Beef Wrap May 21

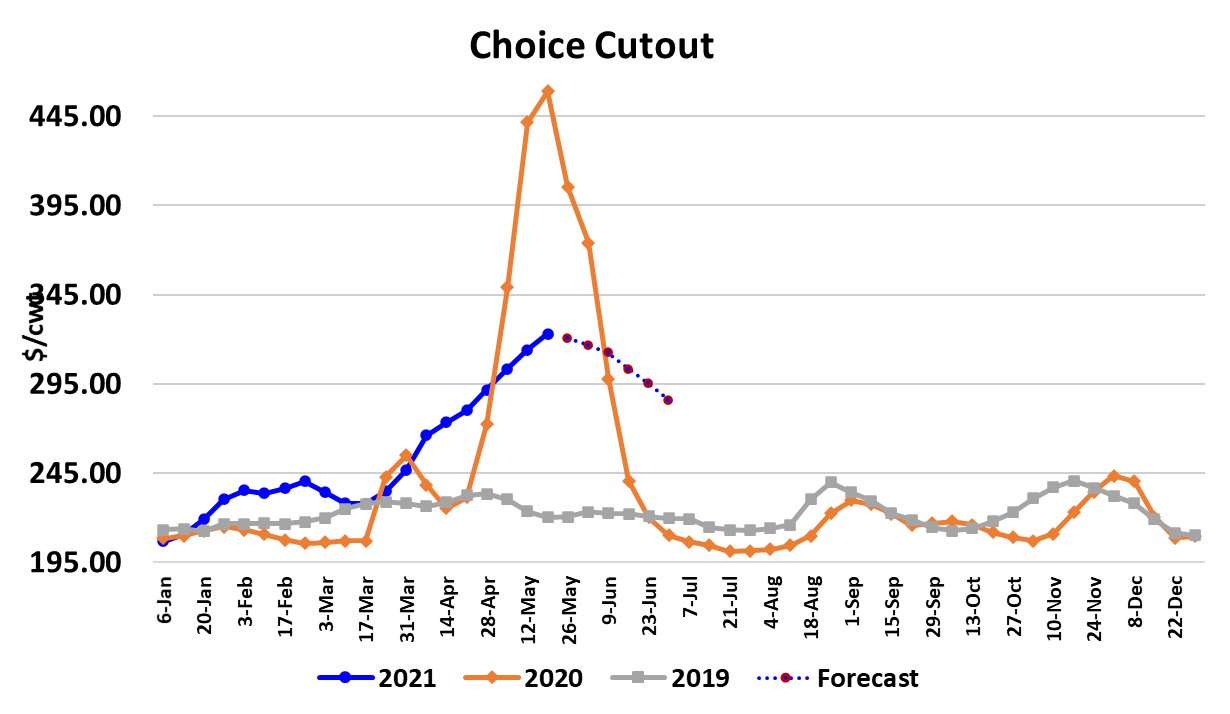

Cash cattle prices were essentially unchanged from last week,

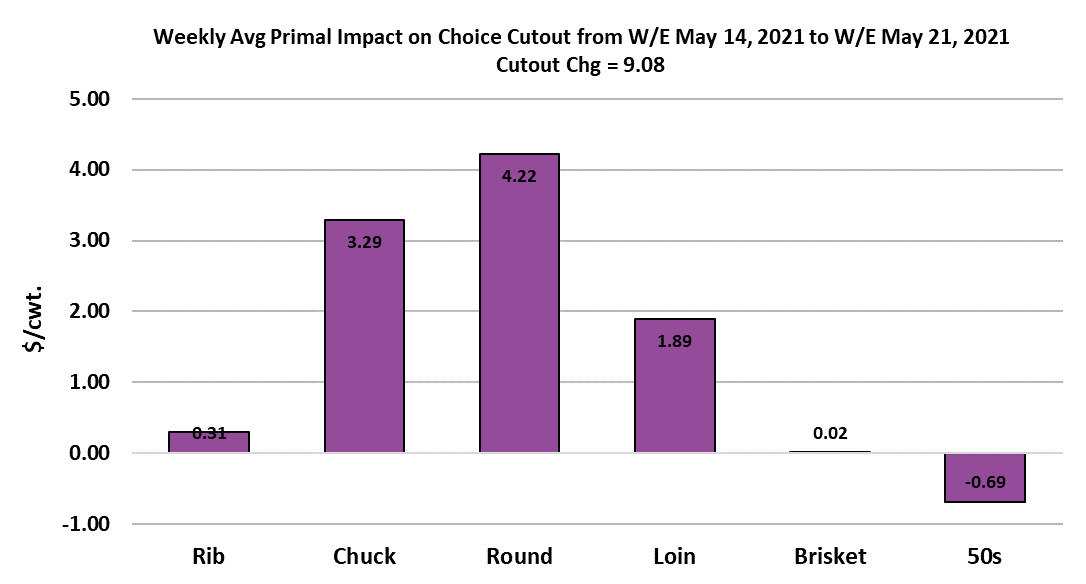

averaging $119.71 on the week. The cutouts, however, kept pushing

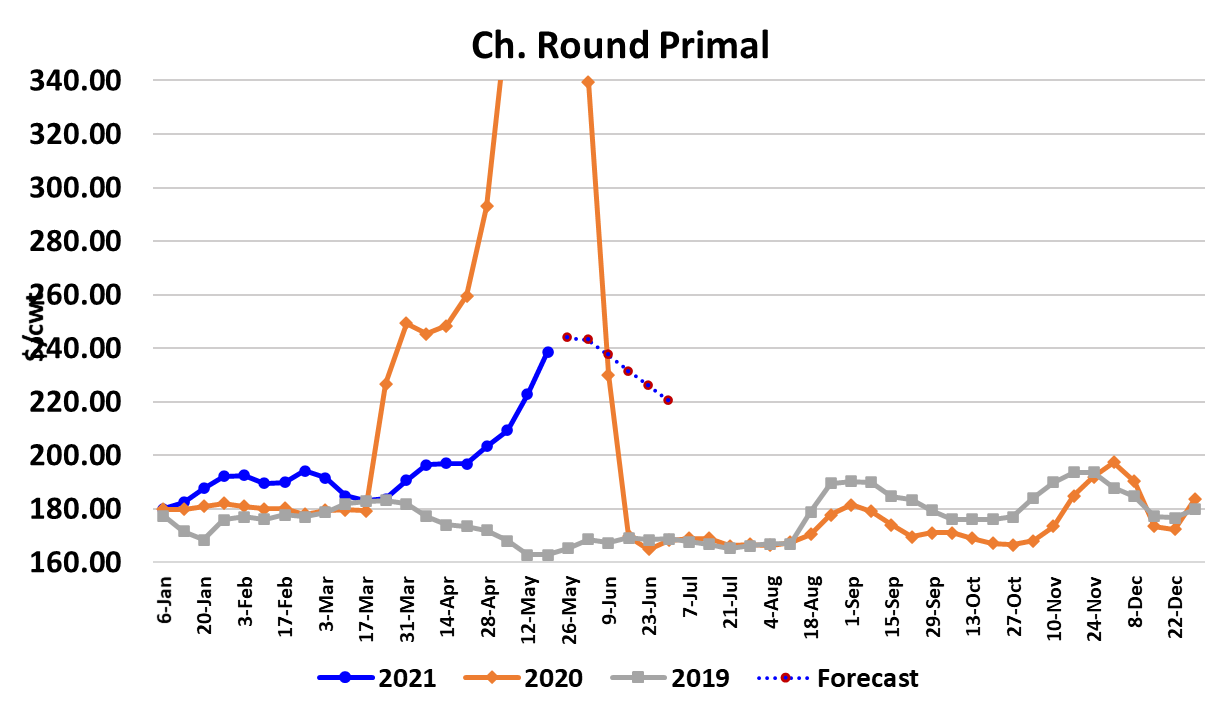

higher, with the Choice adding a little over $9 and the Select up about

$4.60. There are many who are expecting a sharp retracement in the

cutouts now that all of the Memorial Day business is wrapped up, but

I’m not one of them. I think we could see a little softness in the middles,

but keep in mind that Father’s Day follows closely on the heels of

Memorial Day and that is also a big middle meat holiday.

Whatever it is that has driven the end cuts to such high levels is almost

certainly not related to Memorial Day and thus it doesn’t seem

reasonable to expect a big collapse there just because the holiday has

passed. I think that buyers had just better get used to paying a lot more

for beef on an ongoing basis. The labor shortage in packing plants

means that beef production will not be able to expand much beyond

current levels and that situation is likely to persist for a long time. Some

say that once the additional unemployment benefits expire, that will

force more workers back to the job. I don’t really think that the

unemployment benefits are playing as big of a role as people think.

Instead, I believe the pandemic forced workers to look for alternative

employment and many located work in other areas that they found

more enjoyable than their old jobs. I guess almost any job on the

planet would be more enjoyable that working in a packing plant. The

same applies to those who used to work in foodservice, except that the

jobs they found weren’t necessarily more enjoyable, but they paid

better. So, bottom line is that the pandemic caused a huge re-think in

careers for many people, leaving packing plants and restaurants out in

the cold when it comes to the cheap labor they had enjoyed for

decades.

There is only one solution to that problem and that means raising

wages to attract people back into these jobs. When industries pay their

workers more, they have to charge more for their products. That means

more expensive beef coming out of packing plants and more expensive

meals at restaurants. When the price of goods or services rise, people

consume less of them, so this also means a smaller beef industry and a

smaller restaurant industry is the likely long-run result of this labor

pinch. Because the beef industry is comprised of many stages (cowcalf, stocker, feedyards, packers, retailers, etc), coordination between

the stages is accomplished via price signals. So, right now the packing

segment is having a labor problem and it is trying to send the price

signal downstream to the feedyards and cow-calf sectors to slow down

the flow of cattle. Today’s COF report makes it look like cattle feeders

have not yet heeded that signal because placements came in well

above expectations and that just sets the stage for more financial pain

in the feeding sector over the next 6 months or so.

Hopefully, those cattle feeders that did place heavily also hedged by

selling the deferred futures. Anyway, the bottom line is that we have a

supply chain here that is not very well coordinated at the moment and

that means resources will not be used efficiently and also likely

increases the price volatility within the supply chain.

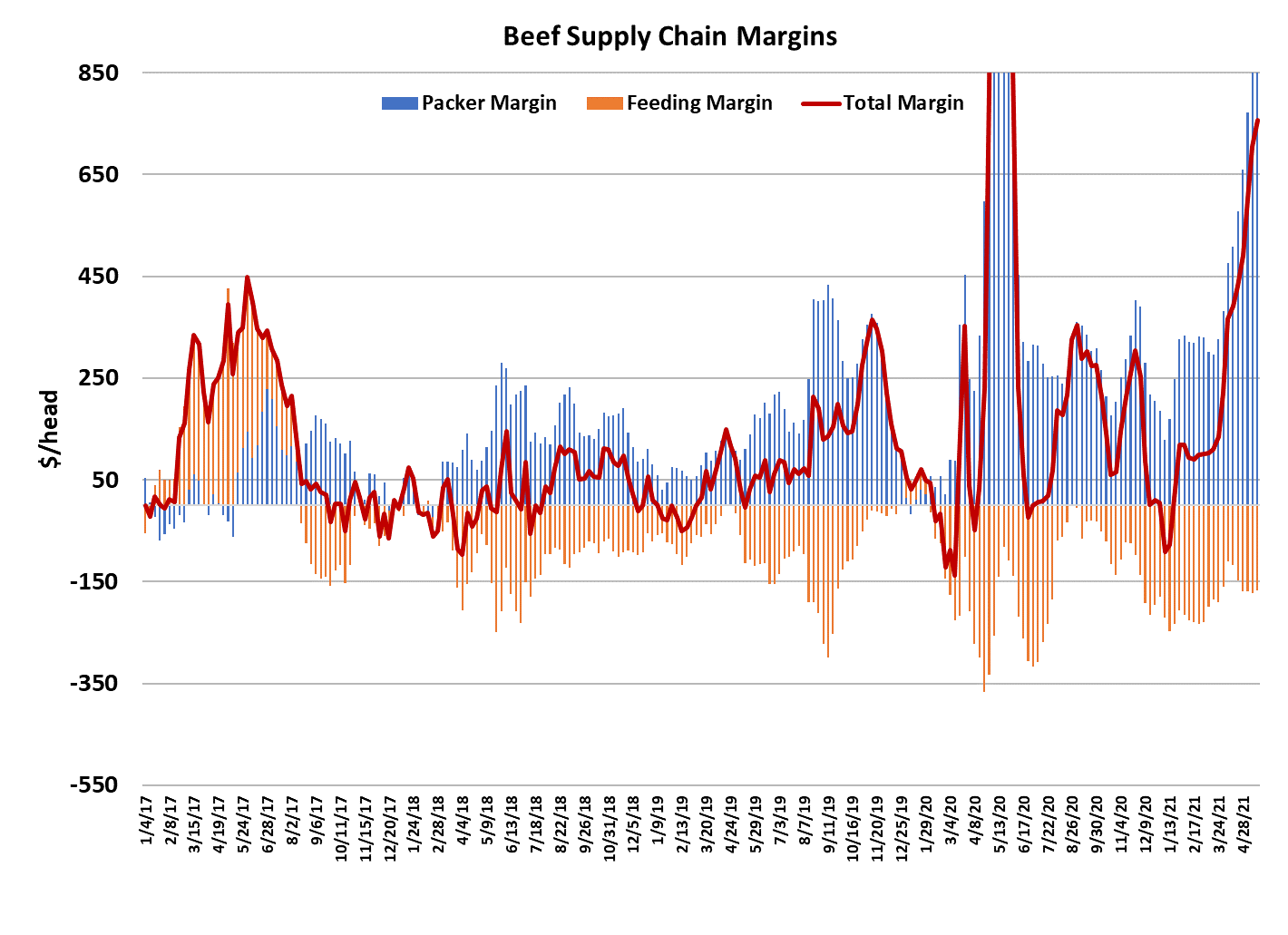

Packer margins this week clocked in at $928/head, up about $50/head

from last week. Packers responded by putting together a very large

Saturday kill by current standards and the weekly total steer and heifer

slaughter came in at 533k. I’d say that represents a practical upper

bound on how many fed animals packers can kill in a week under

current conditions. That big kill may be enough to cool down the

cutouts next week, especially now that Memorial Day purchasing is

done. Cutouts may soften a bit, but I wouldn’t expect them to show

huge declines. Corn prices are well off their highs now and the

weather looks favorable for growing in the near-term. Hopefully, that

will take some of the “commodity supercycle” buying out of the meat

markets in the next few weeks.

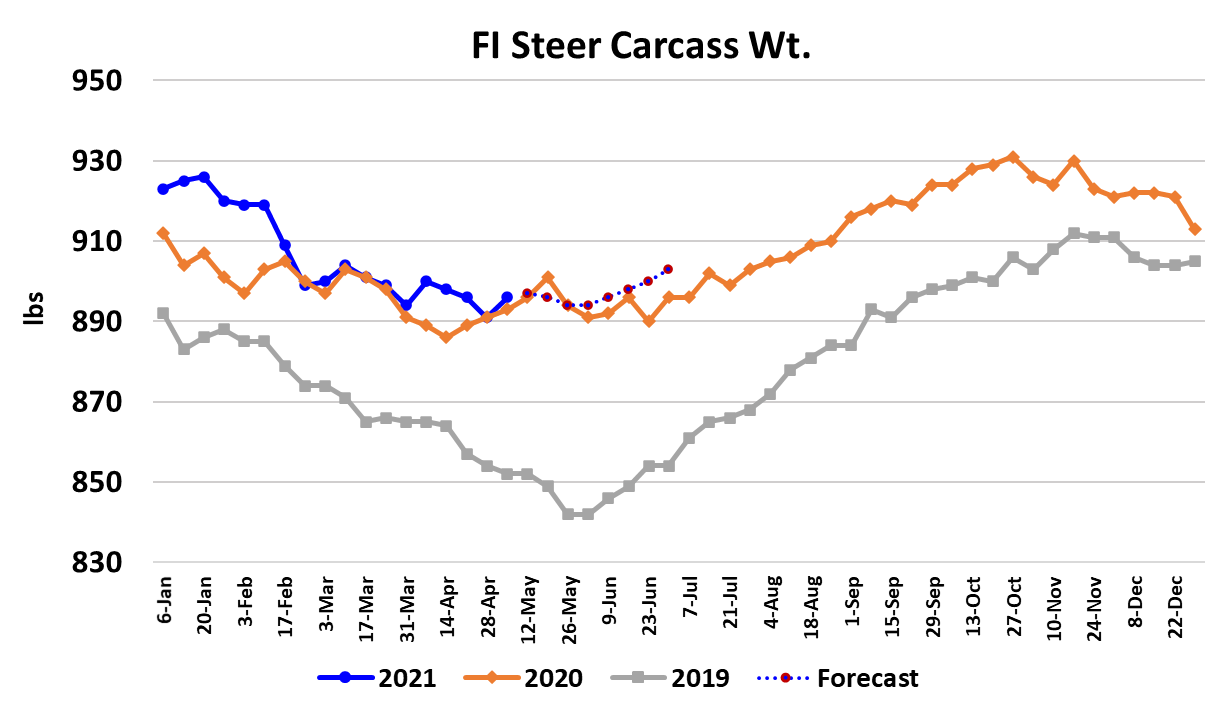

Carcass weights do not look very good at present. Steer weights were

reported up 5 pounds this week and they should be declining

seasonally. The DTDS is at high levels. All of this suggests cattle are

not getting marketed on time and thus some backlog is beginning to

develop. The demand side of the beef market continues to look very

robust and the combined margin chart below indicates that we are still

in the upward phase of this very strong demand cycle. Life is rapidly

getting back to normal in the US and people want to celebrate. Beef is

naturally a part of that and they are buying it with both hands,

regardless of the price. This “back to normal” boost in beef demand

will fade at some point, but may last through most of the summer.

Retailers are rapidly raising beef prices, but that doesn’t seem to

matter in the current euphoria. Keep in mind that retail prices are very

sticky—they don’t come down nearly as fast as they go up and so if

demand falters once we get retails up to very high levels, we could see

problems moving product. I think that day is at least 2 months down

the road, but it is probably coming at some point. Next week, watch for

a modest softening in the cutouts led by the middle meats and keep an

eye on those carcass weights because they are looking ominous once

again.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}