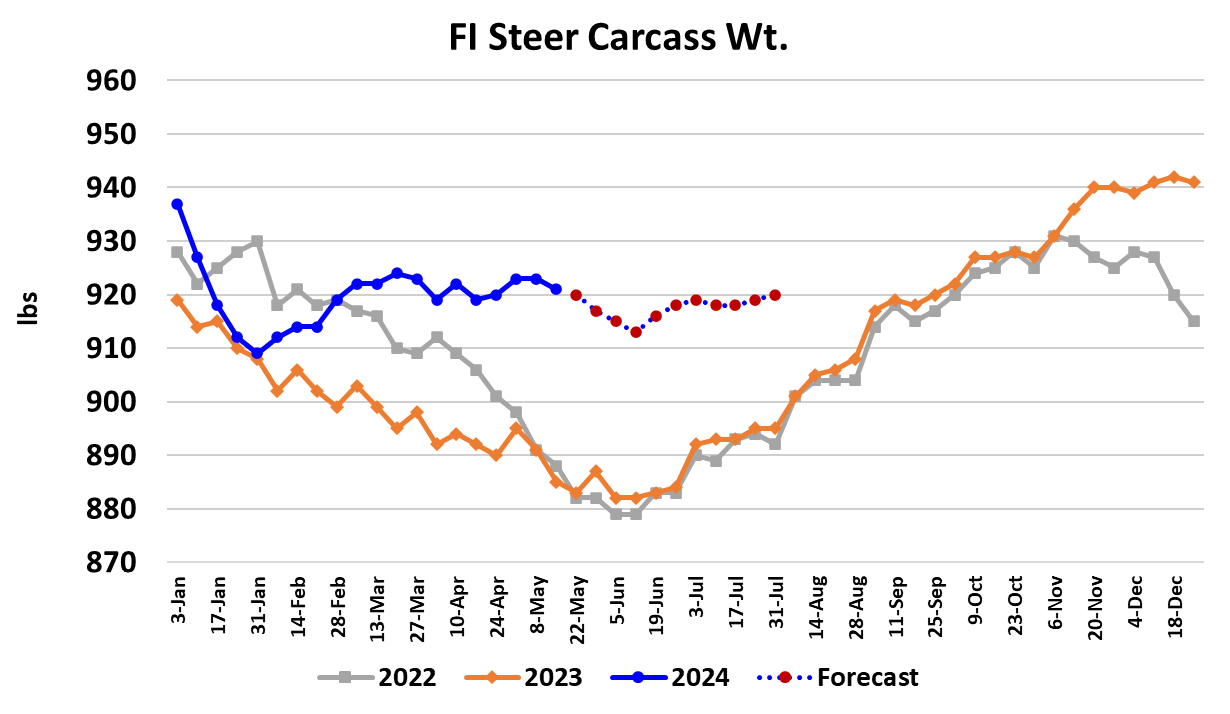

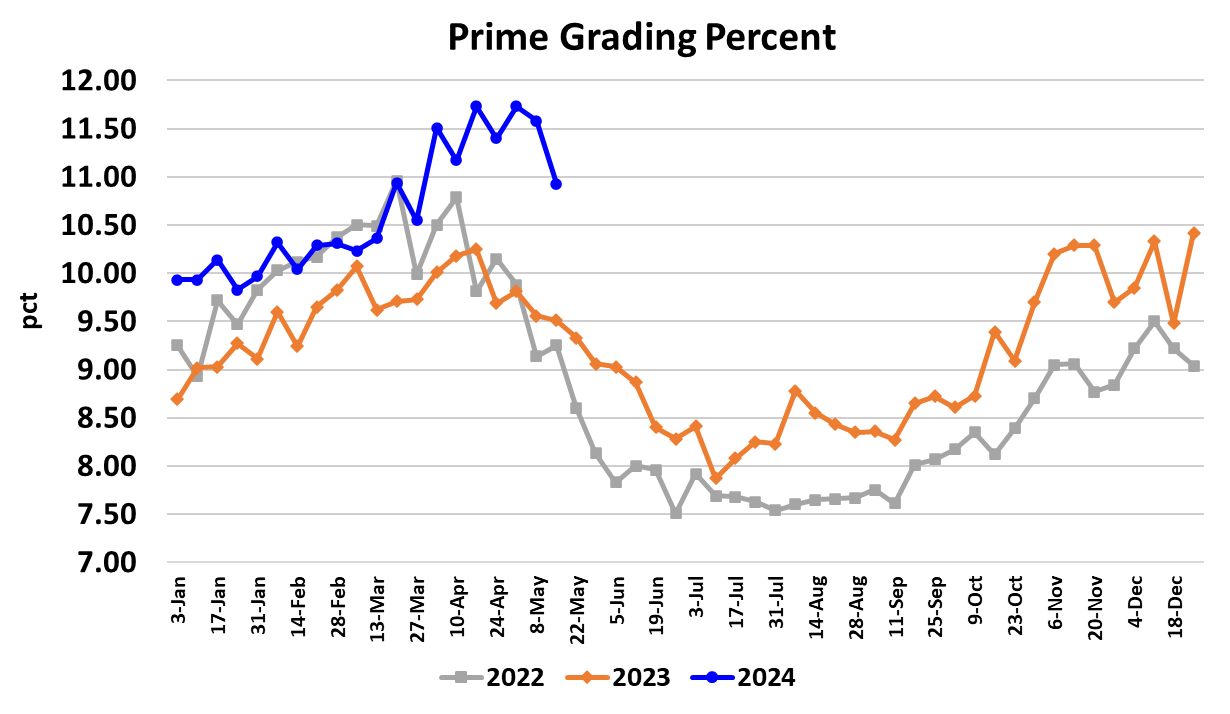

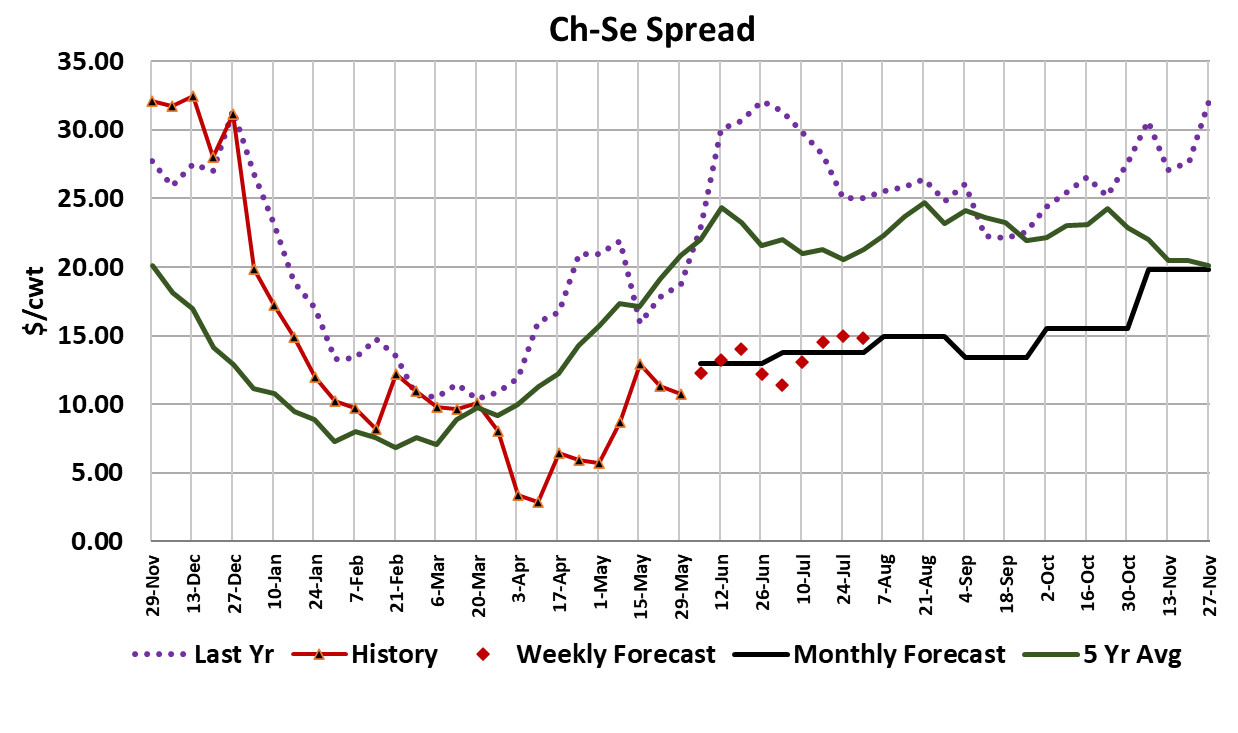

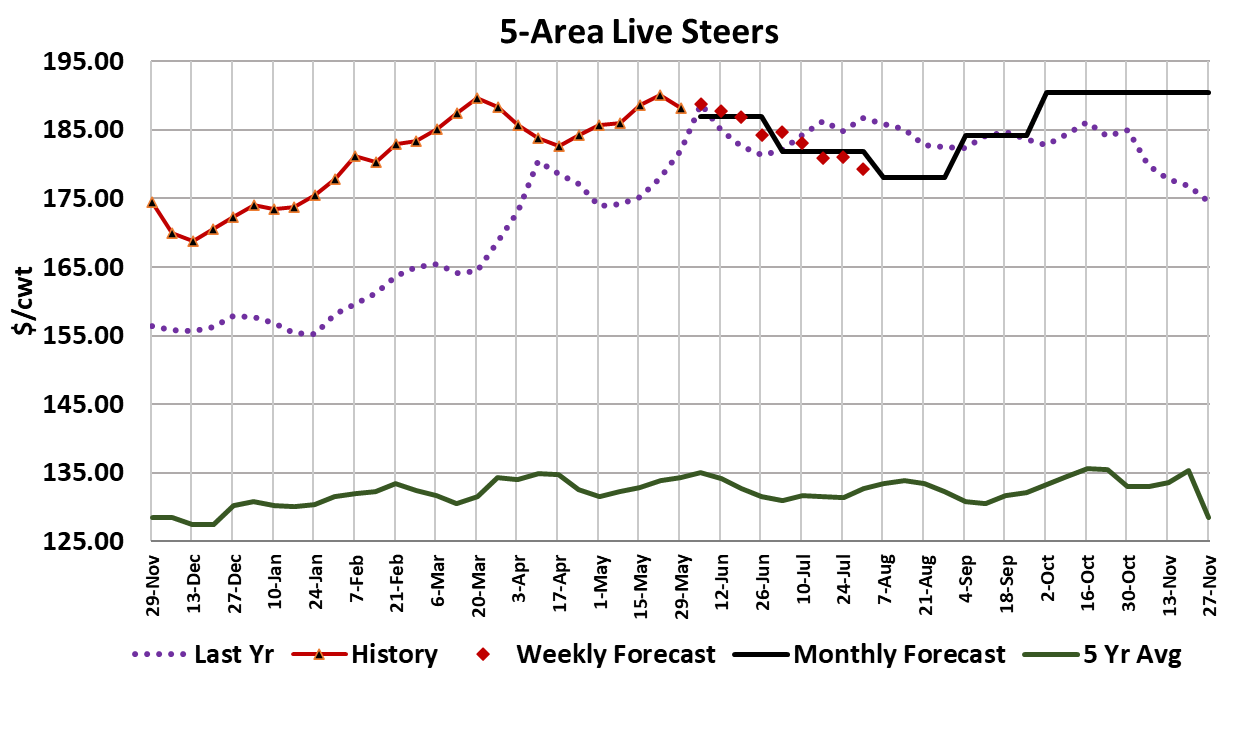

The cattle market took a turn lower this week as trade in the South was established at $186, down $1 from last week and live trade in the North was close to $190, which was down $2-3 from the week before. That should put the five-area average at close to $188 for the week, which would be $2 lower than the record-setting $190 level posted last week. Live cattle futures came out of the gate surprisingly strong on Tuesday following the long holiday weekend, but on Wednesday news surfaced that China had de-listed JBS’s Greeley, CO plant after finding traces of ractopamine in products the plant had shipped. That was all it took to send the futures lower and they continued lower for the next two days, with most-active Aug losing a little over $2.50 on the week. The Greeley plant delisting won’t have a material impact on beef exports because if JBS needs to fill orders for China, they can easily accomplish that from one of their other plants. It seemed like futures traders were just looking for a reason to sell after the cash market had posted a record high the week before and the China story provided that. To be sure, it isn’t unusual for cash cattle prices to decline as we move into summer, so that seasonal tendency probably played a role as well. In addition, we often see cattle prices follow breakevens, which have been trending lower since March. However, my model suggests that the decline in breakevens has almost run its course and will soon turn higher—a result of strengthening feeder cattle pricing that occurred in January. If you recall, last summer cash cattle prices were amazingly stable, holding in a tight range around $185 from July through October. In the summer of 2022, cash cattle prices followed a wave-like pattern, increasing for 4-5 weeks and then decreasing for a similar time frame, but the general trend was higher. The experience of the past couple years makes me wonder if the cattle market will post a significant break this time around, especially a $10 break like the Aug futures are currently implying. The cutouts performed decently coming out of the holiday week, with the biggest gains early and then some small losses toward the end of the week. On a weekly average basis, the Choice cutout gained $1.61 in moving to $313.35 and the Select cutout added $2.21 on its way to $302.54. All primals saw modest price gains, which suggests that the price increase was more a function of the short kill tightening up supplies rather than a new surge of demand. Speaking of demand, the combined margin made its first move lower since late March, which might indicate that the market is nearing the end of this demand upcycle. Movement out of retail over the holiday weekend was reported as better than average, so that provides some hope that Father’s Day and Independence Day will follow suit. The fundamental forecast has the cutouts moving a little higher between now and Father’s Day, but I think there is considerable downside risk to that forecast. Packer margins registered -$90/head this week, a little worse than the week before. If packers can keep the cash cattle market heading lower, then margins should get better over the next few weeks. Cattle feeding margins are very healthy, near $265/head, and poised to get even better during early June as breakevens continue lower. This week’s FI carcass weight data showed steer weights down 2 pounds from the week before, but more-timely data makes it look like the FI weights are going to struggle to get much lower over the next few weeks. We have now reached the point in the calendar where weights typically bottom and turn higher. Given the atypical movement of weights so far this year, it is unclear whether or not that seasonal checkpoint is going to hold this time around. The current forecast has weights remaining in more of a sideways pattern for much of the summer rather than making the traditional V-bottom and heading higher. There should be sufficient market-ready cattle to fuel fed kills in the 500-510k range during June, but poor packer margins might keep actual kills somewhat below that range. This week’s fed kill clocked in at 434k, down 60k from the week before and obviously shortened by the holiday. Next week, I’d look for something larger than 500k as packer refill the pipeline. The percentage of carcasses grading Prime has been record high this spring, but posted a big drop this week. Still, that percentage is well above last year at this time. Cattle producers are answering the call to produce more high-quality beef, which requires lengthening the feeding period and raising carcass weights, both of which have been ongoing this year. With more animals grading Prime and Choice, there are fewer grading Select, and the Select grade is what typically gets ground up to replace 90s. As a result, the Choice-Select spread is unusually narrow for this time of year and may stay that way through the balance of 2024. Beef is shifting from an everyday consumable to a luxury item. In fact, producers may have already gone too far in their quest to produce high grading beef, leaving the lower end of the market too tight. The 90s market added another $5 this week, averaging just over $355. Father’s Day is typically thought of as a steak holiday while Independence Day is more of a hamburger and hot dog affair. My guess is that the 90s won’t post a significant decline until after we get beyond July 4. Next week, look for packer margins to improve as cutouts could add a little to this week’s gains and cheaper cattle will come to slaughter. The futures seem determined to force the cash market lower, but cattle feeders may have other thoughts. Look for a steady cash cattle trade.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}